Agarwood Chips Market Size, Share, and Growth Forecast 2026-2033

Key Market Highlights

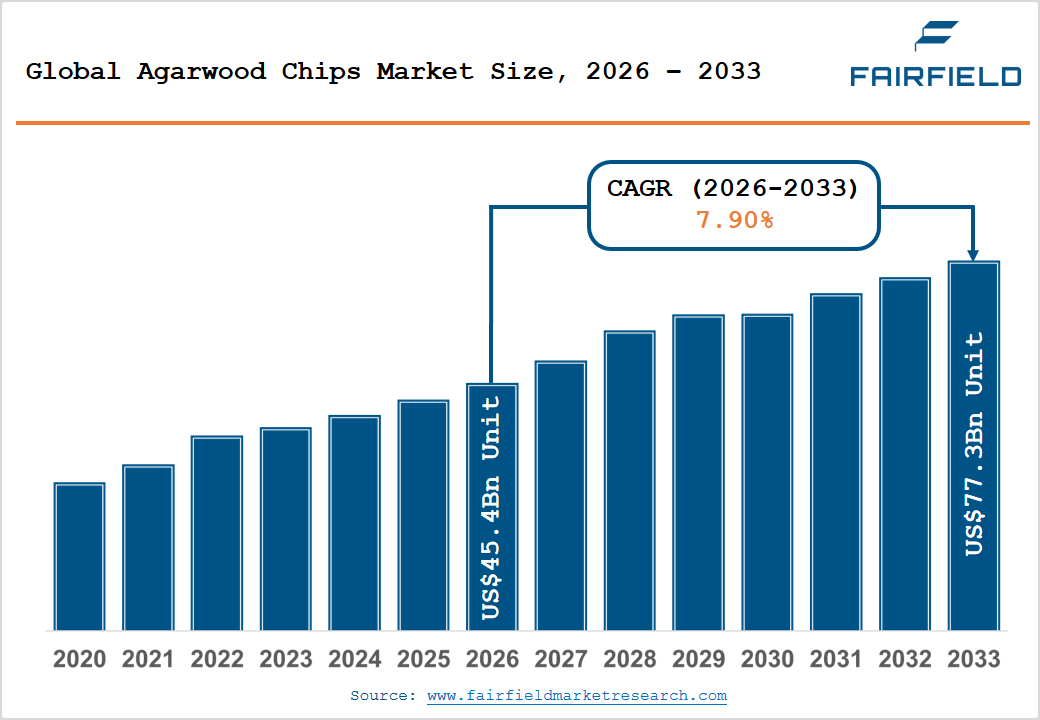

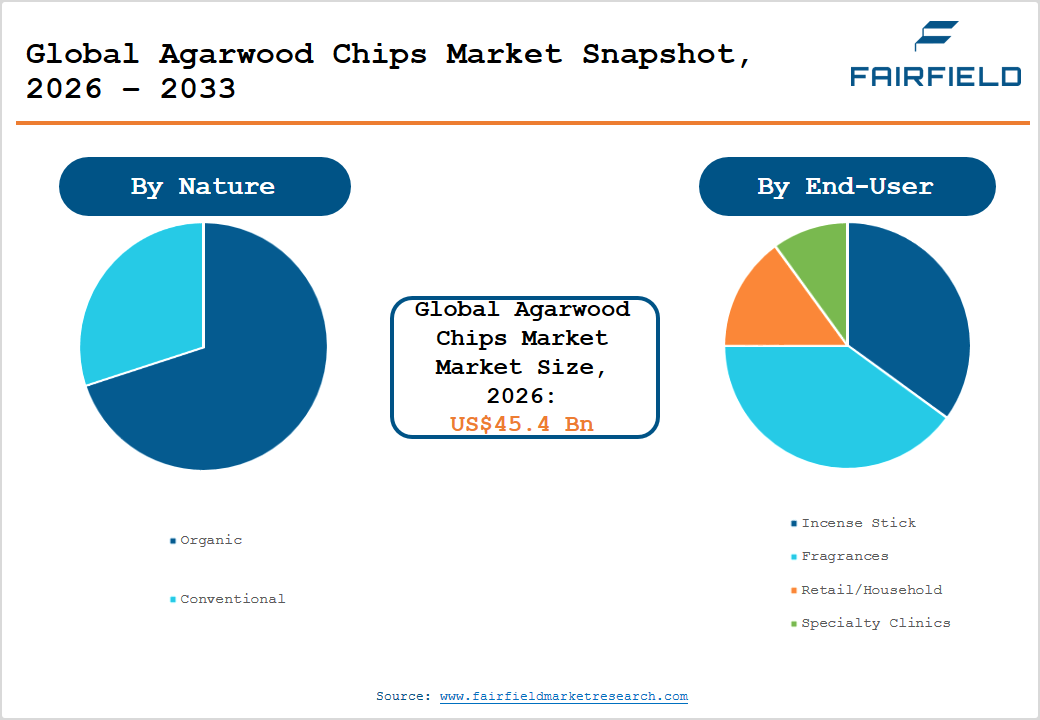

- The global Agarwood Chips Market size is likely to be valued at US$ 45.4 Billion in 2026 and is expected to reach US$ 77.3 Billion by 2033, growing at a CAGR of 90% during the forecast period from 2026 to 2033.

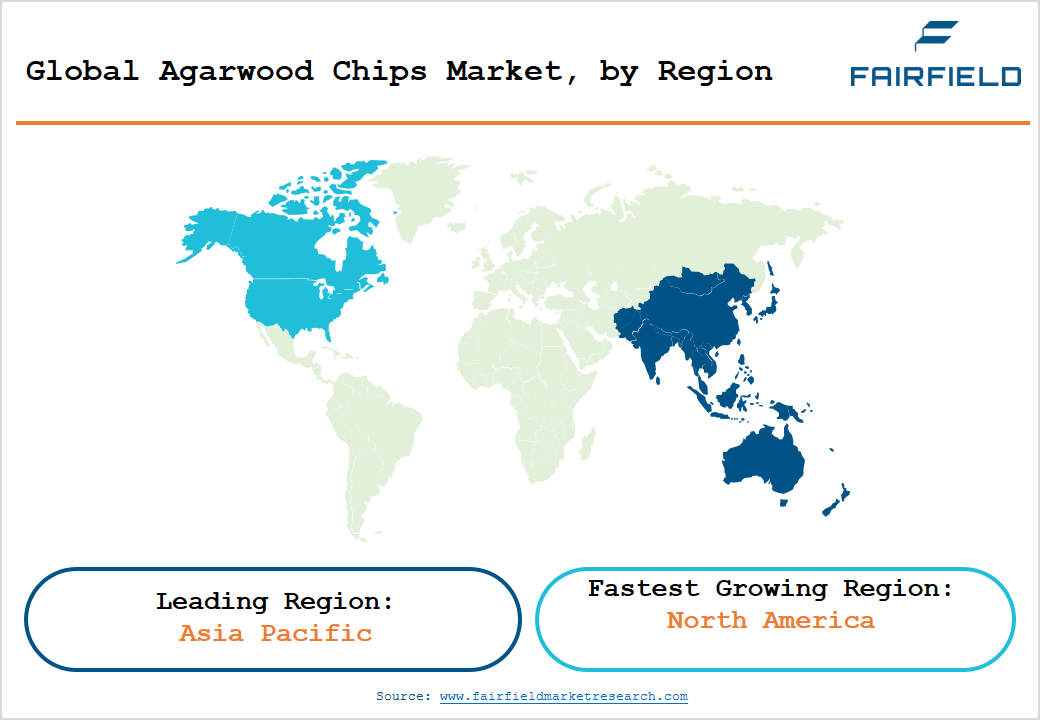

- Leading Region, Asia Pacific leads the global agarwood chips market with approximately 38% revenue share, driven by high production volumes in Vietnam, Indonesia, Malaysia, and large-scale cultural and commercial agarwood consumption in China, Japan, and India.

- Fastest Growing Region, North America is the fastest-growing agarwood chips market, fueled by rising demand for luxury oriental fragrances, natural wellness products, and expanding direct-to-consumer e-commerce channels enabling access to premium agarwood products.

- Dominant Segment, Incense Stick (End-User): The incense stick segment dominates the agarwood chips end-user category with around 38% share, anchored by deep-rooted religious, ceremonial, and cultural agarwood use across Asia Pacific, especially in China, India, and Japan.

- Fastest Growing Segment - Organic (By Nature): The organic agarwood chips segment is the fastest-growing category, driven by surging consumer preference for sustainably sourced, certified products in premium fragrance and wellness markets across Europe and North America.

- Key Market Opportunity - E-Commerce & B2C Expansion: The proliferation of e-commerce platforms presents a pivotal opportunity for agarwood chip producers to directly reach global consumers, bypassing intermediaries and enabling premium brand positioning for certified organic and traceable agarwood products.

Market Dynamics

Market Growth Drivers

- Surging Global Demand for Luxury Oud-Based Fragrances

The global luxury fragrance industry has experienced robust growth in recent years, significantly boosting the demand for agarwood chips as a premium raw material. According to the International Fragrance Association (IFRA), the global fragrance market has been expanding at an appreciable pace, with oud-derived notes becoming one of the most sought-after profiles among high-end perfumers in Europe and the Middle East. The Middle East & Africa region alone accounts for substantial per-capita fragrance expenditure, with Gulf Cooperation Council (GCC) countries such as Saudi Arabia, UAE, and Kuwait driving strong retail demand for pure agarwood chips and oud oil. Globally, oud has transitioned from a niche regional product to a mainstream luxury ingredient, encouraging agarwood producers to scale plantation operations and improve chip grading and certification processes.

- Expansion of Therapeutic and Wellness Applications

Agarwood chips are increasingly gaining recognition beyond incense and perfumery, finding applications in traditional medicine, aromatherapy, and specialty wellness clinics. Research published in the Journal of Ethnopharmacology has highlighted the anxiolytic, antimicrobial, and anti-inflammatory properties of agarwood extracts, validating its relevance in the alternative medicine sector. Countries like Japan, China, and India have long-standing traditions of using agarwood in Ayurvedic, Traditional Chinese Medicine (TCM), and Kampo medicinal systems. The growing global wellness tourism industry, estimated by the Global Wellness Institute to be a multi-trillion-dollar sector, is also amplifying demand for agarwood-infused treatments and aromatherapy sessions at premium health retreats, opening new revenue streams for market participants.

Market Restraints

- Stringent Regulatory Controls and CITES Restrictions

One of the most significant barriers to the agarwood chips market is the strict international trade regulation imposed through CITES Appendix II listing of Aquilaria and Gyrinops species the primary sources of agarwood. Countries that are CITES signatories must ensure that all agarwood exports are accompanied by valid permits certifying that the trade is non-detrimental to wild populations. This bureaucratic compliance creates substantial lead times and cost burdens for small and mid-sized exporters, particularly in Vietnam, Indonesia, and Bangladesh. The resulting supply bottlenecks constrain overall market scalability and limit the ability of producers to respond swiftly to rising global demand.

- Long Gestation Period of Agarwood Cultivation

Plantation-based agarwood production requires a gestation period of 8 to 15 years for trees to mature sufficiently for inoculation and resin formation, making it a capital-intensive and time-consuming endeavor. The infection process, which triggers the production of agarwood resin, requires significant technical expertise and biological inputs such as fungi and microbial inoculants. The high initial investment costs, combined with the risks of crop failure from adverse weather or pest infestation, deter many smallholder farmers from entering the segment. Consequently, agarwood supply remains constrained and price-sensitive, making chips a premium commodity with limited accessibility for price-sensitive end-users in the retail and household segment.

Market Opportunities

- Rise of Organic Agarwood and Sustainable Plantation Certifications

Consumer awareness about ethical sourcing and environmental sustainability at an all-time high, the organic and certified agarwood chips segment represents a compelling growth avenue. Initiatives by organizations such as the Forest Stewardship Council (FSC) and national bodies like APEDA (Agricultural and Processed Food Products Export Development Authority) in India are promoting sustainable agarwood plantation certifications. The emergence of premium organic oud chips marketed through specialty wellness and luxury retail channels is gaining traction in Europe, North America, and the GCC region. In 2023, Asia Plantation Capital announced expanded organic agarwood plantation programs in Thailand and Malaysia, catering to an increasingly conscientious global buyer base that is willing to pay a price premium for traceable, sustainably cultivated agarwood products.

- E-Commerce and B2C Digital Channel Expansion

The rapid proliferation of e-commerce and specialty online marketplaces has created substantial opportunities for agarwood chip brands to reach a wider global consumer base. Direct-to-consumer (D2C) models, facilitated through platforms such as Amazon, Noon, and brand-owned digital storefronts, are enabling producers from Vietnam, India, and Malaysia to tap into the North America and European markets without traditional distribution intermediaries. According to UNCTAD, global e-commerce sales surpassed US$ 7 trillion in 2023, reflecting the enormous potential for digitally enabled specialty commodity sales. B2C channels also allow brands to share product provenance, certification details, and grading information, enhancing consumer trust and enabling premium pricing for certified organic and wild-harvested agarwood chips.

Segmental Insights

- By Nature Analysis

The Conventional segment holds the leading position in the global agarwood chips market, accounting for approximately 65% of total market share. Conventional agarwood chips, sourced from both plantation-cultivated and forest-derived trees using traditional inoculation and harvesting techniques, dominate primarily due to their relatively lower cost of production, widespread availability, and established supply chains across major producing nations such as Vietnam, Indonesia, and India. The majority of commercial buyers, including incense manufacturers and fragrance blenders operating at scale, prefer conventional chips for their consistent availability and cost efficiency. While the organic segment is growing rapidly, conventional chips continue to account for the bulk of both B2B and retail trade volumes globally, underpinned by well-entrenched trade relationships between Southeast Asian producers and Middle Eastern buyers.

- End-User Analysis

Among the key end-user segments, Incense Sticks represent the dominant category, capturing approximately 38% of the global agarwood chips market share. The deep-rooted cultural and religious significance of agarwood-based incense across diverse traditional practices underpins this segment's consistent and high-volume demand. Buddhist and Hindu religious practices, temple rituals, and traditional ceremonial uses collectively drive a substantial portion of agarwood chip consumption channeled into incense stick production. According to India's Ministry of MSME, the incense stick industry employs millions of workers and contributes significantly to rural livelihoods, reflecting the large-scale socioeconomic footprint of the domestic sector. Rising exports of agarwood-based incense products to international markets, coupled with growing consumer preference for natural and aromatherapy-grade incense in wellness and spiritual care applications, further reinforce the Incense Sticks segment's sustained market leadership position.

- Distribution Channel Analysis

The Business to Business (B2B) distribution channel accounts for the leading share within the agarwood chips market, estimated at approximately 62% of total revenues. This dominance is driven by the large-scale procurement practices of fragrance houses, incense manufacturers, pharmaceutical and cosmetic companies, and wellness clinics, which source agarwood chips in bulk quantities directly from producers and plantation companies. Key sourcing hubs in Vietnam, Malaysia, and India maintain long-standing B2B trade relationships with buyers in the UAE, Saudi Arabia, France, and Japan. International trade fairs such as Beauty world Middle East and SIAL Paris serve as critical B2B engagement platforms, enabling agarwood suppliers to forge partnerships and negotiate volume contracts with global fragrance and cosmetic industry players.

Regional Insights

- North America Agarwood Chips Market Trends

North America represents the fastest-growing regional market for agarwood chips, propelled by an accelerating consumer shift toward luxury oriental fragrances, natural wellness products, and artisanal incense. The United States leads regional demand, with a growing population of oud connoisseurs and an expanding network of specialty perfumeries and wellness boutiques that stock premium agarwood chips and derivatives. According to the Fragrance Creators Association, consumer preference for complex, nature-derived fragrance notes in the U.S. has surged, creating a fertile environment for oud-based product lines from international suppliers.

The U.S. Food and Drug Administration (FDA) and U.S. Environmental Protection Agency (EPA) frameworks governing botanical imports and cosmetic ingredients have been increasingly navigated by agarwood suppliers seeking market entry. Canada is also witnessing growing demand through multicultural communities and a vibrant wellness sector. The expansion of specialty e-commerce platforms in the region is enabling Vietnamese and Indian agarwood suppliers to directly access North American consumers, bypassing traditional distribution intermediaries and enhancing market penetration speed.

- Europe Agarwood Chips Market Trends

Europe presents a mature yet steadily expanding market for agarwood chips, particularly driven by the luxury fragrance industries of France, Germany, and the United Kingdom. France, home to world-renowned perfume houses in Grasse and Paris, is a key importer of premium agarwood chips and oud oil for use in haute perfumery. The European Union's rigorous regulations under REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) and the IFRA code of practice govern ingredient use, compelling market entrants to obtain certified and traceable agarwood sourcing.

The U.K. and Germany are also experiencing growing demand from South Asian and Middle Eastern diaspora communities, who maintain cultural traditions of agarwood use in homes and places of worship. Sustainability-focused procurement policies in Europe are incentivizing the shift toward certified organic and FSC-compliant agarwood chips. Spain and France have seen rising consumer interest in oriental fragrance blends featuring oud, aligning with a broader European trend toward personalized luxury perfumery.

- Asia Pacific Agarwood Chips Market Trends

Asia Pacific holds the dominant position in the global agarwood chips market, commanding approximately 38% of global market share. The region is both the primary producer and one of the largest consumers of agarwood chips. Countries such as Vietnam, Indonesia, Malaysia, India, and Thailand are the world's leading agarwood-producing nations, benefiting from optimal tropical climatic conditions for Aquilaria tree cultivation. China remains the region's largest consumer, with agarwood deeply embedded in Traditional Chinese Medicine and cultural rituals.

Japan's high-value ceremonial and Buddhist incense market supports premium-grade agarwood chip imports, while India is simultaneously a major producer and an important domestic consumer through its large incense stick manufacturing sector. ASEAN member states, particularly Vietnam and Laos, are receiving increasing government support to develop sustainable agarwood plantation programs, in alignment with CITES guidelines. The Association of Southeast Asian Nations (ASEAN) has been promoting intra-regional trade facilitation for sustainably sourced non-timber forest products, which includes agarwood, bolstering regional supply chain efficiency and international trade competitiveness.

Competitive Landscape

The global agarwood chips market is highly fragmented, comprising a large number of smallholder farmers, regional plantation enterprises, and a limited number of organized multinational players. Key market participants differentiate themselves through CITES compliance certifications, organic and sustainable sourcing credentials, proprietary inoculation technologies that enhance resin yield, and robust B2B export networks. Companies such as Asia Plantation Capital and Grandawood Agarwood Australia have adopted vertically integrated business models, controlling the entire value chain from plantation management to retail distribution. Strategic expansions, joint ventures with local farmers, and investments in quality grading and chip standardization are emerging as key competitive strategies to capture premium market segments and establish brand credibility among discerning global buyers.

Key Market Developments

- March, 2024: Asia Plantation Capital Pte Ltd. announced the expansion of its agarwood plantation network across Thailand and Malaysia, incorporating advanced biotechnology-based inoculation methods to improve resin yield per tree by up to 30%, targeting premium B2B fragrance markets.

- November, 2024: Grandawood Agarwood Australia launched a new line of certified organic agarwood chips for the North American and European luxury fragrance markets, backed by third-party sustainability and traceability certifications, reinforcing its premium positioning.

- January, 2025: ASSAM AROMAS signed a multi-year supply agreement with a leading Middle Eastern fragrance conglomerate, securing long-term B2B contracts for premium-grade Assam agarwood chips, underscoring India's growing role in global agarwood trade.

Companies Covered in Agarwood Chips Market

- Grandawood Agarwood Australia

- Binh Nghia Agarwood Co., Ltd

- Hoang Giang Agarwood Ltd.

- Aalam Ul Oud

- KAB Industries

- Duy Hai AGARWOOD

- Thien Phu Agarwood Co., Ltd

- Asia Plantation Capital Pte Ltd.

- Ori Oud Asia

- ASSAM AROMAS

- Sadaharitha Plantations Limited

- Green Agro

- Thai Borai Agarwood Co., Ltd.

- KANHA AROMA

- Homegrown Concept Sdn Bhd (HGC)

- Pure Incense Ltd.

- Al Haramain Perfumes

- Treedom Sustainable Agroforestry

Market Segmentation

By Nature

- Organic

- Conventional

By End-User

- Incense Stick

- Fragrances

- Retail/Household

- Specialty Clinics

- Others

By Distribution Channel

- Business to Business (B2B)

- Business to Consumers (B2C)

By Regions

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Executive Summary

- Global Agarwood Chips Market Snapshot

- Future Projections

- Key Market Trends

- Regional Snapshot, by Value, 2026

- Analyst Recommendations

- Market Overview

- Market Definitions and Segmentations

- Market Dynamics

- Drivers

- Restraints

- Market Opportunities

- Value Chain Analysis

- COVID-19 Impact Analysis

- Porter's Five Forces Analysis

- Impact of Russia-Ukraine Conflict

- PESTLE Analysis

- Regulatory Analysis

- Price Trend Analysis

- Current Prices and Future Projections, 2025-2033

- Price Impact Factors

- Global Agarwood Chips Market Outlook, 2020 - 2033

- Global Agarwood Chips Market Outlook, by By Nature, Value (US$ Bn), 2020-2033

- Organic

- Conventional

- Global Agarwood Chips Market Outlook, by End-user, Value (US$ Bn), 2020-2033

- Incense Stick

- Fragrances

- Retail/Household

- Specialty Clinics

- Others

- Global Agarwood Chips Market Outlook, by By Distribution Channel, Value (US$ Bn), 2020-2033

- Business to Business (B2B)

- Business to Consumers (B2C)

- Global Agarwood Chips Market Outlook, by Region, Value (US$ Bn), 2020-2033

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Global Agarwood Chips Market Outlook, by By Nature, Value (US$ Bn), 2020-2033

- North America Agarwood Chips Market Outlook, 2020 - 2033

- North America Agarwood Chips Market Outlook, by By Nature, Value (US$ Bn), 2020-2033

- Organic

- Conventional

- North America Agarwood Chips Market Outlook, by End-user, Value (US$ Bn), 2020-2033

- Incense Stick

- Fragrances

- Retail/Household

- Specialty Clinics

- Others

- North America Agarwood Chips Market Outlook, by By Distribution Channel, Value (US$ Bn), 2020-2033

- Business to Business (B2B)

- Business to Consumers (B2C)

- North America Agarwood Chips Market Outlook, by Country, Value (US$ Bn), 2020-2033

- S. Agarwood Chips Market Outlook, by By Nature, 2020-2033

- S. Agarwood Chips Market Outlook, by End-user, 2020-2033

- S. Agarwood Chips Market Outlook, by By Distribution Channel, 2020-2033

- Canada Agarwood Chips Market Outlook, by By Nature, 2020-2033

- Canada Agarwood Chips Market Outlook, by End-user, 2020-2033

- Canada Agarwood Chips Market Outlook, by By Distribution Channel, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- North America Agarwood Chips Market Outlook, by By Nature, Value (US$ Bn), 2020-2033

- Europe Agarwood Chips Market Outlook, 2020 - 2033

- Europe Agarwood Chips Market Outlook, by By Nature, Value (US$ Bn), 2020-2033

- Organic

- Conventional

- Europe Agarwood Chips Market Outlook, by End-user, Value (US$ Bn), 2020-2033

- Incense Stick

- Fragrances

- Retail/Household

- Specialty Clinics

- Others

- Europe Agarwood Chips Market Outlook, by By Distribution Channel, Value (US$ Bn), 2020-2033

- Business to Business (B2B)

- Business to Consumers (B2C)

- Europe Agarwood Chips Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Germany Agarwood Chips Market Outlook, by By Nature, 2020-2033

- Germany Agarwood Chips Market Outlook, by End-user, 2020-2033

- Germany Agarwood Chips Market Outlook, by By Distribution Channel, 2020-2033

- Italy Agarwood Chips Market Outlook, by By Nature, 2020-2033

- Italy Agarwood Chips Market Outlook, by End-user, 2020-2033

- Italy Agarwood Chips Market Outlook, by By Distribution Channel, 2020-2033

- France Agarwood Chips Market Outlook, by By Nature, 2020-2033

- France Agarwood Chips Market Outlook, by End-user, 2020-2033

- France Agarwood Chips Market Outlook, by By Distribution Channel, 2020-2033

- K. Agarwood Chips Market Outlook, by By Nature, 2020-2033

- K. Agarwood Chips Market Outlook, by End-user, 2020-2033

- K. Agarwood Chips Market Outlook, by By Distribution Channel, 2020-2033

- Spain Agarwood Chips Market Outlook, by By Nature, 2020-2033

- Spain Agarwood Chips Market Outlook, by End-user, 2020-2033

- Spain Agarwood Chips Market Outlook, by By Distribution Channel, 2020-2033

- Russia Agarwood Chips Market Outlook, by By Nature, 2020-2033

- Russia Agarwood Chips Market Outlook, by End-user, 2020-2033

- Russia Agarwood Chips Market Outlook, by By Distribution Channel, 2020-2033

- Rest of Europe Agarwood Chips Market Outlook, by By Nature, 2020-2033

- Rest of Europe Agarwood Chips Market Outlook, by End-user, 2020-2033

- Rest of Europe Agarwood Chips Market Outlook, by By Distribution Channel, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Europe Agarwood Chips Market Outlook, by By Nature, Value (US$ Bn), 2020-2033

- Asia Pacific Agarwood Chips Market Outlook, 2020 - 2033

- Asia Pacific Agarwood Chips Market Outlook, by By Nature, Value (US$ Bn), 2020-2033

- Organic

- Conventional

- Asia Pacific Agarwood Chips Market Outlook, by End-user, Value (US$ Bn), 2020-2033

- Incense Stick

- Fragrances

- Retail/Household

- Specialty Clinics

- Others

- Asia Pacific Agarwood Chips Market Outlook, by By Distribution Channel, Value (US$ Bn), 2020-2033

- Business to Business (B2B)

- Business to Consumers (B2C)

- Asia Pacific Agarwood Chips Market Outlook, by Country, Value (US$ Bn), 2020-2033

- China Agarwood Chips Market Outlook, by By Nature, 2020-2033

- China Agarwood Chips Market Outlook, by End-user, 2020-2033

- China Agarwood Chips Market Outlook, by By Distribution Channel, 2020-2033

- Japan Agarwood Chips Market Outlook, by By Nature, 2020-2033

- Japan Agarwood Chips Market Outlook, by End-user, 2020-2033

- Japan Agarwood Chips Market Outlook, by By Distribution Channel, 2020-2033

- South Korea Agarwood Chips Market Outlook, by By Nature, 2020-2033

- South Korea Agarwood Chips Market Outlook, by End-user, 2020-2033

- South Korea Agarwood Chips Market Outlook, by By Distribution Channel, 2020-2033

- India Agarwood Chips Market Outlook, by By Nature, 2020-2033

- India Agarwood Chips Market Outlook, by End-user, 2020-2033

- India Agarwood Chips Market Outlook, by By Distribution Channel, 2020-2033

- Southeast Asia Agarwood Chips Market Outlook, by By Nature, 2020-2033

- Southeast Asia Agarwood Chips Market Outlook, by End-user, 2020-2033

- Southeast Asia Agarwood Chips Market Outlook, by By Distribution Channel, 2020-2033

- Rest of SAO Agarwood Chips Market Outlook, by By Nature, 2020-2033

- Rest of SAO Agarwood Chips Market Outlook, by End-user, 2020-2033

- Rest of SAO Agarwood Chips Market Outlook, by By Distribution Channel, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Asia Pacific Agarwood Chips Market Outlook, by By Nature, Value (US$ Bn), 2020-2033

- Latin America Agarwood Chips Market Outlook, 2020 - 2033

- Latin America Agarwood Chips Market Outlook, by By Nature, Value (US$ Bn), 2020-2033

- Organic

- Conventional

- Latin America Agarwood Chips Market Outlook, by End-user, Value (US$ Bn), 2020-2033

- Incense Stick

- Fragrances

- Retail/Household

- Specialty Clinics

- Others

- Latin America Agarwood Chips Market Outlook, by By Distribution Channel, Value (US$ Bn), 2020-2033

- Business to Business (B2B)

- Business to Consumers (B2C)

- Latin America Agarwood Chips Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Brazil Agarwood Chips Market Outlook, by By Nature, 2020-2033

- Brazil Agarwood Chips Market Outlook, by End-user, 2020-2033

- Brazil Agarwood Chips Market Outlook, by By Distribution Channel, 2020-2033

- Mexico Agarwood Chips Market Outlook, by By Nature, 2020-2033

- Mexico Agarwood Chips Market Outlook, by End-user, 2020-2033

- Mexico Agarwood Chips Market Outlook, by By Distribution Channel, 2020-2033

- Argentina Agarwood Chips Market Outlook, by By Nature, 2020-2033

- Argentina Agarwood Chips Market Outlook, by End-user, 2020-2033

- Argentina Agarwood Chips Market Outlook, by By Distribution Channel, 2020-2033

- Rest of LATAM Agarwood Chips Market Outlook, by By Nature, 2020-2033

- Rest of LATAM Agarwood Chips Market Outlook, by End-user, 2020-2033

- Rest of LATAM Agarwood Chips Market Outlook, by By Distribution Channel, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Latin America Agarwood Chips Market Outlook, by By Nature, Value (US$ Bn), 2020-2033

- Middle East & Africa Agarwood Chips Market Outlook, 2020 - 2033

- Middle East & Africa Agarwood Chips Market Outlook, by By Nature, Value (US$ Bn), 2020-2033

- Organic

- Conventional

- Middle East & Africa Agarwood Chips Market Outlook, by End-user, Value (US$ Bn), 2020-2033

- Incense Stick

- Fragrances

- Retail/Household

- Specialty Clinics

- Others

- Middle East & Africa Agarwood Chips Market Outlook, by By Distribution Channel, Value (US$ Bn), 2020-2033

- Business to Business (B2B)

- Business to Consumers (B2C)

- Middle East & Africa Agarwood Chips Market Outlook, by Country, Value (US$ Bn), 2020-2033

- GCC Agarwood Chips Market Outlook, by By Nature, 2020-2033

- GCC Agarwood Chips Market Outlook, by End-user, 2020-2033

- GCC Agarwood Chips Market Outlook, by By Distribution Channel, 2020-2033

- South Africa Agarwood Chips Market Outlook, by By Nature, 2020-2033

- South Africa Agarwood Chips Market Outlook, by End-user, 2020-2033

- South Africa Agarwood Chips Market Outlook, by By Distribution Channel, 2020-2033

- Egypt Agarwood Chips Market Outlook, by By Nature, 2020-2033

- Egypt Agarwood Chips Market Outlook, by End-user, 2020-2033

- Egypt Agarwood Chips Market Outlook, by By Distribution Channel, 2020-2033

- Nigeria Agarwood Chips Market Outlook, by By Nature, 2020-2033

- Nigeria Agarwood Chips Market Outlook, by End-user, 2020-2033

- Nigeria Agarwood Chips Market Outlook, by By Distribution Channel, 2020-2033

- Rest of Middle East Agarwood Chips Market Outlook, by By Nature, 2020-2033

- Rest of Middle East Agarwood Chips Market Outlook, by End-user, 2020-2033

- Rest of Middle East Agarwood Chips Market Outlook, by By Distribution Channel, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Middle East & Africa Agarwood Chips Market Outlook, by By Nature, Value (US$ Bn), 2020-2033

- Competitive Landscape

- Company Vs Segment Heatmap

- Company Market Share Analysis, 2025

- Competitive Dashboard

- Company Profiles

- Grandawood Agarwood Australia

- Company Overview

- Product Portfolio

- Financial Overview

- Business Strategies and Developments

- Binh Nghia Agarwood Co., Ltd

- Hoang Giang Agarwood Ltd.

- Aalam Ul Oud

- KAB Industries

- Duy Hai AGARWOOD.

- Thien Phu agarwood Co.,Ltd

- Asia Plantation Capital Pte Ltd.

- Ori Oud Asia

- ASSAM AROMAS

- Sadaharitha plantations limited

- Green Agro

- Thai Borai Agarwood Co.,Ltd.

- KANHA AROMA

- Homegrown Concept Sdn Bhd (HGC)

- Grandawood Agarwood Australia

- Appendix

- Research Methodology

- Report Assumptions

- Acronyms and Abbreviations

|

BASE YEAR |

HISTORICAL DATA |

FORECAST PERIOD |

UNITS |

|||

|

2025 |

2019 - 2024 |

2026 - 2033 |

Value: US$ Million |

|||

|

REPORT FEATURES |

DETAILS |

|

By Nature |

|

|

By End-user |

|

|

By Distribution Channel |

|

|

Geographical Coverage |

|

|

Leading Companies |

|

|

Report Highlights |

Key Market Indicators, Macro-micro economic impact analysis, Technological Roadmap, Key Trends, Driver, Restraints, and Future Opportunities & Revenue Pockets, Porter’s 5 Forces Analysis, Historical Trend (2019-2024), Market Estimates and Forecast, Market Dynamics, Industry Trends, Competition Landscape, Category, Region, Country-wise Trends & Analysis, COVID-19 Impact Analysis (Demand and Supply Chain) |