Automotive Metal Market Size, Share, and Growth Forecast 2026 - 2033

Key Market Highlights

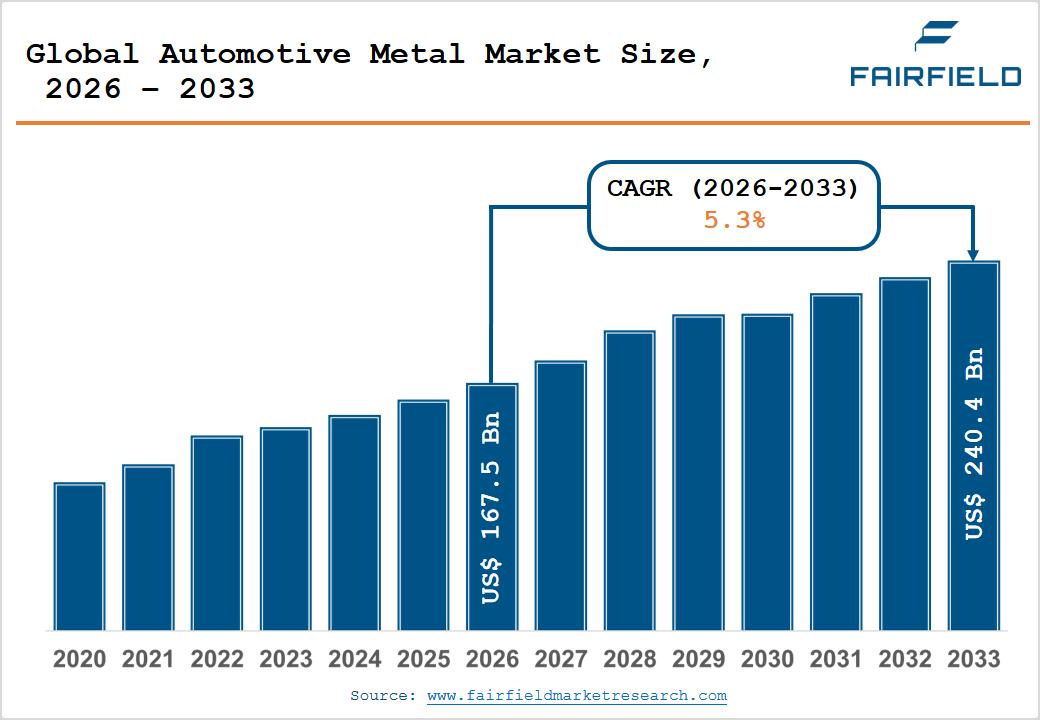

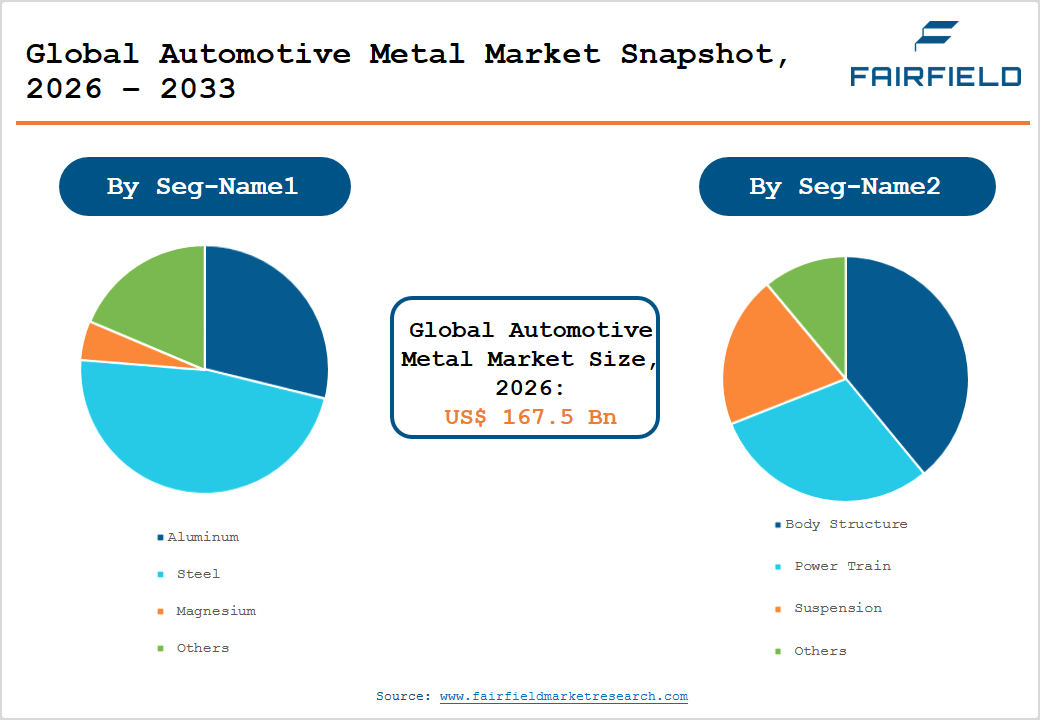

- The global Automotive Metal Market size is likely to be valued at US$ 167.5 Billion in 2026 and is expected to reach US$ 240.4 Billion by 2033, growing at a CAGR of 5.30% during the forecast period from 2026 to 2033.

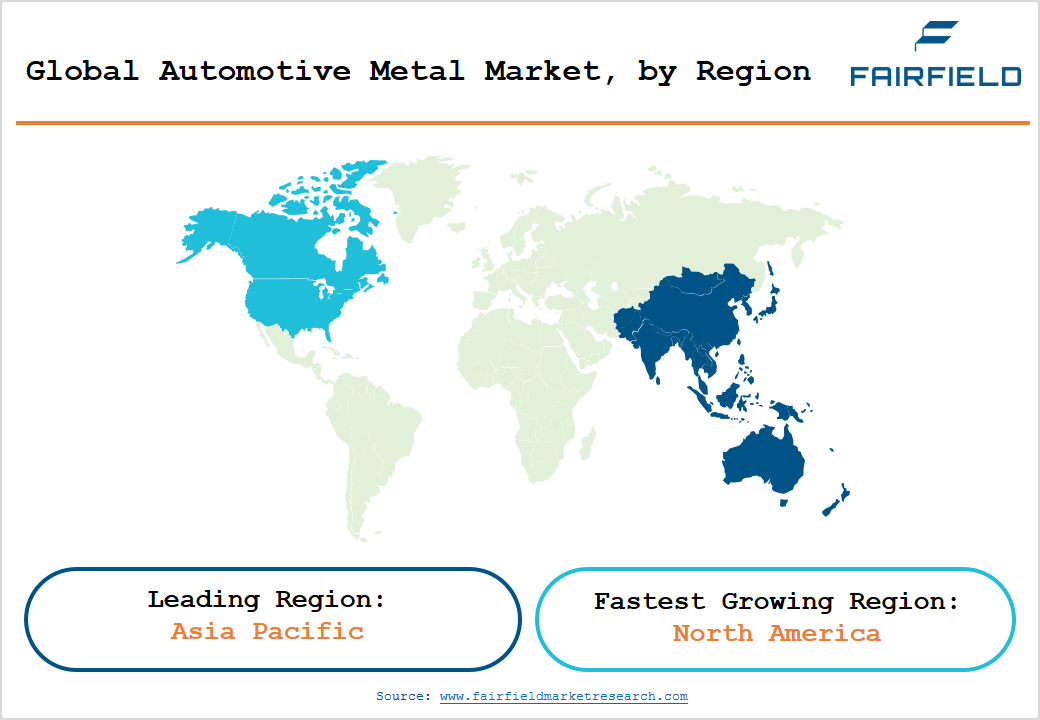

- Asia Pacific leads the global automotive metal market with approximately 50% market share, driven by China's dominant vehicle production volumes and the regional presence of Nippon Steel, POSCO, and JFE Steel Corporation.

- North America is the fastest-growing regional market, propelled by aggressive EV adoption targets, Inflation Reduction Act (IRA) incentives, and significant lightweighting investments by General Motors, Ford, and Tesla.

- Steel leads the product type segment with approximately 55% market share, supported by widespread adoption of AHSS grades by global OEMs and the World Steel Association's data confirming automotive as a critical end-use sector.

- Aluminum is the fastest-growing product type, driven by EV battery enclosure applications, with aluminum content per vehicle projected to exceed 250 kg by 2030 per the Aluminum Association.

- Rapidly expanding EV platforms globally present a significant opportunity, as EVs require 25-30% more lightweight metals per vehicle than ICE counterparts, creating durable incremental demand for aluminum and AHSS producers.

Market Dynamics

Market Growth Drivers

- Surging Demand for Lightweight Metals in Electric Vehicle Manufacturing

The accelerating global transition to electric vehicles is fundamentally reshaping automotive metals demand. Automakers face intense pressure to reduce vehicle weight to extend battery range and comply with carbon emission standards. This surge directly translates into heightened demand for lightweight automotive metals, particularly aluminum and magnesium alloys. A typical electric vehicle uses approximately 25-30% more aluminum than a conventional internal combustion engine (ICE) vehicle. As EV production scales rapidly, automakers such as Tesla, BMW, and Volkswagen are increasingly incorporating aluminum-intensive architectures and AHSS body structures to optimize battery performance and vehicle safety ratings, directly sustaining automotive metal market growth.

- Stringent Government Emission Regulations Accelerating AHSS Adoption

Governments worldwide are enacting increasingly rigorous fuel economy and carbon emission standards, compelling automakers to adopt advanced high-strength steel (AHSS) and aluminum to reduce vehicle weight without compromising structural integrity. In U.S., the National Highway Traffic Safety Administration (NHTSA) and the Environmental Protection Agency (EPA) have established Corporate Average Fuel Economy (CAFE) standards requiring automakers to achieve approximately 49 miles per gallon (mpg) by 2026. The sustained tightening of global emission norms ensures a durable demand tailwind for automotive metal producers through the forecast horizon.

Market Restraints

- Volatility in Raw Material Prices

Persistent volatility in prices of key raw materials including iron ore, bauxite, and primary aluminum poses a significant challenge to automotive metal market participants. According to the World Bank Commodity Markets Outlook, global iron ore prices fluctuated between 2021 and 2023, disrupting supply chain planning and squeezing margins for steel producers and automotive OEMs alike. Aluminum prices similarly witnessed sharp swings following geopolitical tensions and energy cost surges, particularly in Europe. This instability makes long-term supply contracting difficult, discourages capital investment in capacity expansion, and can translate into higher vehicle manufacturing costs ultimately impacting end-consumer affordability and slowing market volume growth.

- High Environmental Compliance Costs in Metal Production

Steel and aluminum production are among the most energy-intensive and carbon-emitting industrial activities globally. The World Steel Association reports that the steel industry contributes approximately 7-9% of global CO₂ emissions. Increasingly stringent environmental regulations including the EU's Carbon Border Adjustment Mechanism (CBAM) impose significant compliance costs on metal producers. Transitioning to greener production technologies such as hydrogen-based direct reduced iron (DRI) or electric arc furnaces (EAF) requires substantial capital outlay. Smaller manufacturers may struggle with such financial burdens, limiting market participation and potentially creating supply gaps that hamper the automotive metal market's ability to meet growing OEM demand efficiently.

Market Opportunities

- Growing Aluminum Adoption in EV Battery Enclosures and Structural Components

The rapid proliferation of electric vehicles presents a transformative opportunity for aluminum producers in the automotive metals market. EV battery enclosures, structural crash management systems, and thermal management components are increasingly manufactured from aluminum due to its lightweight properties, corrosion resistance, and superior formability. Novelis Inc., a leading automotive-grade aluminum rolling company, has announced plans to expand its automotive aluminum production capacity annually to meet rising EV demand. According to the Aluminum Association, automotive aluminum demand in North America is expected to grow substantially, with aluminum content per vehicle. This structural demand expansion offers significant long-term revenue streams for aluminum producers including Alcoa Corporation, Norsk Hydro ASA, and Constellium SE, making it one of the most compelling opportunities in the automotive metal market landscape.

- Advanced High-Strength Steel Innovation for Next-Generation EV Platforms

Innovation in advanced high-strength steel (AHSS) grades including dual-phase, martensitic, and press-hardened steels represents a compelling opportunity for automotive steel producers targeting next-generation electric and hybrid vehicle platforms. Third-generation AHSS can reduce vehicle body weight by up to 25% compared to conventional mild steel, according to WorldAutoSteel, while remaining cost-competitive relative to aluminum. ArcelorMittal and POSCO have announced dedicated R&D investments in high-performance steel grades tailored for EV body structures and battery enclosures. India's expanding automotive sector highlighted by the Society of Indian Automobile Manufacturers (SIAM) reporting strong double-digit production growth and Southeast Asia's growing OEM base represent high-potential demand markets for cost-effective AHSS solutions. These factors collectively position AHSS innovation as a key revenue driver through 2033, particularly for producers with localized manufacturing capabilities in high-growth regions.

Segmental Insights

- By Product Type Analysis

Steel dominates the automotive metal market by product type, commanding approximately 55% of total market share in 2026. This dominance is underpinned by steel's combination of structural strength, crashworthiness, cost efficiency, and recyclability. According to the World Steel Association, the automotive sector consumes approximately 12-13% of total global steel production annually, underscoring its critical demand role. Advanced high-strength steel (AHSS) grades continue to gain prominence within this segment as automakers seek to simultaneously meet stringent safety standards and fuel economy regulations. Major producers including ArcelorMittal, POSCO, and Nippon Steel Corporation have developed specialized automotive steel grades enabling significant vehicle weight reduction while maintaining structural performance, further consolidating steel's leading position within the product type segment of the automotive metal market.

- By Application Analysis

The Body Structure application segment leads the automotive metal market, representing approximately 38% of total market share in 2026. The body structure comprising the vehicle's frame, door panels, pillars, and roof is the single largest consumer of automotive metals, demanding materials offering high structural rigidity, crash energy absorption, and superior formability. The shift toward advanced high-strength steel and aluminum-intensive body structures across global automotive platforms has further elevated demand within this segment. According to the American Iron and Steel Institute (AISI), approximately 54% of a modern vehicle's body structure is now composed of high-strength or advanced high-strength steel grades, underscoring this segment's critical reliance on engineered metals and reinforcing its position as the dominant application category in the automotive metal market.

- By Vehicle Type Analysis

Passenger cars represent the leading vehicle type segment in the automotive metal market, accounting for approximately 58% of total market share in 2026. This leadership is driven by the sheer global volume of passenger car production; the International Organization of Motor Vehicle Manufacturers (OICA) reported global passenger car output at approximately 67 million units in 2023. Passenger cars are the primary beneficiaries of lightweighting trends, incorporating high volumes of aluminum, AHSS, and magnesium alloys to meet stringent emission standards and improve fuel efficiency. The rapid proliferation of electric passenger vehicles which utilize greater quantities of aluminum and specialty metals per vehicle compared to ICE counterparts further amplifies demand in this segment, reinforcing its dominant position through the forecast horizon of 2033.

Regional Insights

- North America Automotive Metal Market Trends

North America is the fastest-growing region in the automotive metal market, driven by robust automotive manufacturing activity, aggressive EV adoption targets, and significant lightweighting investments by General Motors, Ford Motor Company, and Tesla. The United States remains the regional anchor, supported by the Inflation Reduction Act (IRA), which incentivizes domestic EV and EV component manufacturing and strengthens regional supply chains for automotive-grade aluminum and steel. The U.S. Department of Energy's Vehicle Technologies Office (VTO) has actively funded lightweight materials research, promoting integration of advanced alloys in next-generation vehicle platforms.

The region benefits from a well-developed aluminum supply chain anchored by Novelis and Alcoa Corporation, both operating major automotive-grade aluminum processing facilities. Canada contributes through its integrated steel sector and EV supply chain investments. United States Steel Corporation (U.S. Steel) and Nucor Corporation are expanding production of AHSS grades for automotive applications. These developments collectively position North America as the most dynamically growing automotive metal market regionally, with momentum expected to accelerate through 2033 as EV adoption broadens across the continent.

- Europe Automotive Metal Market Trends

Europe maintains a strategically important position in the global automotive metal market, underpinned by its concentration of premium automotive manufacturers including Volkswagen Group, BMW Group, Mercedes-Benz Group AG, Stellantis, and Renault Group. Germany remains the epicenter of European automotive metal consumption, accounting for the largest share of regional demand, driven by its leadership in both conventional and electric vehicle production. France, Spain, and the United Kingdom further contribute through their established OEM manufacturing footprints, while Italy and the Czech Republic are growing contributors to regional metal demand.

The European Green Deal and the EU mandate banning new internal combustion engine vehicle sales by 2035 are fundamentally reshaping material choices. European automakers are rapidly transitioning to aluminum-intensive EV platforms, creating sustained demand for high-purity aluminum and AHSS. ThyssenKrupp AG and SSAB AB are investing in hydrogen-based green steel production to align with the EU's carbon neutrality objectives, contributing to market innovation. Norsk Hydro ASA and Constellium SE are similarly expanding automotive aluminum capacity, ensuring long-term supply resilience aligned with European OEM decarbonization roadmaps.

- Asia Pacific Automotive Metal Market Trends

Asia Pacific dominates the global automotive metal market with approximately 50% of total market share, driven by unparalleled vehicle production volumes and the presence of the world's largest automotive metal producers. China is the undisputed regional leader, accounting for the majority of demand supported by its status as the world's largest automobile and EV market. According to the China Association of Automobile Manufacturers (CAAM), China produced over 30 million vehicles in 2023, generating enormous demand for steel, aluminum, and specialty automotive metals across body structure, powertrain, and suspension applications.

Japan and South Korea contribute significantly through established automotive OEMs including Toyota Motor Corporation, Honda Motor Co., Hyundai Motor Company, and Kia Corporation, alongside world-class steel producers Nippon Steel Corporation, JFE Steel Corporation, and POSCO. India is rapidly emerging as a high-growth market, with the Society of Indian Automobile Manufacturers (SIAM) reporting robust domestic vehicle production expansion. The region's competitive manufacturing cost structure, integrated raw material-to-finished-metal supply chains, and large domestic consumption bases collectively reinforce Asia Pacific's dominant market position through 2033.

Competitive Landscape

The global automotive metal market exhibits a moderately consolidated structure, with a handful of large multinational producers notably ArcelorMittal, Nippon Steel Corporation, POSCO, ThyssenKrupp AG, and Alcoa Corporation commanding substantial market shares. Leaders differentiate through proprietary AHSS and aluminum alloy grades, long-term OEM supply agreements, and strategic co-development partnerships with automakers. Key business model trends include vertical integration across raw material sourcing and processing, investments in green steel and low-carbon aluminum production, and geographic diversification across North America, Europe, and Asia Pacific automotive hubs. Emerging players are focusing on niche segments, including magnesium alloys and specialty non-ferrous metals targeting EV-specific applications and next-generation lightweighting platforms.

Key Market Developments

- In January 2025: ArcelorMittal announced a major investment in a new electric arc furnace (EAF) facility in Europe, aimed at producing low-carbon automotive steel grades to meet stringent OEM decarbonization requirements aligned with the European Green Deal.

- In March 2024: Novelis Inc. expanded its automotive-grade aluminum rolling capacity in North America by approximately 100,000 metric tons annually to support rising EV lightweighting demand from General Motors and Ford Motor Company.

- In November 2023: POSCO launched its new XF450 ultra-high-strength steel grade specifically designed for EV battery pack housings and structural components, targeting global automotive OEM partnerships across Asia Pacific, Europe, and North America.

Companies Covered in Automotive Metal Market

- ArcelorMittal

- Nippon Steel Corporation

- POSCO

- SSAB AB

- Tata Steel Limited

- ThyssenKrupp AG

- United States Steel Corporation (U.S. Steel)

- Hyundai Steel Company

- JFE Steel Corporation

- Alcoa Corporation

- Novelis Inc.

- Kobe Steel, Ltd.

- Norsk Hydro ASA

- Reliance Steel & Aluminum Co.

- Constellium SE

- Voestalpine AG

- Baoshan Iron & Steel Co., Ltd. (Baosteel Group)

- Hindalco Industries Limited

- Kaiser Aluminum Corporation

- Salzgitter AG

Market Segmentation

By Product Type

- Aluminum

- Steel

- Magnesium

- Others

By Application

- Body Structure

- Power Train

- Suspension

- Others

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Executive Summary

- Global Automotive Metal Market Snapshot

- Future Projections

- Key Market Trends

- Regional Snapshot, by Value, 2026

- Analyst Recommendations

- Market Overview

- Market Definitions and Segmentations

- Market Dynamics

- Drivers

- Restraints

- Market Opportunities

- Value Chain Analysis

- COVID-19 Impact Analysis

- Porter's Five Forces Analysis

- Impact of Russia-Ukraine Conflict

- PESTLE Analysis

- Regulatory Analysis

- Price Trend Analysis

- Current Prices and Future Projections, 2025-2033

- Price Impact Factors

- Global Automotive Metal Market Outlook, 2020 - 2033

- Global Automotive Metal Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Aluminum

- Steel

- Magnesium

- Others

- Global Automotive Metal Market Outlook, by Application, Value (US$ Bn), 2020-2033

- Body Structure

- Power Train

- Suspension

- Others

- Global Automotive Metal Market Outlook, by Vehicle Type, Value (US$ Bn), 2020-2033

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Global Automotive Metal Market Outlook, by Region, Value (US$ Bn), 2020-2033

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Global Automotive Metal Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- North America Automotive Metal Market Outlook, 2020 - 2033

- North America Automotive Metal Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Aluminum

- Steel

- Magnesium

- Others

- North America Automotive Metal Market Outlook, by Application, Value (US$ Bn), 2020-2033

- Body Structure

- Power Train

- Suspension

- Others

- North America Automotive Metal Market Outlook, by Vehicle Type, Value (US$ Bn), 2020-2033

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- North America Automotive Metal Market Outlook, by Country, Value (US$ Bn), 2020-2033

- S. Automotive Metal Market Outlook, by Product Type, 2020-2033

- S. Automotive Metal Market Outlook, by Application, 2020-2033

- S. Automotive Metal Market Outlook, by Vehicle Type, 2020-2033

- Canada Automotive Metal Market Outlook, by Product Type, 2020-2033

- Canada Automotive Metal Market Outlook, by Application, 2020-2033

- Canada Automotive Metal Market Outlook, by Vehicle Type, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- North America Automotive Metal Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Europe Automotive Metal Market Outlook, 2020 - 2033

- Europe Automotive Metal Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Aluminum

- Steel

- Magnesium

- Others

- Europe Automotive Metal Market Outlook, by Application, Value (US$ Bn), 2020-2033

- Body Structure

- Power Train

- Suspension

- Others

- Europe Automotive Metal Market Outlook, by Vehicle Type, Value (US$ Bn), 2020-2033

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Europe Automotive Metal Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Germany Automotive Metal Market Outlook, by Product Type, 2020-2033

- Germany Automotive Metal Market Outlook, by Application, 2020-2033

- Germany Automotive Metal Market Outlook, by Vehicle Type, 2020-2033

- Italy Automotive Metal Market Outlook, by Product Type, 2020-2033

- Italy Automotive Metal Market Outlook, by Application, 2020-2033

- Italy Automotive Metal Market Outlook, by Vehicle Type, 2020-2033

- France Automotive Metal Market Outlook, by Product Type, 2020-2033

- France Automotive Metal Market Outlook, by Application, 2020-2033

- France Automotive Metal Market Outlook, by Vehicle Type, 2020-2033

- K. Automotive Metal Market Outlook, by Product Type, 2020-2033

- K. Automotive Metal Market Outlook, by Application, 2020-2033

- K. Automotive Metal Market Outlook, by Vehicle Type, 2020-2033

- Spain Automotive Metal Market Outlook, by Product Type, 2020-2033

- Spain Automotive Metal Market Outlook, by Application, 2020-2033

- Spain Automotive Metal Market Outlook, by Vehicle Type, 2020-2033

- Russia Automotive Metal Market Outlook, by Product Type, 2020-2033

- Russia Automotive Metal Market Outlook, by Application, 2020-2033

- Russia Automotive Metal Market Outlook, by Vehicle Type, 2020-2033

- Rest of Europe Automotive Metal Market Outlook, by Product Type, 2020-2033

- Rest of Europe Automotive Metal Market Outlook, by Application, 2020-2033

- Rest of Europe Automotive Metal Market Outlook, by Vehicle Type, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Europe Automotive Metal Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Asia Pacific Automotive Metal Market Outlook, 2020 - 2033

- Asia Pacific Automotive Metal Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Aluminum

- Steel

- Magnesium

- Others

- Asia Pacific Automotive Metal Market Outlook, by Application, Value (US$ Bn), 2020-2033

- Body Structure

- Power Train

- Suspension

- Others

- Asia Pacific Automotive Metal Market Outlook, by Vehicle Type, Value (US$ Bn), 2020-2033

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Asia Pacific Automotive Metal Market Outlook, by Country, Value (US$ Bn), 2020-2033

- China Automotive Metal Market Outlook, by Product Type, 2020-2033

- China Automotive Metal Market Outlook, by Application, 2020-2033

- China Automotive Metal Market Outlook, by Vehicle Type, 2020-2033

- Japan Automotive Metal Market Outlook, by Product Type, 2020-2033

- Japan Automotive Metal Market Outlook, by Application, 2020-2033

- Japan Automotive Metal Market Outlook, by Vehicle Type, 2020-2033

- South Korea Automotive Metal Market Outlook, by Product Type, 2020-2033

- South Korea Automotive Metal Market Outlook, by Application, 2020-2033

- South Korea Automotive Metal Market Outlook, by Vehicle Type, 2020-2033

- India Automotive Metal Market Outlook, by Product Type, 2020-2033

- India Automotive Metal Market Outlook, by Application, 2020-2033

- India Automotive Metal Market Outlook, by Vehicle Type, 2020-2033

- Southeast Asia Automotive Metal Market Outlook, by Product Type, 2020-2033

- Southeast Asia Automotive Metal Market Outlook, by Application, 2020-2033

- Southeast Asia Automotive Metal Market Outlook, by Vehicle Type, 2020-2033

- Rest of SAO Automotive Metal Market Outlook, by Product Type, 2020-2033

- Rest of SAO Automotive Metal Market Outlook, by Application, 2020-2033

- Rest of SAO Automotive Metal Market Outlook, by Vehicle Type, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Asia Pacific Automotive Metal Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Latin America Automotive Metal Market Outlook, 2020 - 2033

- Latin America Automotive Metal Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Aluminum

- Steel

- Magnesium

- Others

- Latin America Automotive Metal Market Outlook, by Application, Value (US$ Bn), 2020-2033

- Body Structure

- Power Train

- Suspension

- Others

- Latin America Automotive Metal Market Outlook, by Vehicle Type, Value (US$ Bn), 2020-2033

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Latin America Automotive Metal Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Brazil Automotive Metal Market Outlook, by Product Type, 2020-2033

- Brazil Automotive Metal Market Outlook, by Application, 2020-2033

- Brazil Automotive Metal Market Outlook, by Vehicle Type, 2020-2033

- Mexico Automotive Metal Market Outlook, by Product Type, 2020-2033

- Mexico Automotive Metal Market Outlook, by Application, 2020-2033

- Mexico Automotive Metal Market Outlook, by Vehicle Type, 2020-2033

- Argentina Automotive Metal Market Outlook, by Product Type, 2020-2033

- Argentina Automotive Metal Market Outlook, by Application, 2020-2033

- Argentina Automotive Metal Market Outlook, by Vehicle Type, 2020-2033

- Rest of LATAM Automotive Metal Market Outlook, by Product Type, 2020-2033

- Rest of LATAM Automotive Metal Market Outlook, by Application, 2020-2033

- Rest of LATAM Automotive Metal Market Outlook, by Vehicle Type, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Latin America Automotive Metal Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Middle East & Africa Automotive Metal Market Outlook, 2020 - 2033

- Middle East & Africa Automotive Metal Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Aluminum

- Steel

- Magnesium

- Others

- Middle East & Africa Automotive Metal Market Outlook, by Application, Value (US$ Bn), 2020-2033

- Body Structure

- Power Train

- Suspension

- Others

- Middle East & Africa Automotive Metal Market Outlook, by Vehicle Type, Value (US$ Bn), 2020-2033

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Middle East & Africa Automotive Metal Market Outlook, by Country, Value (US$ Bn), 2020-2033

- GCC Automotive Metal Market Outlook, by Product Type, 2020-2033

- GCC Automotive Metal Market Outlook, by Application, 2020-2033

- GCC Automotive Metal Market Outlook, by Vehicle Type, 2020-2033

- South Africa Automotive Metal Market Outlook, by Product Type, 2020-2033

- South Africa Automotive Metal Market Outlook, by Application, 2020-2033

- South Africa Automotive Metal Market Outlook, by Vehicle Type, 2020-2033

- Egypt Automotive Metal Market Outlook, by Product Type, 2020-2033

- Egypt Automotive Metal Market Outlook, by Application, 2020-2033

- Egypt Automotive Metal Market Outlook, by Vehicle Type, 2020-2033

- Nigeria Automotive Metal Market Outlook, by Product Type, 2020-2033

- Nigeria Automotive Metal Market Outlook, by Application, 2020-2033

- Nigeria Automotive Metal Market Outlook, by Vehicle Type, 2020-2033

- Rest of Middle East Automotive Metal Market Outlook, by Product Type, 2020-2033

- Rest of Middle East Automotive Metal Market Outlook, by Application, 2020-2033

- Rest of Middle East Automotive Metal Market Outlook, by Vehicle Type, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Middle East & Africa Automotive Metal Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Competitive Landscape

- Company Vs Segment Heatmap

- Company Market Share Analysis, 2025

- Competitive Dashboard

- Company Profiles

- ArcelorMittal

- Company Overview

- Product Portfolio

- Financial Overview

- Business Strategies and Developments

- Nippon Steel Corporation

- POSCO

- SSAB AB

- Tata Steel Limited

- ThyssenKrupp AG

- United States Steel Corporation (U.S. Steel)

- Hyundai Steel Company

- JFE Steel Corporation

- Alcoa Corporation

- Novelis Inc.

- Kobe Steel, Ltd.

- Norsk Hydro ASA

- Reliance Steel & Aluminum Co.

- Constellium SE

- ArcelorMittal

- Appendix

- Research Methodology

- Report Assumptions

- Acronyms and Abbreviations

|

BASE YEAR |

HISTORICAL DATA |

FORECAST PERIOD |

UNITS |

|||

|

2025 |

|

2019 - 2024 |

2026 - 2033 |

Value: US$ Million |

||

|

REPORT FEATURES |

DETAILS |

|

By Product Type Coverage |

|

|

By Application Coverage |

|

|

Geographical Coverage |

|

|

Leading Companies |

|

|

Report Highlights |

Key Market Indicators, Macro-micro economic impact analysis, Technological Roadmap, Key Trends, Driver, Restraints, and Future Opportunities & Revenue Pockets, Porter’s 5 Forces Analysis, Historical Trend (2019-2024), Market Estimates and Forecast, Market Dynamics, Industry Trends, Competition Landscape, Category, Region, Country-wise Trends & Analysis, COVID-19 Impact Analysis (Demand and Supply Chain) |