Centrifugal Pumps Market Size, Share, and Growth Forecast 2026–2033

Key Market Highlights

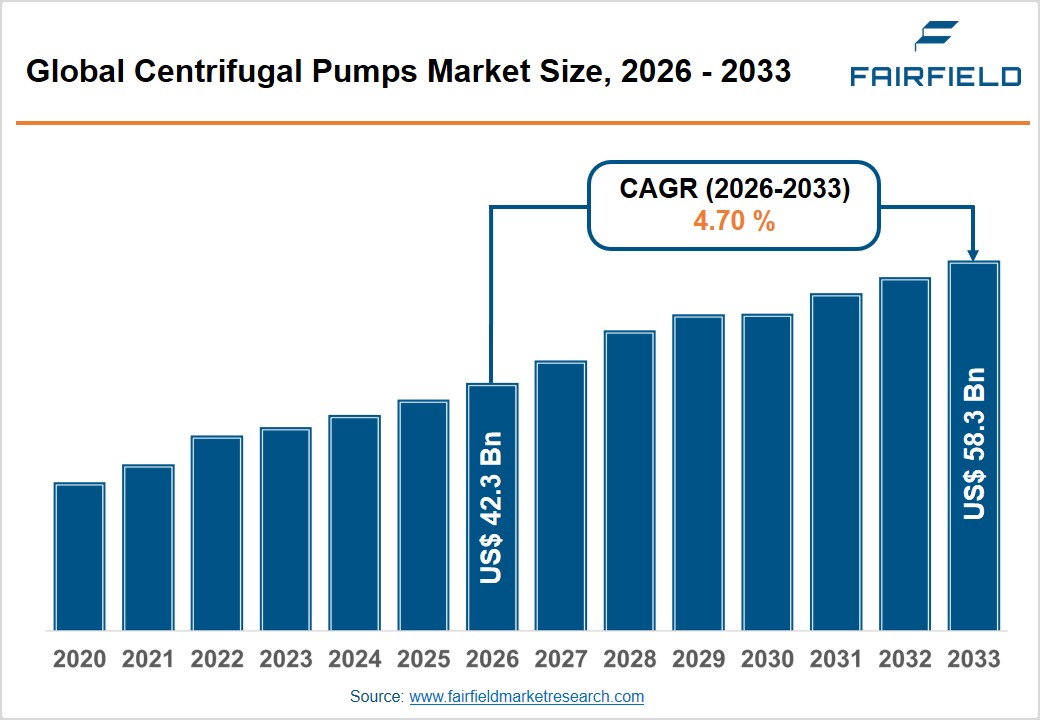

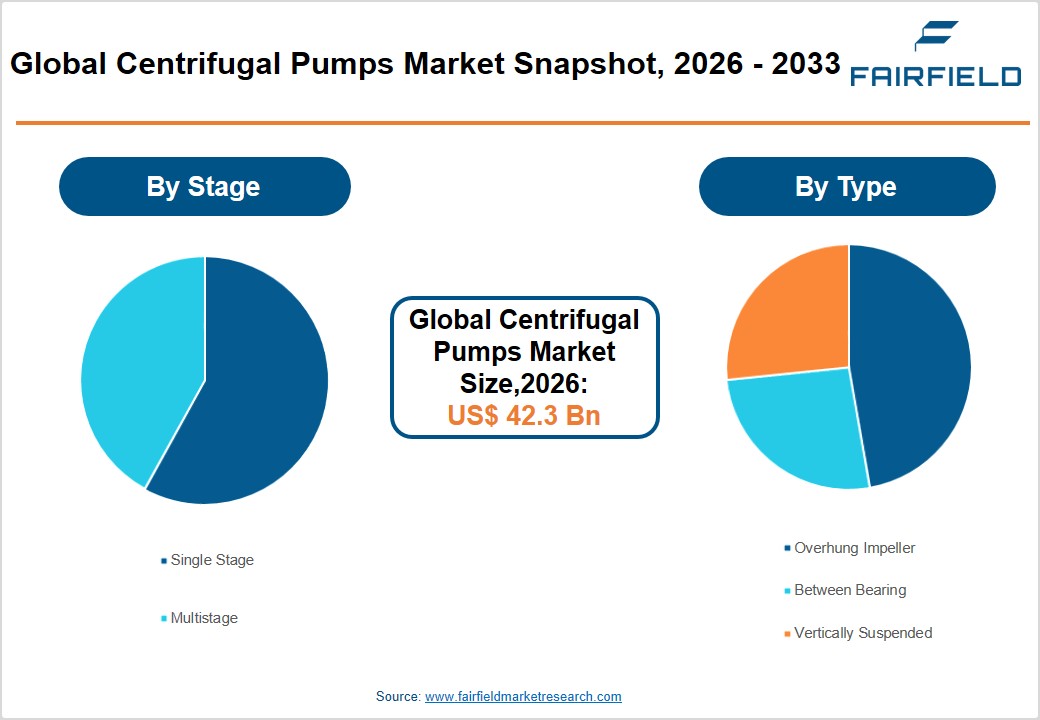

- The global Centrifugal Pumps Market size is likely to be valued at USD 42.3 billion in 2026 and is expected to reach USD 58.3 billion by 2033, growing at a CAGR of 4.70% during the forecast period from 2026 to 2033.

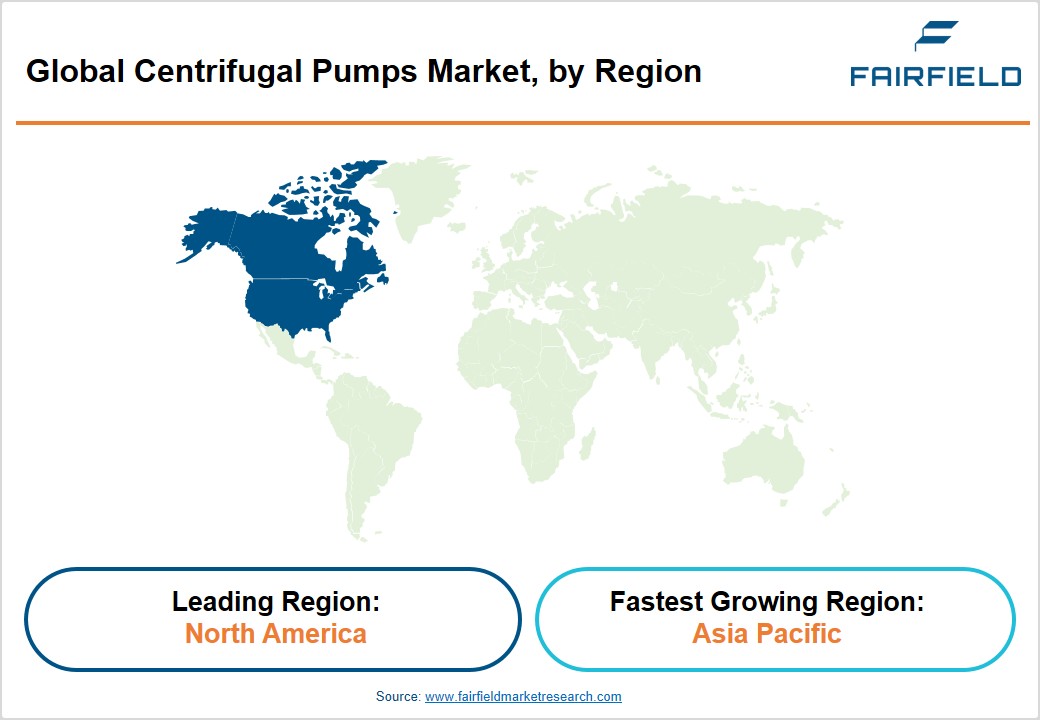

- Asia Pacific dominates the global centrifugal pumps market with approximately 49% revenue share in 2026, driven by China's large-scale water infrastructure investments and India's rapidly expanding industrial and municipal water sectors.

- The MEA region is projected as the fastest-growing market, propelled by GCC desalination mega-projects, Saudi Arabia's Vision 2030, and expanding municipal water networks across Sub-Saharan Africa.

- The Electrical segment commands approximately 74% of the market in 2026, underpinned by widespread grid infrastructure, VFD-enabled efficiency gains, and mandatory IE3/IE4 motor efficiency standards under IEC 60034-30-1.

- The Multistage segment is gaining traction driven by rising adoption in high-pressure desalination, deep-well water abstraction, and pipeline boosting applications, especially across GCC and Asia Pacific energy infrastructure projects.

- The integration of IIoT, AI-driven predictive maintenance, and digital twin technology into centrifugal pump systems presents a high-value differentiation opportunity, enabling premium pricing and long-term service revenue in energy-efficiency-focused markets.

Market Dynamics

Market Growth Drivers

- Rising Global Water and Wastewater Infrastructure Investments

Escalating urbanization and growing freshwater scarcity are compelling governments worldwide to scale up water infrastructure spending, directly boosting centrifugal pump demand. According to the United Nations Environment Programme (UNEP), over 2 billion people currently lack access to safe drinking water, prompting multilateral funding institutions such as the World Bank and the Asian Development Bank (ADB) to commit hundreds of billions of dollars to water security projects through 2030. In U.S., the Infrastructure Investment and Jobs Act allocated US$ 55 billion specifically for water and wastewater systems. Centrifugal pumps preferred for high-flow, low-to-medium head applications are indispensable in water intake, distribution, and treatment facilities, making this spending wave a powerful growth catalyst for the market.

- Robust Expansion of the Oil & Gas and Power Generation Sectors

The oil & gas industry remains one of the largest consumers of centrifugal pumps, employing them across upstream, midstream, and downstream operations including crude transfer, pipeline boosting, refinery processing, and desalination. The International Energy Agency (IEA) projected global upstream oil and gas capital expenditure to exceed billions in 2024, with sustained investment levels anticipated through the decade. Simultaneously, power plant operators worldwide rely on centrifugal pumps for cooling-water circulation, boiler feed, and condensate extraction. The rapid build-out of both conventional thermal plants and nuclear facilities in Asia particularly in China and India is generating incremental pump procurement volumes and reinforcing the market's growth trajectory.

Market Restraints

- High Capital Cost and Maintenance Requirements

Centrifugal pumps especially multi-stage and vertically suspended variants engineered for harsh or high-pressure applications demand significant upfront capital expenditure and ongoing maintenance investment. Seal replacements, impeller refurbishment, and bearing overhauls add to total cost of ownership, making budget-constrained municipalities and small industrial operators hesitant to upgrade. According to the Hydraulic Institute, pump system energy and maintenance costs over a 20-year lifecycle can exceed ten times the initial purchase price, dampening adoption rates particularly in price-sensitive markets across Latin America and Sub-Saharan Africa.

- Vulnerability to Cavitation and Operational Inefficiencies

Centrifugal pumps are inherently susceptible to cavitation a phenomenon caused by local pressure drops that form vapor bubbles, leading to noise, vibration, and accelerated material degradation. The Hydraulic Institute estimates that cavitation-related failures account for a substantial share of unscheduled pump downtime in process industries, translating into costly repairs and production losses. Industries operating with variable flow demands or low inlet pressures must invest heavily in monitoring systems such as variable-frequency drives (VFDs) and condition-based maintenance platforms, adding to operational complexity and total expenditure, which can constrain market growth in cost-sensitive end-user segments.

Market Opportunities

- Adoption of Smart, IoT-Enabled Pump Systems

The convergence of Industrial Internet of Things (IIoT) technology with centrifugal pump engineering is creating a compelling growth opportunity for market participants. Smart pumps embedded with sensors, real-time analytics, and remote monitoring capabilities enable predictive maintenance, significantly reducing unplanned downtime. Grundfos and Xylem Inc. have already launched connected pump platforms that integrate with cloud-based digital twins, allowing operators to optimize energy consumption in real time. The global industrial IoT market is projected by the International Telecommunication Union (ITU) to connect over 125 billion devices by 2030. Companies investing in intelligent pump ecosystems can differentiate their offerings, command premium pricing, and capture share in energy-efficiency-focused markets in Europe and North America, the latter supported by U.S. Department of Energy (DOE) pump efficiency standards under 10 CFR Part 431.

- Growing Demand from Middle East & Africa Desalination and Water Projects

The Middle East & Africa (MEA) region is emerging as the fastest-growing market for centrifugal pumps, driven by large-scale desalination and water infrastructure projects. The Gulf Cooperation Council (GCC) nations particularly Saudi Arabia, the UAE, and Kuwait are collectively investing tens of billions of dollars to expand desalination capacity, with Saudi Arabia's Vision 2030 earmarking water security as a national strategic priority. The International Desalination Association (IDA) notes that global desalination capacity surpassed 100 million m³/day in recent years, with a significant share located in the GCC. High-capacity centrifugal pumps are critical for seawater intake, brine management, and product water distribution in such plants, offering market players a sustained pipeline of procurement opportunities in this rapidly developing region.

Segmental Insights

- By Stage Analysis

The Single Stage segment holds the dominant share within the By Stage category, accounting for approximately 62% of the overall centrifugal pumps market in 2026. Single-stage centrifugal pumps are preferred for their mechanical simplicity, lower acquisition cost, ease of maintenance, and suitability for high-flow, low-to-moderate head applications. They are extensively employed in water supply systems, HVAC, irrigation, and general industrial process loops. According to the Hydraulic Institute, single-stage pumps represent the most widely installed pump type globally due to their versatility across operating conditions. The growing emphasis on energy-efficient water distribution systems in developing economies, combined with steady replacement cycles in established industrial hubs, continues to reinforce the segment's leading position in the global market.

- By Type Analysis

Among the three types Overhung Impeller, Between Bearing, and Vertically Suspended the Overhung Impeller segment commands the leading market share of approximately 48% in 2026. Overhung impeller pumps are characterized by their compact design, straightforward installation, and cost competitiveness, making them the go-to choice for light-to-medium duty applications in water treatment, chemical processing, HVAC, and food & beverage manufacturing. The American National Standards Institute (ANSI) and ISO 2858 standards govern their design parameters widely used across North America and Europe. Their broad compatibility with standard motor frames and widespread availability of spare parts further strengthen their adoption rate across both industrial and commercial end-users, cementing their leadership within the by type category.

- By Operation Type Analysis

The Electrical segment is the dominant operation type, capturing an estimated 74% share of the centrifugal pumps market in 2026. Electrically driven centrifugal pumps benefit from mature motor technology, widespread power grid infrastructure, and a broad range of drive options including variable-frequency drives (VFDs) that enhance part-load energy efficiency. The U.S. Department of Energy (DOE) reports that pumping systems account for roughly 20% of worldwide electricity consumption in industrial facilities, underscoring the scale of electric pump deployment. Increasing regulatory mandates on pump motor efficiency such as IE3 and IE4 standards under IEC 60034-30-1 are driving replacement of older units with high-efficiency electric pump systems, consolidating the segment's dominance.

- By End User Analysis

The Industrial end-user segment leads the centrifugal pumps market, representing approximately 68% of total demand in 2026. Industrial applications span oil & gas, chemical processing, power generation, mining, pulp & paper, and water & wastewater treatment all sectors that collectively operate millions of pump units globally. The International Energy Agency (IEA) highlights that motor systems including pumps are the single largest end-use of electricity in the industrial sector. Growing capital expenditure in refinery upgrades, LNG infrastructure, and process-plant expansions in Asia and the Middle East is translating into sustained procurement demand. The industrial segment's dominance is further reinforced by stringent process-reliability requirements that favor technologically advanced centrifugal pump solutions over alternative pump technologies.

Regional Insights

- North America Centrifugal Pumps Trends

North America remains a prominent and technologically mature market for centrifugal pumps, underpinned by ongoing infrastructure renewal, stringent regulatory standards, and a robust innovation ecosystem. U.S. leads regional demand, with the Infrastructure Investment and Jobs Act channeling billions into water and wastewater infrastructure improvements and an additional US$ 65 billion into the power grid. Energy efficiency standards enforced by the U.S. Department of Energy (DOE) under 10 CFR Part 431 mandate minimum efficiency levels for clean water pumps, compelling end-users to upgrade aging fleets.

Canada's expanding oil sands and mining activities also sustain demand for heavy-duty centrifugal pump solutions. Mexico is experiencing incremental growth driven by industrial development in the Bajío corridor and expanding municipal water treatment networks supported by the Comisión Nacional del Agua (CONAGUA). The region's emphasis on digital transformation including adoption of IIoT-enabled pump monitoring positions North American manufacturers and end-users at the forefront of smart pump technology innovation.

- Europe Centrifugal Pumps Trends

Germany leads the European centrifugal pumps market, driven by its expansive chemical, automotive, and energy sectors, along with a strong presence of global pump manufacturers including KSB SE & Co. KGaA and Wilo SE. The European Union's Ecodesign Regulation for Energy-Related Products mandates pump efficiency improvements across member states, driving replacement cycles toward premium, high-efficiency units. The U.K. water utility sector, under Ofwat's regulatory framework, continues to invest in network upgrades, sustaining centrifugal pump procurement activity.

France and Spain are witnessing growth in agricultural irrigation and water management infrastructure, particularly as both nations face heightened drought risks per assessments by the European Environment Agency (EEA). Europe's regulatory harmonization under CE marking and ATEX directives for hazardous-area pump installations ensures a consistent quality baseline, supporting premium product positioning by regional manufacturers and facilitating cross-border trade within the single market.

- Asia Pacific Centrifugal Pumps Trends

Asia Pacific commands approximately 49% of the global centrifugal pumps market, making it the undisputed leading region. China is the single largest national market, fueled by massive investments in water diversion projects such as the South-to-North Water Diversion Project, as well as rapid industrialization and power plant construction. The Ministry of Water Resources of China allocated over billions for water infrastructure from 2021 to 2025, directly stimulating centrifugal pump procurement.

India represents a high-growth sub-market, supported by the government's Jal Jeevan Mission a flagship program targeting universal piped water supply to all rural households by 2024 and expanding thermal and renewable power capacity. Japan's precision-engineering culture drives demand for technologically advanced, low-vibration centrifugal pump systems in semiconductor fabrication and pharmaceutical manufacturing. ASEAN economies including Vietnam, Indonesia, and Thailand are rapidly industrializing, generating incremental pump demand across manufacturing, agro-processing, and municipal water sectors.

Competitive Landscape

The global centrifugal pumps market is moderately consolidated, with multinational leaders Grundfos, Xylem Inc., Flowserve Corporation, Sulzer Ltd., and KSB SE & Co. KGaA collectively holding a significant revenue share alongside a long tail of regional manufacturers. Leading players differentiate through advanced hydraulic engineering, comprehensive aftermarket service networks, and digital pump management platforms. Strategic priorities include mergers and acquisitions to expand geographic footprint, heavy R&D investment in smart and energy-efficient pump technologies, and long-term service agreements with major industrial clients. Business models are increasingly shifting from transactional equipment sales toward pump-as-a-service (PaaS) and outcome-based maintenance contracts, enhancing customer retention and recurring revenue streams.

Key Developments

- In January 2025, Xylem Inc. announced the expansion of its Flygt brand smart pump portfolio with the launch of AI-driven predictive maintenance capabilities integrated into its Xylem Vue digital platform, targeting water utilities across North America and Europe.

- In October 2024, Grundfos unveiled its next-generation iSOLUTIONS intelligent pump system at IFAT Munich, featuring integrated IoT sensors and real-time energy optimization algorithms designed to reduce lifecycle energy costs by up to 30% in water treatment applications.

- In March 2024, Flowserve Corporation secured a major long-term service agreement with a leading Saudi Aramco refinery complex to supply and maintain high-pressure centrifugal pumps for crude oil processing and water injection operations in the Kingdom of Saudi Arabia, underscoring the strategic importance of the MEA region.

Companies Covered in Centrifugal Pumps Market

- Grundfos

- Xylem Inc.

- Flowserve Corporation

- Sulzer Ltd.

- KSB SE & Co. KGaA

- Ebara Corporation

- Wilo SE

- ITT Inc.

- Kirloskar Brothers Limited

- CIRCOR International Inc.

- Baker Hughes Company

- Alfa Laval

- Weir Group PLC

- SPX FLOW Inc.

- Pentair plc

- Goulds Water Technology (a Xylem brand)

- IDEX Corporation

- Torishima Pump Mfg. Co., Ltd.

- Roper Technologies, Inc.

- Colfax Corporation (CIRCOR parent)

Market Segmentation

By Stage

- Single Stage

- Multistage

By Type

- Overhung Impeller

- Between Bearing

- Vertically Suspended

By Operation Type

- Electrical

- Hydraulic

- Air-drive

By End User

- Industrial

- Commercial

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Executive Summary

- Global Centrifugal Pumps Market Snapshot

- Future Projections

- Key Market Trends

- Regional Snapshot, by Value, 2026

- Analyst Recommendations

- Market Overview

- Market Definitions and Segmentations

- Market Dynamics

- Drivers

- Restraints

- Market Opportunities

- Value Chain Analysis

- COVID-19 Impact Analysis

- Porter's Five Forces Analysis

- Impact of Russia-Ukraine Conflict

- PESTLE Analysis

- Regulatory Analysis

- Price Trend Analysis

- Current Prices and Future Projections, 2025-2033

- Price Impact Factors

- Global Centrifugal Pumps Market Outlook, 2020 - 2033

- Global Centrifugal Pumps Market Outlook, by Stage, Value (US$ Bn), 2020-2033

- Single Stage

- Multistage

- Global Centrifugal Pumps Market Outlook, by Type, Value (US$ Bn), 2020-2033

- Overhung Impeller

- Between Bearing

- Vertically Suspended

- Global Centrifugal Pumps Market Outlook, by Operation Type, Value (US$ Bn), 2020-2033

- Electrical

- Hydraulic

- Air-drive

- Global Centrifugal Pumps Market Outlook, by End User , Value (US$ Bn), 2020-2033

- Industrial

- Commercial

- Global Centrifugal Pumps Market Outlook, by Region, Value (US$ Bn), 2020-2033

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Global Centrifugal Pumps Market Outlook, by Stage, Value (US$ Bn), 2020-2033

- North America Centrifugal Pumps Market Outlook, 2020 - 2033

- North America Centrifugal Pumps Market Outlook, by Stage, Value (US$ Bn), 2020-2033

- Single Stage

- Multistage

- North America Centrifugal Pumps Market Outlook, by Type, Value (US$ Bn), 2020-2033

- Overhung Impeller

- Between Bearing

- Vertically Suspended

- North America Centrifugal Pumps Market Outlook, by Operation Type, Value (US$ Bn), 2020-2033

- Electrical

- Hydraulic

- Air-drive

- North America Centrifugal Pumps Market Outlook, by End User , Value (US$ Bn), 2020-2033

- Industrial

- Commercial

- North America Centrifugal Pumps Market Outlook, by Country, Value (US$ Bn), 2020-2033

- U.S. Centrifugal Pumps Market Outlook, by Stage, 2020-2033

- U.S. Centrifugal Pumps Market Outlook, by Type, 2020-2033

- U.S. Centrifugal Pumps Market Outlook, by Operation Type, 2020-2033

- U.S. Centrifugal Pumps Market Outlook, by End User , 2020-2033

- Canada Centrifugal Pumps Market Outlook, by Stage, 2020-2033

- Canada Centrifugal Pumps Market Outlook, by Type, 2020-2033

- Canada Centrifugal Pumps Market Outlook, by Operation Type, 2020-2033

- Canada Centrifugal Pumps Market Outlook, by End User , 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- North America Centrifugal Pumps Market Outlook, by Stage, Value (US$ Bn), 2020-2033

- Europe Centrifugal Pumps Market Outlook, 2020 - 2033

- Europe Centrifugal Pumps Market Outlook, by Stage, Value (US$ Bn), 2020-2033

- Single Stage

- Multistage

- Europe Centrifugal Pumps Market Outlook, by Type, Value (US$ Bn), 2020-2033

- Overhung Impeller

- Between Bearing

- Vertically Suspended

- Europe Centrifugal Pumps Market Outlook, by Operation Type, Value (US$ Bn), 2020-2033

- Electrical

- Hydraulic

- Air-drive

- Europe Centrifugal Pumps Market Outlook, by End User , Value (US$ Bn), 2020-2033

- Industrial

- Commercial

- Europe Centrifugal Pumps Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Germany Centrifugal Pumps Market Outlook, by Stage, 2020-2033

- Germany Centrifugal Pumps Market Outlook, by Type, 2020-2033

- Germany Centrifugal Pumps Market Outlook, by Operation Type, 2020-2033

- Germany Centrifugal Pumps Market Outlook, by End User , 2020-2033

- Italy Centrifugal Pumps Market Outlook, by Stage, 2020-2033

- Italy Centrifugal Pumps Market Outlook, by Type, 2020-2033

- Italy Centrifugal Pumps Market Outlook, by Operation Type, 2020-2033

- Italy Centrifugal Pumps Market Outlook, by End User , 2020-2033

- France Centrifugal Pumps Market Outlook, by Stage, 2020-2033

- France Centrifugal Pumps Market Outlook, by Type, 2020-2033

- France Centrifugal Pumps Market Outlook, by Operation Type, 2020-2033

- France Centrifugal Pumps Market Outlook, by End User , 2020-2033

- U.K. Centrifugal Pumps Market Outlook, by Stage, 2020-2033

- U.K. Centrifugal Pumps Market Outlook, by Type, 2020-2033

- U.K. Centrifugal Pumps Market Outlook, by Operation Type, 2020-2033

- U.K. Centrifugal Pumps Market Outlook, by End User , 2020-2033

- Spain Centrifugal Pumps Market Outlook, by Stage, 2020-2033

- Spain Centrifugal Pumps Market Outlook, by Type, 2020-2033

- Spain Centrifugal Pumps Market Outlook, by Operation Type, 2020-2033

- Spain Centrifugal Pumps Market Outlook, by End User , 2020-2033

- Russia Centrifugal Pumps Market Outlook, by Stage, 2020-2033

- Russia Centrifugal Pumps Market Outlook, by Type, 2020-2033

- Russia Centrifugal Pumps Market Outlook, by Operation Type, 2020-2033

- Russia Centrifugal Pumps Market Outlook, by End User , 2020-2033

- Rest of Europe Centrifugal Pumps Market Outlook, by Stage, 2020-2033

- Rest of Europe Centrifugal Pumps Market Outlook, by Type, 2020-2033

- Rest of Europe Centrifugal Pumps Market Outlook, by Operation Type, 2020-2033

- Rest of Europe Centrifugal Pumps Market Outlook, by End User , 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Europe Centrifugal Pumps Market Outlook, by Stage, Value (US$ Bn), 2020-2033

- Asia Pacific Centrifugal Pumps Market Outlook, 2020 - 2033

- Asia Pacific Centrifugal Pumps Market Outlook, by Stage, Value (US$ Bn), 2020-2033

- Single Stage

- Multistage

- Asia Pacific Centrifugal Pumps Market Outlook, by Type, Value (US$ Bn), 2020-2033

- Overhung Impeller

- Between Bearing

- Vertically Suspended

- Asia Pacific Centrifugal Pumps Market Outlook, by Operation Type, Value (US$ Bn), 2020-2033

- Electrical

- Hydraulic

- Air-drive

- Asia Pacific Centrifugal Pumps Market Outlook, by End User , Value (US$ Bn), 2020-2033

- Industrial

- Commercial

- Asia Pacific Centrifugal Pumps Market Outlook, by Country, Value (US$ Bn), 2020-2033

- China Centrifugal Pumps Market Outlook, by Stage, 2020-2033

- China Centrifugal Pumps Market Outlook, by Type, 2020-2033

- China Centrifugal Pumps Market Outlook, by Operation Type, 2020-2033

- China Centrifugal Pumps Market Outlook, by End User , 2020-2033

- Japan Centrifugal Pumps Market Outlook, by Stage, 2020-2033

- Japan Centrifugal Pumps Market Outlook, by Type, 2020-2033

- Japan Centrifugal Pumps Market Outlook, by Operation Type, 2020-2033

- Japan Centrifugal Pumps Market Outlook, by End User , 2020-2033

- South Korea Centrifugal Pumps Market Outlook, by Stage, 2020-2033

- South Korea Centrifugal Pumps Market Outlook, by Type, 2020-2033

- South Korea Centrifugal Pumps Market Outlook, by Operation Type, 2020-2033

- South Korea Centrifugal Pumps Market Outlook, by End User , 2020-2033

- India Centrifugal Pumps Market Outlook, by Stage, 2020-2033

- India Centrifugal Pumps Market Outlook, by Type, 2020-2033

- India Centrifugal Pumps Market Outlook, by Operation Type, 2020-2033

- India Centrifugal Pumps Market Outlook, by End User , 2020-2033

- Southeast Asia Centrifugal Pumps Market Outlook, by Stage, 2020-2033

- Southeast Asia Centrifugal Pumps Market Outlook, by Type, 2020-2033

- Southeast Asia Centrifugal Pumps Market Outlook, by Operation Type, 2020-2033

- Southeast Asia Centrifugal Pumps Market Outlook, by End User , 2020-2033

- Rest of SAO Centrifugal Pumps Market Outlook, by Stage, 2020-2033

- Rest of SAO Centrifugal Pumps Market Outlook, by Type, 2020-2033

- Rest of SAO Centrifugal Pumps Market Outlook, by Operation Type, 2020-2033

- Rest of SAO Centrifugal Pumps Market Outlook, by End User , 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Asia Pacific Centrifugal Pumps Market Outlook, by Stage, Value (US$ Bn), 2020-2033

- Latin America Centrifugal Pumps Market Outlook, 2020 - 2033

- Latin America Centrifugal Pumps Market Outlook, by Stage, Value (US$ Bn), 2020-2033

- Single Stage

- Multistage

- Latin America Centrifugal Pumps Market Outlook, by Type, Value (US$ Bn), 2020-2033

- Overhung Impeller

- Between Bearing

- Vertically Suspended

- Latin America Centrifugal Pumps Market Outlook, by Operation Type, Value (US$ Bn), 2020-2033

- Electrical

- Hydraulic

- Air-drive

- Latin America Centrifugal Pumps Market Outlook, by End User , Value (US$ Bn), 2020-2033

- Industrial

- Commercial

- Latin America Centrifugal Pumps Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Brazil Centrifugal Pumps Market Outlook, by Stage, 2020-2033

- Brazil Centrifugal Pumps Market Outlook, by Type, 2020-2033

- Brazil Centrifugal Pumps Market Outlook, by Operation Type, 2020-2033

- Brazil Centrifugal Pumps Market Outlook, by End User , 2020-2033

- Mexico Centrifugal Pumps Market Outlook, by Stage, 2020-2033

- Mexico Centrifugal Pumps Market Outlook, by Type, 2020-2033

- Mexico Centrifugal Pumps Market Outlook, by Operation Type, 2020-2033

- Mexico Centrifugal Pumps Market Outlook, by End User , 2020-2033

- Argentina Centrifugal Pumps Market Outlook, by Stage, 2020-2033

- Argentina Centrifugal Pumps Market Outlook, by Type, 2020-2033

- Argentina Centrifugal Pumps Market Outlook, by Operation Type, 2020-2033

- Argentina Centrifugal Pumps Market Outlook, by End User , 2020-2033

- Rest of LATAM Centrifugal Pumps Market Outlook, by Stage, 2020-2033

- Rest of LATAM Centrifugal Pumps Market Outlook, by Type, 2020-2033

- Rest of LATAM Centrifugal Pumps Market Outlook, by Operation Type, 2020-2033

- Rest of LATAM Centrifugal Pumps Market Outlook, by End User , 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Latin America Centrifugal Pumps Market Outlook, by Stage, Value (US$ Bn), 2020-2033

- Middle East & Africa Centrifugal Pumps Market Outlook, 2020 - 2033

- Middle East & Africa Centrifugal Pumps Market Outlook, by Stage, Value (US$ Bn), 2020-2033

- Single Stage

- Multistage

- Middle East & Africa Centrifugal Pumps Market Outlook, by Type, Value (US$ Bn), 2020-2033

- Overhung Impeller

- Between Bearing

- Vertically Suspended

- Middle East & Africa Centrifugal Pumps Market Outlook, by Operation Type, Value (US$ Bn), 2020-2033

- Electrical

- Hydraulic

- Air-drive

- Middle East & Africa Centrifugal Pumps Market Outlook, by End User , Value (US$ Bn), 2020-2033

- Industrial

- Commercial

- Middle East & Africa Centrifugal Pumps Market Outlook, by Country, Value (US$ Bn), 2020-2033

- GCC Centrifugal Pumps Market Outlook, by Stage, 2020-2033

- GCC Centrifugal Pumps Market Outlook, by Type, 2020-2033

- GCC Centrifugal Pumps Market Outlook, by Operation Type, 2020-2033

- GCC Centrifugal Pumps Market Outlook, by End User , 2020-2033

- South Africa Centrifugal Pumps Market Outlook, by Stage, 2020-2033

- South Africa Centrifugal Pumps Market Outlook, by Type, 2020-2033

- South Africa Centrifugal Pumps Market Outlook, by Operation Type, 2020-2033

- South Africa Centrifugal Pumps Market Outlook, by End User , 2020-2033

- Egypt Centrifugal Pumps Market Outlook, by Stage, 2020-2033

- Egypt Centrifugal Pumps Market Outlook, by Type, 2020-2033

- Egypt Centrifugal Pumps Market Outlook, by Operation Type, 2020-2033

- Egypt Centrifugal Pumps Market Outlook, by End User , 2020-2033

- Nigeria Centrifugal Pumps Market Outlook, by Stage, 2020-2033

- Nigeria Centrifugal Pumps Market Outlook, by Type, 2020-2033

- Nigeria Centrifugal Pumps Market Outlook, by Operation Type, 2020-2033

- Nigeria Centrifugal Pumps Market Outlook, by End User , 2020-2033

- Rest of Middle East Centrifugal Pumps Market Outlook, by Stage, 2020-2033

- Rest of Middle East Centrifugal Pumps Market Outlook, by Type, 2020-2033

- Rest of Middle East Centrifugal Pumps Market Outlook, by Operation Type, 2020-2033

- Rest of Middle East Centrifugal Pumps Market Outlook, by End User , 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Middle East & Africa Centrifugal Pumps Market Outlook, by Stage, Value (US$ Bn), 2020-2033

- Competitive Landscape

- Company Vs Segment Heatmap

- Company Market Share Analysis, 2025

- Competitive Dashboard

- Company Profiles

- Grundfos

- Company Overview

- Product Portfolio

- Financial Overview

- Business Strategies and Developments

- Xylem Inc.

- Flowserve Corporation

- Sulzer Ltd.

- KSB SE & Co. KGaA

- Ebara Corporation

- Wilo SE

- ITT Inc.

- Kirloskar Brothers Limited

- CIRCOR International Inc.

- Baker Hughes Company

- Alfa Laval

- Weir Group PLC

- SPX FLOW Inc.

- Pentair plc

- Grundfos

- Appendix

- Research Methodology

- Report Assumptions

- Acronyms and Abbreviations

|

BASE YEAR |

HISTORICAL DATA |

FORECAST PERIOD |

UNITS |

|||

|

2025 |

|

2020 - 2025 |

2026 - 2033 |

Value: US$ Million |

||

|

REPORT FEATURES |

DETAILS |

|

By Stage Coverage |

|

|

By Type Coverage |

|

|

Geographical Coverage |

|

|

Leading Companies |

|

|

Report Highlights |

Key Market Indicators, Macro-micro economic impact analysis, Technological Roadmap, Key Trends, Driver, Restraints, and Future Opportunities & Revenue Pockets, Porter’s 5 Forces Analysis, Historical Trend (2019-2024), Market Estimates and Forecast, Market Dynamics, Industry Trends, Competition Landscape, Category, Region, Country-wise Trends & Analysis, COVID-19 Impact Analysis (Demand and Supply Chain) |