Engineering Plastic Compounds Market Outlook

Global Engineering Plastic Compounds Market Thrives as Demand for Metal, Glass, and Ceramics Alternative Rises

An excellent alternative to metal, glass or even ceramics, engineering plastic compounds are being increasingly finding place in most demanding applications owing to their mechanical strength, heat resistance, and chemical attack resistance properties. As a result the global engineering plastic compounds market has wide scope for application in areas such as automotive and industrial, renewable energy, medical technology, and transport. Engineering plastic compounds encompasses several plastics under its umbrella, among which polyamide, polycarbonate, Styrenics (ABS & SAN), Poly butylene Terephthalate (PBT), Polyoxymethylene (POM), Polymethyl methacrylate (PMMA) and Thermoplastic Elastomers (TPE) are the most prominent one’s.

The Engineering Plastic Compounds Market is valued at USD 73.4 Bn in 2026 and is projected to reach USD 121 Bn, growing at a CAGR of 7% by 2033.The increasing trend for lightweight vehicles, increasing demand for connected vehicles and growing awareness about the reduction of vehicular emissions are driving the engineering plastics compound market in the automotive & transportation end-use industry.

Metals and glass are continuously being replaced by lighter materials because of continuous developments and property upgradation in the plastic industry. For instance, polyamides have replaced metal automotive gear shift module because of their lightweight and high-strength properties. Metal replacement is playing a very crucial role in the automotive industry to reduce vehicle weight, easy integration of parts, and decrease in total manufacturing costs. Owing to government regulations and concerns regarding fuel efficiency standards and consumer preferences for vehicles with high gas mileage, automobile manufacturers are focusing on enhancing fuel economy. Engineering plastic compounds are also used in electrical components of hybrid electric cars due to their favourable properties, for instance, high heat resistance.

Although there is a tremendous usage of engineering plastics resins in several industries, but its compounds are mostly in demand for high temperature applications such as automotive, industrial, aerospace, and electronics manufacturing. To process these EP resins into compounds the plastics are melted with additives, fillers, or reinforcers, which changes its physical, thermal, electrical, or aesthetic characteristics. Based on the addition of these additives several properties can be achieved including conductivity, flame retardance, wear resistance, structural, and precolored.

COVID-19 Impact on Global Engineering Plastic Compounds Market

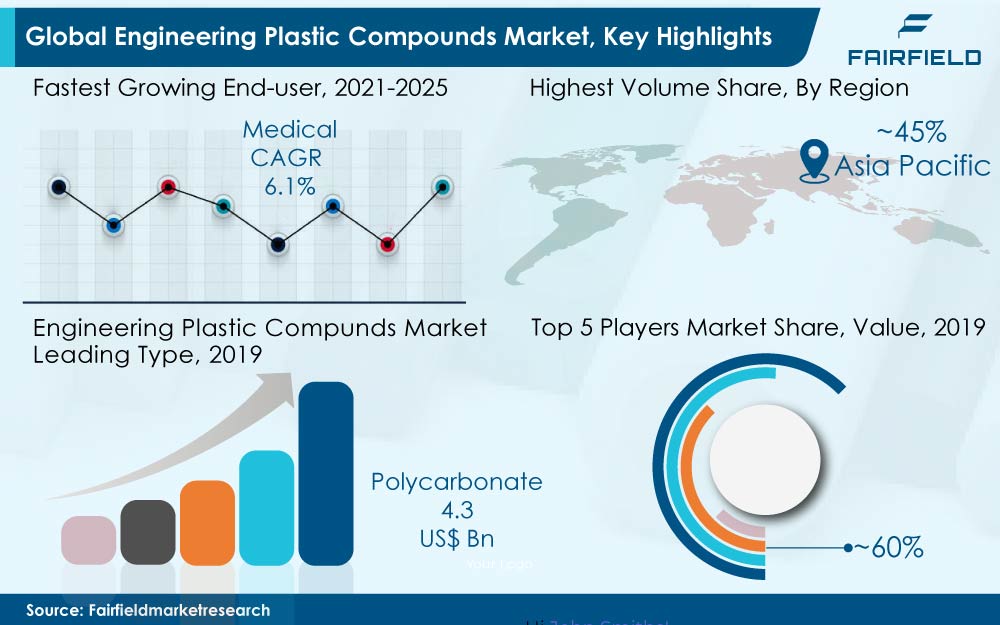

Medical devices and instruments are in a constant state of evolution, and with the current ongoing covid situation it has become essential to respond to trends within and outside the hospital premises to attain better care at lesser system costs. The trends toward miniaturization and compactness are driving new requirements in the medical industry. Hygiene and public health safety continue to receive strong consideration globally, demanding devices to withstand a range of chemicals and sterilization procedures. There was a time when reusability of a product was considered as a leap ahead advantage, but not any more in the medical industry, especially in orthopedics. The use of single-use products is the answer and is the latest trend in orthopedics application. This has forced the industry to go for plastic materials by which the cost can be reduced to an extent. Increasing client demands in sophisticated medical applications with high-performance materials and long-term preparation constancy, has impelled manufacturers to extend its portfolio of engineering plastics compounds for medical technology.

Increasing Demand for Engineering Plastic Compounds in Electric Vehicles Boosts Market

Engineering plastic compounds market has tremendous opportunity in the automotive sector. To reduce weight and achieve greater fuel efficiency, plastics are becoming immensely popular in automotive applications. Dozens of different plastics are used to make 2,000 or more parts of varying shapes and sizes, from lights and bumpers to engine components, dashboards, headrests, switches, clips, panoramic roofs, seats, airbags, and seat belts Several engineering plastics compounds such as polyamide, polycarbonate, and ABS together account for a substantial share in the automotive manufacturing. Apart from this, plastic usage has also imparted other benefits to the car manufacturers such as saving their overall investments. For instance, a nylon bracket that holds together components under the hood might have mounts and other features moulded right into it.

Engineering thermoplastics are apparently lighter and stronger than several metals such as aluminium, magnesium alloys, aluminium alloys and others, which are offering great potential to replace traditional metal parts. One of the most important drivers aiding the growth of engineering plastics compounds are unexplored opportunities of replacing metals not only in automobiles, but also in the application areas of household appliances, construction, and infrastructure, to list down a few. For example, nylon replacing metals in under-the-hood motor vehicle applications and polycarbonate in the construction, medical and consumer markets.

Avoided Emissions - Production Approach to be Adopted by Manufacturers to Curb Emissions

To achieve goals of sustainable manufacturing various manufacturers are privately investing in research organizations to develop a novel, eco-friendly, and closed-loop route for recycling engineering plastics. For instance, Exeter Advanced Technologies (X-AT) along with some industrial companies has developed a recycling process through solvolysis process. This process separates composites/plastic compounds into different components, such as fillers, fibres and resins, under specific temperatures and pressures for reuse in new applications. Further, companies such as Entec polymers are also offering post-consumer nylon products that are certified to UL’s most rigorous adherence standard for PCR based products. Mitsubishi Chemicals has developed a bio-based polycarbonate resin derived mainly from plant-based isosorbide, which has excellent durability, making possible its deployment in a wide variety of applications such as for optical, electronic equipment, automotive housings, interior and exterior decor.

'Avoided emissions' refers to the emissions related environmental benefits that occur downstream in the use phase of our products. While avoided emissions do not count toward any specific Science Based Targets, they result in reduced emissions for customers and end-users. For example, DSM Engineering Plastics provides products for packaging films in the food industry, which require effective oxygen barrier properties and high puncture resistance. These films play an important role in reducing food waste by protecting food during transport, retail, and consumer use, and extending shelf life. Reducing food waste diminishes the burden on the food production system, leading to significant avoided emissions. By adopting this production approach, companies can gain goodwill in the market and gain traction from customers as well end users.

China and India - Driving the Engineering Plastic Compounds Industry, Globally

Asia Pacific region holds the largest share of more than 45% in the engineering plastics compound market owing to rapidly growing economies such as China and India, and ASEAN countries including Malaysia and Thailand. The major factor driving their growth is the increasing investments due to the high consumption of engineering plastic compounds. Owing to the increase in disposable income, the consumer buying pattern has changed; it has been influenced by globalization and westernization. These countries are also attracting attention of foreign investors to set up manufacturing plants and generate employment and revenue in the countries. This has created many opportunities for global manufacturers to set up their plants in the emerging economies.

The increasing population in Asia Pacific is boosting the demand in end-use industries, such as automotive & transportation, electrical & electronics, consumer appliances, and building & construction. The growth of the automotive industry has resulted in increased demand for engineering plastics compound. The booming electrical & electronics sector is also driving the growth of the engineering plastics compound market.

Top 8 Companies Hold About 60% Share in the Global Engineering Plastics Compounds Market

The key companies operating the global engineering plastic compounds market are BASF SE, Idemitsu Kosan Company Ltd., SABIC, Asahi Kasei Advance Corporation, Lanxess AG, and Covestro AG, among others. According to Fairfield Analysis, the top eight companies hold about 60% share in the engineering plastics compounds market. These companies are continuously developing their product portfolio to meet the increasing demand from automotive, building and construction, and electronics industries. Further, these companies are also expanding their production base with heavy investments concentrating in Asia Pacific countries owing to easy access to raw materials, and low labour and technology cost.

Above companies together hold compounding capacity of more than 2.6 million tons of products such as PBT compounds, polycarbonate compounds, TPE compounds, polyamide compounds, and ABS compounds. Other key players operating in the market includes Trinseo, Kraiburg TPE, Radici Plastics, Petrochemical Conversion Company (PCC), Chevron Philips, Repsol, and Polyone Corporation, among others. These companies jointly have production capacities of around 11.3 million tonnes.

The Global Engineering Plastics Compounds Market is Segmented as Below:

Type Coverage

- Polycarbonate

- Polyamide

- Polymethyl Methacrylate

- Polyoxymethylene

- Polybutylene Terephthalate

- Acrylonitrile Butadiene Styrene

- Styrene-Acrylonitrile

- Thermoplastic Elastomer

- Misc. (UHMWPE, LCP ASA, PI, PVDF, etc.)

End Use Industry Coverage

- Automotive

- Aerospace

- Electrical and electronics

- Building and construction

- Consumer goods and appliances

- Medical

- (Packaging, Industrial applications, etc.)

Geographical Coverage

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Spain

- Italy

- Poland

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- Thailand

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Leading Companies

- BASF

- SABIC

- Idemitsu

- Asahi Kasei Engineering Plastics

- Elix Polymer

- Lanxess

- Siko Polymers

- Bhansali Engineers Polymer Ltd.

- Polyplastics

- Covestro

- Ineos Styrosolution

- Celanese Corporation

- Others

Inside This Report You Will Find:

1. Executive Summary

2. Market Overview

3. Global Production Capacity Analysis

4. Price Trends Analysis and Future Projects 2017 - 2025

5. Global Engineering Plastic Compounds Market Outlook 2017 - 2025

6. North America Engineering Plastic Compounds Market Outlook 2017 - 2025

7. Europe Engineering Plastic Compounds Market Outlook 2017 - 2025

8. Asia Pacific Engineering Plastic Compounds Market Outlook 2017 - 2025

9. Latin America Engineering Plastic Compounds Market Outlook 2017 - 2025

10. Middle East & Africa Engineering Plastic Compounds Market Outlook 2017 - 2025

11. Competitive Landscape

12. Appendix

Post Sale Support, Research Updates & Offerings:

We value the trust shown by our customers in Fairfield Market Research. We support our clients through our post sale support, research updates and offerings.

- The report will be prepared in a PPT format and will be delivered in a PDF format.

- Additionally, Market Estimation and Forecast numbers will be shared in Excel Workbook.

- If a report being sold was published over a year ago, we will offer a complimentary copy of the updated research report along with Market Estimation and Forecast numbers within 2-3 weeks’ time of the sale.

- If we update this research study within the next 2 quarters, post purchase of the report, we will offer a Complimentary copy of the updated Market Estimation and Forecast numbers in Excel Workbook.

- If there is a geopolitical conflict, pandemic, recession, and the like which can impact global economic scenario and business activity, which might entirely alter the market dynamics or future projections in the industry, we will create a Research Update upon your request at a nominal charge.

- Executive Summary

- Global Engineering Plastic Compounds Market Snapshot

- Future Projections

- Key Market Trends

- Regional Snapshot, by Value, 2026

- Analyst Recommendations

- Market Overview

- Market Definitions and Segmentations

- Market Dynamics

- Drivers

- Restraints

- Market Opportunities

- Value Chain Analysis

- COVID-19 Impact Analysis

- Porter's Fiver Forces Analysis

- Impact of Russia-Ukraine Conflict

- PESTLE Analysis

- Regulatory Analysis

- Price Trend Analysis

- Current Prices and Future Projections, 2025-2033

- Price Impact Factors

- Global Engineering Plastic Compounds Market Outlook, 2020 - 2033

- Global Engineering Plastic Compounds Market Outlook, by Type Coverage, Value (US$ Bn), 2020-2033

- Polycarbonate

- Polyamide

- Polyamide

- Polyoxymethylene

- Polybutylene Terephthalate

- Acrylonitrile Butadiene Styrene

- Styrene-Acrylonitrile

- Thermoplastic Elastomer

- (UHMWPE, LCP ASA, PI, PVDF

- Global Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, Value (US$ Bn), 2020-2033

- Automotive

- Aerospace

- Electrical and electronics

- Building and construction

- Consumer goods and appliances

- Medical

- (Packaging, Industrial applications, etc.)

- Global Engineering Plastic Compounds Market Outlook, by Region, Value (US$ Bn), 2020-2033

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Global Engineering Plastic Compounds Market Outlook, by Type Coverage, Value (US$ Bn), 2020-2033

- North America Engineering Plastic Compounds Market Outlook, 2020 - 2033

- North America Engineering Plastic Compounds Market Outlook, by Type Coverage, Value (US$ Bn), 2020-2033

- Polycarbonate

- Polyamide

- Polyamide

- Polyoxymethylene

- Polybutylene Terephthalate

- Acrylonitrile Butadiene Styrene

- Styrene-Acrylonitrile

- Thermoplastic Elastomer

- (UHMWPE, LCP ASA, PI, PVDF

- North America Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, Value (US$ Bn), 2020-2033

- Automotive

- Aerospace

- Electrical and electronics

- Building and construction

- Consumer goods and appliances

- Medical

- (Packaging, Industrial applications, etc.)

- North America Engineering Plastic Compounds Market Outlook, by Country, Value (US$ Bn), 2020-2033

- S. Engineering Plastic Compounds Market Outlook, by Type Coverage, 2020-2033

- S. Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, 2020-2033

- Canada Engineering Plastic Compounds Market Outlook, by Type Coverage, 2020-2033

- Canada Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- North America Engineering Plastic Compounds Market Outlook, by Type Coverage, Value (US$ Bn), 2020-2033

- Europe Engineering Plastic Compounds Market Outlook, 2020 - 2033

- Europe Engineering Plastic Compounds Market Outlook, by Type Coverage, Value (US$ Bn), 2020-2033

- Polycarbonate

- Polyamide

- Polyamide

- Polyoxymethylene

- Polybutylene Terephthalate

- Acrylonitrile Butadiene Styrene

- Styrene-Acrylonitrile

- Thermoplastic Elastomer

- (UHMWPE, LCP ASA, PI, PVDF

- Europe Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, Value (US$ Bn), 2020-2033

- Automotive

- Aerospace

- Electrical and electronics

- Building and construction

- Consumer goods and appliances

- Medical

- (Packaging, Industrial applications, etc.)

- Europe Engineering Plastic Compounds Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Germany Engineering Plastic Compounds Market Outlook, by Type Coverage, 2020-2033

- Germany Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, 2020-2033

- Italy Engineering Plastic Compounds Market Outlook, by Type Coverage, 2020-2033

- Italy Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, 2020-2033

- France Engineering Plastic Compounds Market Outlook, by Type Coverage, 2020-2033

- France Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, 2020-2033

- K. Engineering Plastic Compounds Market Outlook, by Type Coverage, 2020-2033

- K. Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, 2020-2033

- Spain Engineering Plastic Compounds Market Outlook, by Type Coverage, 2020-2033

- Spain Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, 2020-2033

- Russia Engineering Plastic Compounds Market Outlook, by Type Coverage, 2020-2033

- Russia Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, 2020-2033

- Rest of Europe Engineering Plastic Compounds Market Outlook, by Type Coverage, 2020-2033

- Rest of Europe Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Europe Engineering Plastic Compounds Market Outlook, by Type Coverage, Value (US$ Bn), 2020-2033

- Asia Pacific Engineering Plastic Compounds Market Outlook, 2020 - 2033

- Asia Pacific Engineering Plastic Compounds Market Outlook, by Type Coverage, Value (US$ Bn), 2020-2033

- Polycarbonate

- Polyamide

- Polyamide

- Polyoxymethylene

- Polybutylene Terephthalate

- Acrylonitrile Butadiene Styrene

- Styrene-Acrylonitrile

- Thermoplastic Elastomer

- (UHMWPE, LCP ASA, PI, PVDF

- Asia Pacific Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, Value (US$ Bn), 2020-2033

- Automotive

- Aerospace

- Electrical and electronics

- Building and construction

- Consumer goods and appliances

- Medical

- (Packaging, Industrial applications, etc.)

- Asia Pacific Engineering Plastic Compounds Market Outlook, by Country, Value (US$ Bn), 2020-2033

- China Engineering Plastic Compounds Market Outlook, by Type Coverage, 2020-2033

- China Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, 2020-2033

- Japan Engineering Plastic Compounds Market Outlook, by Type Coverage, 2020-2033

- Japan Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, 2020-2033

- South Korea Engineering Plastic Compounds Market Outlook, by Type Coverage, 2020-2033

- South Korea Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, 2020-2033

- India Engineering Plastic Compounds Market Outlook, by Type Coverage, 2020-2033

- India Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, 2020-2033

- Southeast Asia Engineering Plastic Compounds Market Outlook, by Type Coverage, 2020-2033

- Southeast Asia Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, 2020-2033

- Rest of SAO Engineering Plastic Compounds Market Outlook, by Type Coverage, 2020-2033

- Rest of SAO Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Asia Pacific Engineering Plastic Compounds Market Outlook, by Type Coverage, Value (US$ Bn), 2020-2033

- Latin America Engineering Plastic Compounds Market Outlook, 2020 - 2033

- Latin America Engineering Plastic Compounds Market Outlook, by Type Coverage, Value (US$ Bn), 2020-2033

- Polycarbonate

- Polyamide

- Polyamide

- Polyoxymethylene

- Polybutylene Terephthalate

- Acrylonitrile Butadiene Styrene

- Styrene-Acrylonitrile

- Thermoplastic Elastomer

- (UHMWPE, LCP ASA, PI, PVDF

- Latin America Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, Value (US$ Bn), 2020-2033

- Automotive

- Aerospace

- Electrical and electronics

- Building and construction

- Consumer goods and appliances

- Medical

- (Packaging, Industrial applications, etc.)

- Latin America Engineering Plastic Compounds Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Brazil Engineering Plastic Compounds Market Outlook, by Type Coverage, 2020-2033

- Brazil Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, 2020-2033

- Mexico Engineering Plastic Compounds Market Outlook, by Type Coverage, 2020-2033

- Mexico Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, 2020-2033

- Argentina Engineering Plastic Compounds Market Outlook, by Type Coverage, 2020-2033

- Argentina Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, 2020-2033

- Rest of LATAM Engineering Plastic Compounds Market Outlook, by Type Coverage, 2020-2033

- Rest of LATAM Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Latin America Engineering Plastic Compounds Market Outlook, by Type Coverage, Value (US$ Bn), 2020-2033

- Middle East & Africa Engineering Plastic Compounds Market Outlook, 2020 - 2033

- Middle East & Africa Engineering Plastic Compounds Market Outlook, by Type Coverage, Value (US$ Bn), 2020-2033

- Polycarbonate

- Polyamide

- Polyamide

- Polyoxymethylene

- Polybutylene Terephthalate

- Acrylonitrile Butadiene Styrene

- Styrene-Acrylonitrile

- Thermoplastic Elastomer

- (UHMWPE, LCP ASA, PI, PVDF

- Middle East & Africa Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, Value (US$ Bn), 2020-2033

- Automotive

- Aerospace

- Electrical and electronics

- Building and construction

- Consumer goods and appliances

- Medical

- (Packaging, Industrial applications, etc.)

- Middle East & Africa Engineering Plastic Compounds Market Outlook, by Country, Value (US$ Bn), 2020-2033

- GCC Engineering Plastic Compounds Market Outlook, by Type Coverage, 2020-2033

- GCC Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, 2020-2033

- South Africa Engineering Plastic Compounds Market Outlook, by Type Coverage, 2020-2033

- South Africa Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, 2020-2033

- Egypt Engineering Plastic Compounds Market Outlook, by Type Coverage, 2020-2033

- Egypt Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, 2020-2033

- Nigeria Engineering Plastic Compounds Market Outlook, by Type Coverage, 2020-2033

- Nigeria Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, 2020-2033

- Rest of Middle East Engineering Plastic Compounds Market Outlook, by Type Coverage, 2020-2033

- Rest of Middle East Engineering Plastic Compounds Market Outlook, by End Use Industry Coverage, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Middle East & Africa Engineering Plastic Compounds Market Outlook, by Type Coverage, Value (US$ Bn), 2020-2033

- Competitive Landscape

- Company Vs Segment Heatmap

- Company Market Share Analysis, 2025

- Competitive Dashboard

- Company Profiles

- BASF

- Company Overview

- Product Portfolio

- Financial Overview

- Business Strategies and Developments

- SABIC

- Idemitsu

- Asahi Kasei Engineering Plastics

- Elix Polymer

- Lanxess

- Siko Polymers

- Bhansali Engineers Polymer Ltd.

- Polyplastics

- Covestro

- BASF

- Appendix

- Research Methodology

- Report Assumptions

- Acronyms and Abbreviations

|

BASE YEAR |

HISTORICAL DATA |

FORECAST PERIOD |

UNITS |

|||

|

2025 |

|

2019 - 2024 |

|

2026 - 2033 |

Value: US$ Billion |

|

REPORT FEATURES |

DETAILS |

|

Type Coverage |

|

|

End Use Industry Coverage |

|

|

Geographical Coverage |

|

|

Leading Companies |

|

|

Report Highlights |

Market Estimates and Forecast, Market Dynamics, Industry Trends, Competition Landscape, Porters Five Forces Analysis, Factorization Analysis, Type-, End Use Industry-, Region-, Country-wise Trends & Analysis, COVID-19 Impact Analysis (Demand), Key Trends |