Biosolids Market Outlook

Global Biosolids Market Presents Effective Solution for Reusing Waste Material

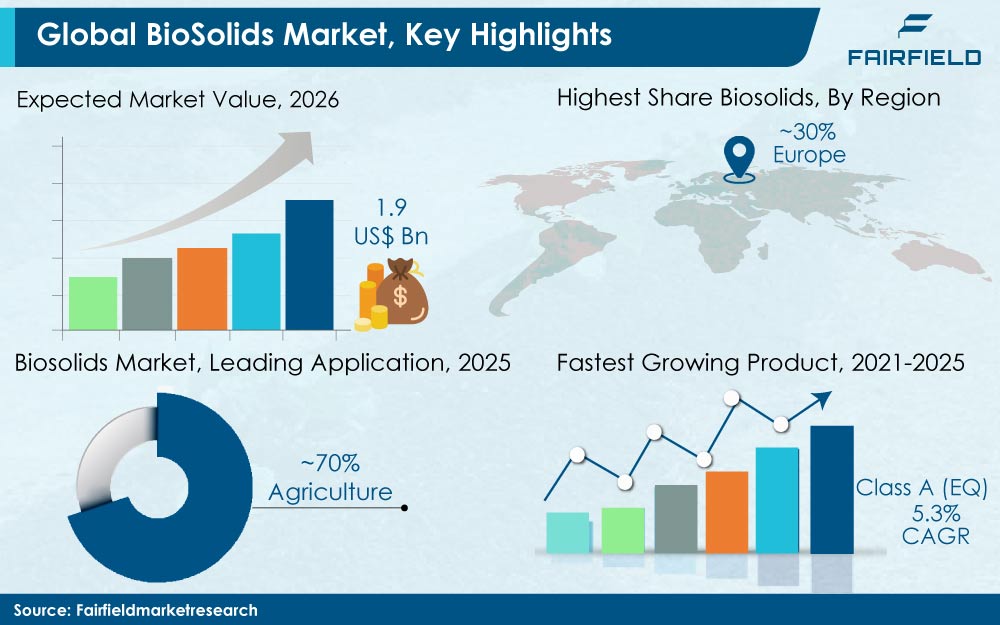

The Biosolids Market is valued at USD 3 Bn in 2026 and is projected to reach USD 5.4 Bn, growing at a CAGR of 9% by 2033.It is estimated that around 80% (90% in developing countries) of the wastewater, worldwide, is released into the environment untreated. Wastewater sewage contains nutrients that can be used for agriculture purpose. As the resources around the world become scarce and expensive, it is important to convert wastewater into a beneficial asset. Biosolids, organic materials derived from the wastewater treatment of domestic and industrial sewage sludge, have gathered a significant movement as an alternative to dispose of digested municipal sludge.

It is estimated that more than 35 million tonnes of biosolids were produced (for beneficial use) around the globe in the year 2018. Europe alone accounted for more than 25% of the global consumption in 2018. European Commission and European Governments have supported biosolids as best environmental solutions for waste disposal. The U.S., largest producer in North America, consumes most of the biosolids for land application. All of these findings indicate that the global biosolids market is slated to witness exponential rise in the coming years.

Countries in Asia Pacific region such as China and India are investing in the development of sludge management strategies and selecting better routes for sludge treatment and disposal instead of adopting landfilling and incineration. China is projected to surpass North America in the coming years as the country has invested heavily in wastewater treatment technologies for environmental protection.

Class A and Class A (EQ) to Account for 50% Share in Global Biosolids Market

Based upon regulations, biosolids can be classified as Class A, Class B, and Class A (EQ). Class A biosolids are free of pathogens and can be used in applications where public contact is likely. Class A meets the standards set by governing bodies such as the U.S. EPA. On the other hand, Class B has low level of pathogens and is used in agricultural or land reclamation applications. However, due to bad odour, high vector attraction, and pathogens there is significant shift of customers from Class B to Class A and Class A (EQ). Together, they are expected to account for more than 50% of the total biosolids market by the end of forecast period. Furthermore, Class B also attracts a lot of attention from regulatory authorities and cannot be applied in home lawns and gardens.

In terms of consumption, agriculture accounted for more than 60% of the biosolids market in 2018. For their high nutrition value, containing micro and macro nutrients, biosolids in agriculture are used as fertilizers, soil replacement products or a soil conditioner. Other key applications of biosolids include forestry and landscaping, land reclamation, construction materials, and heat generation.

Government Backs Biosolids Management Program for Circular Economy

Foremost factor supporting the rising consumption of biosolids is increasing pressure from regulatory bodies to phase out landfilling, stringent regulations on wastewater, sewage treatment, and waste disposal. The European Union (EU) and the U.S. Government is closely scrutinizing landfill and incineration aspects and imposition of strict laws. Biosolids in land application offers greenhouse gas benefits with carbon recycling and nourishing vegetation for further CO2 capture. Biosolids have a major role to play in circular economies. The recycling of biosolids into agriculture is recognised by the U.K. Government and EU as the best environmental option.

The global biosolids market makes a valid case for eliminating the need for commercial fertilizers. There is a growing trend towards the use of biosolids in amenity horticulture (floriculture, greenhouse container, arboriculture, etc.). Biosolids offers various benefits such as reducing the dependency on synthetic fertilizers, lower greenhouse emissions, improve water holding capacity, and improve soil structure. Biosolids are also expected to play an important role in treatment and reclamation of former mining sites as they can upgrade the mined land and assist in vegetation establishment.

Malodour Creates Negative Publicity for Global Biosolids Market

In the past few years, malodour from biosolids has become a bothersome aspect in customer perception. Organizations such as EPA are emphasizing on need to get better support from the public to make these biosolids programs a successful model. Effectively and safely managing biosolids is also a major challenge for the community as they are produced in large quantities. Public and other stakeholders must understand that biosolids are the product of modern sanitation and are not optional. Treatment and disposal of wastewater solids is key to sanitation and waste management.

Transportation (and the cost of moving) of disposal water/waste and difficulties in raising capital for new plants are few factors likely to restrict the market growth.

Synergies with Fertilizer Companies Opens New Avenues for Biosolids Manufacturers

Companies operating in the global biosolids market such as Cleanaway, SUEZ, Veolia, and Thames Water have integrated business operations. These companies offer end-to-end business solutions and hold strong positions in their respective regions. Companies are also coming up new strategies to form a partnership with fertilizer companies to develop new application avenues.

In 2019, Aries Clean Energy received approvals for its world’s first large scale biosolids gasification plant. This will convert waste into renewable energy and biochar. With the need of cost competitive technologies and innovation, many companies are expected to come up with disruptive technologies over the next few years to come. Companies in the U.S such as Mannco are focused on developing new technologies to produce low cost, energy efficient and exceptional quality (EQ) biosolids.

The Global Biosolids Market is Segmented as Below:

Product Coverage

- Class A

- Class B

- Class A (EQ)

Application Coverage

- Agriculture

- Forestry

- Land Reclamation

- (Construction Materials, Energy Generation etc.)

Geographical Coverage

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia and New Zealand

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Egypt

- Rest of Middle East & Africa

Leading Companies

- SUEZ

- Veolia Environnement S.A.

- Severn Trent Water

- Cambi

- Black & Veatch

- Cleanaway

- Englobe Corporation

- Casella Waste Systems Inc.

- FCC Group

- Remondis SE & Co. KG

- Executive Summary

- Global Biosolids Market Snapshot

- Future Projections

- Key Market Trends

- Regional Snapshot, by Value, 2026

- Analyst Recommendations

- Market Overview

- Market Definitions and Segmentations

- Market Dynamics

- Drivers

- Restraints

- Market Opportunities

- Value Chain Analysis

- COVID-19 Impact Analysis

- Porter's Fiver Forces Analysis

- Impact of Russia-Ukraine Conflict

- PESTLE Analysis

- Regulatory Analysis

- Price Trend Analysis

- Current Prices and Future Projections, 2025-2033

- Price Impact Factors

- Global Biosolids Market Outlook, 2020 - 2033

- Global Biosolids Market Outlook, by Product Coverage, Value (US$ Bn), 2020-2033

- Class A

- Class B

- Class A (EQ)

- Global Biosolids Market Outlook, by Application Coverage, Value (US$ Bn), 2020-2033

- Agriculture

- Forestry

- Land Reclamation (Construction Materials, Energy Generation etc.)

- Global Biosolids Market Outlook, by Region, Value (US$ Bn), 2020-2033

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Global Biosolids Market Outlook, by Product Coverage, Value (US$ Bn), 2020-2033

- North America Biosolids Market Outlook, 2020 - 2033

- North America Biosolids Market Outlook, by Product Coverage, Value (US$ Bn), 2020-2033

- Class A

- Class B

- Class A (EQ)

- North America Biosolids Market Outlook, by Application Coverage, Value (US$ Bn), 2020-2033

- Agriculture

- Forestry

- Land Reclamation (Construction Materials, Energy Generation etc.)

- North America Biosolids Market Outlook, by Country, Value (US$ Bn), 2020-2033

- S. Biosolids Market Outlook, by Product Coverage, 2020-2033

- S. Biosolids Market Outlook, by Application Coverage, 2020-2033

- Canada Biosolids Market Outlook, by Product Coverage, 2020-2033

- Canada Biosolids Market Outlook, by Application Coverage, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- North America Biosolids Market Outlook, by Product Coverage, Value (US$ Bn), 2020-2033

- Europe Biosolids Market Outlook, 2020 - 2033

- Europe Biosolids Market Outlook, by Product Coverage, Value (US$ Bn), 2020-2033

- Class A

- Class B

- Class A (EQ)

- Europe Biosolids Market Outlook, by Application Coverage, Value (US$ Bn), 2020-2033

- Agriculture

- Forestry

- Land Reclamation (Construction Materials, Energy Generation etc.)

- Europe Biosolids Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Germany Biosolids Market Outlook, by Product Coverage, 2020-2033

- Germany Biosolids Market Outlook, by Application Coverage, 2020-2033

- Italy Biosolids Market Outlook, by Product Coverage, 2020-2033

- Italy Biosolids Market Outlook, by Application Coverage, 2020-2033

- France Biosolids Market Outlook, by Product Coverage, 2020-2033

- France Biosolids Market Outlook, by Application Coverage, 2020-2033

- K. Biosolids Market Outlook, by Product Coverage, 2020-2033

- K. Biosolids Market Outlook, by Application Coverage, 2020-2033

- Spain Biosolids Market Outlook, by Product Coverage, 2020-2033

- Spain Biosolids Market Outlook, by Application Coverage, 2020-2033

- Russia Biosolids Market Outlook, by Product Coverage, 2020-2033

- Russia Biosolids Market Outlook, by Application Coverage, 2020-2033

- Rest of Europe Biosolids Market Outlook, by Product Coverage, 2020-2033

- Rest of Europe Biosolids Market Outlook, by Application Coverage, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Europe Biosolids Market Outlook, by Product Coverage, Value (US$ Bn), 2020-2033

- Asia Pacific Biosolids Market Outlook, 2020 - 2033

- Asia Pacific Biosolids Market Outlook, by Product Coverage, Value (US$ Bn), 2020-2033

- Class A

- Class B

- Class A (EQ)

- Asia Pacific Biosolids Market Outlook, by Application Coverage, Value (US$ Bn), 2020-2033

- Agriculture

- Forestry

- Land Reclamation (Construction Materials, Energy Generation etc.)

- Asia Pacific Biosolids Market Outlook, by Country, Value (US$ Bn), 2020-2033

- China Biosolids Market Outlook, by Product Coverage, 2020-2033

- China Biosolids Market Outlook, by Application Coverage, 2020-2033

- Japan Biosolids Market Outlook, by Product Coverage, 2020-2033

- Japan Biosolids Market Outlook, by Application Coverage, 2020-2033

- South Korea Biosolids Market Outlook, by Product Coverage, 2020-2033

- South Korea Biosolids Market Outlook, by Application Coverage, 2020-2033

- India Biosolids Market Outlook, by Product Coverage, 2020-2033

- India Biosolids Market Outlook, by Application Coverage, 2020-2033

- Southeast Asia Biosolids Market Outlook, by Product Coverage, 2020-2033

- Southeast Asia Biosolids Market Outlook, by Application Coverage, 2020-2033

- Rest of SAO Biosolids Market Outlook, by Product Coverage, 2020-2033

- Rest of SAO Biosolids Market Outlook, by Application Coverage, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Asia Pacific Biosolids Market Outlook, by Product Coverage, Value (US$ Bn), 2020-2033

- Latin America Biosolids Market Outlook, 2020 - 2033

- Latin America Biosolids Market Outlook, by Product Coverage, Value (US$ Bn), 2020-2033

- Class A

- Class B

- Class A (EQ)

- Latin America Biosolids Market Outlook, by Application Coverage, Value (US$ Bn), 2020-2033

- Agriculture

- Forestry

- Land Reclamation (Construction Materials, Energy Generation etc.)

- Latin America Biosolids Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Brazil Biosolids Market Outlook, by Product Coverage, 2020-2033

- Brazil Biosolids Market Outlook, by Application Coverage, 2020-2033

- Mexico Biosolids Market Outlook, by Product Coverage, 2020-2033

- Mexico Biosolids Market Outlook, by Application Coverage, 2020-2033

- Argentina Biosolids Market Outlook, by Product Coverage, 2020-2033

- Argentina Biosolids Market Outlook, by Application Coverage, 2020-2033

- Rest of LATAM Biosolids Market Outlook, by Product Coverage, 2020-2033

- Rest of LATAM Biosolids Market Outlook, by Application Coverage, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Latin America Biosolids Market Outlook, by Product Coverage, Value (US$ Bn), 2020-2033

- Middle East & Africa Biosolids Market Outlook, 2020 - 2033

- Middle East & Africa Biosolids Market Outlook, by Product Coverage, Value (US$ Bn), 2020-2033

- Class A

- Class B

- Class A (EQ)

- Middle East & Africa Biosolids Market Outlook, by Application Coverage, Value (US$ Bn), 2020-2033

- Agriculture

- Forestry

- Land Reclamation (Construction Materials, Energy Generation etc.)

- Middle East & Africa Biosolids Market Outlook, by Country, Value (US$ Bn), 2020-2033

- GCC Biosolids Market Outlook, by Product Coverage, 2020-2033

- GCC Biosolids Market Outlook, by Application Coverage, 2020-2033

- South Africa Biosolids Market Outlook, by Product Coverage, 2020-2033

- South Africa Biosolids Market Outlook, by Application Coverage, 2020-2033

- Egypt Biosolids Market Outlook, by Product Coverage, 2020-2033

- Egypt Biosolids Market Outlook, by Application Coverage, 2020-2033

- Nigeria Biosolids Market Outlook, by Product Coverage, 2020-2033

- Nigeria Biosolids Market Outlook, by Application Coverage, 2020-2033

- Rest of Middle East Biosolids Market Outlook, by Product Coverage, 2020-2033

- Rest of Middle East Biosolids Market Outlook, by Application Coverage, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Middle East & Africa Biosolids Market Outlook, by Product Coverage, Value (US$ Bn), 2020-2033

- Competitive Landscape

- Company Vs Segment Heatmap

- Company Market Share Analysis, 2025

- Competitive Dashboard

- Company Profiles

- SUEZ

- Company Overview

- Product Portfolio

- Financial Overview

- Business Strategies and Developments

- Veolia Environnement S.A.

- Severn Trent Water

- Cambi

- Black & Veatch

- Cleanaway

- Englobe Corporation

- Casella Waste Systems Inc.

- FCC Group

- Remondis SE & Co. KG

- SUEZ

- Appendix

- Research Methodology

- Report Assumptions

- Acronyms and Abbreviations

|

BASE YEAR |

HISTORICAL DATA |

FORECAST PERIOD |

UNITS |

|||

|

2015 |

2019 - 2014 |

2026 - 2033 |

Value: US$ Million |

|||

|

REPORT FEATURES |

DETAILS |

|

Product Coverage |

|

|

Application Coverage |

|

|

Geographical Coverage |

|

|

Leading Companies |

|

|

Report Highlights |

Market Estimates and Forecast, Market Dynamics, Industry Trends, Competition Landscape, Product-, Application-, Region-, Country-wise Trends & Analysis, COVID-19 Impact Analysis (Demand and Supply), Key Trends |