Hair Extension Market

Global Hair Extension Industry Analysis, Size, Share, Growth, Trends, and Forecast 2026-2033 – (By Product Type ,By Packaging Type, By Distribution Channel, By Geographic Coverage and By Company)

Global Hair Extension Market: Comprehensive Strategic Analysis

Executive Summary & Key Highlights

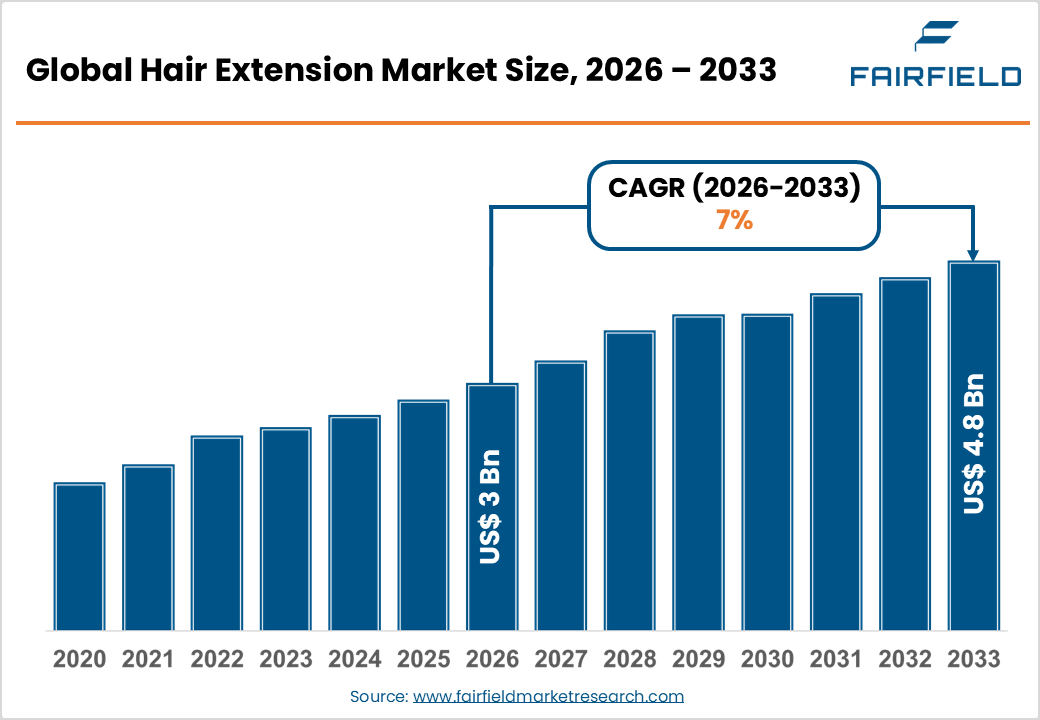

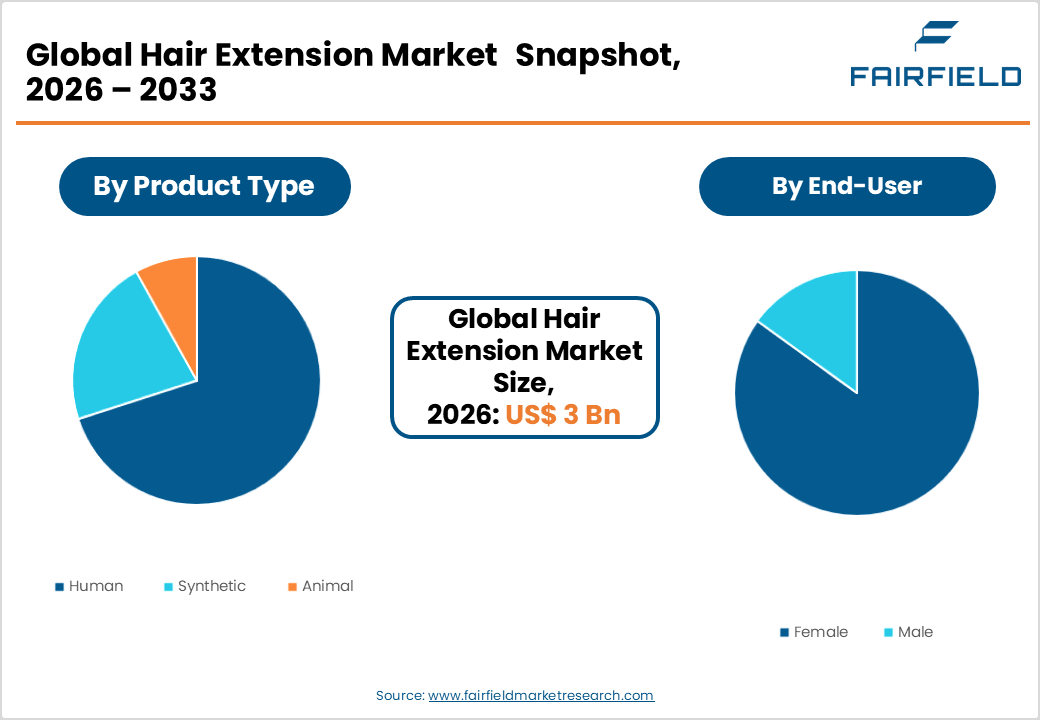

- The global hair extension market size is likely to be valued at USD 3 billion in 2026 and is expected to reach USD 4.8 billion by 2033, growing at a CAGR of 7.00% during the forecast period from 2026 to 2033.

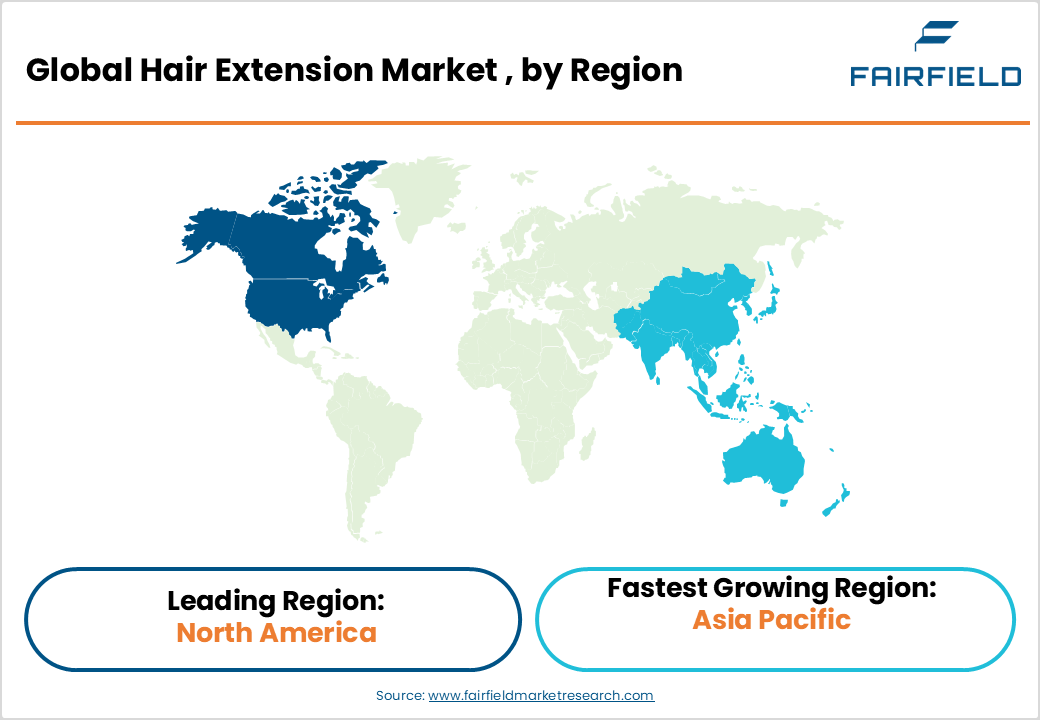

- North America leads the global Hair Extension market with approximately 38% share, driven by the U.S.'s well-established salon industry, high African-American consumer demand, and a robust e-commerce beauty retail ecosystem.

- Asia Pacific is the fastest-growing region, benefiting from its dominant global role as a human hair supplier, rapidly expanding middle-class consumer base, and explosive e-commerce penetration across China and ASEAN markets.

- Human hair extensions command approximately 53% of market share by product type, prized for their natural appearance, heat-styling versatility, and strong professional salon preference across global markets.

- Non-store-based channels, particularly e-commerce, are the fastest-growing distribution segment, driven by expanding online beauty platforms, influencer-led social commerce, and DTC brand growth in Asia Pacific and North America.

- The rapidly growing male personal grooming industry presents a high-growth frontier, with brands developing male-targeted extension systems to capture first-mover advantage among Millennial and Gen Z male consumers globally.

Market Dynamics: Drivers, Restraints, and Opportunities Analysis

Market Growth Drivers

Social Media Influence and Beauty Culture Driving Mass Adoption

The outsized influence of social media platforms particularly Instagram, TikTok, and YouTube has fundamentally transformed consumer awareness and aspiration around hair extensions. Beauty content on TikTok alone has generated billions of views under hair transformation hashtags, directly driving consumer trial and purchase intent. According to Statista, the number of social media users globally surpassed 5 billion in 2024, amplifying the reach of beauty influencers and brand campaigns exponentially. Celebrity endorsements by figures such as Kim Kardashian, Beyoncé, and Cardi B, who openly advocate hair extension use, have destigmatized the product and elevated it to mainstream status. This cultural normalization, reinforced by user-generated tutorials demonstrating DIY clip-in and tape-in applications, is a structural, self-reinforcing demand driver for the global hair extension market.

Rising Prevalence of Hair Loss Disorders Driving Therapeutic Demand

Beyond aesthetic motivation, the growing clinical prevalence of alopecia and other hair loss conditions is creating a parallel therapeutic demand stream for hair extensions. According to the American Academy of Dermatology (AAD), alopecia areata affects approximately 6.8 million people in the U.S. alone, while androgenetic alopecia impacts over 50 million men and 30 million women in the country. Globally, the World Health Organization (WHO) acknowledges hair loss as a condition significantly affecting quality of life and psychological well-being. Hair extensions particularly human hair and medical-grade synthetic variants offer non-surgical, non-pharmaceutical solutions for individuals experiencing thinning or significant hair loss, supporting demand from both salon-based professional application and direct consumer channels. This therapeutic segment represents a high-loyalty, recurrent revenue opportunity for market participants.

Market Restraints

High Cost of Premium Human Hair Extensions

Premium human hair extensions particularly Remy and Virgin human hair variants sourced from India, Brazil, and Eastern Europe carry significant price premiums, limiting their accessibility to middle and lower-income consumer segments. High-quality human hair extension sets can retail for USD 200 to over USD 1,500 depending on hair origin, length, and application method. Additionally, professional salon application costs for methods such as micro-link bonds or tape-in extensions can add several hundred dollars. This price barrier restricts repeat purchase frequency and confines premium human hair product adoption primarily to higher-income demographics in developed markets, limiting overall volume growth.

Risk of Hair and Scalp Damage Dampening Consumer Confidence

A well-documented concern among consumers and dermatologists is the potential for hair and scalp damage resulting from improper application or long-term wear of hair extensions. Research published in the Journal of the American Academy of Dermatology identifies traction alopecia as a significant risk associated with heavy or incorrectly applied extensions, particularly in protective styling. The British Association of Dermatologists has issued consumer advisories highlighting these risks. Such health concerns, amplified by social media reports of adverse outcomes, create hesitancy among new consumers and constrain repeat purchase rates, particularly in markets where professional application services are expensive or inaccessible.

Market Opportunities

Expanding Male Grooming Segment Opening a High-Growth Demand Frontier

The rapid growth of the male personal grooming industry represents an underexplored but high-potential opportunity for hair extension manufacturers. The global men's grooming market, valued at over USD 80 billion according to Euromonitor International, is growing at a robust pace, with hair care and styling products among the fastest-growing sub-categories. Changing social norms around masculinity and personal appearance particularly among Millennials and Gen Z men are normalizing the use of hair enhancements. Brands including Balmain Hair Group have begun developing male-targeted extension systems. Manufacturers that develop application methods suited to shorter male hair lengths, launch discreet packaging formats, and market through male-oriented digital channels stand to capture a first-mover advantage in this nascent but rapidly expanding segment.

Non-Store-Based and E-Commerce Channels Unlocking Global Consumer Reach

The explosive growth of e-commerce beauty retail represents a transformative distribution opportunity for hair extension brands. Online platforms including Amazon, Sally Beauty's digital storefront, AliExpress, and direct-to-consumer brand websites have dramatically reduced the geographic and informational barriers to hair extension purchase. According to the U.S. Census Bureau, U.S. e-commerce sales grew by approximately 8.6% year-on-year in 2023, with beauty and personal care among the top-growing categories. In Asia Pacific, platforms such as Lazada, Shopee, and JD.com have made premium hair extensions accessible in markets where physical specialty retail penetration remains limited. Brands investing in video-based e-commerce content, AR-powered virtual try-on tools, and subscription-based replenishment models can build durable, scalable consumer relationships through non-store channels.

Segmentation Analysis: Category-Wise Strategic Assessment

By Product Type Analysis

The Human Hair extension segment is the dominant product type, commanding approximately 53% of total market share. Human hair extensions particularly Remy hair, where the cuticle layers remain intact and aligned are prized for their natural appearance, superior blendability, and styling versatility. Unlike synthetic alternatives, human hair extensions can be washed, heat-styled, colored, and treated like natural hair, commanding a strong loyalty premium among professional users and discerning consumers. According to the Professional Beauty Association (PBA), human hair extension services constitute one of the fastest-growing revenue categories in professional salons across North America. The growing global hair donor supply from India and Southeast Asia, combined with expanding ethical sourcing awareness, further reinforces this segment's market leadership.

By End-User Analysis

The Female end-user segment dominates the Hair Extension market, accounting for approximately 88% of total market share. Women remain the primary consumer base for hair extensions across all product types and application methods driven by longstanding beauty conventions, cultural traditions of hair adornment, and a substantially wider range of extension styles available for longer hair lengths. Hair extensions are deeply integrated into professional styling, bridal, and theatrical markets that are predominantly female-focused. The U.S. Bureau of Labor Statistics reports that women account for the vast majority of professional beauty service expenditures. Across cultures from African-American protective styling traditions to South Asian bridal hair practices hair extension use is a deeply embedded cultural norm, ensuring structural dominance of the female segment.

By Distribution Channel Analysis

The Store-based distribution channel leads the Hair Extension market, holding approximately 61% of total distribution channel share. Physical retail encompassing professional beauty supply stores, salon-exclusive channels, and specialty beauty retailers such as Sally Beauty and Ulta Beauty remains the preferred purchase touchpoint for hair extensions due to the consumer need for tactile product evaluation. The ability to assess hair texture, color match, and quality in person is critical for a product category where sensory attributes directly determine purchase satisfaction. Additionally, professional salon-based distribution where stylists sell and apply extensions as part of a service package accounts for a significant portion of store-based revenues, particularly for premium human hair products from brands like Great Lengths and SO.CAP. Original USA.

Regional Market Assessment: Strategic Geography Analysis

North America Hair Extension Trends

North America leads the global Hair Extension market with approximately 38% of total market share, with the United States as the undisputed regional powerhouse. The U.S. market benefits from a highly developed professional salon industry, strong African-American consumer demand for protective styling extensions, and a robust e-commerce ecosystem for direct-to-consumer hair product brands. The Professional Beauty Association (PBA) reports that the U.S. salon services industry generates over USD 50 billion annually, with hair extension services representing one of its fastest-growing revenue categories.

The U.S. regulatory environment, governed by the FDA for cosmetic product safety and the Federal Trade Commission (FTC) for marketing claims, provides a structured framework that supports consumer confidence in branded extension products. Canada is an emerging sub-market, with growing multicultural consumer demographics in cities such as Toronto and Vancouver driving demand for diverse hair extension products. The North American market is also an innovation hub, with brands pioneering heat-free application systems, sustainable packaging, and AR-based virtual try-on technology for online retail.

Europe Hair Extension Trends

Europe represents a mature and fashion-forward market for hair extensions, with the U.K., Germany, France, and Italy as the most significant national markets. The U.K. is particularly noteworthy, with a vibrant professional salon culture, a large Afro-Caribbean consumer demographic, and prominent fashion and entertainment industries that drive consistent demand for high-end human hair extensions. Great Lengths Universal Hair Extensions Srl, headquartered in Italy, is among the world's most recognized premium extension brands, reflecting Europe's strong manufacturing and brand heritage in this category.

Germany and France present growth opportunities driven by an expanding multicultural population and increasing salon professionalization. The EU Cosmetics Regulation (EC) No 1223/2009 governs hair product safety standards across the region, ensuring product quality compliance and consumer protection. Spain is emerging as a growth market, underpinned by a dynamic fashion industry and growing consumer investment in personal appearance. European brands are increasingly emphasizing ethically sourced human hair and eco-friendly packaging, responding to the region's strong sustainability culture and regulatory push toward responsible sourcing.

Asia Pacific Hair Extension Trends

Asia Pacific is the fastest-growing regional market for hair extensions, fueled by its dual role as both the world's largest supplier of raw human hair and a rapidly expanding end-consumer market. India is the dominant global source of human hair, with temples such as the Tirumala Tirupati Devasthanams (TTD) in Andhra Pradesh supplying millions of kilograms of high-quality donor hair annually to global extension manufacturers. Indian companies are increasingly capturing more value by processing and finishing extensions domestically before export, moving up the value chain.

China is both a major manufacturer producing synthetic and blended extensions at scale for global export and a growing end-consumer market, driven by an expanding middle class and strong social media beauty culture. Japan's mature and highly aesthetic personal care market supports consistent premium extension demand, with ASEAN nations including Vietnam, Indonesia, and Thailand emerging as both low-cost manufacturing hubs and fast-growing consumer markets. The region's young demographic profile, high smartphone penetration, and e-commerce adoption create a favorable structural environment for sustained market expansion.

Competitive Landscape: Market Structure and Strategic Positioning

The global hair extension market is highly fragmented, comprising a large number of specialized brands, regional manufacturers, and private-label suppliers alongside a small cohort of internationally recognized premium brands. Companies such as Great Lengths, Balmain Hair Group, and SO.CAP. Original USA differentiates through premium human hair quality, professional salon distribution, and brand equity built over decades. Mid-tier and value players compete primarily on price, targeting mass retail and e-commerce channels. Key competitive strategies include expanding direct-to-consumer digital channels, developing proprietary application technologies, building ethical sourcing credentials, and forging influencer and celebrity partnerships. Private-label extension manufacturing for major beauty retailers is also a growing business model, intensifying competition in the mid-market segment.

Key Players

- Balmain Hair Group B.V.

- Viva Femina Inc.

- Hairlocs

- Great Lengths Universal Hair Extensions Srl

- Hair Visions International

- Racoon International

- Easihair Pro USA

- CAP. Original USA

- Cinderella Hair Extensions

Key Industry Developments

-

February 2025: Balmain Hair Group B.V. launched a new collection of ethically sourced Remy human hair extensions featuring QR-code-based traceability, enabling consumers to verify the geographic origin and ethical sourcing credentials of each product.

-

October 2024: Great Lengths Universal Hair Extensions Srl expanded its professional salon distribution network into 10 new Asian markets, including Vietnam, Thailand, and Malaysia, to capitalize on rapidly growing professional hair services demand across Southeast Asia.

-

May 2024: Easihair Pro USA introduced an advanced heat-free nano-bond application system targeting salon professionals, claiming significantly reduced application time and lower risk of traction damage compared to traditional bonding methods.

Global Hair Extension Market Segmentation-

By Product Type

- Synthetic

- Human

- Animal fastest

By End-user

- Male

- Female

By Distribution Channel

- Store-based

- Non-store-based

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Executive Summary

- Global Hair Extension Market Snapshot

- Future Projections

- Key Market Trends

- Regional Snapshot, by Value, 2026

- Analyst Recommendations

- Market Overview

- Market Definitions and Segmentations

- Market Dynamics

- Drivers

- Restraints

- Market Opportunities

- Value Chain Analysis

- COVID-19 Impact Analysis

- Porter's Five Forces Analysis

- Impact of Russia-Ukraine Conflict

- PESTLE Analysis

- Regulatory Analysis

- Price Trend Analysis

- Current Prices and Future Projections, 2025-2033

- Price Impact Factors

- Global Hair Extension Market Outlook, 2020 - 2033

- Global Hair Extension Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Synthetic

- Human

- Animal fastest

- Global Hair Extension Market Outlook, By End-user, Value (US$ Bn), 2020-2033

- Male

- Female

- Global Hair Extension Market Outlook, by Distribution Channel, Value (US$ Bn), 2020-2033

- Store-based

- Non-store-based

- Global Hair Extension Market Outlook, by Region, Value (US$ Bn), 2020-2033

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Global Hair Extension Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- North America Hair Extension Market Outlook, 2020 - 2033

- North America Hair Extension Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Synthetic

- Human

- Animal fastest

- North America Hair Extension Market Outlook, By End-user, Value (US$ Bn), 2020-2033

- Male

- Female

- North America Hair Extension Market Outlook, by Distribution Channel, Value (US$ Bn), 2020-2033

- Store-based

- Non-store-based

- North America Hair Extension Market Outlook, by Country, Value (US$ Bn), 2020-2033

- U.S. Hair Extension Market Outlook, by Product Type, 2020-2033

- U.S. Hair Extension Market Outlook, By End-user, 2020-2033

- U.S. Hair Extension Market Outlook, by Distribution Channel, 2020-2033

- Canada Hair Extension Market Outlook, by Product Type, 2020-2033

- Canada Hair Extension Market Outlook, By End-user, 2020-2033

- Canada Hair Extension Market Outlook, by Distribution Channel, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- North America Hair Extension Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Europe Hair Extension Market Outlook, 2020 - 2033

- Europe Hair Extension Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Synthetic

- Human

- Animal fastest

- Europe Hair Extension Market Outlook, By End-user, Value (US$ Bn), 2020-2033

- Male

- Female

- Europe Hair Extension Market Outlook, by Distribution Channel, Value (US$ Bn), 2020-2033

- Store-based

- Non-store-based

- Europe Hair Extension Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Germany Hair Extension Market Outlook, by Product Type, 2020-2033

- Germany Hair Extension Market Outlook, By End-user, 2020-2033

- Germany Hair Extension Market Outlook, by Distribution Channel, 2020-2033

- Italy Hair Extension Market Outlook, by Product Type, 2020-2033

- Italy Hair Extension Market Outlook, By End-user, 2020-2033

- Italy Hair Extension Market Outlook, by Distribution Channel, 2020-2033

- France Hair Extension Market Outlook, by Product Type, 2020-2033

- France Hair Extension Market Outlook, By End-user, 2020-2033

- France Hair Extension Market Outlook, by Distribution Channel, 2020-2033

- U.K. Hair Extension Market Outlook, by Product Type, 2020-2033

- U.K. Hair Extension Market Outlook, By End-user, 2020-2033

- U.K. Hair Extension Market Outlook, by Distribution Channel, 2020-2033

- Spain Hair Extension Market Outlook, by Product Type, 2020-2033

- Spain Hair Extension Market Outlook, By End-user, 2020-2033

- Spain Hair Extension Market Outlook, by Distribution Channel, 2020-2033

- Russia Hair Extension Market Outlook, by Product Type, 2020-2033

- Russia Hair Extension Market Outlook, By End-user, 2020-2033

- Russia Hair Extension Market Outlook, by Distribution Channel, 2020-2033

- Rest of Europe Hair Extension Market Outlook, by Product Type, 2020-2033

- Rest of Europe Hair Extension Market Outlook, By End-user, 2020-2033

- Rest of Europe Hair Extension Market Outlook, by Distribution Channel, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Europe Hair Extension Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Asia Pacific Hair Extension Market Outlook, 2020 - 2033

- Asia Pacific Hair Extension Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Synthetic

- Human

- Animal fastest

- Asia Pacific Hair Extension Market Outlook, by End-user, Value (US$ Bn), 2020-2033

- Male

- Female

- Asia Pacific Hair Extension Market Outlook, by Distribution Channel, Value (US$ Bn), 2020-2033

- Store-based

- Non-store-based

- Asia Pacific Hair Extension Market Outlook, by Country, Value (US$ Bn), 2020-2033

- China Hair Extension Market Outlook, by Product Type, 2020-2033

- China Hair Extension Market Outlook, By End-user, 2020-2033

- China Hair Extension Market Outlook, by Distribution Channel, 2020-2033

- Japan Hair Extension Market Outlook, by Product Type, 2020-2033

- Japan Hair Extension Market Outlook, By End-user, 2020-2033

- Japan Hair Extension Market Outlook, by Distribution Channel, 2020-2033

- South Korea Hair Extension Market Outlook, by Product Type, 2020-2033

- South Korea Hair Extension Market Outlook, By End-user, 2020-2033

- South Korea Hair Extension Market Outlook, by Distribution Channel, 2020-2033

- India Hair Extension Market Outlook, by Product Type, 2020-2033

- India Hair Extension Market Outlook, By End-user, 2020-2033

- India Hair Extension Market Outlook, by Distribution Channel, 2020-2033

- Southeast Asia Hair Extension Market Outlook, by Product Type, 2020-2033

- Southeast Asia Hair Extension Market Outlook, By End-user, 2020-2033

- Southeast Asia Hair Extension Market Outlook, by Distribution Channel, 2020-2033

- Rest of SAO Hair Extension Market Outlook, by Product Type, 2020-2033

- Rest of SAO Hair Extension Market Outlook, By End-user, 2020-2033

- Rest of SAO Hair Extension Market Outlook, by Distribution Channel, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Asia Pacific Hair Extension Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Latin America Hair Extension Market Outlook, 2020 - 2033

- Latin America Hair Extension Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Synthetic

- Human

- Animal fastest

- Latin America Hair Extension Market Outlook, By End-user, Value (US$ Bn), 2020-2033

- Male

- Female

- Latin America Hair Extension Market Outlook, by Distribution Channel, Value (US$ Bn), 2020-2033

- Store-based

- Non-store-based

- Latin America Hair Extension Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Brazil Hair Extension Market Outlook, by Product Type, 2020-2033

- Brazil Hair Extension Market Outlook, By End-user, 2020-2033

- Brazil Hair Extension Market Outlook, by Distribution Channel, 2020-2033

- Mexico Hair Extension Market Outlook, by Product Type, 2020-2033

- Mexico Hair Extension Market Outlook, By End-user, 2020-2033

- Mexico Hair Extension Market Outlook, by Distribution Channel, 2020-2033

- Argentina Hair Extension Market Outlook, by Product Type, 2020-2033

- Argentina Hair Extension Market Outlook, By End-user, 2020-2033

- Argentina Hair Extension Market Outlook, by Distribution Channel, 2020-2033

- Rest of LATAM Hair Extension Market Outlook, by Product Type, 2020-2033

- Rest of LATAM Hair Extension Market Outlook, By End-user, 2020-2033

- Rest of LATAM Hair Extension Market Outlook, by Distribution Channel, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Latin America Hair Extension Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Middle East & Africa Hair Extension Market Outlook, 2020 - 2033

- Middle East & Africa Hair Extension Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Synthetic

- Human

- Animal fastest

- Middle East & Africa Hair Extension Market Outlook, By End-user, Value (US$ Bn), 2020-2033

- Male

- Female

- Middle East & Africa Hair Extension Market Outlook, by Distribution Channel, Value (US$ Bn), 2020-2033

- Store-based

- Non-store-based

- Middle East & Africa Hair Extension Market Outlook, by Country, Value (US$ Bn), 2020-2033

- GCC Hair Extension Market Outlook, by Product Type, 2020-2033

- GCC Hair Extension Market Outlook, By End-user, 2020-2033

- GCC Hair Extension Market Outlook, by Distribution Channel, 2020-2033

- South Africa Hair Extension Market Outlook, by Product Type, 2020-2033

- South Africa Hair Extension Market Outlook, By End-user, 2020-2033

- South Africa Hair Extension Market Outlook, by Distribution Channel, 2020-2033

- Egypt Hair Extension Market Outlook, by Product Type, 2020-2033

- Egypt Hair Extension Market Outlook, By End-user, 2020-2033

- Egypt Hair Extension Market Outlook, by Distribution Channel, 2020-2033

- Nigeria Hair Extension Market Outlook, by Product Type, 2020-2033

- Nigeria Hair Extension Market Outlook, By End-user, 2020-2033

- Nigeria Hair Extension Market Outlook, by Distribution Channel, 2020-2033

- Rest of Middle East Hair Extension Market Outlook, by Product Type, 2020-2033

- Rest of Middle East Hair Extension Market Outlook, By End-user, 2020-2033

- Rest of Middle East Hair Extension Market Outlook, by Distribution Channel, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Middle East & Africa Hair Extension Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Competitive Landscape

- Company Vs Segment Heatmap

- Company Market Share Analysis, 2025

- Competitive Dashboard

- Company Profiles

- Balmain Hair Group B.V.

- Company Overview

- Product Portfolio

- Financial Overview

- Business Strategies and Developments

- Viva Femina Inc.

- Hairlocs

- Great Lengths Universal Hair Extensions Srl

- Hair Visions International

- Racoon International

- Easihair Pro USA

- CAP. Original USA

- Cinderella Hair Extensions

- Balmain Hair Group B.V.

- Appendix

- Research Methodology

- Report Assumptions

- Acronyms and Abbreviations

|

BASE YEAR |

HISTORICAL DATA |

FORECAST PERIOD |

UNITS |

|||

|

2025 |

|

2019 - 2025 |

2026 - 2033 |

Value: US$ Billion |

||

|

REPORT FEATURES |

DETAILS |

|

By Product-Type Coverage |

|

|

By Packaging Type Coverage |

|

|

Geographical Coverage |

|

|

Leading Companies |

|

|

Report Highlights |

Key Market Indicators, Macro-micro economic impact analysis, Technological Roadmap, Key Trends, Driver, Restraints, and Future Opportunities & Revenue Pockets, Porter’s 5 Forces Analysis, Historical Trend (2019-2024), Market Estimates and Forecast, Market Dynamics, Industry Trends, Competition Landscape, Category, Region, Country-wise Trends & Analysis, COVID-19 Impact Analysis (Demand and Supply Chain) |

Our Research Methodology

Considering the volatility of business today, traditional approaches to strategizing a game plan can be unfruitful if not detrimental. True ambiguity is no way to determine a forecast. A myriad of predetermined factors must be accounted for such as the degree of risk involved, the magnitude of circumstances, as well as conditions or consequences that are not known or unpredictable. To circumvent binary views that cast uncertainty, the application of market research intelligence to strategically posture, move, and enable actionable outcomes is necessary.

View Methodology

Quality Assured

Rigorous Validation Process

Confidentiality Assured

End-to-end Data Security

Custom Research Services

Tailored To Your Objectives

FAQs

The hair extension market size is USD 3 billion in 2026.

The hair extension market is projected 7% CAGR by 2033.

The hair extension market growth drivers include rising beauty consciousness via social media, premium human hair demand, and e-commerce expansion.

North America is a dominating region for hair extension market.

Great Lengths SpA, Easihair Pro, Cinderellahair Inc., and Perfect Locks are some leading industry players in the hair extension market.

Related Reports

Premium Cosmeceuticals Market Insights, Competitive Landscape, and Market Forecast 2033

Premium Cosmeceuticals Market to reach US$95.03 Bn by 2033 at 3.9% CAGR, driven by clinical skincare, AI personalization, and premium beauty.

Textile Manufacturing Market Insights, Competitive Landscape, and Market Forecast 2033

Textile manufacturing market is valued at US$ 301 Bn in 2026 & projected to reach US$ 409.62 Bn by 2033, growing at a CAGR of 4.5% through 2033.

Tourism Market Insights, Competitive Landscape, and Market Forecast 2033

Global Tourism Market valued at US$ 10,800 Bn in 2026, projected to reach US$ 16,454.90 Bn by 2033, growing at a CAGR of 6.2% during the forecast period.

Personal Care Active Ingredients Market Insights, Competitive Landscape, and Market Forecast 2033

The personal care active ingredients market to grow from US$ 24.10 Bn in 2026 to US$ 35.53 Bn by 2033, registering a CAGR of 5.7% during the forecast period.

Reusable E-commerce Packaging Market by Insights, Competitive Landscape, and Market Forecast 2033

Reusable E-commerce Packaging Market to grow from US$ 9.30 Bn in 2026 to US$ 17.55 Bn by 2033, expanding at a CAGR of 9.5%.

Post Consumer Recycled Packaging Market Insights, Competitive Landscape, and Market Forecast 2033

Post-Consumer Recycled Packaging Market to grow from US$ 25.10 Bn in 2026 to US$ 43.30 Bn by 2033, expanding at a CAGR of 8.1%.