Telecom Cloud Market Size, Share, and Growth Forecast 2026 – 2033

Key Market Highlights

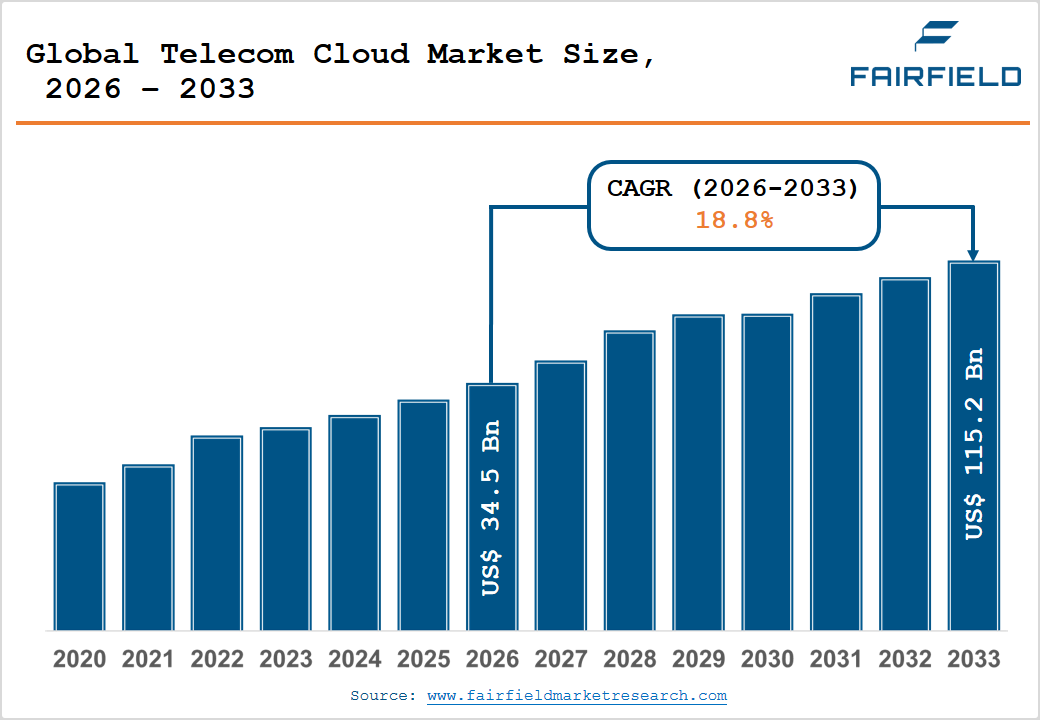

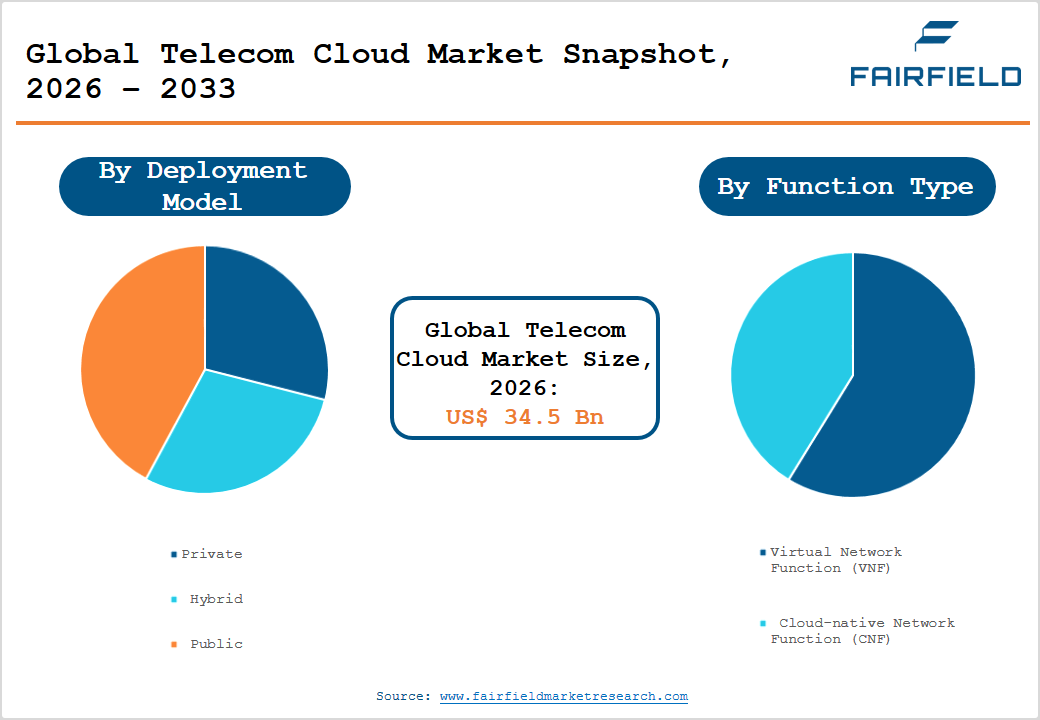

- The global telecom cloud market size is likely to be valued at US$34.5 billion in 2026 and is expected to reach US$115.2 billion by 2033, growing at a CAGR of 18.80% during the forecast period from 2026 to 2033.

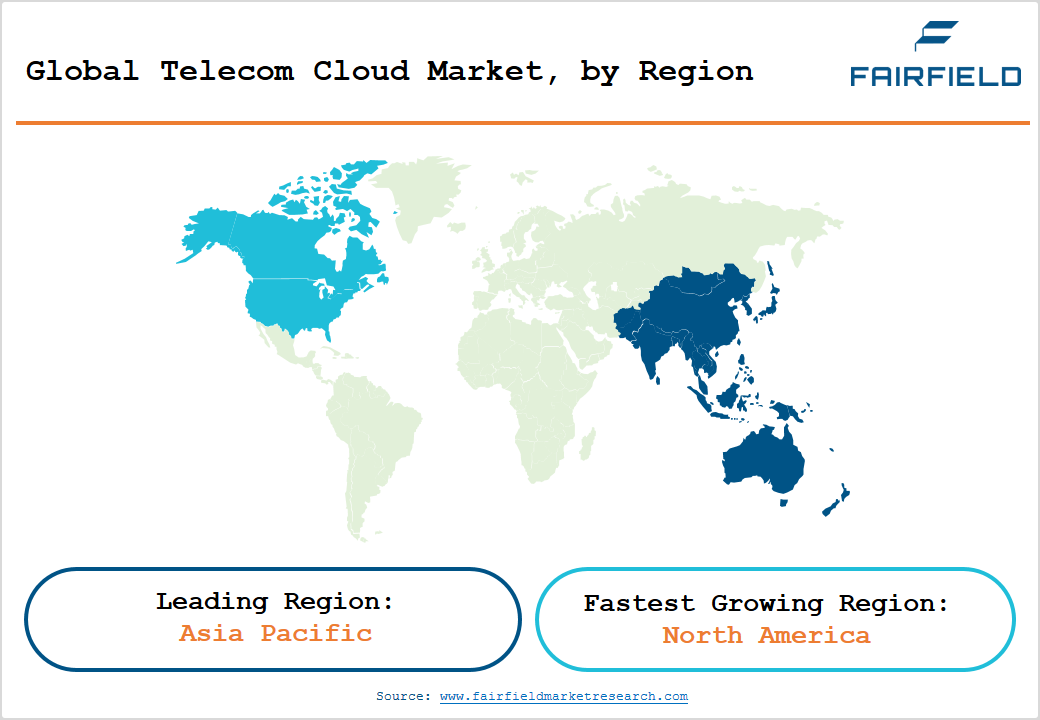

- Leading Region Market: Asia Pacific dominates the Telecom Cloud Market with approximately 38% global share in 2026, driven by massive 5G deployments and cloud-native transformation programs by China Mobile, NTT Docomo, and Reliance Jio, supported by strong government digital infrastructure mandates.

- Fastest Growing Region Market: North America is the fastest-growing region, fueled by aggressive carrier 5G network modernization, Open RAN policy support under the CHIPS and Science Act, and deep integration with hyperscaler ecosystems led by AWS, Microsoft Azure, and Google Cloud Platform.

- Dominant Segment: The Hybrid Cloud deployment model Segment leads with approximately 45% market share in 2026, as telecom operators balance data sovereignty and regulatory compliance with public cloud scalability, enabling phased, risk-managed migration of workloads to cloud-native environments.

- Fastest Growing Segment: Cloud-Native Network Functions (CNF) represent the fastest-growing segment within Function Type, accelerated by 5G Standalone core rollouts, Open RAN ecosystem expansion, and vendor adoption of containerization technologies such as Kubernetes for agile network service delivery.

- Key Market Opportunity: Multi-Access Edge Computing (MEC) and distributed edge cloud deployments present a compelling opportunity, as demand for ultra-low latency applications including autonomous systems, industrial IoT, and augmented reality drives investment in telecom edge infrastructure per ETSI and ITU

Market Dynamics

Market Growth Drivers

- Rapid 5G Deployment and Network Function Virtualization (NFV) Adoption

The global rollout of 5G networks is a central catalyst for telecom cloud adoption. According to the GSMA Intelligence, the number of 5G connections worldwide is expected to surpass 2 billion by 2025, with operators in North America, Europe, and Asia Pacific front-loading infrastructure investments. 5G architecture inherently demands cloud-native solutions to support network slicing, edge computing, and ultra-low latency services. Simultaneously, the transition from hardware-centric systems to software-defined, virtualized environments via NFV and Software-Defined Networking (SDN) allows carriers to decouple network functions from proprietary hardware. This significantly reduces operational expenditure (OPEX) and enables faster service innovation, driving heightened investment in cloud-native telecom infrastructure globally.

- Surge in Mobile Data Traffic and IoT Connectivity Requirements

Exponential growth in mobile data traffic and the proliferation of Internet of Things (IoT) devices are compelling telecom operators to modernize their infrastructure through cloud adoption. Global mobile data traffic is projected to increase more than threefold between 2022 and 2028, reaching approximately 330 exabytes per month by 2028. This unprecedented data surge demands highly scalable, elastic infrastructure that only cloud architectures can efficiently provide. Telecom cloud platforms enable operators to dynamically allocate computing and networking resources in real time, ensuring consistent quality of service. The convergence of IoT, edge computing, and mobile broadband is further reinforcing the necessity for cloud-based telecom frameworks among both large carriers and emerging regional operators.

Market Restraints

- Data Security, Privacy Concerns, and Regulatory Compliance Complexity

Migrating sensitive telecom workloads to cloud environments introduces significant data security and privacy risks. Telecom operators handle vast volumes of sensitive subscriber information, making them prime targets for cyberattacks. According to the European Union Agency for Cybersecurity (ENISA), telecom remains among the most targeted sectors for advanced persistent threats. Compliance with frameworks such as the General Data Protection Regulation (GDPR) in Europe and various national data sovereignty laws adds further complexity. Operators face challenges reconciling global cloud deployments with local regulatory requirements, particularly in regions enforcing strict data localization policies. These compounding concerns often delay or scale back cloud migration initiatives, restraining the pace of market growth.

- High Migration Costs and Legacy System Integration Challenges

The transition from legacy, hardware-based telecom infrastructure to cloud-native architectures involves substantial upfront investment and operational disruption. Many incumbent operators continue to rely on proprietary network equipment that is difficult and expensive to integrate with open, cloud-based platforms. A 2023 TM Forum survey indicated that over 60% of telecom executives cited legacy system complexity as a top barrier to cloud transformation. Skill shortages in cloud-native engineering and DevOps further compound the challenge. The migration process involves significant re-architecting of network functions, extensive testing, and staff retraining, all of which inflate total cost of ownership (TCO) and extend transition timelines, thereby acting as a notable restraint on market expansion.

Market Opportunities

- Cloud-Native Network Functions (CNF) and Open RAN Ecosystem Expansion

The rapid evolution towards Cloud-Native Network Functions (CNF) and the expanding Open Radio Access Network (Open RAN) ecosystem present substantial growth opportunities for market participants. Unlike traditional Virtual Network Functions (VNF), CNFs leverage containerization technologies such as Kubernetes and Docker to deliver far greater resource efficiency, automation, and scalability. The O-RAN Alliance, a global consortium of over 300 leading operators and vendors, is actively defining open, interoperable specifications that facilitate multivendor cloud-native deployments. As more operators pilot and adopt Open RAN architectures particularly in the U.S. following the CHIPS and Science Act provisions demand for cloud-native telecom platforms is expected to surge, opening lucrative opportunities for solution providers offering orchestration, lifecycle management, and AI-driven automation capabilities.

- Edge Cloud and Multi-Access Edge Computing (MEC) for Latency-Sensitive Applications

The growing demand for ultra-low latency applications including autonomous vehicles, industrial automation, augmented reality, and real-time analytics is driving significant investment in Multi-Access Edge Computing (MEC) and distributed edge cloud architectures. The European Telecommunications Standards Institute (ETSI) has been instrumental in standardizing MEC frameworks, enabling operators to deploy computing resources closer to end users. According to the International Telecommunication Union (ITU), global investment in telecom edge infrastructure is forecast to accelerate substantially through the late 2020s. This creates compelling opportunities for telecom cloud vendors to differentiate through purpose-built edge platforms, micro data center solutions, and seamless integration between core and edge cloud environments, particularly in verticals such as manufacturing, healthcare, and smart cities.

Segmental Insights

- Deployment Model Analysis

Among the deployment models, the Hybrid Cloud segment holds the leading position in the Telecom Cloud Market, commanding approximately 45% market share in 2026. Hybrid deployments enable telecom operators to maintain sensitive core network functions on private infrastructure while leveraging the scalability and cost-efficiency of public cloud for non-critical workloads. This approach addresses data sovereignty concerns without sacrificing flexibility. Operators such as Deutsche Telekom and AT&T have publicly documented hybrid strategies that balance regulatory compliance with innovation speed. The hybrid model also facilitates gradual cloud migration, reducing operational risk during transitions. As 5G network slicing requirements intensify, hybrid architectures are increasingly seen as the pragmatic path enabling operators to orchestrate workloads dynamically across private and public environments.

- Enterprise Type Analysis

Large Enterprises constitute the dominant segment in the Telecom Cloud Market by enterprise type, accounting for approximately 68% market share in 2026. Large telecom operators and multinational enterprises possess the financial resources, technical expertise, and regulatory bandwidth to undertake complex, large-scale cloud transformations. Global carriers such as Verizon, Vodafone, and China Mobile have committed multi-billion-dollar investments to cloud infrastructure modernization. A majority of major global telecom companies have launched cloud-native transformation initiatives. Moreover, large enterprises benefit from greater negotiating leverage with hyperscaler partners like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform (GCP), enabling more favorable commercial arrangements that further reinforce their dominant market position.

- Function Type Analysis

The Virtual Network Function (VNF) segment currently leads the Function Type category with an estimated market share of approximately 58% share in 2026. VNFs replaced traditional hardware-based network appliances by running network services as software on standard commercial off-the-shelf (COTS) hardware, significantly lowering deployment costs and enabling centralized management. The widespread adoption of NFV frameworks, supported by standards bodies such as the European Telecommunications Standards Institute (ETSI), has embedded VNFs deeply into existing operator networks. While Cloud-Native Network Functions (CNF) are gaining momentum for greenfield 5G deployments, the installed base of VNF infrastructure and the operational familiarity operators have developed continue to sustain its leadership. Major vendors including Ericsson, Nokia, and Cisco maintain extensive VNF portfolios catering to the global operator community.

- Service Type Analysis

Infrastructure as a Service (IaaS) represents the leading segment within the Service Type category, holding approximately 43% share in 2026. Telecom operators fundamentally require scalable, on-demand compute, storage, and networking infrastructure to underpin their cloud transformation journeys, making IaaS the foundational layer of adoption. Leading hyperscalers Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform (GCP) have developed telecom-specific IaaS offerings with carrier-grade reliability, global points of presence, and compliance certifications tailored to the sector. Partnerships such as AT&T's agreement with Microsoft Azure and DISH Network's collaboration with AWS underscore the strategic centrality of IaaS in telecom cloud deployments, as operators seek to offload capital-intensive hardware procurement to cloud service providers.

Regional Insights

- North America Telecom Cloud Trends

North America is the fastest-growing region in the global Telecom Cloud Market, driven by aggressive 5G deployments, a mature hyperscaler ecosystem, and a favorable policy environment. The U.S. market is particularly dynamic, with carriers such as AT&T, Verizon, and T-Mobile executing substantial cloud-native transformation programs. The CHIPS and Science Act (2022) and FCC initiatives supporting Open RAN development are accelerating vendor diversification and cloud adoption in network infrastructure. The presence of global hyperscalers AWS, Microsoft Azure, and Google Cloud Platform headquartered in the U.S. ensures ready access to cutting-edge cloud services tailored for telecom workloads.

The Canadian telecom sector mirrors these trends, with Bell Canada and TELUS both pursuing cloud-native core deployments in alignment with the Canadian Radio-television and Telecommunications Commission (CRTC) modernization directives. North America's advanced venture capital ecosystem and strong university-industry research collaboration further stimulate innovation in telecom cloud orchestration, AI/ML-driven network management, and edge computing, reinforcing the region's position as the foremost growth frontier.

- Europe Telecom Cloud Trends

Europe represents a significant and mature segment of the Telecom Cloud Market, underpinned by robust regulatory frameworks and strong operator commitment to digital infrastructure modernization. Germany, as home to Deutsche Telekom one of the world's largest telecom operators is a key contributor, with the operator's Open Telekom Cloud platform exemplifying the regional push towards sovereign cloud solutions. In the United Kingdom, BT Group and Vodafone have outlined extensive cloud transformation roadmaps, while France's Orange and Spain's Telefónica are pursuing cloud-native network strategies aligned with the European Electronic Communications Code (EECC).

The European Union's European Gigabit Society targets and the EU Cloud Rulebook initiative are harmonizing cloud standards and compliance requirements across member states, reducing regulatory fragmentation. The ETSI continues to be a globally influential standards body shaping NFV and MEC specifications, ensuring European operators maintain interoperability across multivendor environments. These regulatory and institutional tailwinds, combined with increasing enterprise demand for private and hybrid telecom cloud services, sustain Europe's strong positioning in the global market.

- Asia Pacific Telecom Cloud Trends

Asia Pacific is the leading region in the Telecom Cloud Market, commanding approximately 38% market share in 2026, driven by the sheer scale of telecom operations in China, Japan, India, and Southeast Asia. China is home to the world's three largest telecom operators China Mobile, China Unicom, and China Telecom all of which are executing major cloud-native transformation programs under directives aligned with the 14th Five-Year Plan for digital infrastructure. Huawei and ZTE play pivotal roles as both infrastructure vendors and cloud platform providers within the domestic ecosystem.

In Japan, operators such as NTT Docomo and SoftBank are at the vanguard of 5G standalone (SA) core deployments leveraging cloud-native architectures. India's rapid 5G rollout by Reliance Jio and Bharti Airtel, supported by the Department of Telecommunications (DoT) policy framework, is generating substantial demand for telecom cloud solutions. Across ASEAN, nations including Singapore, Indonesia, and Vietnam are investing in national digital infrastructure programs that incorporate telecom cloud as a foundational element, further reinforcing the region's dominant market position.

Competitive Landscape

The Telecom Cloud Market exhibits a moderately consolidated structure, dominated by a combination of global hyperscalers and established telecom equipment vendors. Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform (GCP) leverage their vast infrastructure scale and telecom-specific solution portfolios to secure long-term operator partnerships. Equipment incumbents such as Ericsson, Nokia, and Cisco compete through deep domain expertise, standards leadership, and end-to-end managed service capabilities. Key competitive differentiators include carrier-grade reliability, security certifications, Open RAN compatibility, and AI-driven network automation. Market participants are increasingly pursuing co-innovation partnerships, joint ventures, and mergers and acquisitions to broaden their cloud-native telecom portfolios and expand geographic reach.

Key Market Developments

- January, 2025: Microsoft Azure expanded its Azure for Operators portfolio with new AI-powered network analytics and Open RAN orchestration capabilities, deepening partnerships with major U.S. and European carriers seeking to accelerate cloud-native core deployments.

- September, 2024: Ericsson announced the commercial launch of its cloud-native 5G Standalone core solution deployed on AWS infrastructure, enabling operators in North America and Asia Pacific to run fully containerized network functions on public cloud platforms.

- March, 2024: Nokia and Google Cloud extended their strategic partnership to co-develop AI/ML-powered network automation and edge cloud solutions targeted at telecom operators globally, building on their earlier collaboration on Open RAN cloud deployments.

Companies Covered in Telecom Cloud Market

- Amazon Web Services (AWS)

- Microsoft Azure

- Google Cloud Platform (GCP)

- IBM Cloud

- Oracle Cloud

- Cisco Systems, Inc.

- Nokia

- Ericsson

- Huawei Technologies Co., Ltd.

- Samsung Electronics

- VMware, Inc.

- HPE (Hewlett Packard Enterprise)

- Dell Technologies

- NEC Corporation

- Amdocs Ltd.

- Rakuten Symphony

- Mavenir Systems

- Wind River Systems

- Red Hat (IBM)

- Altiostar Networks

Market Segmentation

By Deployment Model

- Private

- Hybrid

- Public

By Enterprise Type

- Large Enterprises

- Small & Medium Enterprises

By Function Type

- Virtual Network Function (VNF)

- Cloud-native Network Function (CNF)

By Service Type

- Software as a Service (SaaS)

- Infrastructure as a Service (IaaS)

- Platform as a Service (PaaS)

Regions

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Executive Summary

- Global Telecom Cloud Market Snapshot

- Future Projections

- Key Market Trends

- Regional Snapshot, by Value, 2026

- Analyst Recommendations

- Market Overview

- Market Definitions and Segmentations

- Market Dynamics

- Drivers

- Restraints

- Market Opportunities

- Value Chain Analysis

- COVID-19 Impact Analysis

- Porter's Five Forces Analysis

- Impact of Russia-Ukraine Conflict

- PESTLE Analysis

- Regulatory Analysis

- Price Trend Analysis

- Current Prices and Future Projections, 2025-2033

- Price Impact Factors

- Global Telecom Cloud Market Outlook, 2020 - 2033

- Global Telecom Cloud Market Outlook, by Deployment Model, Value (US$ Bn), 2020-2033

- Private

- Hybrid

- Public

- Global Telecom Cloud Market Outlook, by Function Type, Value (US$ Bn), 2020-2033

- Virtual Network Function (VNF)

- Cloud-native Network Function (CNF)

- Global Telecom Cloud Market Outlook, by Service Type, Value (US$ Bn), 2020-2033

- SaaS

- IaaS

- PaaS

- Global Telecom Cloud Market Outlook, by Region, Value (US$ Bn), 2020-2033

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Global Telecom Cloud Market Outlook, by Deployment Model, Value (US$ Bn), 2020-2033

- North America Telecom Cloud Market Outlook, 2020 - 2033

- North America Telecom Cloud Market Outlook, by Deployment Model, Value (US$ Bn), 2020-2033

- Private

- Hybrid

- Public

- North America Telecom Cloud Market Outlook, by Function Type, Value (US$ Bn), 2020-2033

- Virtual Network Function (VNF)

- Cloud-native Network Function (CNF)

- North America Telecom Cloud Market Outlook, by Service Type, Value (US$ Bn), 2020-2033

- SaaS

- IaaS

- PaaS

- North America Telecom Cloud Market Outlook, by Country, Value (US$ Bn), 2020-2033

- U.S. Telecom Cloud Market Outlook, by Deployment Model, 2020-2033

- U.S. Telecom Cloud Market Outlook, by Function Type, 2020-2033

- U.S. Telecom Cloud Market Outlook, by Service Type, 2020-2033

- Canada Telecom Cloud Market Outlook, by Deployment Model, 2020-2033

- Canada Telecom Cloud Market Outlook, by Function Type, 2020-2033

- Canada Telecom Cloud Market Outlook, by Service Type, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- North America Telecom Cloud Market Outlook, by Deployment Model, Value (US$ Bn), 2020-2033

- Europe Telecom Cloud Market Outlook, 2020 - 2033

- Europe Telecom Cloud Market Outlook, by Deployment Model, Value (US$ Bn), 2020-2033

- Private

- Hybrid

- Public

- Europe Telecom Cloud Market Outlook, by Function Type, Value (US$ Bn), 2020-2033

- Virtual Network Function (VNF)

- Cloud-native Network Function (CNF)

- Europe Telecom Cloud Market Outlook, by Service Type, Value (US$ Bn), 2020-2033

- SaaS

- IaaS

- PaaS

- Europe Telecom Cloud Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Germany Telecom Cloud Market Outlook, by Deployment Model, 2020-2033

- Germany Telecom Cloud Market Outlook, by Function Type, 2020-2033

- Germany Telecom Cloud Market Outlook, by Service Type, 2020-2033

- Italy Telecom Cloud Market Outlook, by Deployment Model, 2020-2033

- Italy Telecom Cloud Market Outlook, by Function Type, 2020-2033

- Italy Telecom Cloud Market Outlook, by Service Type, 2020-2033

- France Telecom Cloud Market Outlook, by Deployment Model, 2020-2033

- France Telecom Cloud Market Outlook, by Function Type, 2020-2033

- France Telecom Cloud Market Outlook, by Service Type, 2020-2033

- U.K. Telecom Cloud Market Outlook, by Deployment Model, 2020-2033

- U.K. Telecom Cloud Market Outlook, by Function Type, 2020-2033

- U.K. Telecom Cloud Market Outlook, by Service Type, 2020-2033

- Spain Telecom Cloud Market Outlook, by Deployment Model, 2020-2033

- Spain Telecom Cloud Market Outlook, by Function Type, 2020-2033

- Spain Telecom Cloud Market Outlook, by Service Type, 2020-2033

- Russia Telecom Cloud Market Outlook, by Deployment Model, 2020-2033

- Russia Telecom Cloud Market Outlook, by Function Type, 2020-2033

- Russia Telecom Cloud Market Outlook, by Service Type, 2020-2033

- Rest of Europe Telecom Cloud Market Outlook, by Deployment Model, 2020-2033

- Rest of Europe Telecom Cloud Market Outlook, by Function Type, 2020-2033

- Rest of Europe Telecom Cloud Market Outlook, by Service Type, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Europe Telecom Cloud Market Outlook, by Deployment Model, Value (US$ Bn), 2020-2033

- Asia Pacific Telecom Cloud Market Outlook, 2020 - 2033

- Asia Pacific Telecom Cloud Market Outlook, by Deployment Model, Value (US$ Bn), 2020-2033

- Private

- Hybrid

- Public

- Asia Pacific Telecom Cloud Market Outlook, by Function Type, Value (US$ Bn), 2020-2033

- Virtual Network Function (VNF)

- Cloud-native Network Function (CNF)

- Asia Pacific Telecom Cloud Market Outlook, by Service Type, Value (US$ Bn), 2020-2033

- SaaS

- IaaS

- PaaS

- Asia Pacific Telecom Cloud Market Outlook, by Country, Value (US$ Bn), 2020-2033

- China Telecom Cloud Market Outlook, by Deployment Model, 2020-2033

- China Telecom Cloud Market Outlook, by Function Type, 2020-2033

- China Telecom Cloud Market Outlook, by Service Type, 2020-2033

- Japan Telecom Cloud Market Outlook, by Deployment Model, 2020-2033

- Japan Telecom Cloud Market Outlook, by Function Type, 2020-2033

- Japan Telecom Cloud Market Outlook, by Service Type, 2020-2033

- South Korea Telecom Cloud Market Outlook, by Deployment Model, 2020-2033

- South Korea Telecom Cloud Market Outlook, by Function Type, 2020-2033

- South Korea Telecom Cloud Market Outlook, by Service Type, 2020-2033

- India Telecom Cloud Market Outlook, by Deployment Model, 2020-2033

- India Telecom Cloud Market Outlook, by Function Type, 2020-2033

- India Telecom Cloud Market Outlook, by Service Type, 2020-2033

- Southeast Asia Telecom Cloud Market Outlook, by Deployment Model, 2020-2033

- Southeast Asia Telecom Cloud Market Outlook, by Function Type, 2020-2033

- Southeast Asia Telecom Cloud Market Outlook, by Service Type, 2020-2033

- Rest of SAO Telecom Cloud Market Outlook, by Deployment Model, 2020-2033

- Rest of SAO Telecom Cloud Market Outlook, by Function Type, 2020-2033

- Rest of SAO Telecom Cloud Market Outlook, by Service Type, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Asia Pacific Telecom Cloud Market Outlook, by Deployment Model, Value (US$ Bn), 2020-2033

- Latin America Telecom Cloud Market Outlook, 2020 - 2033

- Latin America Telecom Cloud Market Outlook, by Deployment Model, Value (US$ Bn), 2020-2033

- Private

- Hybrid

- Public

- Latin America Telecom Cloud Market Outlook, by Function Type, Value (US$ Bn), 2020-2033

- Virtual Network Function (VNF)

- Cloud-native Network Function (CNF)

- Latin America Telecom Cloud Market Outlook, by Service Type, Value (US$ Bn), 2020-2033

- SaaS

- IaaS

- PaaS

- Latin America Telecom Cloud Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Brazil Telecom Cloud Market Outlook, by Deployment Model, 2020-2033

- Brazil Telecom Cloud Market Outlook, by Function Type, 2020-2033

- Brazil Telecom Cloud Market Outlook, by Service Type, 2020-2033

- Mexico Telecom Cloud Market Outlook, by Deployment Model, 2020-2033

- Mexico Telecom Cloud Market Outlook, by Function Type, 2020-2033

- Mexico Telecom Cloud Market Outlook, by Service Type, 2020-2033

- Argentina Telecom Cloud Market Outlook, by Deployment Model, 2020-2033

- Argentina Telecom Cloud Market Outlook, by Function Type, 2020-2033

- Argentina Telecom Cloud Market Outlook, by Service Type, 2020-2033

- Rest of LATAM Telecom Cloud Market Outlook, by Deployment Model, 2020-2033

- Rest of LATAM Telecom Cloud Market Outlook, by Function Type, 2020-2033

- Rest of LATAM Telecom Cloud Market Outlook, by Service Type, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Latin America Telecom Cloud Market Outlook, by Deployment Model, Value (US$ Bn), 2020-2033

- Middle East & Africa Telecom Cloud Market Outlook, 2020 - 2033

- Middle East & Africa Telecom Cloud Market Outlook, by Deployment Model, Value (US$ Bn), 2020-2033

- Private

- Hybrid

- Public

- Middle East & Africa Telecom Cloud Market Outlook, by Function Type, Value (US$ Bn), 2020-2033

- Virtual Network Function (VNF)

- Cloud-native Network Function (CNF)

- Middle East & Africa Telecom Cloud Market Outlook, by Service Type, Value (US$ Bn), 2020-2033

- SaaS

- IaaS

- PaaS

- Middle East & Africa Telecom Cloud Market Outlook, by Country, Value (US$ Bn), 2020-2033

- GCC Telecom Cloud Market Outlook, by Deployment Model, 2020-2033

- GCC Telecom Cloud Market Outlook, by Function Type, 2020-2033

- GCC Telecom Cloud Market Outlook, by Service Type, 2020-2033

- South Africa Telecom Cloud Market Outlook, by Deployment Model, 2020-2033

- South Africa Telecom Cloud Market Outlook, by Function Type, 2020-2033

- South Africa Telecom Cloud Market Outlook, by Service Type, 2020-2033

- Egypt Telecom Cloud Market Outlook, by Deployment Model, 2020-2033

- Egypt Telecom Cloud Market Outlook, by Function Type, 2020-2033

- Egypt Telecom Cloud Market Outlook, by Service Type, 2020-2033

- Nigeria Telecom Cloud Market Outlook, by Deployment Model, 2020-2033

- Nigeria Telecom Cloud Market Outlook, by Function Type, 2020-2033

- Nigeria Telecom Cloud Market Outlook, by Service Type, 2020-2033

- Rest of Middle East Telecom Cloud Market Outlook, by Deployment Model, 2020-2033

- Rest of Middle East Telecom Cloud Market Outlook, by Function Type, 2020-2033

- Rest of Middle East Telecom Cloud Market Outlook, by Service Type, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Middle East & Africa Telecom Cloud Market Outlook, by Deployment Model, Value (US$ Bn), 2020-2033

- Competitive Landscape

- Company Vs Segment Heatmap

- Company Market Share Analysis, 2025

- Competitive Dashboard

- Company Profiles

- Amazon Web Services (AWS)

- Company Overview

- Product Portfolio

- Financial Overview

- Business Strategies and Developments

- Microsoft Azure

- Google Cloud Platform (GCP)

- IBM Cloud

- Oracle Cloud

- Cisco Systems, Inc.

- Nokia

- Ericsson

- Huawei Technologies Co., Ltd.

- Samsung Electronics

- VMware, Inc.

- HPE (Hewlett Packard Enterprise)

- Dell Technologies

- NEC Corporation

- Amdocs Ltd.

- Amazon Web Services (AWS)

- Appendix

- Research Methodology

- Report Assumptions

- Acronyms and Abbreviations

|

BASE YEAR |

HISTORICAL DATA |

FORECAST PERIOD |

UNITS |

|||

|

2025 |

|

2019 - 2024 |

2026 - 2033 |

Value: US$ Million |

||

|

REPORT FEATURES |

DETAILS |

|

By Deployment Model Coverage |

|

|

By Function Type Coverage |

|

|

Geographical Coverage |

|

|

Leading Companies |

|

|

Report Highlights |

Key Market Indicators, Macro-micro economic impact analysis, Technological Roadmap, Key Trends, Driver, Restraints, and Future Opportunities & Revenue Pockets, Porter’s 5 Forces Analysis, Historical Trend (2019-2024), Market Estimates and Forecast, Market Dynamics, Industry Trends, Competition Landscape, Category, Region, Country-wise Trends & Analysis, COVID-19 Impact Analysis (Demand and Supply Chain) |