Architectural Metal Coating Market Size, Share, and Growth Forecast 2026 – 2033

Key Market Highlights

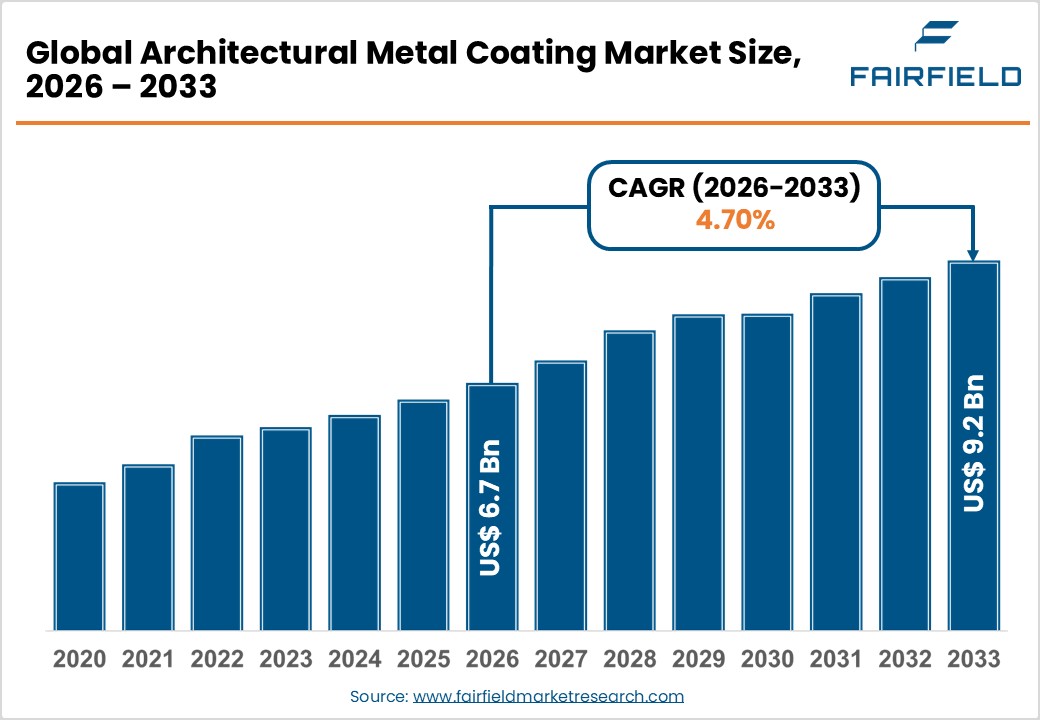

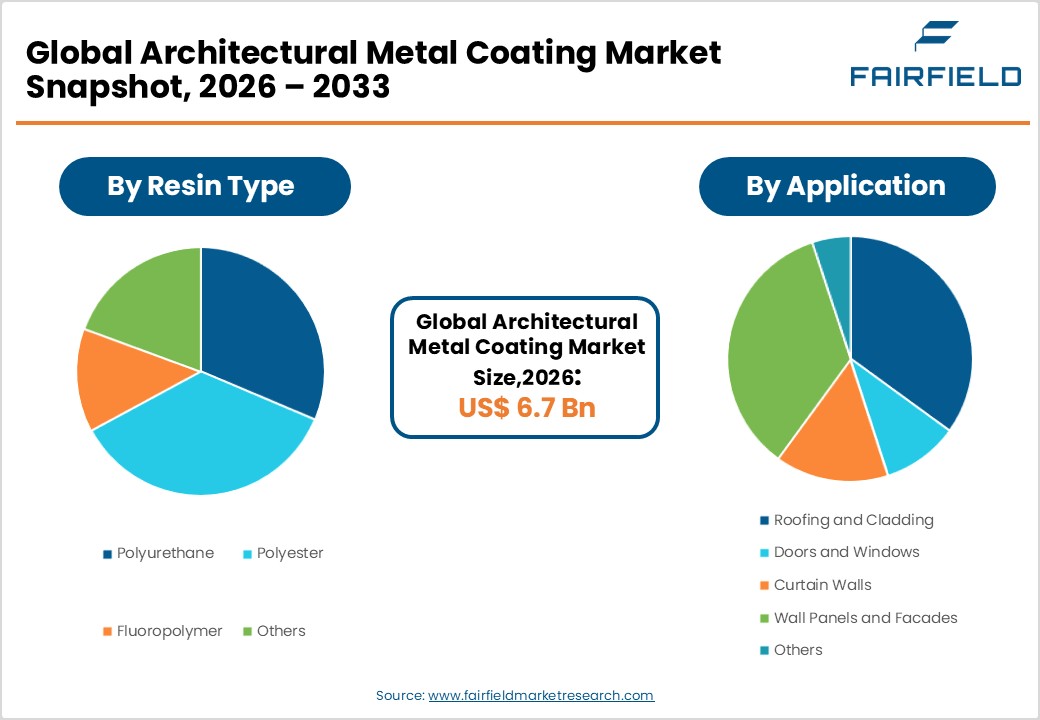

- The global Architectural Metal Coating market size is likely to be valued at US$ 6.7 Billion in 2026 and is expected to reach US$ 9.2 Billion by 2033, growing at a CAGR of 4.70% during the forecast period from 2026 to 2033.

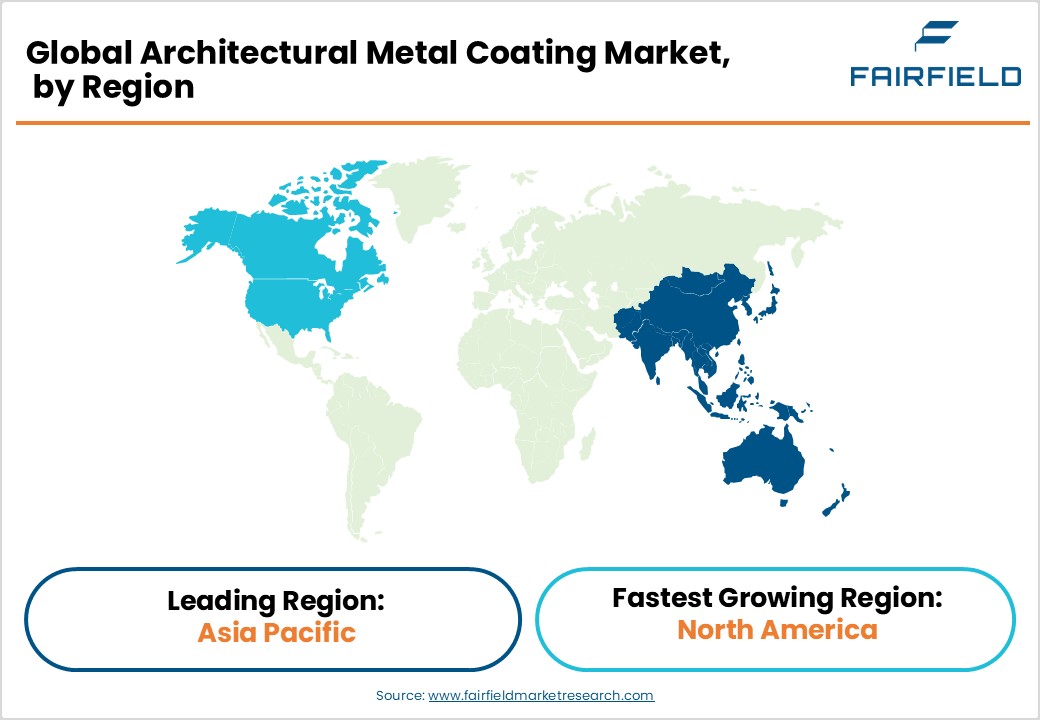

- Asia Pacific dominates the global architectural metal coating market with approximately 45% share, driven by massive urbanization, government infrastructure programs, and the expanding commercial construction sector across China, India, and ASEAN nations.

- North America is the fastest-growing regional market, supported by over US$ 2.0 trillion in annual construction spending, cool-roof mandates, and strong regulatory incentives promoting energy-efficient architectural coatings in commercial and institutional buildings.

- Roofing and Cladding leads by application with approximately 38% share, driven by the widespread adoption of coated metal roofing systems in commercial construction and regulatory requirements for cool-roof compliant coatings across North America and Europe.

- Curtain Walls and Wall Panels & Facades are among the fastest-growing application segments, propelled by rising high-rise commercial construction in Asia Pacific and increasing specification of fluoropolymer coatings for long-life aesthetic performance.

- The rapid expansion of green building certifications (LEED, BREEAM) and energy efficiency mandates globally creates a high-growth opportunity for manufacturers developing sustainable, thermally reflective, and low-VOC architectural metal coating solutions.

Market Dynamics

Market Growth Drivers

- Rising Demand for Sustainable and High-Performance Building Envelopes

The global construction industry's pivot toward sustainable building design has significantly elevated the demand for architectural metal coatings that offer thermal reflectivity, corrosion resistance, and environmental compliance. According to the International Energy Agency (IEA), buildings account for nearly 30% of global energy consumption; as a result, governments and developers are increasingly investing in cool-roof coatings and advanced cladding solutions. Fluoropolymer and polyurethane-based architectural coatings are gaining traction due to their superior weatherability and long service life often exceeding 20 years reducing lifecycle maintenance costs. This focus on operational sustainability continues to position architectural metal coatings as critical components of energy-efficient building designs.

- Accelerating Urbanization and Boom in Commercial Construction

Global urban population is projected to reach 6.7 billion by 2050 according to the United Nations, necessitating a significant expansion of commercial, industrial, and institutional infrastructure. This urban growth is directly correlated with rising demand for metal-clad facades, curtain walls, and architectural roofing systems that require high-quality coatings for protection and aesthetics. The Asian Development Bank (ADB) estimates that Asia alone requires infrastructure investment of over US$ 1.7 trillion per year through 2030. Such massive construction activity is translating into robust off-take for architectural metal coating products, particularly polyester and polyurethane resin-based systems suited for large-scale commercial applications.

Market Restraints

- Volatility in Raw Material Prices

Architectural metal coatings are dependent on petrochemical-derived inputs, including titanium dioxide, resins, and solvents, whose prices are inherently tied to crude oil market fluctuations. The U.S. Bureau of Labor Statistics (BLS) has documented significant producer price index (PPI) swings for chemical intermediates, resulting in unpredictable cost structures for coating manufacturers. This margin compression adversely affects small and mid-sized regional coating producers who lack the scale to absorb input price shocks, limiting competitive pricing strategies and constraining product innovation investments across the market.

- Stringent Environmental Regulations on VOC Emissions

Regulatory frameworks such as the U.S. Environmental Protection Agency (EPA) National Emission Standards and the European Union's Directive 2004/42/EC impose strict limits on volatile organic compound (VOC) emissions from architectural coatings. Compliance with these standards necessitates significant reformulation investments and increases production costs, particularly for solvent-borne coating systems. Smaller manufacturers face disproportionate compliance burdens, while the transition to low-VOC or waterborne systems can affect application performance, creating technical and commercial headwinds across the global architectural metal coating ecosystem.

Market Opportunities

- Expansion of Green Building Certifications and Cool Roof Mandates

Growing adoption of sustainability mandates is creating significant commercial opportunities in the architectural metal coating segment. As of 2023, the USGBC reported over 100,000 LEED-certified projects worldwide, with increasing emphasis on thermally reflective coatings for facades and roofing systems. In the U.S., the DOE's Better Buildings Initiative actively promotes reflective coating adoption in public buildings. Similarly, the European Green Deal targets a 55% reduction in greenhouse gas emissions by 2030, indirectly propelling demand for energy-saving metal coatings. Manufacturers that develop fluoropolymer and solar-reflective coating innovations stand to capture premium pricing in the rapidly expanding green construction market.

- Rising Infrastructure Investment and Smart Cities Development Across Asia Pacific

The Asia Pacific region presents a compelling growth opportunity for architectural metal coating stakeholders, driven by government-led smart city and infrastructure programs. India's Smart Cities Mission encompassing 100 cities and China's continued push under the 14th Five-Year Plan for urban renewal and public infrastructure expansion are generating massive construction activity. According to the World Bank, developing economies in Asia account for over 60% of global construction output growth. This creates a high-volume opportunity for coating manufacturers to supply polyester and polyurethane systems for roofing, curtain walls, and facade cladding projects, particularly in Tier-2 and Tier-3 cities undergoing rapid development.

Segmental Insights

- Resin Type Analysis

Polyurethane leads the architectural metal coating market by resin type, commanding approximately 34% market share. Polyurethane coatings are preferred for their exceptional adhesion properties, high abrasion resistance, and superior gloss retention qualities critical for exposed architectural surfaces. According to the American Coatings Association (ACA), polyurethane-based systems consistently outperform alternatives in accelerated weathering tests, making them ideal for roofing, facades, and curtain wall applications in diverse climatic conditions. The growing adoption of two-component polyurethane coatings in commercial high-rise construction further reinforces segment dominance. Rising product innovation by companies such as PPG Industries and AkzoNobel in UV-stable polyurethane formulations continues to widen the performance gap versus competing resin systems.

- Application Analysis

Roofing and Cladding holds the leading position in the architectural metal coating market by application, accounting for approximately 38% of the total market share. Metal roofing systems, particularly steel and aluminum panels with factory-applied coatings, are widely employed across commercial, industrial, and institutional construction. The Metal Roofing Alliance (MRA) estimates that metal roofing accounts for approximately 15% of the low-slope roofing market in the U.S. and is witnessing consistent growth due to its 40-70 year service life potential. Cool-roof coating requirements under the California Title 24 building code and equivalent standards globally are further accelerating coated metal roofing adoption, solidifying the segment's dominance in the overall architectural metal coating market.

Regional Insights

- North America Architectural Metal Coating Trends

North America represents the fastest-growing regional market for architectural metal coatings, supported by robust construction investment, regulatory innovation incentives, and high adoption of premium coating technologies. The U.S. Census Bureau reported construction spending exceeding US$ 2.0 trillion in 2023, with commercial and institutional segments driving significant demand for high-performance metal facade and roofing coatings. Regulatory frameworks such as ENERGY STAR and California Title 24 building codes are compelling the adoption of thermally reflective and low-VOC architectural coatings.

The U.S. market is characterized by a strong innovation ecosystem, with leading players investing in sustainable coating platforms and waterborne formulations. Canada's push for net-zero buildings under its 2030 Emissions Reduction Plan is additionally generating demand for energy-efficient architectural metal coatings in new commercial developments. The presence of major coating companies including PPG Industries, The Sherwin-Williams Company, and RPM International Inc. provides a technically advanced domestic supply base supporting North America's accelerating market growth.

- Europe Architectural Metal Coating Trends

Europe is a significant and mature market for architectural metal coatings, driven by stringent environmental regulations and a deep commitment to sustainable construction. Germany, France, the U.K., and Spain are key markets, collectively underpinned by the EU Green Deal and the European Commission's Renovation Wave Strategy, which targets doubling the rate of energy-efficient building renovations by 2030. This policy landscape is accelerating demand for high-durability, low-VOC architectural coatings for both new construction and retrofit projects across the region.

Germany's building sector, regulated under the Building Energy Act (GEG), mandates energy-efficient envelope solutions, creating a consistent pull for advanced fluoropolymer and polyurethane coatings. The U.K.'s Future Homes Standard similarly promotes thermally efficient cladding systems. Meanwhile, Spain and France are witnessing increased commercial real estate development, supporting growing off-take for metal facade coatings. Harmonized EN 15217 energy performance standards across the EU further drive specification-level adoption of compliant architectural coatings.

- Asia Pacific Architectural Metal Coating Trends

Asia Pacific is the dominant regional market, holding approximately 45% of global market share, propelled by unprecedented urbanization, manufacturing cost advantages, and large-scale public infrastructure investment. China remains the largest single-country market, with its 14th Five-Year Plan targeting significant public and commercial construction activity across Tier-1 and Tier-2 cities. Japan's advanced construction standards and adoption of high-performance coatings for seismic-resistant building facades maintain steady demand, while India's infrastructure boom underpinned by government programs including PM Gati Shakti and Housing for All is rapidly expanding the addressable market.

ASEAN nations including Vietnam, Indonesia, and Malaysia are witnessing accelerated commercial and industrial construction, supported by foreign direct investment and expanding manufacturing hubs. Regional manufacturers such as Asian Paints Limited, Nippon Paint Holdings, and Kansai Paint are leveraging local production advantages to offer competitively priced products. The Asian Development Bank projects infrastructure investment needs of over US$ 26 trillion across Asia through 2030, underscoring the region's enduring demand trajectory for architectural metal coatings.

Competitive Landscape

The architectural metal coating market is moderately consolidated, with the top five players PPG Industries, AkzoNobel, Sherwin-Williams, Axalta Coating Systems, and BASF SE collectively holding a significant share of global revenues. Market leaders differentiate through proprietary resin chemistry, vertically integrated supply chains, and broad distribution networks. Key strategies include portfolio expansion into waterborne and high-durability fluoropolymer systems, geographic penetration in high-growth Asia Pacific markets, and R&D investment in sustainable, low-VOC formulations. Strategic partnerships with architectural firms, OEM metal fabricators, and sustainability certification bodies are increasingly common business model trends shaping competitive positioning.

Key Developments

- In March 2025, PPG Industries, Inc. launched PPG DURANAR® XL, an enhanced fluoropolymer architectural coating with improved chalk and fade resistance ratings for curtain wall and metal facade applications, targeting LEED-compliant commercial construction projects.

- In October 2024, AkzoNobel N.V. announced an expansion of its Interpon D3000 powder coating range with new low-gloss finishes optimized for architectural aluminum profiles, meeting Qualicoat Class 3 specifications for extreme weather conditions.

- In June 2024, The Sherwin-Williams Company introduced a new generation of its Coil Coatings platform featuring bio-based polyester resin technology, reducing the carbon footprint of architectural metal coatings by approximately 18% versus conventional systems.

Companies Covered in Architectural Metal Coating Market

- PPG Industries, Inc.

- AkzoNobel N.V.

- The Sherwin-Williams Company

- RPM International Inc.

- Axalta Coating Systems Ltd.

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- Asian Paints Limited

- BASF SE

- Jotun A/S

- Valspar (part of Sherwin-Williams)

- Carlisle Companies Incorporated

- Henkel AG & Co. KGaA

- Axson Technologies

- The Crown Paints Ltd.

- Tiger Drylac Group

- Teknos Group

- Beckers Group

- Wacker Chemie AG

Market Segmentation

By Resin Type

- Polyurethane

- Polyester

- Fluoropolymer

- Others

By Application

- Roofing and Cladding

- Doors and Windows

- Curtain Walls

- Wall Panels and Facades

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Executive Summary

- Global Architectural Metal Coating Market Snapshot

- Future Projections

- Key Market Trends

- Regional Snapshot, by Value, 2026

- Analyst Recommendations

- Market Overview

- Market Definitions and Segmentations

- Market Dynamics

- Drivers

- Restraints

- Market Opportunities

- Value Chain Analysis

- COVID-19 Impact Analysis

- Porter's Five Forces Analysis

- Impact of Russia-Ukraine Conflict

- PESTLE Analysis

- Regulatory Analysis

- Price Trend Analysis

- Current Prices and Future Projections, 2025-2033

- Price Impact Factors

- Global Architectural Metal Coating Market Outlook, 2020 - 2033

- Global Architectural Metal Coating Market Outlook, by Resin Type, Value (US$ Bn), 2020-2033

- Polyurethane

- Polyester

- Fluoropolymer

- Others

- Global Architectural Metal Coating Market Outlook, by Application, Value (US$ Bn), 2020-2033

- Roofing and Cladding

- Doors and Windows

- Curtain Walls

- Wall Panels and Facades

- Others

- Global Architectural Metal Coating Market Outlook, by Region, Value (US$ Bn), 2020-2033

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Global Architectural Metal Coating Market Outlook, by Resin Type, Value (US$ Bn), 2020-2033

- North America Architectural Metal Coating Market Outlook, 2020 - 2033

- North America Architectural Metal Coating Market Outlook, by Resin Type, Value (US$ Bn), 2020-2033

- Polyurethane

- Polyester

- Fluoropolymer

- Others

- North America Architectural Metal Coating Market Outlook, by Application, Value (US$ Bn), 2020-2033

- Roofing and Cladding

- Doors and Windows

- Curtain Walls

- Wall Panels and Facades

- Others

- North America Architectural Metal Coating Market Outlook, by Country, Value (US$ Bn), 2020-2033

- U.S. Architectural Metal Coating Market Outlook, by Resin Type, 2020-2033

- U.S. Architectural Metal Coating Market Outlook, by Application, 2020-2033

- Canada Architectural Metal Coating Market Outlook, by Resin Type, 2020-2033

- Canada Architectural Metal Coating Market Outlook, by Application, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- North America Architectural Metal Coating Market Outlook, by Resin Type, Value (US$ Bn), 2020-2033

- Europe Architectural Metal Coating Market Outlook, 2020 - 2033

- Europe Architectural Metal Coating Market Outlook, by Resin Type, Value (US$ Bn), 2020-2033

- Polyurethane

- Polyester

- Fluoropolymer

- Others

- Europe Architectural Metal Coating Market Outlook, by Application, Value (US$ Bn), 2020-2033

- Roofing and Cladding

- Doors and Windows

- Curtain Walls

- Wall Panels and Facades

- Others

- Europe Architectural Metal Coating Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Germany Architectural Metal Coating Market Outlook, by Resin Type, 2020-2033

- Germany Architectural Metal Coating Market Outlook, by Application, 2020-2033

- Italy Architectural Metal Coating Market Outlook, by Resin Type, 2020-2033

- Italy Architectural Metal Coating Market Outlook, by Application, 2020-2033

- France Architectural Metal Coating Market Outlook, by Resin Type, 2020-2033

- France Architectural Metal Coating Market Outlook, by Application, 2020-2033

- U.K. Architectural Metal Coating Market Outlook, by Resin Type, 2020-2033

- U.K. Architectural Metal Coating Market Outlook, by Application, 2020-2033

- Spain Architectural Metal Coating Market Outlook, by Resin Type, 2020-2033

- Spain Architectural Metal Coating Market Outlook, by Application, 2020-2033

- Russia Architectural Metal Coating Market Outlook, by Resin Type, 2020-2033

- Russia Architectural Metal Coating Market Outlook, by Application, 2020-2033

- Rest of Europe Architectural Metal Coating Market Outlook, by Resin Type, 2020-2033

- Rest of Europe Architectural Metal Coating Market Outlook, by Application, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Europe Architectural Metal Coating Market Outlook, by Resin Type, Value (US$ Bn), 2020-2033

- Asia Pacific Architectural Metal Coating Market Outlook, 2020 - 2033

- Asia Pacific Architectural Metal Coating Market Outlook, by Resin Type, Value (US$ Bn), 2020-2033

- Polyurethane

- Polyester

- Fluoropolymer

- Others

- Asia Pacific Architectural Metal Coating Market Outlook, by Application, Value (US$ Bn), 2020-2033

- Roofing and Cladding

- Doors and Windows

- Curtain Walls

- Wall Panels and Facades

- Others

- Asia Pacific Architectural Metal Coating Market Outlook, by Country, Value (US$ Bn), 2020-2033

- China Architectural Metal Coating Market Outlook, by Resin Type, 2020-2033

- China Architectural Metal Coating Market Outlook, by Application, 2020-2033

- Japan Architectural Metal Coating Market Outlook, by Resin Type, 2020-2033

- Japan Architectural Metal Coating Market Outlook, by Application, 2020-2033

- South Korea Architectural Metal Coating Market Outlook, by Resin Type, 2020-2033

- South Korea Architectural Metal Coating Market Outlook, by Application, 2020-2033

- India Architectural Metal Coating Market Outlook, by Resin Type, 2020-2033

- India Architectural Metal Coating Market Outlook, by Application, 2020-2033

- Southeast Asia Architectural Metal Coating Market Outlook, by Resin Type, 2020-2033

- Southeast Asia Architectural Metal Coating Market Outlook, by Application, 2020-2033

- Rest of SAO Architectural Metal Coating Market Outlook, by Resin Type, 2020-2033

- Rest of SAO Architectural Metal Coating Market Outlook, by Application, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Asia Pacific Architectural Metal Coating Market Outlook, by Resin Type, Value (US$ Bn), 2020-2033

- Latin America Architectural Metal Coating Market Outlook, 2020 - 2033

- Latin America Architectural Metal Coating Market Outlook, by Resin Type, Value (US$ Bn), 2020-2033

- Polyurethane

- Polyester

- Fluoropolymer

- Others

- Latin America Architectural Metal Coating Market Outlook, by Application, Value (US$ Bn), 2020-2033

- Roofing and Cladding

- Doors and Windows

- Curtain Walls

- Wall Panels and Facades

- Others

- Latin America Architectural Metal Coating Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Brazil Architectural Metal Coating Market Outlook, by Resin Type, 2020-2033

- Brazil Architectural Metal Coating Market Outlook, by Application, 2020-2033

- Mexico Architectural Metal Coating Market Outlook, by Resin Type, 2020-2033

- Mexico Architectural Metal Coating Market Outlook, by Application, 2020-2033

- Argentina Architectural Metal Coating Market Outlook, by Resin Type, 2020-2033

- Argentina Architectural Metal Coating Market Outlook, by Application, 2020-2033

- Rest of LATAM Architectural Metal Coating Market Outlook, by Resin Type, 2020-2033

- Rest of LATAM Architectural Metal Coating Market Outlook, by Application, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Latin America Architectural Metal Coating Market Outlook, by Resin Type, Value (US$ Bn), 2020-2033

- Middle East & Africa Architectural Metal Coating Market Outlook, 2020 - 2033

- Middle East & Africa Architectural Metal Coating Market Outlook, by Resin Type, Value (US$ Bn), 2020-2033

- Polyurethane

- Polyester

- Fluoropolymer

- Others

- Middle East & Africa Architectural Metal Coating Market Outlook, by Application, Value (US$ Bn), 2020-2033

- Roofing and Cladding

- Doors and Windows

- Curtain Walls

- Wall Panels and Facades

- Others

- Middle East & Africa Architectural Metal Coating Market Outlook, by Country, Value (US$ Bn), 2020-2033

- GCC Architectural Metal Coating Market Outlook, by Resin Type, 2020-2033

- GCC Architectural Metal Coating Market Outlook, by Application, 2020-2033

- South Africa Architectural Metal Coating Market Outlook, by Resin Type, 2020-2033

- South Africa Architectural Metal Coating Market Outlook, by Application, 2020-2033

- Egypt Architectural Metal Coating Market Outlook, by Resin Type, 2020-2033

- Egypt Architectural Metal Coating Market Outlook, by Application, 2020-2033

- Nigeria Architectural Metal Coating Market Outlook, by Resin Type, 2020-2033

- Nigeria Architectural Metal Coating Market Outlook, by Application, 2020-2033

- Rest of Middle East Architectural Metal Coating Market Outlook, by Resin Type, 2020-2033

- Rest of Middle East Architectural Metal Coating Market Outlook, by Application, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Middle East & Africa Architectural Metal Coating Market Outlook, by Resin Type, Value (US$ Bn), 2020-2033

- Competitive Landscape

- Company Vs Segment Heatmap

- Company Market Share Analysis, 2025

- Competitive Dashboard

- Company Profiles

- PPG Industries, Inc.

- Company Overview

- Product Portfolio

- Financial Overview

- Business Strategies and Developments

- AkzoNobel N.V.

- The Sherwin Williams Company

- RPM International Inc.

- Axalta Coating Systems Ltd.

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- Asian Paints Limited

- BASF SE

- Jotun A/S

- Valspar (part of Sherwin Williams)

- Carlisle Companies Incorporated

- Henkel AG & Co. KGaA

- Axson Technologies

- The Crown Paints Ltd.

- PPG Industries, Inc.

- Appendix

- Research Methodology

- Report Assumptions

- Acronyms and Abbreviations

|

BASE YEAR |

HISTORICAL DATA |

FORECAST PERIOD |

UNITS |

|||

|

2025 |

|

2020 - 2025 |

2026 - 2033 |

Value: US$ Million |

||

|

REPORT FEATURES |

DETAILS |

|

By Resin Type Coverage |

|

|

By Application Coverage |

|

|

Geographical Coverage |

|

|

Leading Companies |

|

|

Report Highlights |

Key Market Indicators, Macro-micro economic impact analysis, Technological Roadmap, Key Trends, Driver, Restraints, and Future Opportunities & Revenue Pockets, Porter’s 5 Forces Analysis, Historical Trend (2019-2024), Market Estimates and Forecast, Market Dynamics, Industry Trends, Competition Landscape, Category, Region, Country-wise Trends & Analysis, COVID-19 Impact Analysis (Demand and Supply Chain) |