Bubble Tea Market Size, Share, and Growth Forecast 2026 - 2033

Key Market Highlights

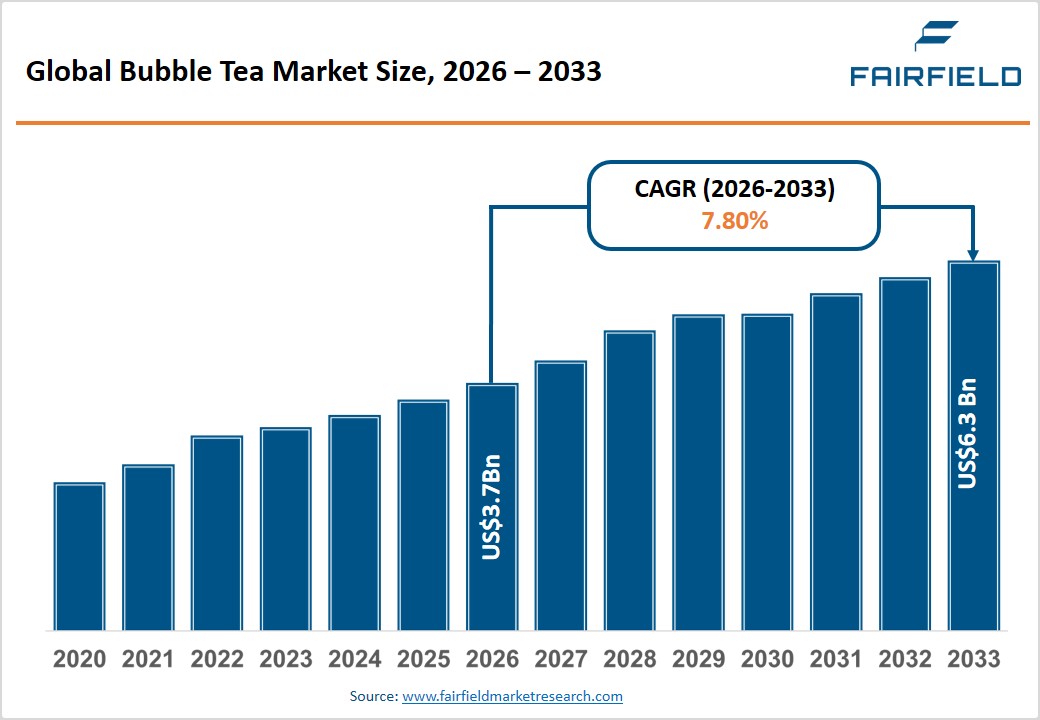

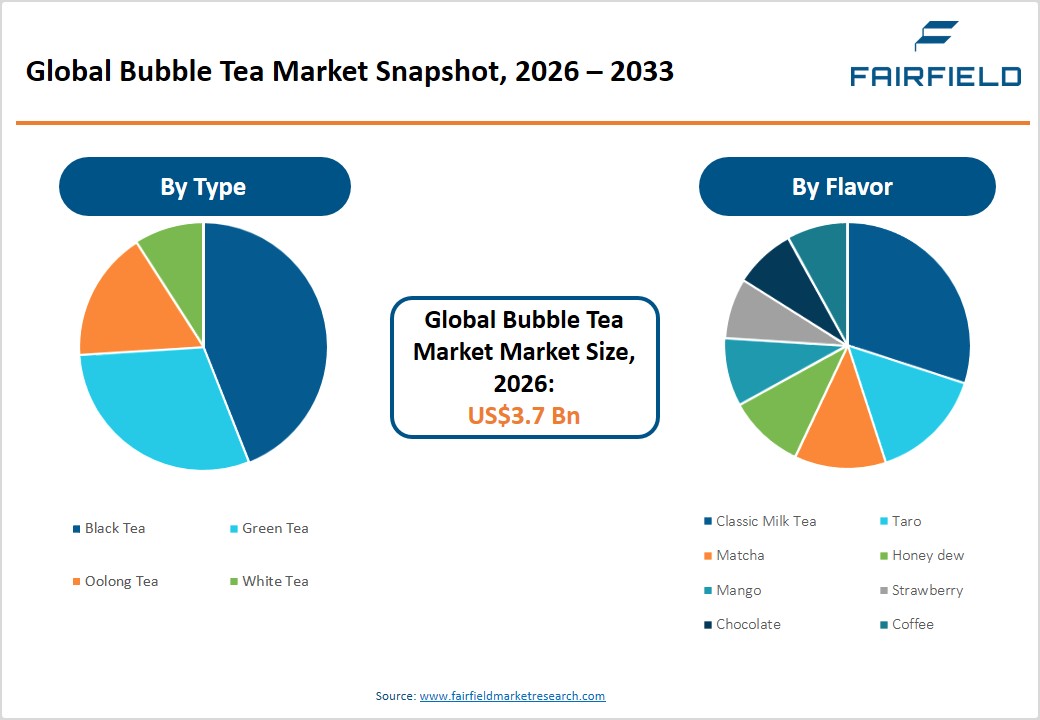

- The global bubble tea market size is likely to be valued at USD 3.7 billion in 2026 and is expected to reach USD 6.3 billion by 2033, growing at a CAGR of 7.80% during the forecast period from 2026 to 2033.

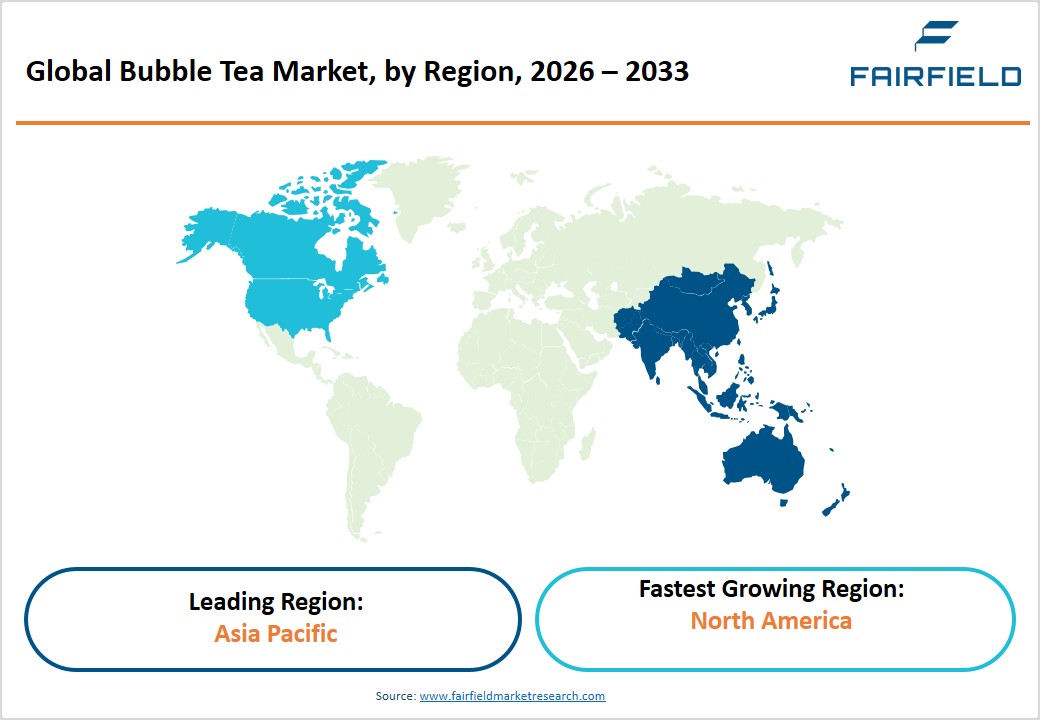

- Leading Region Market: Asia Pacific leads the global bubble tea market with approximately 45% of total revenue, underpinned by Taiwan's origin heritage, deep-rooted tea-drinking culture, and a high density of franchise and independent operators across China, Japan, and ASEAN

- Fastest Growing Region Market: North America is the fastest-growing regional bubble tea market, driven by a culturally diverse population, rapidly expanding Asian-American communities, and accelerating franchise growth by brands such as Kung Fu Tea, which surpassed 400 U.S. outlets in 2024.

- Dominant Segment: Black Tea-based Bubble Tea holds the leading share approximately 45% in the By Type category, supported by global black tea familiarity, versatile flavor pairing capabilities, and consistent raw material availability from major producing nations including China and India.

- Fastest Growing Segment: The Online Retail distribution channel is the fastest-growing segment, propelled by rising e-commerce adoption, RTD bubble tea product launches by brands such as Quickly, and sustained post-pandemic consumer interest in home preparation kits and packaged bubble tea formats.

- Key Market Opportunity: The proliferation of ready-to-drink (RTD) and packaged bubble tea products sold via online retail channels represents a major growth opportunity, enabling brands to penetrate markets with limited physical store infrastructure and establish diversified revenue streams beyond brick-and-mortar operations.

Market Dynamics

Market Growth Drivers

Rising Interest in Flexible and Health-Focused Beverage Options

The growing preference among millennials and Gen Z consumers for customizable, visually appealing beverages represents a pivotal driver of the bubble tea market. According to the International Tea Committee, global tea consumption has been rising steadily, with specialty tea segments outpacing conventional categories in volume growth. Bubble tea, with its diverse array of bases, flavors, and toppings, aligns perfectly with consumer desire for personalized beverage experiences. The ability to tailor sweetness levels, milk options including dairy-free alternatives and toppings such as tapioca pearls or jelly cubes enhances consumer loyalty. In 2023, plant-based milk alternatives accounted for a rapidly growing proportion of milk tea orders, particularly in the United States, United Kingdom, and Australia, reinforcing the product's adaptability to evolving dietary preferences and driving sustained market traction.

Health-Conscious Shift Away from Carbonated Soft Drinks

Health-conscious consumers are transitioning from carbonated soft drinks to tea-based alternatives, recognizing bubble tea as a functional beverage that provides antioxidants and has lower acidity compared to colas. This shift is being amplified by policy changes the UK's sugar levy, which increased in 2024, has made bubble tea a cost-effective option compared to premium carbonated drinks, particularly among university students. A pivotal indicator of this industry pivot emerged in November 2025, Coca-Cola introduced Cappy Bubble, its boba-infused juice, signaling that carbonated beverage leaders increasingly view tea-based drinks as a permanent rival, not a fleeting trend. On the product side, traditional milk tea offerings have been complemented by fruit-based teas, cheese teas, low-sugar variants, and plant-based formulations, aligning with broader wellness and clean-label trends. Lactose-free milk, oat milk, and reduced-calorie sweeteners have been increasingly incorporated to address health-conscious consumers without compromising taste.

Market Restraints

Intense Competition from Alternative Caffeinated & Functional Beverages

The widespread availability of rival caffeinated drinks such as coffee (booming in Western markets) and chocolate along with entrenched consumption habits, acts as a key barrier to bubble tea's growth, through 2025–2030. The growing availability of suitable alternatives like unsweetened tea, coconut water, and fruit-infused teas, which offer benefits similar to bubble tea, is also hampering market expansion. Competitive pressure is intensifying at the institutional level as well in May 2025, major international coffee retailers began an aggressive expansion of fruit-based jelly drinks, directly challenging the market share of bubble tea in urban centers. In the European context specifically, bubble tea is facing a considerable challenge in the form of competition from well-established beverage categories like coffee, where deeply entrenched café culture creates significant consumer loyalty that bubble tea brands must overcome to establish durable market share.

Supply Chain Vulnerabilities for Key Raw Materials

The bubble tea market is heavily reliant on the consistent supply of tapioca pearls, derived from cassava starch primarily sourced from Thailand, Vietnam, and Taiwan. Disruptions in cassava cultivation caused by climate events, export restrictions, or logistical bottlenecks directly impact production costs and product availability. Global tapioca shortages caused significant supply disruptions across multiple markets, exposing the sector's supply chain fragility. Fluctuating global tea prices driven by erratic weather patterns in major producing nations including China and India further contribute to input cost volatility, squeezing operator margins and leading to inconsistent product quality that adversely affects brand reputation and consumer retention.

Market Opportunities

Premiumization & Functional Ingredient Innovation

Consumer willingness to pay a premium for health-aligned, ingredient-transparent bubble tea formulations is creating a high-margin product opportunity for forward-looking brands. The availability of low-sugar bubble tea and fruit-infused tea has broadened appeal, with some chains reporting a 15% sales increase from this segment alone. Innovation is moving beyond sugar reduction in April 2025, a wellness-focused beverage company debuted a new line of prebiotic-infused pearls aimed at improving gut health, catering to health-conscious consumers. Supply chain transparency is also emerging as a differentiator: oolong producers are adopting blockchain-based traceability systems, enabling consumers to verify harvest dates and processing methods via QR codes a feature that resonates with Gen Z consumers who prioritize authenticity. Together, these innovations allow brands to command higher average selling prices while competing directly against premium café beverages rather than only within the boba category.

Online Retail and Ready-to-Drink (RTD) Bubble Tea Segment

The expansion of e-commerce and the emergence of ready-to-drink (RTD) bubble tea products present significant untapped commercial opportunities. Retail platforms such as Amazon and regional supermarket chains are increasingly stocking packaged bubble tea kits, concentrates, and instant tapioca pearl sets, enabling consumers to replicate the café experience at home. According to the Food and Agriculture Organization (FAO), global packaged beverages sold via online retail channels demonstrated robust growth during 2020–2023, a trend that has sustained post-pandemic. In 2024, Quickly launched a line of shelf-stable bubble tea products for retail distribution across North America and Europe. This segment opens new revenue streams for traditional brands, reducing dependence on brick-and-mortar outlets and enabling penetration of geographies with limited physical store infrastructure.

Segmental Insights

By Tea Type Analysis

The Black Tea-based Bubble Tea segment holds the dominant position in the global bubble tea market by tea type, accounting for approximately 45% of total market revenue. Black tea's robust and versatile flavor profile complements the sweetness of flavored syrups and the characteristic chewiness of tapioca pearls, making it the foundational ingredient for the most popular classic milk tea variants. According to the China Tea Marketing Association and the Tea Board of India, black tea remains the most widely consumed tea variety globally, providing a strong and reliable raw material base. Its widespread consumer familiarity across Asia Pacific, North America, and Europe ensures consistent demand. Black tea-based formulations also offer superior shelf stability, which is advantageous for ready-to-drink and pre-packaged bubble tea products, reinforcing the segment's sustained leadership.

By Flavor Analysis

The Classic Milk Tea flavor segment commands the leading position in the bubble tea market, capturing an estimated 38% market share by flavor category. Its widespread consumer familiarity and status as the original bubble tea offering underpin its commercial dominance. Classic Milk Tea serves as the benchmark flavor from which all subsequent variations are derived, consistently ranking as the top-ordered item across major franchise chains including Gong Cha, Chatime, and CoCo Fresh Tea & Juice. Consumer survey data confirms that classic milk tea consistently ranks as the top preference across diverse age groups and geographies. Its adaptability available in hot, cold, or blended formats combined with extensive customization options in sweetness and ice levels, sustains its leadership in a highly competitive and innovation-driven flavor landscape.

By Distribution Channel Analysis

The Business to Consumer (B2C) segment encompassing direct-sale bubble tea cafés, kiosks, and branded storefronts holds the leading position in the bubble tea distribution channel landscape, estimated at approximately 62% of total channel revenue. The experiential nature of bubble tea consumption, where real-time customization and product freshness are core value propositions, makes in-store purchasing the preferred modality for the majority of consumers. Physical outlets enable brands to deliver tailored experiences including adjustable sweetness levels, ice quantities, and topping selections that enhance overall satisfaction., café-format beverage businesses demonstrated strong resilience in post-pandemic foot traffic recovery. Leading brands such as Tiger Sugar and Boba Guys leverage ambiance-driven retail strategies and social media-worthy aesthetics to engage younger demographics.

Regional Insights

North America Bubble Tea Trends

North America is the fastest-growing regional market for bubble tea, driven by demographic diversity, the rapid growth of Asian-American communities, and the mainstream adoption of Asian food and beverage trends. The United States leads regional consumption, with a dense concentration of bubble tea outlets in major metropolitan areas. In 2024, Kung Fu Tea surpassed 400 outlets nationwide, affirming the strength of consumer demand. Regulatory frameworks administered by the U.S. Food and Drug Administration (FDA) including mandatory calorie disclosure requirements for chain restaurants under the Affordable Care Act have incentivized operators to invest in reduced-sugar and dairy-free formulations, fostering product innovation.

Canada is also experiencing notable market expansion, particularly in Toronto and Vancouver, supported by large immigrant communities with established familiarity with bubble tea culture. The growing influence of social media on F&B discovery continues to accelerate trial and repeat purchases among younger demographics. Regional franchisors are increasingly partnering with delivery aggregators such as DoorDash and Uber Eats to reach consumers beyond physical outlets, further expanding the bubble tea market's reach across North American geographies.

Europe Bubble Tea Trends

Europe's bubble tea market is gaining momentum, with the United Kingdom, Germany, France, and Spain emerging as primary growth markets. The U.K. leads regional consumption, underpinned by a sizable East Asian diaspora and growing mainstream consumer interest in global beverage trends. Leading franchise brands including Gong Cha and Chatime have established multi-outlet presences across London, Manchester, and Birmingham. The European Food Safety Authority (EFSA) regulates novel food ingredients associated with bubble tea production, including certain tapioca-based additives, ensuring consumer safety and bolstering market confidence.

In Germany and France, brands are expanding through cost-efficient mall-based kiosk formats, reducing real estate expenditure while maximizing consumer footfall. Sugar taxation policies across several EU member states are accelerating investment in health-conscious formulations incorporating natural sweeteners such as monk fruit and stevia. Regulatory harmonization under the EU Food Law framework provides a consistent compliance infrastructure for brands expanding across multiple European markets, streamlining product development, labeling requirements, and market entry strategies for both established chains and emerging operators.

Asia Pacific Bubble Tea Trends

Asia Pacific dominates the global bubble tea market, accounting for approximately 45% of total revenue. The region benefits from its status as the birthplace of bubble tea in Taiwan during the 1980s, deeply embedded tea-drinking cultures, abundant raw material availability, and a high density of both independent and franchise operators. China is the large national market, supported by a massive consumer base, rapid urbanization, and a vibrant café culture. Taiwanese heritage brands such as Sharetea and Tea Ren's Tea Time continue to maintain strong domestic market leadership while simultaneously driving global category exports.

India and Southeast Asian markets including Thailand, Vietnam, Indonesia, and the Philippines are witnessing accelerated growth driven by large youth populations and rising disposable incomes. According to the Asian Development Bank, Southeast Asia's middle-income groups is projected to expand substantially through 2030, directly fueling premium beverage demand. Japan's bubble tea market continues to evolve with premium matcha and hojicha-infused variants gaining consumer traction. Manufacturing advantages, including geographic proximity to tapioca and tea production hubs, maintain competitive operational cost structures across the region, supporting both domestic consumption and export growth.

Competitive Landscape

The global bubble tea market exhibits a moderately fragmented competitive landscape, characterized by the coexistence of large international franchise chains and numerous regional or independent operators. Leading players including Gong Cha, Chatime, CoCo Fresh Tea & Juice, and Kung Fu Tea pursue aggressive franchise expansion strategies while differentiating through proprietary tea blends, seasonal menu innovations, and digital loyalty programs. Smaller artisanal brands compete through premium ingredient positioning and locally inspired flavor curation. Digital ordering platforms, mobile loyalty applications, and social media-driven marketing are increasingly critical competitive differentiators. Strategic vertical integration particularly in tapioca pearl and tea concentrate sourcing is emerging as a pivotal competitive lever for market leaders seeking cost optimization and supply chain resilience.

Key Market Developments

- March 2024: Gong Cha announced the opening of its 2,000th global outlet, marking a landmark milestone in the brand's international franchise expansion strategy across Asia, North America, and Europe, reinforcing its position as one of the world's largest bubble tea chains.

- January 2025: Chatime launched a new line of reduced-sugar bubble tea products featuring natural sweeteners, directly responding to escalating regulatory scrutiny and shifting consumer preferences toward healthier and lower-calorie beverage options across its global markets.

- September 2023: Tiger Sugar expanded into the Middle East through a strategic partnership with a regional franchise operator, establishing new outlets in Dubai and Abu Dhabi to capitalize on the region's growing appetite for premium and experiential beverages.

Companies Covered in Bubble Tea Market

- Gong Cha

- Kung Fu Tea

- Tiger Sugar

- Sharetea

- Boba Guys

- Tapioca Express

- Chatime

- Tea Ren's Tea Time

- CoCo Fresh Tea & Juice

- Quickly

- Happy Lemon

- DaBoba

- Cojiitii

- TACHUNGHO

- Xing Fu Tang

- The Alley

- Machi Machi

- Others

Market Segmentation

By Tea Type

- Black Tea-based Bubble Tea

- Green Tea-based Bubble Tea

- Oolong Tea-based Bubble Tea

- White Tea-based Bubble Tea

By Flavor

- Classic Milk Tea

- Taro

- Matcha

- Honeydew

- Mango

- Strawberry

- Chocolate

- Coffee

By Distribution Channel

- Business to Business Sales of Bubble Tea

- Business to Consumer Sales of Bubble Tea

- Hypermarkets/Supermarkets

- Convenience Stores

- Online Retail

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Executive Summary

- Global Bubble Tea Market Snapshot

- Future Projections

- Key Market Trends

- Regional Snapshot, by Value, 2026

- Analyst Recommendations

- Market Overview

- Market Definitions and Segmentations

- Market Dynamics

- Drivers

- Restraints

- Market Opportunities

- Value Chain Analysis

- COVID-19 Impact Analysis

- Porter's Five Forces Analysis

- Impact of Russia-Ukraine Conflict

- PESTLE Analysis

- Regulatory Analysis

- Price Trend Analysis

- Current Prices and Future Projections, 2025-2033

- Price Impact Factors

- Global Bubble Tea Market Outlook, 2020 - 2033

- Global Bubble Tea Market Outlook, By Type:, Value (US$ Mn), 2020-2033

- Black Tea-based Bubble Tea

- Green Tea-based Bubble Tea

- Oolong Tea-based Bubble Tea

- White Tea-based Bubble Tea

- Global Bubble Tea Market Outlook, By Flavor:, Value (US$ Mn), 2020-2033

- Classic Milk Tea

- Taro

- Matcha

- Honeydew

- Mango

- Strawberry

- Chocolate

- Coffee

- Global Bubble Tea Market Outlook, By Distribution Channel:, Value (US$ Mn), 2020-2033

- Business to Business Sales of Bubble Tea

- Business to Consumer Sales of Bubble Tea

- Hypermarkets/Supermarkets

- Convenience Stores

- Online Retail

- Global Bubble Tea Market Outlook, by Region, Value (US$ Mn), 2020-2033

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Global Bubble Tea Market Outlook, By Type:, Value (US$ Mn), 2020-2033

- North America Bubble Tea Market Outlook, 2020 - 2033

- North America Bubble Tea Market Outlook, By Type:, Value (US$ Mn), 2020-2033

- Black Tea-based Bubble Tea

- Green Tea-based Bubble Tea

- Oolong Tea-based Bubble Tea

- White Tea-based Bubble Tea

- North America Bubble Tea Market Outlook, By Flavor:, Value (US$ Mn), 2020-2033

- Classic Milk Tea

- Taro

- Matcha

- Honeydew

- Mango

- Strawberry

- Chocolate

- Coffee

- North America Bubble Tea Market Outlook, By Distribution Channel:, Value (US$ Mn), 2020-2033

- Business to Business Sales of Bubble Tea

- Business to Consumer Sales of Bubble Tea

- Hypermarkets/Supermarkets

- Convenience Stores

- Online Retail

- North America Bubble Tea Market Outlook, by Country, Value (US$ Mn), 2020-2033

- U.S. Bubble Tea Market Outlook, By Type:, 2020-2033

- U.S. Bubble Tea Market Outlook, By Flavor:, 2020-2033

- U.S. Bubble Tea Market Outlook, By Distribution Channel:, 2020-2033

- Canada Bubble Tea Market Outlook, By Type:, 2020-2033

- Canada Bubble Tea Market Outlook, By Flavor:, 2020-2033

- Canada Bubble Tea Market Outlook, By Distribution Channel:, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- North America Bubble Tea Market Outlook, By Type:, Value (US$ Mn), 2020-2033

- Europe Bubble Tea Market Outlook, 2020 - 2033

- Europe Bubble Tea Market Outlook, By Type:, Value (US$ Mn), 2020-2033

- Black Tea-based Bubble Tea

- Green Tea-based Bubble Tea

- Oolong Tea-based Bubble Tea

- White Tea-based Bubble Tea

- Europe Bubble Tea Market Outlook, By Flavor:, Value (US$ Mn), 2020-2033

- Classic Milk Tea

- Taro

- Matcha

- Honeydew

- Mango

- Strawberry

- Chocolate

- Coffee

- Europe Bubble Tea Market Outlook, By Distribution Channel:, Value (US$ Mn), 2020-2033

- Business to Business Sales of Bubble Tea

- Business to Consumer Sales of Bubble Tea

- Hypermarkets/Supermarkets

- Convenience Stores

- Online Retail

- Europe Bubble Tea Market Outlook, by Country, Value (US$ Mn), 2020-2033

- Germany Bubble Tea Market Outlook, By Type:, 2020-2033

- Germany Bubble Tea Market Outlook, By Flavor:, 2020-2033

- Germany Bubble Tea Market Outlook, By Distribution Channel:, 2020-2033

- Italy Bubble Tea Market Outlook, By Type:, 2020-2033

- Italy Bubble Tea Market Outlook, By Flavor:, 2020-2033

- Italy Bubble Tea Market Outlook, By Distribution Channel:, 2020-2033

- France Bubble Tea Market Outlook, By Type:, 2020-2033

- France Bubble Tea Market Outlook, By Flavor:, 2020-2033

- France Bubble Tea Market Outlook, By Distribution Channel:, 2020-2033

- U.K. Bubble Tea Market Outlook, By Type:, 2020-2033

- U.K. Bubble Tea Market Outlook, By Flavor:, 2020-2033

- U.K. Bubble Tea Market Outlook, By Distribution Channel:, 2020-2033

- Spain Bubble Tea Market Outlook, By Type:, 2020-2033

- Spain Bubble Tea Market Outlook, By Flavor:, 2020-2033

- Spain Bubble Tea Market Outlook, By Distribution Channel:, 2020-2033

- Russia Bubble Tea Market Outlook, By Type:, 2020-2033

- Russia Bubble Tea Market Outlook, By Flavor:, 2020-2033

- Russia Bubble Tea Market Outlook, By Distribution Channel:, 2020-2033

- Rest of Europe Bubble Tea Market Outlook, By Type:, 2020-2033

- Rest of Europe Bubble Tea Market Outlook, By Flavor:, 2020-2033

- Rest of Europe Bubble Tea Market Outlook, By Distribution Channel:, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Europe Bubble Tea Market Outlook, By Type:, Value (US$ Mn), 2020-2033

- Asia Pacific Bubble Tea Market Outlook, 2020 - 2033

- Asia Pacific Bubble Tea Market Outlook, By Type:, Value (US$ Mn), 2020-2033

- Black Tea-based Bubble Tea

- Green Tea-based Bubble Tea

- Oolong Tea-based Bubble Tea

- White Tea-based Bubble Tea

- Asia Pacific Bubble Tea Market Outlook, By Flavor:, Value (US$ Mn), 2020-2033

- Classic Milk Tea

- Taro

- Matcha

- Honeydew

- Mango

- Strawberry

- Chocolate

- Coffee

- Asia Pacific Bubble Tea Market Outlook, By Distribution Channel:, Value (US$ Mn), 2020-2033

- Business to Business Sales of Bubble Tea

- Business to Consumer Sales of Bubble Tea

- Hypermarkets/Supermarkets

- Convenience Stores

- Online Retail

- Asia Pacific Bubble Tea Market Outlook, by Country, Value (US$ Mn), 2020-2033

- China Bubble Tea Market Outlook, By Type:, 2020-2033

- China Bubble Tea Market Outlook, By Flavor:, 2020-2033

- China Bubble Tea Market Outlook, By Distribution Channel:, 2020-2033

- Japan Bubble Tea Market Outlook, By Type:, 2020-2033

- Japan Bubble Tea Market Outlook, By Flavor:, 2020-2033

- Japan Bubble Tea Market Outlook, By Distribution Channel:, 2020-2033

- South Korea Bubble Tea Market Outlook, By Type:, 2020-2033

- South Korea Bubble Tea Market Outlook, By Flavor:, 2020-2033

- South Korea Bubble Tea Market Outlook, By Distribution Channel:, 2020-2033

- India Bubble Tea Market Outlook, By Type:, 2020-2033

- India Bubble Tea Market Outlook, By Flavor:, 2020-2033

- India Bubble Tea Market Outlook, By Distribution Channel:, 2020-2033

- Southeast Asia Bubble Tea Market Outlook, By Type:, 2020-2033

- Southeast Asia Bubble Tea Market Outlook, By Flavor:, 2020-2033

- Southeast Asia Bubble Tea Market Outlook, By Distribution Channel:, 2020-2033

- Rest of SAO Bubble Tea Market Outlook, By Type:, 2020-2033

- Rest of SAO Bubble Tea Market Outlook, By Flavor:, 2020-2033

- Rest of SAO Bubble Tea Market Outlook, By Distribution Channel:, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Asia Pacific Bubble Tea Market Outlook, By Type:, Value (US$ Mn), 2020-2033

- Latin America Bubble Tea Market Outlook, 2020 - 2033

- Latin America Bubble Tea Market Outlook, By Type:, Value (US$ Mn), 2020-2033

- Black Tea-based Bubble Tea

- Green Tea-based Bubble Tea

- Oolong Tea-based Bubble Tea

- White Tea-based Bubble Tea

- Latin America Bubble Tea Market Outlook, By Flavor:, Value (US$ Mn), 2020-2033

- Classic Milk Tea

- Taro

- Matcha

- Honeydew

- Mango

- Strawberry

- Chocolate

- Coffee

- Latin America Bubble Tea Market Outlook, By Distribution Channel:, Value (US$ Mn), 2020-2033

- Business to Business Sales of Bubble Tea

- Business to Consumer Sales of Bubble Tea

- Hypermarkets/Supermarkets

- Convenience Stores

- Online Retail

- Latin America Bubble Tea Market Outlook, by Country, Value (US$ Mn), 2020-2033

- Brazil Bubble Tea Market Outlook, By Type:, 2020-2033

- Brazil Bubble Tea Market Outlook, By Flavor:, 2020-2033

- Brazil Bubble Tea Market Outlook, By Distribution Channel:, 2020-2033

- Mexico Bubble Tea Market Outlook, By Type:, 2020-2033

- Mexico Bubble Tea Market Outlook, By Flavor:, 2020-2033

- Mexico Bubble Tea Market Outlook, By Distribution Channel:, 2020-2033

- Argentina Bubble Tea Market Outlook, By Type:, 2020-2033

- Argentina Bubble Tea Market Outlook, By Flavor:, 2020-2033

- Argentina Bubble Tea Market Outlook, By Distribution Channel:, 2020-2033

- Rest of LATAM Bubble Tea Market Outlook, By Type:, 2020-2033

- Rest of LATAM Bubble Tea Market Outlook, By Flavor:, 2020-2033

- Rest of LATAM Bubble Tea Market Outlook, By Distribution Channel:, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Latin America Bubble Tea Market Outlook, By Type:, Value (US$ Mn), 2020-2033

- Middle East & Africa Bubble Tea Market Outlook, 2020 - 2033

- Middle East & Africa Bubble Tea Market Outlook, By Type:, Value (US$ Mn), 2020-2033

- Black Tea-based Bubble Tea

- Green Tea-based Bubble Tea

- Oolong Tea-based Bubble Tea

- White Tea-based Bubble Tea

- Middle East & Africa Bubble Tea Market Outlook, By Flavor:, Value (US$ Mn), 2020-2033

- Classic Milk Tea

- Taro

- Matcha

- Honeydew

- Mango

- Strawberry

- Chocolate

- Coffee

- Middle East & Africa Bubble Tea Market Outlook, By Distribution Channel:, Value (US$ Mn), 2020-2033

- Business to Business Sales of Bubble Tea

- Business to Consumer Sales of Bubble Tea

- Hypermarkets/Supermarkets

- Convenience Stores

- Online Retail

- Middle East & Africa Bubble Tea Market Outlook, by Country, Value (US$ Mn), 2020-2033

- GCC Bubble Tea Market Outlook, By Type:, 2020-2033

- GCC Bubble Tea Market Outlook, By Flavor:, 2020-2033

- GCC Bubble Tea Market Outlook, By Distribution Channel:, 2020-2033

- South Africa Bubble Tea Market Outlook, By Type:, 2020-2033

- South Africa Bubble Tea Market Outlook, By Flavor:, 2020-2033

- South Africa Bubble Tea Market Outlook, By Distribution Channel:, 2020-2033

- Egypt Bubble Tea Market Outlook, By Type:, 2020-2033

- Egypt Bubble Tea Market Outlook, By Flavor:, 2020-2033

- Egypt Bubble Tea Market Outlook, By Distribution Channel:, 2020-2033

- Nigeria Bubble Tea Market Outlook, By Type:, 2020-2033

- Nigeria Bubble Tea Market Outlook, By Flavor:, 2020-2033

- Nigeria Bubble Tea Market Outlook, By Distribution Channel:, 2020-2033

- Rest of Middle East Bubble Tea Market Outlook, By Type:, 2020-2033

- Rest of Middle East Bubble Tea Market Outlook, By Flavor:, 2020-2033

- Rest of Middle East Bubble Tea Market Outlook, By Distribution Channel:, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Middle East & Africa Bubble Tea Market Outlook, By Type:, Value (US$ Mn), 2020-2033

- Competitive Landscape

- Company Vs Segment Heatmap

- Company Market Share Analysis, 2025

- Competitive Dashboard

- Company Profiles

- Gong Cha

- Company Overview

- Product Portfolio

- Financial Overview

- Business Strategies and Developments

- Kung Fu Tea

- Tiger Sugar

- Sharetea

- Boba Guys

- Tapioca Express

- Chatime

- Tea Ren’s Tea Time

- CoCo Fresh Tea & Juice

- Quickly

- Happy Lemon

- DaBoba

- Cojiitii

- TACHUNGHO

- Others

- Gong Cha

- Appendix

- Research Methodology

- Report Assumptions

- Acronyms and Abbreviations

|

BASE YEAR |

HISTORICAL DATA |

FORECAST PERIOD |

UNITS |

|||

|

2025 |

|

2020 - 2025 |

2026 - 2033 |

Value: US$ Million |

||

| REPORT FEATURES |

DETAILS |

| By Type |

|

| By Flavor |

|

| By Distribution Channel |

|

| Geographical Coverage |

|

| Leading Companies |

|

| Report Highlights |

Key Market Indicators, Macro-micro economic impact analysis, Technological Roadmap, Key Trends, Driver, Restraints, and Future Opportunities & Revenue Pockets, Porter’s 5 Forces Analysis, Historical Trend (2019-2024), Market Estimates and Forecast, Market Dynamics, Industry Trends, Competition Landscape, Category, Region, Country-wise Trends & Analysis, COVID-19 Impact Analysis (Demand and Supply Chain) |