Global Glass Bottle and Container Market: Strategic Analysis 2026-2033

Executive Summary & Key Highlights of Glass Bottle and Container Market

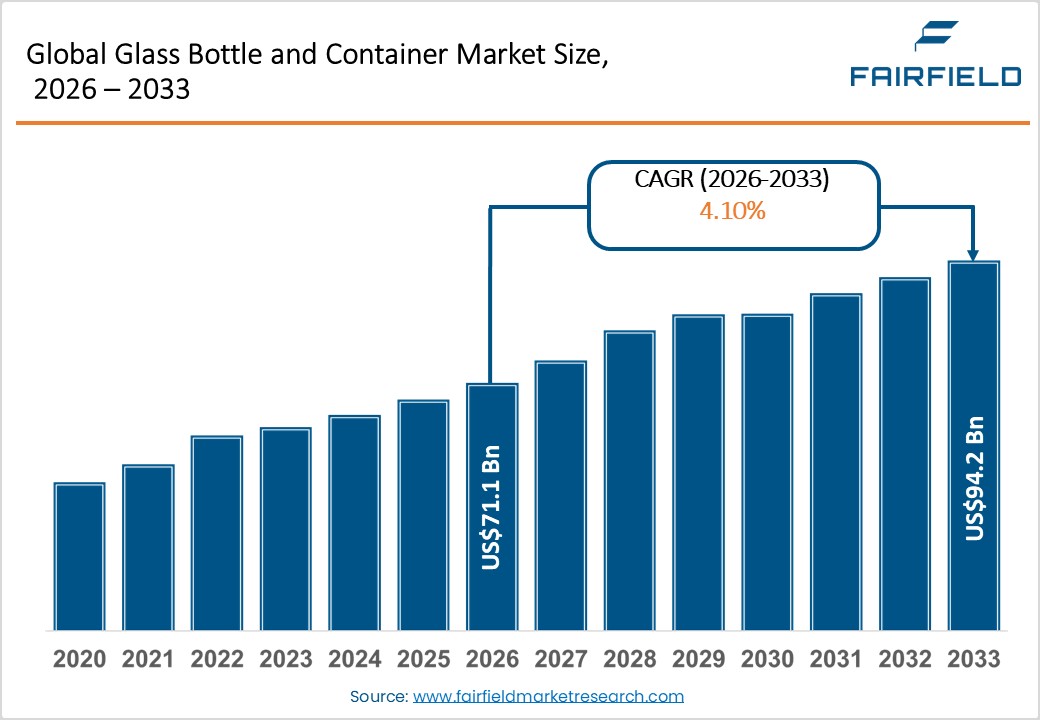

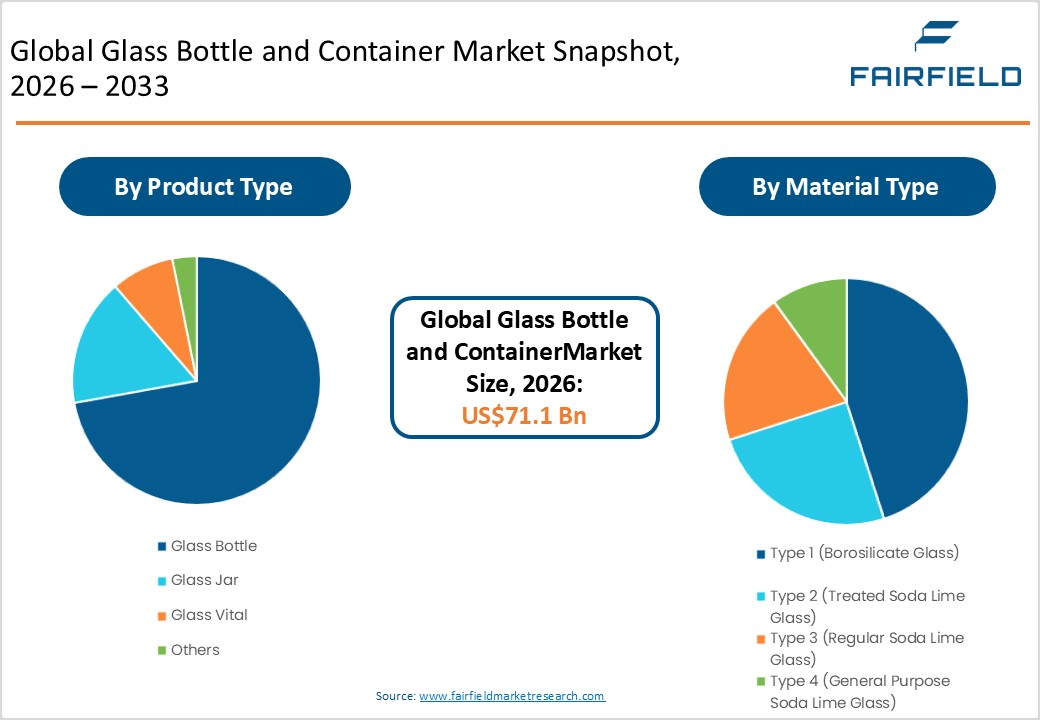

- The global glass bottle and container market reach approximately US$71.1 billion in 2026 and is projected to expand to US$94.2 billion by 2033, representing a compound annual growth rate (CAGR) of 4.1%, Over the forecast period.

- Leading Product – Glass Bottle: Glass Bottle dominates with ~70% share (≈US$49.8B in 2026), driven by strong demand from beverage packaging such as alcohol and soft drinks.

- Glass Jar is the fastest-growing segment, supported by rising food packaging and food storage demand, with ~12% shift toward packaged premium foods.

- Borosilicate Glass (Type 1) leads with ~45% share, widely used in pharmaceuticals and nutraceutical packaging due to high thermal and chemical resistance.

- Treated Soda Lime Glass, (Type 2) is growing fastest due to lower cost and expanding use in cosmetics and consumer health packaging.

- Beverage Packaging holds ~45% market share, driven by premium alcohol brands and strong demand for reusable glass containers.

- Food Packaging is the fastest-growing segment due to rising urbanization and demand for safe packaged foods.

- Sustainability Regulations: Recycling mandates and circular economy policies targeting ~50% recycled content by 2030 are accelerating demand for glass bottles and containers.

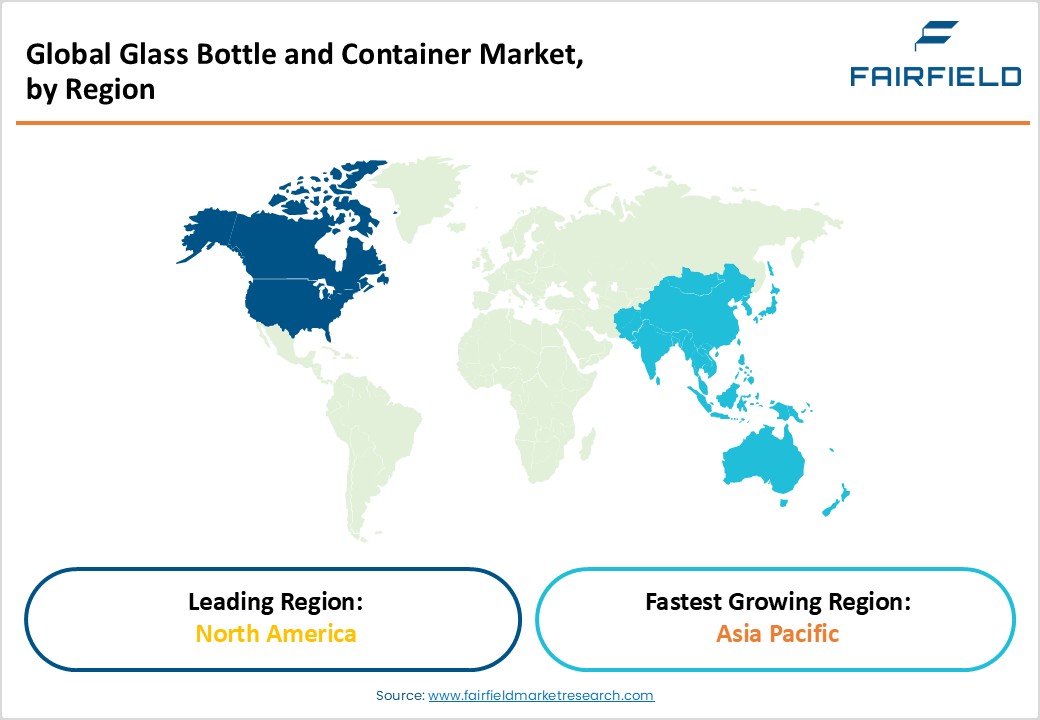

- Asia-Pacific leads with ~36% share, dominated by China (55–60% regional share) and India, supported by urbanization and expanding packaging demand.

Market Dynamics: Drivers, Restraints, and Opportunities Analysis

Market Drivers

- Sustainability Regulations and Consumer Preferences:

Sustainability regulations and shifting consumer preferences are key drivers of the glass bottle and container market, which is projected to grow at about 4.4–5.7% through the early‑to‑mid 2030s. Stricter extended producer responsibility, recycling targets, and circular‑economy frameworks, especially in Europe and North America, are accelerating brand transitions from single‑use plastics to infinitely recyclable glass in beverage, food, and cosmetics packaging. These policies may add incremental percentage points to medium‑term packaging growth versus a no‑policy scenario. Companies adopting recyclable glass formats, lightweight designs, and optimized logistics can strengthen compliance and competitiveness, while slower adopters face higher compliance costs and potential market‑access restrictions.

- Health, Safety, and Premiumization in Food, Beverage, and Pharma

Health, safety, and premiumization are key drivers of the glass bottle and container market. Glass is favored in food, beverage, and pharmaceutical applications due to its chemically inert and impermeable properties, reducing migration and additive concerns linked to some plastics. Food and beverage applications account for around 40% or more of total glass container demand, driven by premium beverages, specialty foods, nutraceuticals, and high‑value pharmaceuticals. The health-safety and premiumization driver operates through risk mitigation for sensitive formulations and value creation via premium appearance and reusability. In APAC and emerging markets, rising middle‑class incomes boost premium beverage demand, while in mature markets, premiumization and craft segments sustain value growth despite stable volumes.

Market Restraints

- Energy and Carbon Cost Exposure

Energy and carbon cost exposure is a key restraint on the glass bottle and container market. Glass manufacturing is highly energy‑intensive, exposing producers to fuel price volatility and carbon taxes or emissions trading schemes, especially in Europe and North America. Shortfalls in recycling quotas increase reliance on virgin raw materials, raising energy intensity per ton and associated carbon liabilities. These factors can limit capacity expansion or trigger plant rationalizations, potentially reducing market growth by a modest but material margin versus underlying demand. To mitigate these pressures, manufacturers are increasing cullet usage, adopting fuel switching and electrification pilots, and joining carbon‑reduction or offset programs, often supported by regional policy incentives aimed at lowering emissions.

- Competition from Alternative Packaging Substrates:

Competition from alternative packaging substrates is a key restraint on the glass bottle and container market. Aluminum cans, PET bottles, paper‑based cartons, and flexible packaging challenge glass on cost, weight, convenience, and transport emissions in several regions. Due to these trade‑offs, multiple market studies project only mid‑single‑digit growth for the glass bottle and container market, as substitution between materials remains limited by performance and pricing differences. This competition can restrict glass’s market share expansion in beverages and certain food categories, even though overall revenues continue to rise through value‑added and premium products. To remain competitive, manufacturers focus on design differentiation, premium positioning, closed‑loop reuse systems, and niche applications where glass performance advantages are critical.

Market Opportunities

- Rising Demand in Emerging Market Consumer Segments:

Growth in emerging‑market consumer segments is a major opportunity for the glass bottle and container market. Rising incomes, rapid urbanization, and increasing demand for packaged food, beverages, and pharmaceuticals are driving strong demand in higher‑growth economies. India’s glass containers market is projected to grow from about US$2.08 billion in 2024 to around US$2.82 billion by 2033, reflecting steady expansion in urban food retail, alcoholic and non‑alcoholic beverages, and pharmaceutical packaging. In China, the glass bottle and container market benefits from large‑scale beverage production, rising health‑conscious consumption, and stricter environmental policies that favor recyclable glass. In several other emerging markets, packaged‑food penetration and e‑commerce‑driven logistics are creating demand for standardized, recyclable glass formats, particularly in sauces, dairy, and personal‑care products. Opportunities include local capacity expansion, joint ventures with regional brand owners, and tailored product strategies that align with urban‑consumer preferences and sustainability expectations.

- Sustainability‑Linked Product and Business Model Innovation:

Sustainability‑linked product and business model innovation is a significant opportunity for the glass bottle and container market. Growing net‑zero and circular‑economy commitments are increasing demand for higher recycled‑content glass, refillable and returnable systems, and lightweight packaging formats with verified environmental performance. Industry reports indicate that using high cullet ratios and advanced melting technologies strengthens supplier positioning in tenders and long‑term supply contracts. This creates opportunities through sustainability‑linked differentiation, including life‑cycle‑assessed packaging, closed‑loop reuse partnerships with retailers and hospitality sectors, and digital traceability systems for container reuse. Although the exact scale of the opportunity is not consistently quantified, it is considered material due to packaging’s share in consumer goods emissions, encouraging investments in collection networks, sorting, cullet processing, and data infrastructure.

Segmentation Analysis: Category-Wise Strategic Assessment

By Product

Glass bottles account for about 70% of global glass bottle and container revenues in 2026, implying a segment worth over US$40 billion with independent estimates placing the bottle segment at US$48 billion within the overall US$71.1 billion 2026 market. This dominance is driven by extensive use in alcoholic and non‑alcoholic beverages, functional drinks, and liquid pharmaceuticals, supported by glass’s inertness and barrier properties. Glass jars hold a smaller share but are the fastest‑growing segment, fueled by premium food, spreads, condiments, and ready‑to‑eat products. Vials and specialized containers serve pharmaceutical and laboratory applications but contribute relatively lower revenue.

By Material

Borosilicate glass holds about 45% market share in 2026 within the glass bottle and container scope, driven by high‑value applications in pharmaceuticals, parenteral drugs, laboratory ware, and temperature‑resistant uses under strict regulatory and technical standards. Although regular soda lime glass dominates overall packaging volume, borosilicate captures a higher value share due to its specialized uses. The treated soda lime glass segment is the fastest‑growing material category, offering a balance of performance and cost for pharmaceutical and cosmetic packaging. Meanwhile, regular and general‑purpose soda lime glass remain widely used in high‑volume beverage and food packaging due to their cost efficiency and established manufacturing base.

By End Use:

Beverage packaging accounts for about 45% of the glass bottle and container market in 2026, in line with industry estimates showing food and beverage together representing around 40% or more of total demand, with beverages holding the larger share. This segment includes alcoholic drinks, non‑alcoholic beverages, and premium bottled water, where glass supports taste preservation, product differentiation, and reuse systems. Growth is driven by premiumization, craft beverage trends, and expanding consumption in emerging markets, though partially limited by competition from cans and PET. Food packaging is the fastest‑growing end‑use segment, supported by rising demand for baby food, sauces, and health‑focused products in reusable glass containers.

Regional Market Assessment: Strategic Geography Analysis

North America Glass Bottle and Container Market

The North America glass bottle and container market, led by the United States, accounts for approximately one‑quarter of global market value in the mid‑2020s. The U.S. glass container and bottles segment exceeds US$15.99 billion in 2026, reflecting strong demand from beverages, packaged foods, and pharmaceuticals. Market maturity is supported by high per‑capita consumption and an established recycling infrastructure. Growth is driven by premium beverages, craft beer and spirits, specialty foods, and pharmaceutical packaging. Regulatory frameworks, including container deposit laws and environmental regulations, shape recycling systems. Investments focus on capacity upgrades, furnace rebuilds with higher cullet ratios, sustainability improvements, and selective expansion near key customers.

Europe Glass Bottle and Container Market

The European glass bottle and container market shows varied dynamics, with Western Europe Germany, the UK, and France accounting for over 60% of regional value. Germany’s container glass TAM was about €4.2 billion (~US$4.6 billion) in 2023, while the UK market is estimated at US$3–4 billion equivalents. France produced around 5.48 million tonnes of container glass in 2025. Regionally, the market is projected to surpass US$28.26 billion by 2033, with forecasts reaching US$35 billion by 2031 and volume growth from 32.54 million tonnes in 2026 to 37.58 million tonnes by 2031, supported by strong recycling policies and sustainability regulations.

Asia-Pacific Glass Bottle and Container Market

The Asia‑Pacific glass bottle and container market is expected to account for about 36% of global value, reaching over US$33.91 billion by 2033. Regional volumes are projected to grow from 26.56 million tonnes in 2025 to 33.72 million tonnes by 2030, while market value expands at a moderate pace. China dominates with 55–60% of APAC demand, its glass container packaging market valued at US$13.56 billion in 2025, with glass holding 60.5% of packaging share in 2024 and 1.9 million tonnes of exports in 2023. India and ASEAN show strong growth, driven by urbanization, packaged beverages, pharmaceuticals, and rising cosmetics demand.

Competitive Landscape: Market Structure and Strategic Positioning

The global glass bottle and container market shows moderate consolidation, with a small group of multinational producers controlling about 40–50% of total capacity based on 2023–2025 production and revenue analyses. Competition is driven by scale advantages in beverage and food packaging, along with material specialization for pharmaceuticals and customized designs for cosmetics and premium beverages. Entry barriers are high due to furnace construction costs often exceeding US$100 million per facility, strict emissions and recycling regulations, and the need for efficient cullet sourcing and logistics networks. Ongoing M&A activity focuses on geographic expansion, lightweighting technology adoption, and portfolio optimization, reflecting gradual market maturation and a shift toward sustainability‑ and efficiency‑driven positioning.

Key Players

- O-I Glass, Inc.

Ardagh Group S.A. - Verallia S.A.

- Vidrala S.A.

Gerresheimer AG - Piramal Glass Private Limited

- Beatson Clark

Vetropack Holding Ltd. - Hindusthan National Glass & Industries Ltd.

- BA Glass B.V.

- Stölzle-Oberglas GmbH

Consol Glass (Pty) Ltd - Nampak Ltd.

- Bormioli Rocco S.p.A.

- AGI Greenpac Limited

Key Developments

- June 2025: O-I Glass secured USD 125 million from the U.S. Department of Energy for hybrid-furnace decarbonization technology.

- December 2024: Gerresheimer acquired Blitz LuxCo (Bormioli Pharma Group) for €800 million to expand its pharmaceutical "moulded glass" business.

- February 2026: Vidrala completed its entry into the South American market by acquiring Chilean manufacturer Cristalerías Toro.

Segmentation

By Product:

- Glass Bottle

- Glass Jar

- Glass Vial

- Other Glass Bottles & Containers

By Material:

- Type 1 (Borosilicate Glass)

- Type 2 (Treated Soda Lime Glass)

- Type 3 (Regular Soda Lime Glass)

- Type 4 (General Purpose Soda Lime Glass)

By End Use:

- Cosmetic and Perfumery

- Pharmaceuticals

- Food Packaging

- Beverage Packaging

- Food Storage

- Candles and Fragrance

- Others

By Region:

- North America

- Latin America

- Asia Pacific

- Europe

- Middle East & Africa

- Executive Summary

- Global Glass Bottle and Container Market Snapshot

- Future Projections

- Key Market Trends

- Regional Snapshot, by Value, 2026

- Analyst Recommendations

- Market Overview

- Market Definitions and Segmentations

- Market Dynamics

- Drivers

- Restraints

- Market Opportunities

- Value Chain Analysis

- COVID-19 Impact Analysis

- Porter's Five Forces Analysis

- Impact of Russia-Ukraine Conflict

- PESTLE Analysis

- Regulatory Analysis

- Price Trend Analysis

- Current Prices and Future Projections, 2025-2033

- Price Impact Factors

- Global Glass Bottle and Container Market Outlook, 2020 - 2033

- Global Glass Bottle and Container Market Outlook, by By Product, Value (US$ Bn), 2020-2033

- Glass Bottle

- Glass Jar

- Glass Vial

- Other Glass Bottles & Containers

- Global Glass Bottle and Container Market Outlook, by By Material, Value (US$ Bn), 2020-2033

- Type 1 (Borosilicate Glass)

- Type 2 (Treated Soda Lime Glass)

- Type 3 (Regular Soda Lime Glass)

- Type 4 (General Purpose Soda Lime Glass)

- Global Glass Bottle and Container Market Outlook, by By End Use, Value (US$ Bn), 2020-2033

- Cosmetic and Perfumery

- Pharmaceuticals

- Food Packaging

- Beverage Packaging

- Food Storage

- Candles and Fragrance

- Others

- Global Glass Bottle and Container Market Outlook, by Region, Value (US$ Bn), 2020-2033

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Global Glass Bottle and Container Market Outlook, by By Product, Value (US$ Bn), 2020-2033

- North America Glass Bottle and Container Market Outlook, 2020 - 2033

- North America Glass Bottle and Container Market Outlook, by By Product, Value (US$ Bn), 2020-2033

- Glass Bottle

- Glass Jar

- Glass Vial

- Other Glass Bottles & Containers

- North America Glass Bottle and Container Market Outlook, by By Material, Value (US$ Bn), 2020-2033

- Type 1 (Borosilicate Glass)

- Type 2 (Treated Soda Lime Glass)

- Type 3 (Regular Soda Lime Glass)

- Type 4 (General Purpose Soda Lime Glass)

- North America Glass Bottle and Container Market Outlook, by By End Use, Value (US$ Bn), 2020-2033

- Cosmetic and Perfumery

- Pharmaceuticals

- Food Packaging

- Beverage Packaging

- Food Storage

- Candles and Fragrance

- Others

- North America Glass Bottle and Container Market Outlook, by Country, Value (US$ Bn), 2020-2033

- S. Glass Bottle and Container Market Outlook, by By Product, 2020-2033

- S. Glass Bottle and Container Market Outlook, by By Material, 2020-2033

- S. Glass Bottle and Container Market Outlook, by By End Use, 2020-2033

- Canada Glass Bottle and Container Market Outlook, by By Product, 2020-2033

- Canada Glass Bottle and Container Market Outlook, by By Material, 2020-2033

- Canada Glass Bottle and Container Market Outlook, by By End Use, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- North America Glass Bottle and Container Market Outlook, by By Product, Value (US$ Bn), 2020-2033

- Europe Glass Bottle and Container Market Outlook, 2020 - 2033

- Europe Glass Bottle and Container Market Outlook, by By Product, Value (US$ Bn), 2020-2033

- Glass Bottle

- Glass Jar

- Glass Vial

- Other Glass Bottles & Containers

- Europe Glass Bottle and Container Market Outlook, by By Material, Value (US$ Bn), 2020-2033

- Type 1 (Borosilicate Glass)

- Type 2 (Treated Soda Lime Glass)

- Type 3 (Regular Soda Lime Glass)

- Type 4 (General Purpose Soda Lime Glass)

- Europe Glass Bottle and Container Market Outlook, by By End Use, Value (US$ Bn), 2020-2033

- Cosmetic and Perfumery

- Pharmaceuticals

- Food Packaging

- Beverage Packaging

- Food Storage

- Candles and Fragrance

- Others

- Europe Glass Bottle and Container Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Germany Glass Bottle and Container Market Outlook, by By Product, 2020-2033

- Germany Glass Bottle and Container Market Outlook, by By Material, 2020-2033

- Germany Glass Bottle and Container Market Outlook, by By End Use, 2020-2033

- Italy Glass Bottle and Container Market Outlook, by By Product, 2020-2033

- Italy Glass Bottle and Container Market Outlook, by By Material, 2020-2033

- Italy Glass Bottle and Container Market Outlook, by By End Use, 2020-2033

- France Glass Bottle and Container Market Outlook, by By Product, 2020-2033

- France Glass Bottle and Container Market Outlook, by By Material, 2020-2033

- France Glass Bottle and Container Market Outlook, by By End Use, 2020-2033

- K. Glass Bottle and Container Market Outlook, by By Product, 2020-2033

- K. Glass Bottle and Container Market Outlook, by By Material, 2020-2033

- K. Glass Bottle and Container Market Outlook, by By End Use, 2020-2033

- Spain Glass Bottle and Container Market Outlook, by By Product, 2020-2033

- Spain Glass Bottle and Container Market Outlook, by By Material, 2020-2033

- Spain Glass Bottle and Container Market Outlook, by By End Use, 2020-2033

- Russia Glass Bottle and Container Market Outlook, by By Product, 2020-2033

- Russia Glass Bottle and Container Market Outlook, by By Material, 2020-2033

- Russia Glass Bottle and Container Market Outlook, by By End Use, 2020-2033

- Rest of Europe Glass Bottle and Container Market Outlook, by By Product, 2020-2033

- Rest of Europe Glass Bottle and Container Market Outlook, by By Material, 2020-2033

- Rest of Europe Glass Bottle and Container Market Outlook, by By End Use, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Europe Glass Bottle and Container Market Outlook, by By Product, Value (US$ Bn), 2020-2033

- Asia Pacific Glass Bottle and Container Market Outlook, 2020 - 2033

- Asia Pacific Glass Bottle and Container Market Outlook, by By Product, Value (US$ Bn), 2020-2033

- Glass Bottle

- Glass Jar

- Glass Vial

- Other Glass Bottles & Containers

- Asia Pacific Glass Bottle and Container Market Outlook, by By Material, Value (US$ Bn), 2020-2033

- Type 1 (Borosilicate Glass)

- Type 2 (Treated Soda Lime Glass)

- Type 3 (Regular Soda Lime Glass)

- Type 4 (General Purpose Soda Lime Glass)

- Asia Pacific Glass Bottle and Container Market Outlook, by By End Use, Value (US$ Bn), 2020-2033

- Cosmetic and Perfumery

- Pharmaceuticals

- Food Packaging

- Beverage Packaging

- Food Storage

- Candles and Fragrance

- Others

- Asia Pacific Glass Bottle and Container Market Outlook, by Country, Value (US$ Bn), 2020-2033

- China Glass Bottle and Container Market Outlook, by By Product, 2020-2033

- China Glass Bottle and Container Market Outlook, by By Material, 2020-2033

- China Glass Bottle and Container Market Outlook, by By End Use, 2020-2033

- Japan Glass Bottle and Container Market Outlook, by By Product, 2020-2033

- Japan Glass Bottle and Container Market Outlook, by By Material, 2020-2033

- Japan Glass Bottle and Container Market Outlook, by By End Use, 2020-2033

- South Korea Glass Bottle and Container Market Outlook, by By Product, 2020-2033

- South Korea Glass Bottle and Container Market Outlook, by By Material, 2020-2033

- South Korea Glass Bottle and Container Market Outlook, by By End Use, 2020-2033

- India Glass Bottle and Container Market Outlook, by By Product, 2020-2033

- India Glass Bottle and Container Market Outlook, by By Material, 2020-2033

- India Glass Bottle and Container Market Outlook, by By End Use, 2020-2033

- Southeast Asia Glass Bottle and Container Market Outlook, by By Product, 2020-2033

- Southeast Asia Glass Bottle and Container Market Outlook, by By Material, 2020-2033

- Southeast Asia Glass Bottle and Container Market Outlook, by By End Use, 2020-2033

- Rest of SAO Glass Bottle and Container Market Outlook, by By Product, 2020-2033

- Rest of SAO Glass Bottle and Container Market Outlook, by By Material, 2020-2033

- Rest of SAO Glass Bottle and Container Market Outlook, by By End Use, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Asia Pacific Glass Bottle and Container Market Outlook, by By Product, Value (US$ Bn), 2020-2033

- Latin America Glass Bottle and Container Market Outlook, 2020 - 2033

- Latin America Glass Bottle and Container Market Outlook, by By Product, Value (US$ Bn), 2020-2033

- Glass Bottle

- Glass Jar

- Glass Vial

- Other Glass Bottles & Containers

- Latin America Glass Bottle and Container Market Outlook, by By Material, Value (US$ Bn), 2020-2033

- Type 1 (Borosilicate Glass)

- Type 2 (Treated Soda Lime Glass)

- Type 3 (Regular Soda Lime Glass)

- Type 4 (General Purpose Soda Lime Glass)

- Latin America Glass Bottle and Container Market Outlook, by By End Use, Value (US$ Bn), 2020-2033

- Cosmetic and Perfumery

- Pharmaceuticals

- Food Packaging

- Beverage Packaging

- Food Storage

- Candles and Fragrance

- Others

- Latin America Glass Bottle and Container Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Brazil Glass Bottle and Container Market Outlook, by By Product, 2020-2033

- Brazil Glass Bottle and Container Market Outlook, by By Material, 2020-2033

- Brazil Glass Bottle and Container Market Outlook, by By End Use, 2020-2033

- Mexico Glass Bottle and Container Market Outlook, by By Product, 2020-2033

- Mexico Glass Bottle and Container Market Outlook, by By Material, 2020-2033

- Mexico Glass Bottle and Container Market Outlook, by By End Use, 2020-2033

- Argentina Glass Bottle and Container Market Outlook, by By Product, 2020-2033

- Argentina Glass Bottle and Container Market Outlook, by By Material, 2020-2033

- Argentina Glass Bottle and Container Market Outlook, by By End Use, 2020-2033

- Rest of LATAM Glass Bottle and Container Market Outlook, by By Product, 2020-2033

- Rest of LATAM Glass Bottle and Container Market Outlook, by By Material, 2020-2033

- Rest of LATAM Glass Bottle and Container Market Outlook, by By End Use, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Latin America Glass Bottle and Container Market Outlook, by By Product, Value (US$ Bn), 2020-2033

- Middle East & Africa Glass Bottle and Container Market Outlook, 2020 - 2033

- Middle East & Africa Glass Bottle and Container Market Outlook, by By Product, Value (US$ Bn), 2020-2033

- Glass Bottle

- Glass Jar

- Glass Vial

- Other Glass Bottles & Containers

- Middle East & Africa Glass Bottle and Container Market Outlook, by By Material, Value (US$ Bn), 2020-2033

- Type 1 (Borosilicate Glass)

- Type 2 (Treated Soda Lime Glass)

- Type 3 (Regular Soda Lime Glass)

- Type 4 (General Purpose Soda Lime Glass)

- Middle East & Africa Glass Bottle and Container Market Outlook, by By End Use, Value (US$ Bn), 2020-2033

- Cosmetic and Perfumery

- Pharmaceuticals

- Food Packaging

- Beverage Packaging

- Food Storage

- Candles and Fragrance

- Others

- Middle East & Africa Glass Bottle and Container Market Outlook, by Country, Value (US$ Bn), 2020-2033

- GCC Glass Bottle and Container Market Outlook, by By Product, 2020-2033

- GCC Glass Bottle and Container Market Outlook, by By Material, 2020-2033

- GCC Glass Bottle and Container Market Outlook, by By End Use, 2020-2033

- South Africa Glass Bottle and Container Market Outlook, by By Product, 2020-2033

- South Africa Glass Bottle and Container Market Outlook, by By Material, 2020-2033

- South Africa Glass Bottle and Container Market Outlook, by By End Use, 2020-2033

- Egypt Glass Bottle and Container Market Outlook, by By Product, 2020-2033

- Egypt Glass Bottle and Container Market Outlook, by By Material, 2020-2033

- Egypt Glass Bottle and Container Market Outlook, by By End Use, 2020-2033

- Nigeria Glass Bottle and Container Market Outlook, by By Product, 2020-2033

- Nigeria Glass Bottle and Container Market Outlook, by By Material, 2020-2033

- Nigeria Glass Bottle and Container Market Outlook, by By End Use, 2020-2033

- Rest of Middle East Glass Bottle and Container Market Outlook, by By Product, 2020-2033

- Rest of Middle East Glass Bottle and Container Market Outlook, by By Material, 2020-2033

- Rest of Middle East Glass Bottle and Container Market Outlook, by By End Use, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Middle East & Africa Glass Bottle and Container Market Outlook, by By Product, Value (US$ Bn), 2020-2033

- Competitive Landscape

- Company Vs Segment Heatmap

- Company Market Share Analysis, 2025

- Competitive Dashboard

- Company Profiles

- O-I Glass, Inc.

- Company Overview

- Product Portfolio

- Financial Overview

- Business Strategies and Developments

- Ardagh Group S.A.

- Verallia S.A.

- Vidrala S.A.

- Gerresheimer AG

- Piramal Glass Private Limited

- Beatson Clark

- Vetropack Holding Ltd.

- Hindusthan National Glass & Industries Ltd.

- BA Glass B.V.

- Stölzle-Oberglas GmbH

- Consol Glass (Pty) Ltd

- Nampak Ltd.

- Bormioli Rocco S.p.A.

- AGI Greenpac Limited

- O-I Glass, Inc.

- Appendix

- Research Methodology

- Report Assumptions

- Acronyms and Abbreviations

|

BASE YEAR |

HISTORICAL DATA |

FORECAST PERIOD |

UNITS |

|||

|

2025 |

|

2020 - 2025 |

2026 - 2033 |

Value: US$ Million |

||

|

REPORT FEATURES |

DETAILS |

|

By Product |

|

|

By Material |

|

|

By End Use |

|

|

Geographical Coverage |

|

|

Leading Companies |

|

|

Report Highlights |

Key Market Indicators, Macro-micro economic impact analysis, Technological Roadmap, Key Trends, Driver, Restraints, and Future Opportunities & Revenue Pockets, Porter’s 5 Forces Analysis, Historical Trend (2019-2024), Market Estimates and Forecast, Market Dynamics, Industry Trends, Competition Landscape, Category, Region, Country-wise Trends & Analysis, COVID-19 Impact Analysis (Demand and Supply Chain) |