Hydrocolloids Market

Global Hydrocolloids Industry Analysis, Size, Share, Growth, Trends, and Forecast 2026-2033 - (By Product Type,By Material Type, By Geographic Coverage and By Company)

Hydrocolloids Market Size, Share, and Growth Forecast 2026 – 2033

Hydrocolloids Market Size and Trend Analysis

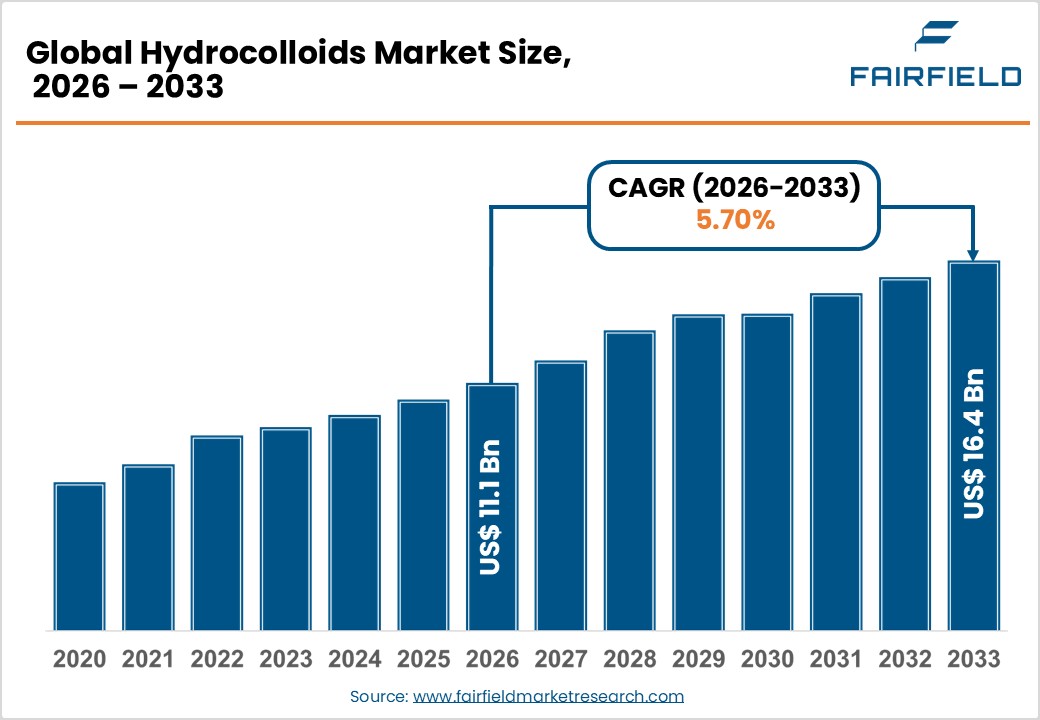

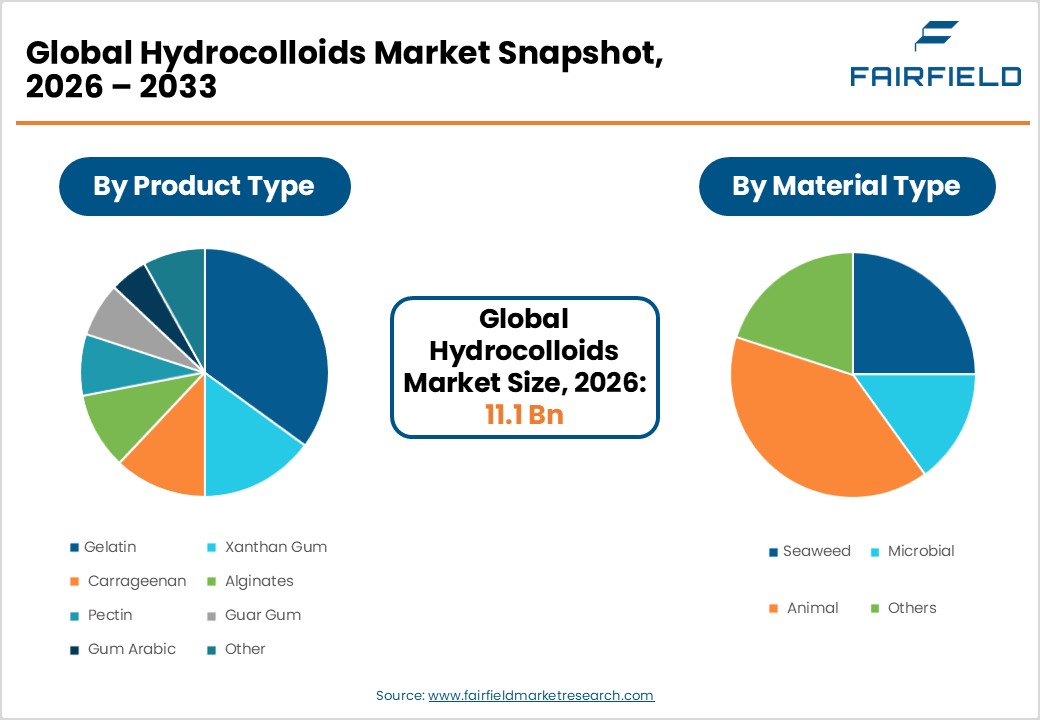

- The global hydrocolloids market size is likely to be valued at US$ 11.1 Billion in 2026 and is expected to reach US$ 16.4 Billion by 2033, growing at a CAGR of 5.70% during the forecast period from 2026 to 2033.

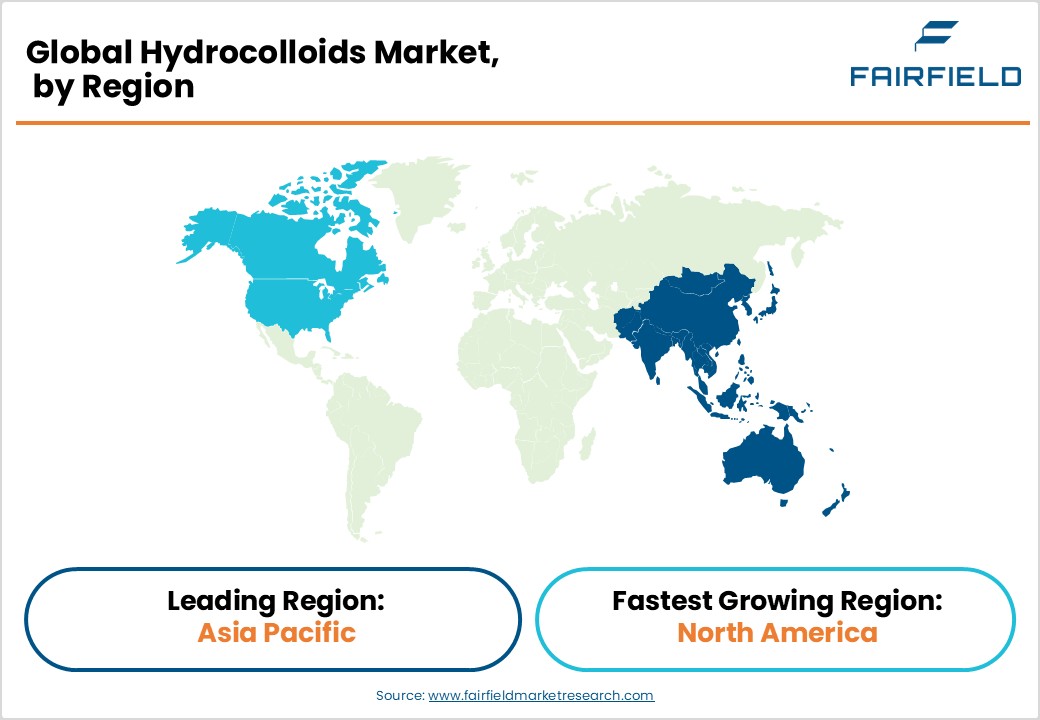

- Leading Region Market: Asia Pacific leads the global hydrocolloids market, commanding approximately 45% of total market share, supported by dominant seaweed production, cost-efficient manufacturing, and strong food & beverage demand across China, India, and ASEAN nations.

- Fastest growing Region Market: North America is the fastest-growing region, propelled by the U.S. clean-label food movement, robust pharmaceutical demand, and a dynamic innovation ecosystem driven by companies including Cargill and Kerry Group plc.

- Leading End-use: The Food & Beverage segment dominates end-use applications, accounting for approximately 57% of total market revenue, driven by widespread adoption of hydrocolloids as texturizers, stabilizers, and emulsifiers in global processed food and beverage formulations.

- Leading Product type: Gelatin is the leading product type with approximately 28% market share, fueled by extensive use in pharmaceutical capsule manufacturing, confectionery, dairy desserts, and fast-growing nutraceutical applications across major global markets.

- The plant-based food sector represents the most significant near-term market opportunity, with rapidly growing demand for Xanthan Gum, Carrageenan, and Pectin in meat alternatives and dairy-free products expected to generate substantial new revenue for hydrocolloid producers.

Market Dynamics

Market Growth Drivers

Rising Demand for Clean-Label and Plant-Based Food Ingredients

The global surge in clean-label food consumption is a primary growth driver for the hydrocolloids market. According to the Food and Agriculture Organization (FAO), the global food industry is witnessing a fundamental shift toward natural and minimally processed ingredients, with over 60% of consumers worldwide actively seeking products with recognizable, natural components. Hydrocolloids such as Pectin, Guar Gum, and Gum Arabic serve as natural alternatives to synthetic additives, meeting growing consumer demand for transparency and food safety. The increasing prevalence of vegan and vegetarian diets with plant-based food retail sales growing significantly across the U.S. and Europe further propels the demand for plant-derived hydrocolloids in beverages, confectionery, and functional food formulations, creating sustained long-term demand momentum.

Expanding Applications in Pharmaceutical Drug Delivery Systems

The pharmaceutical industry represents one of the fastest-growing end-use verticals for hydrocolloids, driving significant market momentum. Hydrocolloids such as Gelatin, Carrageenan, and modified Alginates are extensively utilized as binders, film coatings, sustained-release matrices, and capsule shells in drug delivery systems. According to the World Health Organization (WHO), the global pharmaceutical market surpassed US$ 1.4 trillion in 2023, and increasing formulation complexity necessitates advanced excipients with multifunctional properties. Gelatin alone accounts for a substantial share of global pharmaceutical capsule production. The growing demand for nutraceuticals and dietary supplements, driven by rising health consciousness and aging populations across North America, Europe, and Asia Pacific, further amplifies hydrocolloid consumption in the pharmaceutical sector.

Market Restraints

High Raw Material Price Volatility

A significant restraint challenging the hydrocolloids market is the inherent price volatility of key raw materials. Seaweed-based hydrocolloids including Carrageenan and Alginates are subject to fluctuations in oceanic harvests influenced by climate change, El Niño patterns, and rising sea temperatures. According to the International Seaweed Association, global seaweed production has faced periodic supply disruptions, resulting in price swings that constrain manufacturers’ profit margins. Similarly, Gelatin derived from animal by-products faces supply-side pressures from livestock market dynamics, disease outbreaks, and increasing regulatory scrutiny, creating challenges for consistent cost management and stable pricing across the value chain.

Regulatory Complexity Across Global Markets

The hydrocolloids market faces considerable regulatory barriers, as differing food additive and pharmaceutical excipient standards across jurisdictions create significant compliance complexity. In the European Union, hydrocolloids must comply with the European Food Safety Authority (EFSA) approved additives list under Regulation EC No. 1333/2008, while the U.S. FDA mandates GRAS (Generally Recognized As Safe) classification for food-grade applications. Divergent labeling requirements, maximum usage limits, and ongoing safety reviews for ingredients such as Carrageenan which has faced scrutiny in certain markets add regulatory uncertainty. These challenges increase time-to-market, raise compliance costs, and can restrict the adoption of novel hydrocolloid products in tightly regulated markets.

Market Opportunities

Growing Demand for Hydrocolloids in Plant-Based Meat and Dairy Alternatives

The explosive growth of the plant-based food sector presents a transformative commercial opportunity for hydrocolloid manufacturers. Plant-based meat, dairy alternatives, and egg substitutes rely heavily on hydrocolloids to replicate the texture, mouthfeel, and structural integrity of conventional animal-based products. The Good Food Institute reported that global retail sales of plant-based foods reached approximately US$ 8 billion in 2023, with continued robust growth projected in coming years. Methylcellulose, Xanthan Gum, Carrageenan, and modified starch-based hydrocolloids are critical enabling ingredients in this segment. Companies investing in tailor-made hydrocolloid blend development specifically designed for plant-based food applications stand to capture significant new revenue streams as consumer adoption accelerates across North America, Europe, and Asia Pacific.

Advancing Biomedical and Wound Care Applications

Beyond traditional food and pharmaceutical uses, hydrocolloids are increasingly gaining traction in advanced biomedical applications, including wound dressings, tissue engineering scaffolds, and controlled drug release platforms. Hydrocolloid wound dressings composed of Gelatin, Pectin, and Sodium Alginate are clinically proven to maintain a moist wound environment, accelerate healing, and reduce infection risk. The global wound care market is expanding significantly as aging populations and the rising prevalence of chronic conditions such as diabetes drive demand. Companies investing in medical-grade hydrocolloid R&D can diversify their revenue base and access premium-priced, high-growth niches within the broader healthcare and life sciences sector.

Segmental Insights

Product Type Analysis

Gelatin dominates the hydrocolloids market by product type, commanding approximately 28% of total market revenue in 2026. This market leadership is supported by its unparalleled functional versatility across food, pharmaceutical, and personal care applications. In the food segment, Gelatin is indispensable in confectionery, dairy desserts, and processed meat products due to its unique gelling, binding, and stabilizing properties. In pharmaceuticals, hard and soft Gelatin capsules account for the majority of global oral drug delivery systems. According to the Gelatin Manufacturers Institute of America (GMIA), global gelatin production has grown steadily, driven by rising nutraceutical consumption and pharmaceutical demand. Its clean-label positioning and GRAS regulatory approval further reinforce its leading market position across key geographies, particularly in North America and Europe.

Material Type Analysis

Seaweed-derived hydrocolloids represent the leading material type segment, accounting for approximately 40% share in 2026. This dominance is underpinned by the extensive commercial utility of Carrageenan, Agar, and Alginates all extracted from red and brown seaweeds across the food, pharmaceutical, and personal care industries. These ingredients are highly valued for their superior gelling, thickening, and film-forming capabilities. The International Seaweed Association estimates global annual seaweed production, with Asia-Pacific nations particularly China, Indonesia, and the Philippines serving as the dominant producers. Growing consumer preference for marine-sourced and plant-origin ingredients in food and personal care products further reinforces the dominance of seaweed-based hydrocolloids in the global market.

End-Use Analysis

The Food & Beverage segment is the dominant end-use category in the hydrocolloids market, accounting for approximately 57% market share in 2026. Hydrocolloids serve as essential functional ingredients across a broad spectrum of food products including dairy, bakery, confectionery, sauces, dressings, meat alternatives, and beverages where they perform critical roles as thickeners, stabilizers, emulsifiers, and texturizers. The global food processing industry’s relentless focus on improving product quality, extending shelf life, and enhancing consumer sensory experiences drives sustained demand. According to the Food and Agriculture Organization (FAO), the global population is projected to reach 9.7 billion by 2050, ensuring long-term and expanding demand for food-grade hydrocolloids across all major processing categories and geographies.

Regional Insights

North America Hydrocolloids Market Trends

North America is the fastest-growing region in the global hydrocolloids market, driven by robust demand from the U.S. food processing industry, a dynamic pharmaceutical sector, and a strong innovation ecosystem. The U.S. is the world’s largest consumer of functional food ingredients, with the FDA’s established GRAS framework providing a transparent regulatory pathway that accelerates the adoption of novel hydrocolloid ingredients. The region’s booming clean-label and plant-based food movement led by major companies such as Archer Daniels Midland and Cargill has significantly elevated demand for natural hydrocolloids in new product development.

Canada is also emerging as a meaningful contributor to regional market growth, supported by growing health and wellness trends and expanding pharmaceutical manufacturing activity. The region benefits from strong R&D infrastructure, with food science institutions and universities actively collaborating with industry players to develop next-generation hydrocolloid solutions for functional beverages, nutraceuticals, and biomedical applications. Investment in sustainable and plant-based hydrocolloid sourcing strategies is increasingly becoming a key competitive differentiator for North American ingredient manufacturers.

Europe Hydrocolloids Market Trends

Europe represents a mature yet strategically vital market for hydrocolloids, underpinned by stringent food safety standards, strong sustainability mandates, and a well-established food processing sector. The European Food Safety Authority (EFSA) plays a central role in defining permissible hydrocolloids and their usage levels under Regulation EC No. 1333/2008, creating a harmonized but demanding regulatory environment. Germany, France, and the United Kingdom are the primary contributors to regional demand, collectively accounting for a substantial share of European food and beverage production capacity.

Germany’s advanced food technology sector and France’s leadership in gourmet and artisan food processing drive significant Pectin, Carrageenan, and Guar Gum consumption. The U.K. market is independently aligning its food additive regulations post-Brexit, creating both challenges and new opportunities for hydrocolloid suppliers. Spain, with its growing dairy and meat processing industries, also contributes meaningfully to regional consumption. The European market is increasingly focused on bio-based and sustainably sourced hydrocolloids, closely aligned with the EU Green Deal environmental objectives and circular bioeconomy targets.

Asia Pacific Hydrocolloids Market Trends

Asia Pacific is the dominant region in the global hydrocolloids market, commanding approximately 45% of total market share. The region benefits from its unique dual role as both the world’s largest producer and consumer of hydrocolloids, particularly seaweed-based ingredients such as Agar, Carrageenan, and Alginates sourced from China, Indonesia, the Philippines, and Japan. China alone accounts for the majority of global seaweed cultivation, providing a cost-competitive raw material supply base that underpins the regional manufacturing advantage.

India and ASEAN nations are emerging as high-growth sub-markets, driven by rapid urbanization, an expanding middle class, and accelerating processed food consumption. India’s food processing sector is a major consumer of Guar Gum, produced domestically at scale and exported globally. Japan’s advanced pharmaceutical and cosmetics industries maintain robust demand for high-purity hydrocolloids. The combination of manufacturing cost advantages, proximity to raw material sources, and strong domestic demand positions Asia Pacific as the unrivaled growth engine of the global hydrocolloids market through 2033.

Competitive Landscape

The global hydrocolloids market exhibits a moderately consolidated structure, comprising a mix of large multinational corporations and specialized regional players. Leading companies such as CP Kelco (Cargill), DuPont Nutrition & Biosciences (IFF), Kerry Group plc, and BASF SE collectively hold a significant share of the market, leveraging extensive product portfolios, global supply chains, and deep customer relationships. Key competitive strategies include capacity expansions, strategic acquisitions, and sustained R&D investment in cleaner extraction technologies and customized hydrocolloid blends. Product innovation, regulatory compliance expertise, and vertical supply chain integration serve as primary differentiators, enabling market leaders to sustain competitive advantage amid growing pressure from cost-competitive Asian manufacturers.

Key Market Developments

March, 2024: Cargill, Inc. completed the acquisition of CP Kelco from J.M. Huber Corporation, significantly expanding its hydrocolloid ingredient portfolio across Pectin, Gellan Gum, and Xanthan Gum product lines globally.

January, 2025: Kerry Group plc announced a strategic investment in next-generation plant-based hydrocolloid blend development, targeting the rapidly expanding meat alternative and dairy-free food categories across North American and European markets.

November, 2023: BASF SE launched a new range of bio-based Xanthan Gum solutions under its care chemicals division, aimed at the personal care and cosmetics industry, emphasizing enhanced sustainability credentials and improved biodegradability profiles.

Companies Covered in Hydrocolloids Market

- CP Kelco (Cargill, Inc.)

- DuPont Nutrition & Biosciences (IFF)

- TIC Gums, Inc.

- Ingredion Incorporated

- Ashland Global Holdings Inc.

- Kerry Group plc

- GELITA AG

- BASF SE

- Lubrizol Corporation (Avient Corporation)

- FMC Corporation

- Solenis LLC

- Ashwin Ingredients Pvt. Ltd.

- Feng Yuan Chemical Co., Ltd.

- Merck KGaA

- Agrovista UK Ltd

- Tate & Lyle PLC

- Roquette Frères

- Rousselot (Darling Ingredients)

- Arthur Branwell & Co. Ltd.

- Nexira SAS

Market Segmentation

By Product Type

- Gelatin

- Xanthan Gum

- Carrageenan

- Alginates

- Pectin

- Guar Gum

- Gum Arabic

- Others

By Material Type

- Seaweed

- Microbial

- Animal

- Others

By End-Use

- Food & Beverage

- Pharmaceutical

- Personal Care & Cosmetics

- Others

Regions

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Executive Summary

1.1. Global Hydrocolloids Market Snapshot

1.2. Future Projections

1.3. Key Market Trends

1.4. Regional Snapshot, by Value, 2026

1.5. Analyst Recommendations

- Market Overview

2.1. Market Definitions and Segmentations

2.2. Market Dynamics

2.2.1. Drivers

2.2.2. Restraints

2.2.3. Market Opportunities

2.3. Value Chain Analysis

2.4. COVID-19 Impact Analysis

2.5. Porter's Five Forces Analysis

2.6. Impact of Russia-Ukraine Conflict

2.7. PESTLE Analysis

2.8. Regulatory Analysis

2.9. Price Trend Analysis

2.9.1. Current Prices and Future Projections, 2025-2033

2.9.2. Price Impact Factors

- Global Hydrocolloids Market Outlook, 2020 - 2033

3.1. Global Hydrocolloids Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

3.1.1. Gelatin

3.1.1.1.

3.1.2. Xanthan Gum

3.1.3. Carrageenan

3.1.4. Alginates

3.1.5. Pectin

3.1.6. Guar Gum

3.1.7. Gum Arabic

3.1.8. Other

3.2. Global Hydrocolloids Market Outlook, by Material Type, Value (US$ Bn), 2020-2033

3.2.1. Seaweed

3.2.2. Microbial

3.2.3. Animal

3.2.4. Others

3.3. Global Hydrocolloids Market Outlook, by End-User, Value (US$ Bn), 2020-2033

3.3.1. Food & Beverage

3.3.2. Pharmaceutical

3.3.3. Personal Care & Cosmetics

3.3.4. Others

3.4. Global Hydrocolloids Market Outlook, by Region, Value (US$ Bn), 2020-2033

3.4.1. North America

3.4.2. Europe

3.4.3. Asia Pacific

3.4.4. Latin America

3.4.5. Middle East & Africa

- North America Hydrocolloids Market Outlook, 2020 - 2033

4.1. North America Hydrocolloids Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

4.1.1. Gelatin

4.1.1.1.

4.1.2. Xanthan Gum

4.1.3. Carrageenan

4.1.4. Alginates

4.1.5. Pectin

4.1.6. Guar Gum

4.1.7. Gum Arabic

4.1.8. Other

4.2. North America Hydrocolloids Market Outlook, by Material Type, Value (US$ Bn), 2020-2033

4.2.1. Seaweed

4.2.2. Microbial

4.2.3. Animal

4.2.4. Others

4.3. North America Hydrocolloids Market Outlook, by End-User, Value (US$ Bn), 2020-2033

4.3.1. Food & Beverage

4.3.2. Pharmaceutical

4.3.3. Personal Care & Cosmetics

4.3.4. Others

4.4. North America Hydrocolloids Market Outlook, by Country, Value (US$ Bn), 2020-2033

4.4.1. U.S. Hydrocolloids Market Outlook, by Product Type, 2020-2033

4.4.2. U.S. Hydrocolloids Market Outlook, by Material Type, 2020-2033

4.4.3. U.S. Hydrocolloids Market Outlook, by End-User, 2020-2033

4.4.4. Canada Hydrocolloids Market Outlook, by Product Type, 2020-2033

4.4.5. Canada Hydrocolloids Market Outlook, by Material Type, 2020-2033

4.4.6. Canada Hydrocolloids Market Outlook, by End-User, 2020-2033

4.5. BPS Analysis/Market Attractiveness Analysis

- Europe Hydrocolloids Market Outlook, 2020 - 2033

5.1. Europe Hydrocolloids Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

5.1.1. Gelatin

5.1.1.1.

5.1.2. Xanthan Gum

5.1.3. Carrageenan

5.1.4. Alginates

5.1.5. Pectin

5.1.6. Guar Gum

5.1.7. Gum Arabic

5.1.8. Other

5.2. Europe Hydrocolloids Market Outlook, by Material Type, Value (US$ Bn), 2020-2033

5.2.1. Seaweed

5.2.2. Microbial

5.2.3. Animal

5.2.4. Others

5.3. Europe Hydrocolloids Market Outlook, by End-User, Value (US$ Bn), 2020-2033

5.3.1. Food & Beverage

5.3.2. Pharmaceutical

5.3.3. Personal Care & Cosmetics

5.3.4. Others

5.4. Europe Hydrocolloids Market Outlook, by Country, Value (US$ Bn), 2020-2033

5.4.1. Germany Hydrocolloids Market Outlook, by Product Type, 2020-2033

5.4.2. Germany Hydrocolloids Market Outlook, by Material Type, 2020-2033

5.4.3. Germany Hydrocolloids Market Outlook, by End-User, 2020-2033

5.4.4. Italy Hydrocolloids Market Outlook, by Product Type, 2020-2033

5.4.5. Italy Hydrocolloids Market Outlook, by Material Type, 2020-2033

5.4.6. Italy Hydrocolloids Market Outlook, by End-User, 2020-2033

5.4.7. France Hydrocolloids Market Outlook, by Product Type, 2020-2033

5.4.8. France Hydrocolloids Market Outlook, by Material Type, 2020-2033

5.4.9. France Hydrocolloids Market Outlook, by End-User, 2020-2033

5.4.10. U.K. Hydrocolloids Market Outlook, by Product Type, 2020-2033

5.4.11. U.K. Hydrocolloids Market Outlook, by Material Type, 2020-2033

5.4.12. U.K. Hydrocolloids Market Outlook, by End-User, 2020-2033

5.4.13. Spain Hydrocolloids Market Outlook, by Product Type, 2020-2033

5.4.14. Spain Hydrocolloids Market Outlook, by Material Type, 2020-2033

5.4.15. Spain Hydrocolloids Market Outlook, by End-User, 2020-2033

5.4.16. Russia Hydrocolloids Market Outlook, by Product Type, 2020-2033

5.4.17. Russia Hydrocolloids Market Outlook, by Material Type, 2020-2033

5.4.18. Russia Hydrocolloids Market Outlook, by End-User, 2020-2033

5.4.19. Rest of Europe Hydrocolloids Market Outlook, by Product Type, 2020-2033

5.4.20. Rest of Europe Hydrocolloids Market Outlook, by Material Type, 2020-2033

5.4.21. Rest of Europe Hydrocolloids Market Outlook, by End-User, 2020-2033

5.5. BPS Analysis/Market Attractiveness Analysis

- Asia Pacific Hydrocolloids Market Outlook, 2020 - 2033

6.1. Asia Pacific Hydrocolloids Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

6.1.1. Gelatin

6.1.1.1.

6.1.2. Xanthan Gum

6.1.3. Carrageenan

6.1.4. Alginates

6.1.5. Pectin

6.1.6. Guar Gum

6.1.7. Gum Arabic

6.1.8. Other

6.2. Asia Pacific Hydrocolloids Market Outlook, by Material Type, Value (US$ Bn), 2020-2033

6.2.1. Seaweed

6.2.2. Microbial

6.2.3. Animal

6.2.4. Others

6.3. Asia Pacific Hydrocolloids Market Outlook, by End-User, Value (US$ Bn), 2020-2033

6.3.1. Food & Beverage

6.3.2. Pharmaceutical

6.3.3. Personal Care & Cosmetics

6.3.4. Others

6.4. Asia Pacific Hydrocolloids Market Outlook, by Country, Value (US$ Bn), 2020-2033

6.4.1. China Hydrocolloids Market Outlook, by Product Type, 2020-2033

6.4.2. China Hydrocolloids Market Outlook, by Material Type, 2020-2033

6.4.3. China Hydrocolloids Market Outlook, by End-User, 2020-2033

6.4.4. Japan Hydrocolloids Market Outlook, by Product Type, 2020-2033

6.4.5. Japan Hydrocolloids Market Outlook, by Material Type, 2020-2033

6.4.6. Japan Hydrocolloids Market Outlook, by End-User, 2020-2033

6.4.7. South Korea Hydrocolloids Market Outlook, by Product Type, 2020-2033

6.4.8. South Korea Hydrocolloids Market Outlook, by Material Type, 2020-2033

6.4.9. South Korea Hydrocolloids Market Outlook, by End-User, 2020-2033

6.4.10. India Hydrocolloids Market Outlook, by Product Type, 2020-2033

6.4.11. India Hydrocolloids Market Outlook, by Material Type, 2020-2033

6.4.12. India Hydrocolloids Market Outlook, by End-User, 2020-2033

6.4.13. Southeast Asia Hydrocolloids Market Outlook, by Product Type, 2020-2033

6.4.14. Southeast Asia Hydrocolloids Market Outlook, by Material Type, 2020-2033

6.4.15. Southeast Asia Hydrocolloids Market Outlook, by End-User, 2020-2033

6.4.16. Rest of SAO Hydrocolloids Market Outlook, by Product Type, 2020-2033

6.4.17. Rest of SAO Hydrocolloids Market Outlook, by Material Type, 2020-2033

6.4.18. Rest of SAO Hydrocolloids Market Outlook, by End-User, 2020-2033

6.5. BPS Analysis/Market Attractiveness Analysis

- Latin America Hydrocolloids Market Outlook, 2020 - 2033

7.1. Latin America Hydrocolloids Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

7.1.1. Gelatin

7.1.1.1.

7.1.2. Xanthan Gum

7.1.3. Carrageenan

7.1.4. Alginates

7.1.5. Pectin

7.1.6. Guar Gum

7.1.7. Gum Arabic

7.1.8. Other

7.2. Latin America Hydrocolloids Market Outlook, by Material Type, Value (US$ Bn), 2020-2033

7.2.1. Seaweed

7.2.2. Microbial

7.2.3. Animal

7.2.4. Others

7.3. Latin America Hydrocolloids Market Outlook, by End-User, Value (US$ Bn), 2020-2033

7.3.1. Food & Beverage

7.3.2. Pharmaceutical

7.3.3. Personal Care & Cosmetics

7.3.4. Others

7.4. Latin America Hydrocolloids Market Outlook, by Country, Value (US$ Bn), 2020-2033

7.4.1. Brazil Hydrocolloids Market Outlook, by Product Type, 2020-2033

7.4.2. Brazil Hydrocolloids Market Outlook, by Material Type, 2020-2033

7.4.3. Brazil Hydrocolloids Market Outlook, by End-User, 2020-2033

7.4.4. Mexico Hydrocolloids Market Outlook, by Product Type, 2020-2033

7.4.5. Mexico Hydrocolloids Market Outlook, by Material Type, 2020-2033

7.4.6. Mexico Hydrocolloids Market Outlook, by End-User, 2020-2033

7.4.7. Argentina Hydrocolloids Market Outlook, by Product Type, 2020-2033

7.4.8. Argentina Hydrocolloids Market Outlook, by Material Type, 2020-2033

7.4.9. Argentina Hydrocolloids Market Outlook, by End-User, 2020-2033

7.4.10. Rest of LATAM Hydrocolloids Market Outlook, by Product Type, 2020-2033

7.4.11. Rest of LATAM Hydrocolloids Market Outlook, by Material Type, 2020-2033

7.4.12. Rest of LATAM Hydrocolloids Market Outlook, by End-User, 2020-2033

7.5. BPS Analysis/Market Attractiveness Analysis

- Middle East & Africa Hydrocolloids Market Outlook, 2020 - 2033

8.1. Middle East & Africa Hydrocolloids Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

8.1.1. Gelatin

8.1.1.1.

8.1.2. Xanthan Gum

8.1.3. Carrageenan

8.1.4. Alginates

8.1.5. Pectin

8.1.6. Guar Gum

8.1.7. Gum Arabic

8.1.8. Other

8.2. Middle East & Africa Hydrocolloids Market Outlook, by Material Type, Value (US$ Bn), 2020-2033

8.2.1. Seaweed

8.2.2. Microbial

8.2.3. Animal

8.2.4. Others

8.3. Middle East & Africa Hydrocolloids Market Outlook, by End-User, Value (US$ Bn), 2020-2033

8.3.1. Food & Beverage

8.3.2. Pharmaceutical

8.3.3. Personal Care & Cosmetics

8.3.4. Others

8.4. Middle East & Africa Hydrocolloids Market Outlook, by Country, Value (US$ Bn), 2020-2033

8.4.1. GCC Hydrocolloids Market Outlook, by Product Type, 2020-2033

8.4.2. GCC Hydrocolloids Market Outlook, by Material Type, 2020-2033

8.4.3. GCC Hydrocolloids Market Outlook, by End-User, 2020-2033

8.4.4. South Africa Hydrocolloids Market Outlook, by Product Type, 2020-2033

8.4.5. South Africa Hydrocolloids Market Outlook, by Material Type, 2020-2033

8.4.6. South Africa Hydrocolloids Market Outlook, by End-User, 2020-2033

8.4.7. Egypt Hydrocolloids Market Outlook, by Product Type, 2020-2033

8.4.8. Egypt Hydrocolloids Market Outlook, by Material Type, 2020-2033

8.4.9. Egypt Hydrocolloids Market Outlook, by End-User, 2020-2033

8.4.10. Nigeria Hydrocolloids Market Outlook, by Product Type, 2020-2033

8.4.11. Nigeria Hydrocolloids Market Outlook, by Material Type, 2020-2033

8.4.12. Nigeria Hydrocolloids Market Outlook, by End-User, 2020-2033

8.4.13. Rest of Middle East Hydrocolloids Market Outlook, by Product Type, 2020-2033

8.4.14. Rest of Middle East Hydrocolloids Market Outlook, by Material Type, 2020-2033

8.4.15. Rest of Middle East Hydrocolloids Market Outlook, by End-User, 2020-2033

8.5. BPS Analysis/Market Attractiveness Analysis

- Competitive Landscape

9.1. Company Vs Segment Heatmap

9.2. Company Market Share Analysis, 2025

9.3. Competitive Dashboard

9.4. Company Profiles

9.4.1. CP Kelco (Cargill, Inc.)

9.4.1.1. Company Overview

9.4.1.2. Product Portfolio

9.4.1.3. Financial Overview

9.4.1.4. Business Strategies and Developments

9.4.2. DuPont Nutrition & Biosciences (IFF)

9.4.3. TIC Gums, Inc.

9.4.4. Ingredion Incorporated

9.4.5. Ashland Global Holdings Inc.

9.4.6. Kerry Group plc

9.4.7. GELITA AG

9.4.8. BASF SE

9.4.9. Lubrizol Corporation (Avient Corporation)

9.4.10. FMC Corporation

9.4.11. Solenis LLC

9.4.12. Ashwin Ingredients Pvt. Ltd.

9.4.13. Feng Yuan Chemical Co., Ltd.

9.4.14. Merck KGaA

9.4.15. Agrovista UK Ltd.

- Appendix

10.1. Research Methodology

10.2. Report Assumptions

10.3. Acronyms and Abbreviations

|

BASE YEAR |

HISTORICAL DATA |

FORECAST PERIOD |

UNITS |

|||

|

2025 |

|

2020 - 2025 |

2026 - 2033 |

Value: US$ Million |

||

|

REPORT FEATURES |

DETAILS |

|

By Product Type Coverage |

|

|

By Material Type Coverage |

|

|

Geographical Coverage |

|

|

Leading Companies |

|

|

Report Highlights |

Key Market Indicators, Macro-micro economic impact analysis, Technological Roadmap, Key Trends, Driver, Restraints, and Future Opportunities & Revenue Pockets, Porter’s 5 Forces Analysis, Historical Trend (2019-2024), Market Estimates and Forecast, Market Dynamics, Industry Trends, Competition Landscape, Category, Region, Country-wise Trends & Analysis, COVID-19 Impact Analysis (Demand and Supply Chain) |

Our Research Methodology

Considering the volatility of business today, traditional approaches to strategizing a game plan can be unfruitful if not detrimental. True ambiguity is no way to determine a forecast. A myriad of predetermined factors must be accounted for such as the degree of risk involved, the magnitude of circumstances, as well as conditions or consequences that are not known or unpredictable. To circumvent binary views that cast uncertainty, the application of market research intelligence to strategically posture, move, and enable actionable outcomes is necessary.

View Methodology

Quality Assured

Rigorous Validation Process

Confidentiality Assured

End-to-end Data Security

Custom Research Services

Tailored To Your Objectives

FAQs

The hydrocolloids market size is US$ 11.1 Billion in 2026.

The hydrocolloids market is projected to grow at a CAGR of 5.70% by 2033.

The hydrocolloids market growth drivers include rising clean-label demand, expanding plant-based foods, and increasing pharmaceutical applications.

Asia Pacific is a dominating region for hydrocolloids market.

Cargill, Kerry Group plc, BASF SE, Ingredion Incorporated, and Ashland Global Holdings Inc. are some leading industry players in the hydrocolloids market.

Related Reports

Tortilla Market Insights, Competitive Landscape, and Market Forecast 2033

The tortilla market is projected to reach US$75.36 billion by 2033 growing at a 5.1% CAGR, driven by rising demand for convenient and ready-to-eat foods.

RTD Canned Cocktail Market Insights, Competitive Landscape, and Market Forecast 2033

RTD Canned Cocktail Market to reach US$11.15 Bn by 2033 at 14.2% CAGR, driven by premium RTDs, e-commerce growth, and consumer demand.

Avocado Oil Market Insights, Competitive Landscape, and Market Forecast 2033

The analgesics market is projected to grow from US$58.30 billion in 2026 to US$93.01 billion by 2033, registering a CAGR of 6.9% during the forecast period.

Soda Ash Market Insights, Competitive Landscape, and Market Forecast 2033

The soda ash market is projected to grow from US$15.90 billion in 2026 to US$24.87 billion by 2033, registering a CAGR of 6.6% over the forecast period.

Customized Premixes Market Insights, Competitive Landscape, and Market Forecast 2033

The customized premixes market is forecast to reach US$14.77 Bn by 2033 from US$8.90 Bn in 2026, growing at a CAGR of 7.5% over the forecast period.

Almond Ingredients Market Insights, Competitive Landscape, and Market Forecast 2033

The almond ingredients market is projected to grow from US$ 18.90 billion in 2026 to US$ 33.03 billion by 2033, at an 8.3% CAGR over the forecast period.