Industrial Hose Market Size, Share, and Growth Forecast 2026 – 2033

Key Market Highlights

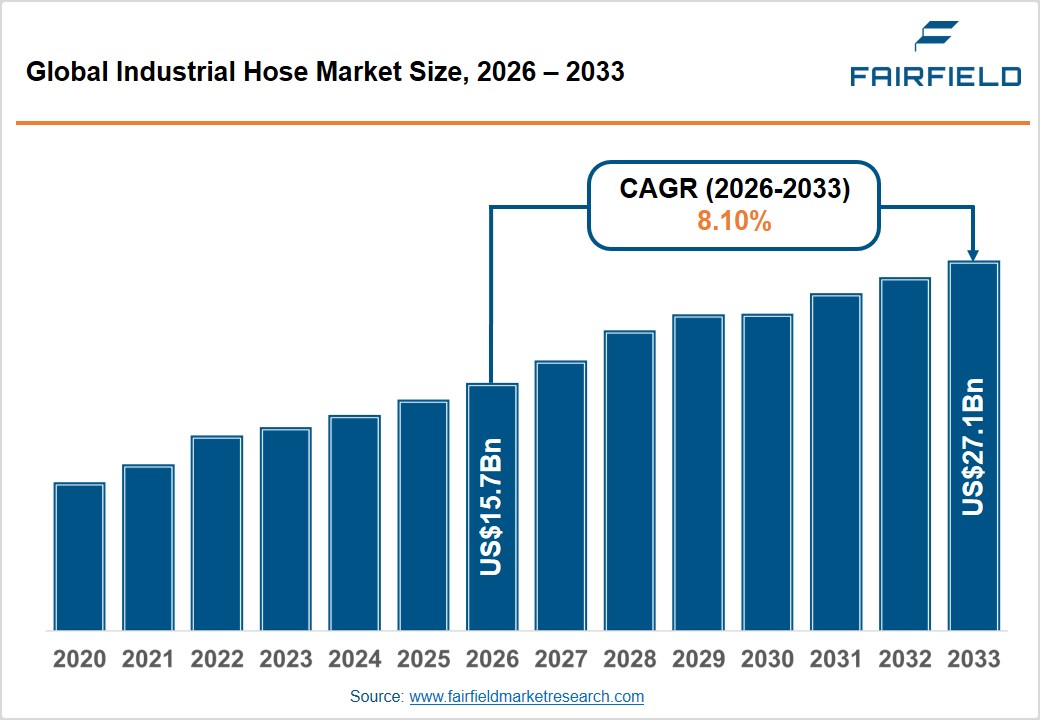

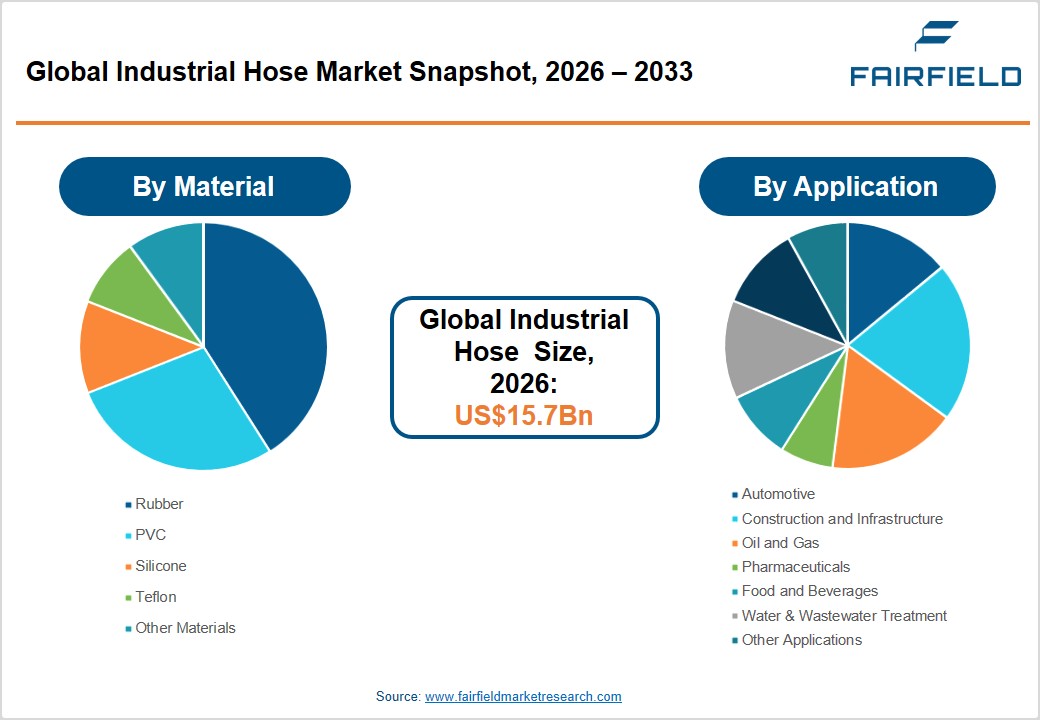

- The global Industrial Hose Market size is likely to be valued at USD 15.7 billion in 2026 and is expected to reach USD 27.1 billion by 2033, growing at a CAGR of 8.10% during the forecast period from 2026 to 2033.

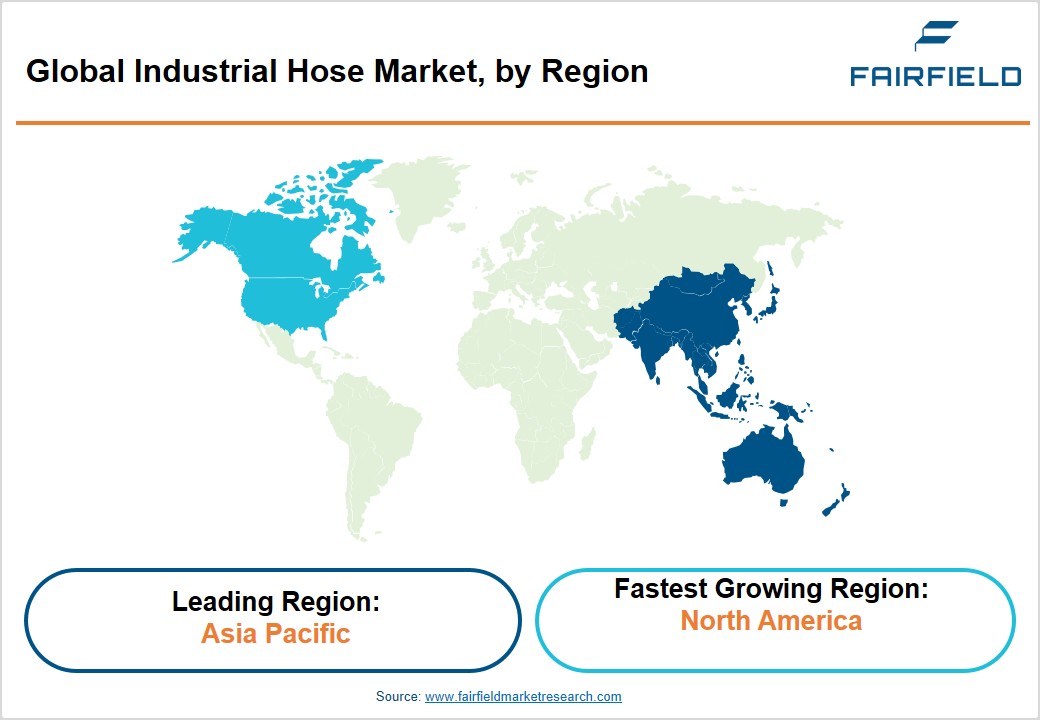

- Leading Region Market: Asia Pacific holds the dominant position in the global industrial hose market with approximately 39% revenue share, led by China's manufacturing powerhouse status, India's infrastructure expansion, and ASEAN's rapid industrialization trajectory.

- Fastest Growing Region Market: North America is the fastest-growing regional market, propelled by massive federal infrastructure investments under the IIJA and IRA, combined with the U.S.'s position as the world's top crude oil producer, exceeding 9 million barrels/day.

- Dominant Segment: Rubber (Material Type) accounts for approximately 38% of industrial hose market share, preferred for its superior mechanical strength, flexibility, and pressure resistance across hydraulic, pneumatic, and steam-transfer applications in heavy industries.

- Fastest Growing Segment: Silicone hoses are the fastest growing material segment, driven by surging demand from pharmaceutical bioprocessing, food & beverage production, and EV automotive cooling systems where high-purity, temperature-resistant materials are mandated.

- Key Market Opportunity: Water & Wastewater Treatment: Global water infrastructure investment, including the US$ 55 billionS. water infrastructure allocation, presents a significant opportunity for manufacturers of chemically resistant and UV-stable industrial hoses for treatment and distribution systems.

Market Dynamics

Market Growth Drivers

Surging Demand from Oil & Gas Sector

The oil & gas sector remains one of the most significant demand generators for industrial hoses, driven by intensifying upstream exploration and midstream transportation activities. According to the International Energy Agency (IEA), global upstream oil & gas capital expenditure rose to approximately US$ 528 billion in 2023, reflecting recovering investment momentum post-pandemic. Industrial hoses are critical in this sector for transferring crude oil, refined fuels, chemicals, and drilling fluids under high-pressure conditions. The expansion of LNG terminals and offshore drilling rigs necessitates high-grade, corrosion-resistant hose assemblies. As global energy demand continues its upward trajectory, the oil & gas sector is expected to sustain consistent procurement of specialized industrial hose products, particularly thermoplastic and rubber variants with enhanced chemical resistance and pressure ratings.

Rapid Industrialization in Emerging Markets

Emerging economies, particularly in Asia Pacific and Latin America, are witnessing unprecedented levels of industrial expansion and infrastructure investment. India's National Infrastructure Pipeline plans massive capital spending through 2025, while China's Belt and Road Initiative keeps driving huge construction and manufacturing projects across more than 68 countries. These programs demand robust fluid management systems, including industrial hoses for water supply, concrete pumping, pneumatic tools, and hydraulic machinery. Additionally, the growth of the automotive manufacturing sector with global vehicle production exceeding 90 million units annually per OICA data further amplifies demand for precision-engineered hoses in assembly and testing applications.

Market Restraints

Volatility in Raw Material Prices

Industrial hoses are manufactured from raw materials including natural rubber, synthetic polymers such as PVC and PTFE, and silicone compounds. These materials are highly susceptible to price fluctuations driven by crude oil price volatility, supply chain disruptions, and geopolitical instability. Natural rubber prices, tracked by the Association of Natural Rubber Producing Countries (ANRPC), have historically exhibited 20–30% price swings year-over-year. Such volatility significantly impacts manufacturing cost structures and erodes profit margins for hose producers, particularly small and mid-sized companies that lack hedging capabilities or backward integration into raw material sourcing.

Stringent Environmental and Safety Regulations

Increasingly stringent environmental and workplace safety regulations across key markets pose compliance challenges for industrial hose manufacturers. In the European Union, regulations under REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) restrict the use of certain plasticizers and additives in hose compounds. Similarly, OSHA standards in the United States mandate strict material testing and pressure-rating certifications for hoses used in hazardous environments. Meeting these regulatory requirements necessitates significant R&D investment and certification costs, creating barriers for smaller players and potentially delaying product launches in regulated sectors such as pharmaceuticals and food processing.

Market Opportunities

Growth in Water & Wastewater Treatment Infrastructure

The global push toward sustainable water management presents a compelling opportunity for industrial hose manufacturers. The United Nations estimates that 2.2 billion people still lack access to safely managed drinking water, driving governments worldwide to increase investment in water and wastewater treatment infrastructure. The U.S. Infrastructure Investment and Jobs Act allocated over US$ 55 billion specifically for water infrastructure improvements. Industrial hoses are indispensable in water treatment facilities for chemical dosing, sludge transfer, and filtration processes. As municipalities upgrade aging water networks and new desalination plants come online in water-stressed regions like the Middle East and North Africa, demand for chemically resistant and UV-stable hose products is expected to surge substantially in the coming years.

Industrial Automation and Smart Hose Technology Adoption for Predictive Maintenance and Precision Flow Control

The accelerating deployment of Industry 4.0 technologies across manufacturing, oil & gas, and chemical processing sectors is creating a high-value growth frontier for smart hose systems integrated with embedded sensors, IoT connectivity, and real-time condition monitoring capabilities. According to the International Federation of Robotics (IFR), global industrial robot installations reached a record 553,052 units in 2022, reflecting the rapid pace of factory automation that demands precision fluid transfer and leak-proof hose assemblies. Smart hoses equipped with pressure, temperature, and flow sensors enable predictive maintenance by transmitting live performance data to centralized SCADA or CMMS platforms, helping operators detect hose degradation before failure significantly reducing unplanned downtime costs estimated at US$ 50 billion annually across process industries per Emerson Automation Solutions. Regulatory momentum around industrial safety standards such as ISO 4413 (hydraulic fluid power) and ISO 4414 (pneumatic fluid power) further incentivizes end-users to upgrade conventional hose assemblies to smart, sensor-integrated alternatives. This convergence of automation expansion and digital monitoring adoption presents industrial hose manufacturers with a compelling opportunity to develop premium, data-enabled hose product lines commanding significantly higher margins than conventional offerings.

Segmental Insights

Material Type Analysis

Rubber dominates the industrial hose market by material type, accounting for approximately 38% of total market share in 2026. This dominance is attributed to rubber's exceptional mechanical properties, including high tensile strength, abrasion resistance, flexibility across a wide temperature range, and superior pressure-bearing capacity. Natural and synthetic rubber hoses find extensive application in hydraulic systems, pneumatic conveyance, and steam handling sectors that form the backbone of manufacturing and construction industries. According to the International Rubber Study Group (IRSG), global rubber consumption continues to grow steadily, underpinned by automotive and industrial demand. Technological advancements in rubber compounding such as EPDM and NBR formulations further enhance performance characteristics, reinforcing rubber's position as the preferred material in demanding industrial environments.

Application Type Analysis

Oil & Gas is the leading application segment in the industrial hose market, commanding approximately 27% of total revenue share in 2026. The sector's dominance stems from the critical role industrial hoses play in upstream drilling, midstream pipeline operations, and downstream refining processes, where hoses must withstand extreme pressures, aggressive chemicals, and high temperatures. The U.S. Energy Information Administration (EIA) reports that global petroleum and other liquid fuel production reached approximately 101.6 million barrels per day in 2023, reflecting the scale of fluid transfer requirements in this sector. With ongoing LNG infrastructure expansions and offshore exploration projects across the Gulf of Mexico, North Sea, and Southeast Asia, oil & gas is expected to remain the dominant application segment throughout the forecast period.

Regional Insights

North America Industrial Hose Market Trends

North America is the fastest-growing regional market for industrial hoses, driven by a confluence of robust energy sector activity, large-scale infrastructure renewal, and advanced manufacturing expansion. The U.S. Infrastructure Investment and Jobs Act (IIJA) and the Inflation Reduction Act (IRA) collectively mobilize hundreds of billions of dollars into roads, bridges, water systems, energy infrastructure, and domestic manufacturing all of which are intensive consumers of industrial hose products. Additionally, the shale revolution continues to drive demand, with the U.S. Energy Information Administration reporting that the United States remained the world's largest crude oil producer in 2023, exceeding 12.9 million barrels per day.

Canada's growing oil sands operations and expanding pipeline infrastructure further complement regional demand. The region also benefits from a well-established innovation ecosystem, with leading players like Parker Hannifin Corporation and Gates Industrial Corporation headquartered in North America, continuously advancing product technologies including smart hoses with embedded sensors for real-time pressure and flow monitoring. Regulatory bodies such as the American National Standards Institute (ANSI) and SAE International ensure high product quality standards, reinforcing market confidence in North American-manufactured hose solutions.

Europe Industrial Hose Market Trends

Europe represents a mature yet innovation-driven market for industrial hoses, characterized by stringent product standards, a strong automotive manufacturing base, and progressive environmental regulations that are reshaping product design. Germany leads the regional market, driven by its dominant automotive sector home to Volkswagen, BMW, and Mercedes-Benzmwhere precision hoses are essential in cooling, hydraulic, and fuel systems. The European Automobile Manufacturers' Association (ACEA) reported 10.5 million new vehicle registrations in Europe in 2023, sustaining OEM and aftermarket hose demand.

The United Kingdom, France, and Spain contribute significantly through chemical processing, food & beverage manufacturing, and water infrastructure sectors. The EU Green Deal and related directives are accelerating demand for low-emission, sustainable hose materials, encouraging manufacturers like Continental AG and Trelleborg AB to invest in bio-based and recyclable hose compounds. Regulatory harmonization under EN ISO 6945 and related standards ensures product compatibility across member states, facilitating cross-border trade and market consistency.

Asia Pacific Industrial Hose Market Trends

Asia Pacific dominates the global industrial hose market, accounting for approximately 39% of total revenue share, driven by China's massive manufacturing output, India's infrastructure boom, Japan's precision engineering sector, and ASEAN nations' rapid industrialization China stays the biggest single-country market, with its industrial sector using massive amounts of hoses in construction, mining, oil & gas, and automotive sectors. The National Bureau of Statistics of China reported fixed-asset investment in manufacturing exceeding CNY 31 trillion in 2023, reflecting sustained industrial activity.

India's rapid infrastructure development under programs like PM Gati Shakti and the Smart Cities Mission is creating robust demand for hoses in water supply, construction, and energy infrastructure. Japan contributes through high-value, precision hose applications in electronics manufacturing and robotics. The region's cost-competitive manufacturing ecosystem combined with growing domestic consumption makes Asia Pacific both the largest production hub and the fastest-growing consumption market, with companies like Polyhose India Pvt. Ltd. and Kanaflex Corporation scaling operations to capture expanding regional demand.

Competitive Landscape

Market Structure Analysis

The global industrial hose market exhibits a moderately consolidated structure, with a handful of multinational corporations commanding significant revenue shares while a large number of regional and niche players compete on specialty products and localized service capabilities. Leading companies such as Parker Hannifin Corporation, Eaton Corporation, and Continental AG leverage extensive distribution networks, diversified product portfolios, and continuous R&D investment as key differentiators. Market leaders are increasingly pursuing strategic mergers, acquisitions, and partnerships to expand geographic reach and product breadth. A notable business model trend is the shift toward integrated fluid conveyance solutions offering hose assemblies, fittings, and digital monitoring tools as bundled packages enhancing customer stickiness and recurring revenue streams.

Key Market Developments

- March, 2024: Parker Hannifin Corporation expanded its hose manufacturing facility in Spartanburg, South Carolina, increasing production capacity for high-pressure hydraulic and industrial hose assemblies to meet rising demand from the oil & gas and construction sectors.

- September, 2024: Continental AG announced the launch of a new bio-based rubber hose product line designed for automotive and industrial applications, developed to meet EU sustainability mandates and reduce dependence on petroleum-derived raw materials.

- February, 2025: Eaton Corporation acquired a specialized thermoplastic hose manufacturer based in Germany, strengthening its European product portfolio and expanding capabilities in high-performance hose solutions for chemical processing and pharmaceutical industries.

Companies Covered in the Industrial Hose Market

- Parker Hannifin Corporation

- Gates Industrial Corporation

- Eaton Corporation

- Continental AG

- Trelleborg AB

- Semperit AG Holding

- Alfagomma S.p.A.

- RYCO Hydraulics

- Transfer Oil S.p.A.

- Polyhose India Pvt. Ltd.

- NORRES Schlauchtechnik GmbH

- Kuriyama of America, Inc.

- Kanaflex Corporation

- Colex International Limited

- Piranha Hose Products, Inc.

- Manuli Hydraulics

- Hansa-Flex AG

- Dunlop Oil & Marine (ContiTech)

Market Segmentation

By Material Type

- Rubber

- PVC

- Silicone

- Teflon (PTFE)

- Other Materials

By Application Type

- Automotive

- Construction & Infrastructure

- Oil & Gas

- Pharmaceuticals

- Food & Beverages

- Water & Wastewater Treatment

- Mining

- Other Applications

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Executive Summary

- Global Industrial Hose Market Snapshot

- Future Projections

- Key Market Trends

- Regional Snapshot, by Value, 2026

- Analyst Recommendations

- Market Overview

- Market Definitions and Segmentations

- Market Dynamics

- Drivers

- Restraints

- Market Opportunities

- Value Chain Analysis

- COVID-19 Impact Analysis

- Porter's Five Forces Analysis

- Impact of Russia-Ukraine Conflict

- PESTLE Analysis

- Regulatory Analysis

- Price Trend Analysis

- Current Prices and Future Projections, 2025-2033

- Price Impact Factors

- Global Industrial Hose Market Outlook, 2020 - 2033

- Global Industrial Hose Market Outlook, by Material Type , Value (US$ Bn), 2020-2033

- Rubber

- PVC

- Silicone

- Teflon

- Other Materials

- Global Industrial Hose Market Outlook, by Application Type , Value (US$ Bn), 2020-2033

- Automotive

- Construction & Infrastructure

- Oil & Gas

- Pharmaceuticals

- Food & Beverages

- Water & Wastewater Treatment

- Mining

- Other Applications

- Global Industrial Hose Market Outlook, by Region, Value (US$ Bn), 2020-2033

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Global Industrial Hose Market Outlook, by Material Type , Value (US$ Bn), 2020-2033

- North America Industrial Hose Market Outlook, 2020 - 2033

- North America Industrial Hose Market Outlook, by Material Type , Value (US$ Bn), 2020-2033

- Rubber

- PVC

- Silicone

- Teflon

- Other Materials

- North America Industrial Hose Market Outlook, by Application Type , Value (US$ Bn), 2020-2033

- Automotive

- Construction & Infrastructure

- Oil & Gas

- Pharmaceuticals

- Food & Beverages

- Water & Wastewater Treatment

- Mining

- Other Applications

- North America Industrial Hose Market Outlook, by Country, Value (US$ Bn), 2020-2033

- U.S. Industrial Hose Market Outlook, by Material Type , 2020-2033

- U.S. Industrial Hose Market Outlook, by Application Type , 2020-2033

- Canada Industrial Hose Market Outlook, by Material Type , 2020-2033

- Canada Industrial Hose Market Outlook, by Application Type , 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- North America Industrial Hose Market Outlook, by Material Type , Value (US$ Bn), 2020-2033

- Europe Industrial Hose Market Outlook, 2020 - 2033

- Europe Industrial Hose Market Outlook, by Material Type , Value (US$ Bn), 2020-2033

- Rubber

- PVC

- Silicone

- Teflon

- Other Materials

- Europe Industrial Hose Market Outlook, by Application Type , Value (US$ Bn), 2020-2033

- Automotive

- Construction & Infrastructure

- Oil & Gas

- Pharmaceuticals

- Food & Beverages

- Water & Wastewater Treatment

- Mining

- Other Applications

- Europe Industrial Hose Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Germany Industrial Hose Market Outlook, by Material Type , 2020-2033

- Germany Industrial Hose Market Outlook, by Application Type , 2020-2033

- Italy Industrial Hose Market Outlook, by Material Type , 2020-2033

- Italy Industrial Hose Market Outlook, by Application Type , 2020-2033

- France Industrial Hose Market Outlook, by Material Type , 2020-2033

- France Industrial Hose Market Outlook, by Application Type , 2020-2033

- U.K. Industrial Hose Market Outlook, by Material Type , 2020-2033

- U.K. Industrial Hose Market Outlook, by Application Type , 2020-2033

- Spain Industrial Hose Market Outlook, by Material Type , 2020-2033

- Spain Industrial Hose Market Outlook, by Application Type , 2020-2033

- Russia Industrial Hose Market Outlook, by Material Type , 2020-2033

- Russia Industrial Hose Market Outlook, by Application Type , 2020-2033

- Rest of Europe Industrial Hose Market Outlook, by Material Type , 2020-2033

- Rest of Europe Industrial Hose Market Outlook, by Application Type , 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Europe Industrial Hose Market Outlook, by Material Type , Value (US$ Bn), 2020-2033

- Asia Pacific Industrial Hose Market Outlook, 2020 - 2033

- Asia Pacific Industrial Hose Market Outlook, by Material Type , Value (US$ Bn), 2020-2033

- Rubber

- PVC

- Silicone

- Teflon

- Other Materials

- Asia Pacific Industrial Hose Market Outlook, by Application Type , Value (US$ Bn), 2020-2033

- Automotive

- Construction & Infrastructure

- Oil & Gas

- Pharmaceuticals

- Food & Beverages

- Water & Wastewater Treatment

- Mining

- Other Applications

- Asia Pacific Industrial Hose Market Outlook, by Country, Value (US$ Bn), 2020-2033

- China Industrial Hose Market Outlook, by Material Type , 2020-2033

- China Industrial Hose Market Outlook, by Application Type , 2020-2033

- Japan Industrial Hose Market Outlook, by Material Type , 2020-2033

- Japan Industrial Hose Market Outlook, by Application Type , 2020-2033

- South Korea Industrial Hose Market Outlook, by Material Type , 2020-2033

- South Korea Industrial Hose Market Outlook, by Application Type , 2020-2033

- India Industrial Hose Market Outlook, by Material Type , 2020-2033

- India Industrial Hose Market Outlook, by Application Type , 2020-2033

- Southeast Asia Industrial Hose Market Outlook, by Material Type , 2020-2033

- Southeast Asia Industrial Hose Market Outlook, by Application Type , 2020-2033

- Rest of SAO Industrial Hose Market Outlook, by Material Type , 2020-2033

- Rest of SAO Industrial Hose Market Outlook, by Application Type , 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Asia Pacific Industrial Hose Market Outlook, by Material Type , Value (US$ Bn), 2020-2033

- Latin America Industrial Hose Market Outlook, 2020 - 2033

- Latin America Industrial Hose Market Outlook, by Material Type , Value (US$ Bn), 2020-2033

- Rubber

- PVC

- Silicone

- Teflon

- Other Materials

- Latin America Industrial Hose Market Outlook, by Application Type , Value (US$ Bn), 2020-2033

- Automotive

- Construction & Infrastructure

- Oil & Gas

- Pharmaceuticals

- Food & Beverages

- Water & Wastewater Treatment

- Mining

- Other Applications

- Latin America Industrial Hose Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Brazil Industrial Hose Market Outlook, by Material Type , 2020-2033

- Brazil Industrial Hose Market Outlook, by Application Type , 2020-2033

- Mexico Industrial Hose Market Outlook, by Material Type , 2020-2033

- Mexico Industrial Hose Market Outlook, by Application Type , 2020-2033

- Argentina Industrial Hose Market Outlook, by Material Type , 2020-2033

- Argentina Industrial Hose Market Outlook, by Application Type , 2020-2033

- Rest of LATAM Industrial Hose Market Outlook, by Material Type , 2020-2033

- Rest of LATAM Industrial Hose Market Outlook, by Application Type , 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Latin America Industrial Hose Market Outlook, by Material Type , Value (US$ Bn), 2020-2033

- Middle East & Africa Industrial Hose Market Outlook, 2020 - 2033

- Middle East & Africa Industrial Hose Market Outlook, by Material Type , Value (US$ Bn), 2020-2033

- Rubber

- PVC

- Silicone

- Teflon

- Other Materials

- Middle East & Africa Industrial Hose Market Outlook, by Application Type , Value (US$ Bn), 2020-2033

- Automotive

- Construction & Infrastructure

- Oil & Gas

- Pharmaceuticals

- Food & Beverages

- Water & Wastewater Treatment

- Mining

- Other Applications

- Middle East & Africa Industrial Hose Market Outlook, by Country, Value (US$ Bn), 2020-2033

- GCC Industrial Hose Market Outlook, by Material Type , 2020-2033

- GCC Industrial Hose Market Outlook, by Application Type , 2020-2033

- South Africa Industrial Hose Market Outlook, by Material Type , 2020-2033

- South Africa Industrial Hose Market Outlook, by Application Type , 2020-2033

- Egypt Industrial Hose Market Outlook, by Material Type , 2020-2033

- Egypt Industrial Hose Market Outlook, by Application Type , 2020-2033

- Nigeria Industrial Hose Market Outlook, by Material Type , 2020-2033

- Nigeria Industrial Hose Market Outlook, by Application Type , 2020-2033

- Rest of Middle East Industrial Hose Market Outlook, by Material Type , 2020-2033

- Rest of Middle East Industrial Hose Market Outlook, by Application Type , 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Middle East & Africa Industrial Hose Market Outlook, by Material Type , Value (US$ Bn), 2020-2033

- Competitive Landscape

- Company Vs Segment Heatmap

- Company Market Share Analysis, 2025

- Competitive Dashboard

- Company Profiles

- Parker Hannifin Corporation

- Company Overview

- Product Portfolio

- Financial Overview

- Business Strategies and Developments

- Gates Industrial Corporation

- Eaton Corporation

- Continental AG

- Trelleborg AB

- Semperit AG Holding

- Alfagomma S.p.A.

- RYCO Hydraulics

- Transfer Oil S.p.A.

- Polyhose India Pvt. Ltd.

- NORRES Schlauchtechnik GmbH

- Kuriyama of America, Inc.

- Kanaflex Corporation

- Colex International Limited

- Piranha Hose Products, Inc.

- Parker Hannifin Corporation

- Appendix

- Research Methodology

- Report Assumptions

- Acronyms and Abbreviations

|

BASE YEAR |

HISTORICAL DATA |

FORECAST PERIOD |

UNITS |

|||

|

2025 |

|

2020 - 2025 |

2026 - 2033 |

Value: US$ Million |

||

|

REPORT FEATURES |

DETAILS |

|

Material Type |

|

|

Application |

|

|

Geographical Coverage |

|

|

Leading Companies |

|

|

Report Highlights |

Key Market Indicators, Macro-micro economic impact analysis, Technological Roadmap, Key Trends, Driver, Restraints, and Future Opportunities & Revenue Pockets, Porter’s 5 Forces Analysis, Historical Trend (2019-2024), Market Estimates and Forecast, Market Dynamics, Industry Trends, Competition Landscape, Category, Region, Country-wise Trends & Analysis, COVID-19 Impact Analysis (Demand and Supply Chain) |