Polycarbonate Market Size, Share, and Growth Forecast 2026 - 2033

Key Market Highlights

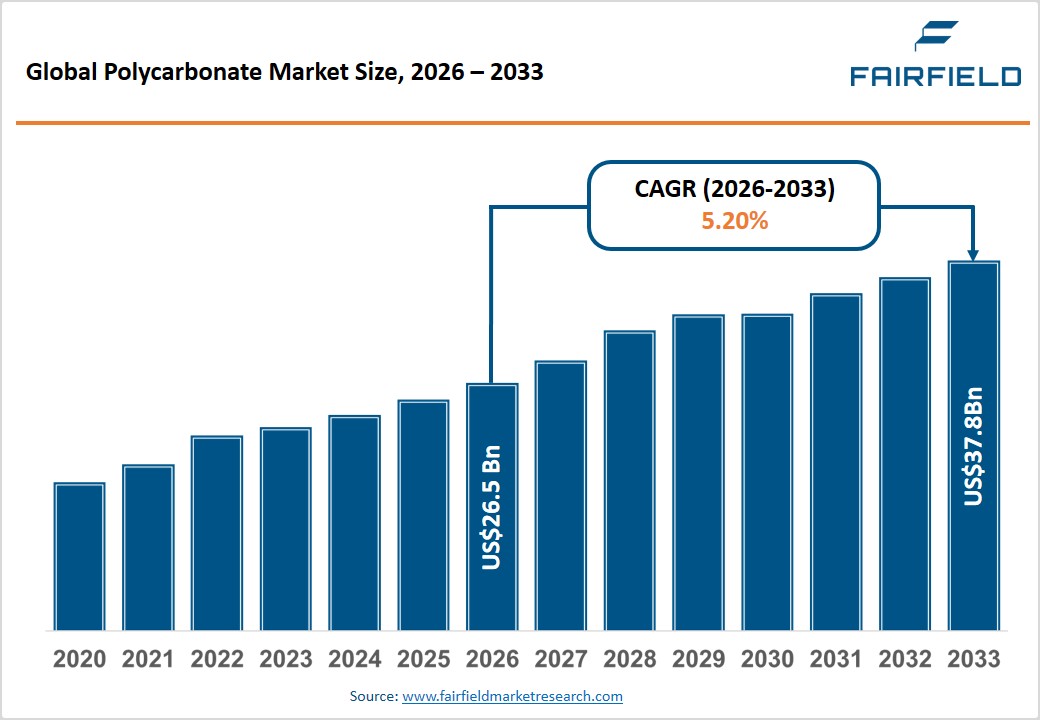

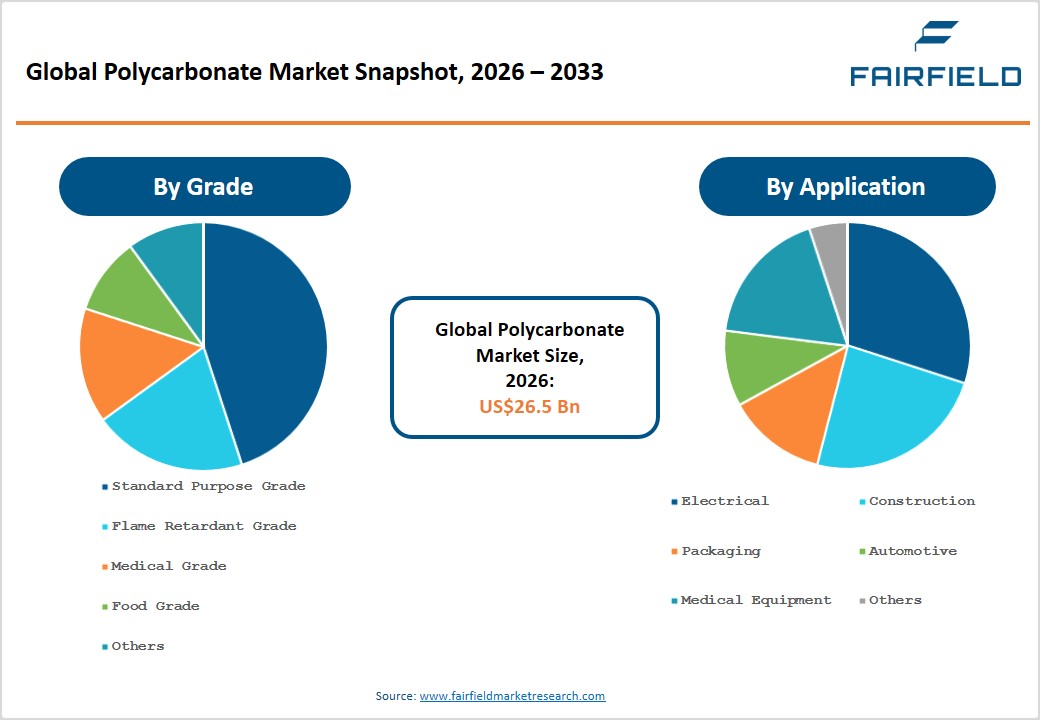

- The global Polycarbonate Market size is likely to be valued at US$ 26.5 Billion in 2026 and is expected to reach US$ 37.8 Billion by 2033, growing at a CAGR of 5.20% during the forecast period from 2026 to 2033.

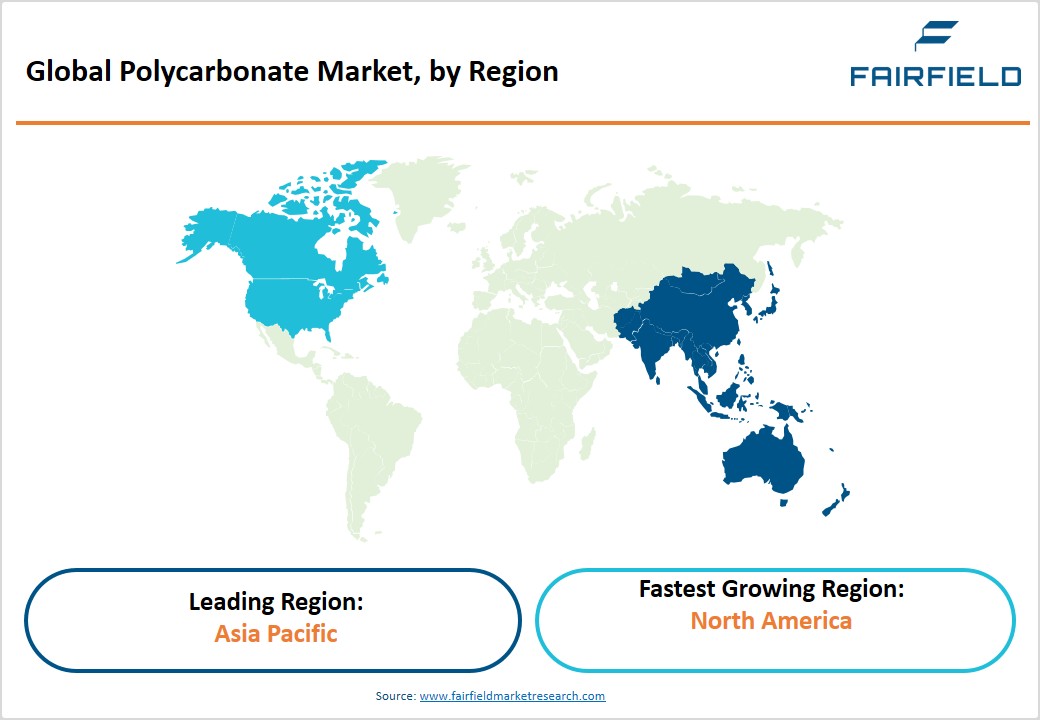

- Leading Region Market: Asia Pacific dominates the global polycarbonate market with approximately 55% share in 2026, driven by China's large-scale manufacturing base, Japan's high-performance specialty grades, and India's rapidly expanding electronics and automotive sectors.

- Fastest Growing Region Market: North America is the fastest-growing polycarbonate market, propelled by EV production ramp-up, semiconductor manufacturing investments under the CHIPS Act, and infrastructure modernization driving sustained demand for engineering thermoplastics.

- Dominant Segment: Standard Purpose Grade holds the leading position by grade 45% share in 2026, owing to its versatile application across high-volume automotive, electrical, and construction end-use sectors and compatibility with standard processing techniques.

- Fastest Growing Segment: Medical Grade polycarbonate is among the fastest-growing segments, driven by expanding global healthcare infrastructure, increasing medical device manufacturing in Asia Pacific, and rising demand for biocompatible, sterilizable polymer solutions.

- Key Market Opportunity – Sustainable & Recyclable Polycarbonate: Growing circular economy mandates and ESG procurement policies are creating significant opportunity for bio-based and chemically recyclable polycarbonate grades, particularly in Europe and North America, enabling premium pricing and long-term supply partnerships.

Market Dynamics

Market Growth Drivers

Rising Demand from Automotive Lightweight Initiatives

The global automotive industry's shift toward vehicle lightweight to comply with stringent emissions regulations is a significant growth catalyst for polycarbonate demand. Polycarbonate components weigh up to 50% less than conventional glass, making them ideal for glazing, headlamp lenses, instrument panels, and exterior body panels. The International Energy Agency (IEA) reports that passenger vehicles account for approximately 17% of global CO₂ emissions, intensifying regulatory pressure on automakers to reduce vehicle weight. Regulatory frameworks such as the European Union's CO₂ emission standards (targeting 100 g CO₂/km by 2025 for new cars) are compelling OEMs to substitute traditional materials with advanced engineering plastics. As electric vehicle production scales globally with the International Energy Agency reporting over 14 million EV sales in 2023 the demand for lightweight, durable polycarbonate parts is set to accelerate further.

Expanding Electrical & Electronics Manufacturing

The exponential growth of global electronics manufacturing is a powerful demand driver for polycarbonate, which offers superior electrical insulation, heat resistance up to 135°C, and flame-retardant properties. According to the World Semiconductor Trade Statistics (WSTS), global semiconductor sales reached approximately US$ 527 billion in 2023, with downstream demand for electronic enclosures, connectors, and display components rising proportionally. Polycarbonate's intrinsic dielectric properties make it critical in switchgear housings, power distribution equipment, and circuit breaker components. The rapid rollout of 5G infrastructure and expansion of data centers globally with the International Data Corporation (IDC) projecting data center spending to exceed US$ 400 billion by 2027 is further reinforcing the need for high-performance thermoplastics in the electrical engineering segment.

Market Restraints

Environmental Concerns and Regulatory Pressure on BPA-Based Polycarbonate

A significant restraint facing the polycarbonate market is the growing regulatory scrutiny surrounding Bisphenol A (BPA), the primary monomer used in conventional polycarbonate synthesis. BPA has been classified as an endocrine disruptor by the European Chemicals Agency (ECHA) and is subject to increasing restrictions in food contact and medical applications. The European Union restricted BPA use in thermal paper from January 2020 and continues to tighten its scope. This regulatory climate is forcing manufacturers to invest in costlier BPA-free or alternative material solutions, potentially slowing adoption in sensitive application segments and adding reformulation costs that compress margins.

High Raw Material Price Volatility

Polycarbonate production is directly dependent on petrochemical feedstocks primarily Bisphenol A (BPA) and phosgene whose prices are subject to significant volatility linked to crude oil dynamics. The U.S. Energy Information Administration (EIA) has documented recurring cycles of crude oil price instability that translate into upstream petrochemical cost inflation. During 2021–2022, global supply chain disruptions caused specialty chemical prices to surge by over 30–40% in certain categories, directly impacting polycarbonate production economics. Such input cost unpredictability makes it difficult for mid-tier manufacturers to offer stable pricing, thereby constraining capacity expansions and discouraging new market entrants, particularly in price-sensitive emerging markets.

Market Opportunities

Surge in Sustainable and Recyclable Polycarbonate Demand

The global shift toward circular economy principles and sustainable materials presents a significant opportunity for manufacturers to develop bio-based and chemically recyclable polycarbonate grades. The European Commission's Circular Economy Action Plan mandates increasing recycled content across plastics applications, while Japan's Ministry of Economy, Trade and Industry (METI) has set targets for bio-based plastics to account for 2 million tonnes of domestic usage by 2030. Key players such as Covestro AG have already begun commercializing polycarbonate produced using up to 100% bio-circular feedstocks. This trend represents a dual opportunity: capturing premium pricing for sustainable-grade products and securing supply agreements with ESG-committed end-users in automotive, electronics, and packaging sectors, where sustainability credentials are increasingly influencing procurement decisions.

Electronics Industry Expansion and 5G Infrastructure Rollout Driving Demand for High-Performance Polycarbonate

The rapid global rollout of 5G network infrastructure and the steady growth of the consumer electronics industry are creating a strong, high‑value demand for polycarbonate. This is because polycarbonate offers an excellent combination of high thermal stability, good electrical insulation, flame retardancy, and optical clarity. As 5G networks expand, there is growing need for base station enclosures, antenna radomes, and small‑cell housings, where polycarbonate’s low dielectric constant and ability to transmit radio signals make it a preferred material over traditional plastics and metals. At the same time, the smartphone market continues to drive demand for precision‑grade polycarbonate used in device frames, camera lens covers, and display substrates. The fast adoption of LED lighting systems also boosts polycarbonate demand, as it is widely used for light diffusers and heat‑resistant components in luminaires. Together, the expansion of 5G infrastructure, the miniaturization of electronic devices, and the shift to energy‑efficient lighting create a structurally growing opportunity for manufacturers of high‑performance, engineering‑grade, and flame‑retardant polycarbonate.

Segmental Insights

By Grade Analysis

The Standard Purpose Grade segment dominates the polycarbonate market, accounting for approximately 45%share in 2026. This grade's leadership position is attributable to its broad applicability across the highest-volume end-use industries, including automotive, electronics, and construction. Standard purpose polycarbonate offers the optimal balance of mechanical strength, optical clarity, and processability at cost-effective production scales. According to Plastics Europe, engineering thermoplastics including polycarbonate account for a growing share of total polymer demand in Europe, with automotive and electrical applications as the primary offtake sectors. The grade's compatibility with standard injection molding and extrusion processes enables high-volume, low-cost manufacturing, sustaining its dominant position as global industrialization and consumer electronics demand continue to expand.

By Application Analysis

The Electrical segment leads the polycarbonate market by application, representing an estimated 32% share in 2026. Polycarbonate's excellent dielectric strength, dimensional stability, and flame-retardant properties particularly in UL 94 V-0 rated formulations make it the material of choice for electrical enclosures, connectors, switchgear, and lighting components. The International Electrotechnical Commission (IEC) standards for electrical insulation materials consistently reference polycarbonate among approved thermoplastics. The global electrification drive, rising energy infrastructure investments, and the proliferation of consumer electronics continue to sustain the dominance of this segment. Increasing penetration of smart grid technologies and LED lighting driven by government energy efficiency mandates across North America, Europe, and Asia Pacific further reinforces electrical applications as the primary growth engine.

Regional Insights

North America Polycarbonate Market Trends

North America represents the fastest-growing regional market for polycarbonate, driven by robust automotive sector recovery, expanding electronics manufacturing reshoring initiatives, and significant public investments in infrastructure modernization. The U.S. Infrastructure Investment and Jobs Act (2021), is indirectly stimulating demand for durable engineering plastics including polycarbonate in construction and electrical applications. The region's well-established automotive OEM base anchored by General Motors, Ford, and Tesla is increasingly integrating polycarbonate glazing and interior components as electric vehicle production scales.

On the regulatory front, the U.S. Environmental Protection Agency (EPA) and FDA provide a structured framework governing material approvals for food-contact and medical applications, creating a stable compliance environment that supports product innovation. The CHIPS and Science Act (2022), committing over US$ 52 billion to domestic semiconductor manufacturing, is expected to generate sustained downstream demand for polycarbonate in semiconductor packaging and electronic device components, reinforcing North America's trajectory as the fastest-growing polycarbonate market.

Europe Polycarbonate Market Trends

Europe remains a significant polycarbonate market, anchored by its advanced automotive, electrical engineering, and precision manufacturing industries. Germany, as Europe's largest automotive manufacturer and home to Covestro AG one of the world's leading polycarbonate producers plays a central role in shaping regional market dynamics. The European Green Deal and the bloc's Fit for 55 climate package are accelerating vehicle electrification, which in turn drives polycarbonate demand for lightweight automotive glazing and EV battery housings. France and Spain are emerging as renewable energy hubs, with solar panel backsheets and wind turbine components increasingly utilizing UV-stabilized polycarbonate grades. The U.K. retains its position as a leading market for medical devices and optical applications. The European Chemicals Agency's (ECHA) REACH regulation continues to impose stringent material safety standards, incentivizing manufacturers to develop compliant, next-generation formulations while simultaneously raising barriers to entry for non-compliant suppliers a dynamic that consolidates market share among established European producers.

Asia Pacific Polycarbonate Market Trends

Asia Pacific is the dominant region in the global polycarbonate market, commanding approximately 55% share in 2026. The region's leadership is underpinned by China's position as the world's largest polycarbonate consumer and manufacturer, supported by a comprehensive petrochemical feedstock supply chain and vast electronics assembly capacity. According to China's National Development and Reform Commission (NDRC), polycarbonate production capacity in China has expanded significantly, with domestic producers like Wanhua Chemical Group and Kingfa Sci. & Tech. scaling operations to meet both domestic and export demand.

Japan maintains technological leadership in high-performance optical and medical-grade polycarbonate, with Teijin Limited, Mitsubishi Engineering Plastics, and Idemitsu Kosan at the forefront. India's booming electronics manufacturing sector spurred by the Production Linked Incentive (PLI) scheme targeting over US$ 10 billion in mobile manufacturing incentives and expanding automotive OEM base are rapidly increasing domestic polycarbonate consumption. ASEAN nations, particularly Vietnam, Thailand, and Indonesia, are emerging as high-growth markets driven by foreign direct investment in electronics and automotive assembly, making Asia Pacific the undisputed engine of global polycarbonate market growth.

Competitive Landscape

Market Structure Analysis

The global polycarbonate market exhibits a moderately consolidated structure, with a small number of large integrated chemical conglomerates including Covestro, SABIC, Teijin Limited, and LG Chem commanding significant production capacity and global distribution networks. Key strategic differentiators include proprietary resin formulations, backward integration into BPA and phosgene feedstocks, and geographic diversification across Asia Pacific, Europe, and North America. Leading players are increasingly focusing on sustainability-driven product portfolios, bio-based polycarbonate grades, and chemical recycling investments to align with tightening ESG mandates. Strategic capacity expansions in Asia particularly China and R&D investment in specialty grades (flame retardant, optical, medical) are the primary competitive battlegrounds, with mid-tier regional producers competing primarily on cost and localized supply chain agility.

Key Market Developments

- April 2024: Covestro AG announced a strategic investment to scale its bio-circular polycarbonate production capacity in Germany, targeting carbon-neutral polymer grades for automotive and electronics customers under its CQ product line.

- September 2024: SABIC unveiled its LNP ELCRIN iQ series of recycled-content polycarbonate compounds at K 2024 trade fair, reinforcing its commitment to circular economy materials for electrical and automotive applications.

- March 2023: Wanhua Chemical Group officially commenced commercial production at its expanded polycarbonate facility in Yantai, China, adding approximately 130,000 tonnes/year of annual capacity to the Asia Pacific supply chain.

Companies Covered in Polycarbonate Market

- Covestro AG

- SABIC

- LG Chem

- Teijin Limited

- Mitsubishi Engineering Plastics Corporation

- Lotte Chemical

- Chi Mei Corporation

- Formosa Chemicals & Fibre Corporation

- Idemitsu Kosan

- Trinseo

- Wanhua Chemical Group

- Asahi Kasei Corporation

- Sumitomo Chemical

- Kingfa Sci. & Tech. Co., Ltd.

- Mitsubishi Gas Chemical Company

- Bayer AG

- Evonik Industries AG

Market Segmentation

The Polycarbonate Market report provides comprehensive segmentation coverage across the following categories:

By Grade

- Standard Purpose Grade

- Flame Retardant Grade

- Medical Grade

- Food Grade

- Others

By Application

- Electrical

- Construction

- Packaging

- Automotive

- Medical Equipment

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Executive Summary

- Global Polycarbonate Market Snapshot

- Future Projections

- Key Market Trends

- Regional Snapshot, by Value, 2026

- Analyst Recommendations

- Market Overview

- Market Definitions and Segmentations

- Market Dynamics

- Drivers

- Restraints

- Market Opportunities

- Value Chain Analysis

- COVID-19 Impact Analysis

- Porter's Five Forces Analysis

- Impact of Russia-Ukraine Conflict

- PESTLE Analysis

- Regulatory Analysis

- Price Trend Analysis

- Current Prices and Future Projections, 2025-2033

- Price Impact Factors

- Global Polycarbonate Market Outlook, 2020 - 2033

- Global Polycarbonate Market Outlook, by Grade, Value (US$ Bn), 2020-2033

- Standard Purpose Grade

- Flame Retardant Grade

- Medical Grade

- Food Grade

- Others

- Global Polycarbonate Market Outlook, by Application, Value (US$ Bn), 2020-2033

- Electrical

- Construction

- Packaging

- Automotive

- Medical Equipment

- Others

- Global Polycarbonate Market Outlook, by Region, Value (US$ Bn), 2020-2033

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Global Polycarbonate Market Outlook, by Grade, Value (US$ Bn), 2020-2033

- North America Polycarbonate Market Outlook, 2020 - 2033

- North America Polycarbonate Market Outlook, by Grade, Value (US$ Bn), 2020-2033

- Standard Purpose Grade

- Flame Retardant Grade

- Medical Grade

- Food Grade

- Others

- North America Polycarbonate Market Outlook, by Application, Value (US$ Bn), 2020-2033

- Electrical

- Construction

- Packaging

- Automotive

- Medical Equipment

- Others

- North America Polycarbonate Market Outlook, by Country, Value (US$ Bn), 2020-2033

- S. Polycarbonate Market Outlook, by Grade, 2020-2033

- S. Polycarbonate Market Outlook, by Application, 2020-2033

- Canada Polycarbonate Market Outlook, by Grade, 2020-2033

- Canada Polycarbonate Market Outlook, by Application, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- North America Polycarbonate Market Outlook, by Grade, Value (US$ Bn), 2020-2033

- Europe Polycarbonate Market Outlook, 2020 - 2033

- Europe Polycarbonate Market Outlook, by Grade, Value (US$ Bn), 2020-2033

- Standard Purpose Grade

- Flame Retardant Grade

- Medical Grade

- Food Grade

- Others

- Europe Polycarbonate Market Outlook, by Application, Value (US$ Bn), 2020-2033

- Electrical

- Construction

- Packaging

- Automotive

- Medical Equipment

- Others

- Europe Polycarbonate Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Germany Polycarbonate Market Outlook, by Grade, 2020-2033

- Germany Polycarbonate Market Outlook, by Application, 2020-2033

- Italy Polycarbonate Market Outlook, by Grade, 2020-2033

- Italy Polycarbonate Market Outlook, by Application, 2020-2033

- France Polycarbonate Market Outlook, by Grade, 2020-2033

- France Polycarbonate Market Outlook, by Application, 2020-2033

- K. Polycarbonate Market Outlook, by Grade, 2020-2033

- K. Polycarbonate Market Outlook, by Application, 2020-2033

- Spain Polycarbonate Market Outlook, by Grade, 2020-2033

- Spain Polycarbonate Market Outlook, by Application, 2020-2033

- Russia Polycarbonate Market Outlook, by Grade, 2020-2033

- Russia Polycarbonate Market Outlook, by Application, 2020-2033

- Rest of Europe Polycarbonate Market Outlook, by Grade, 2020-2033

- Rest of Europe Polycarbonate Market Outlook, by Application, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Europe Polycarbonate Market Outlook, by Grade, Value (US$ Bn), 2020-2033

- Asia Pacific Polycarbonate Market Outlook, 2020 - 2033

- Asia Pacific Polycarbonate Market Outlook, by Grade, Value (US$ Bn), 2020-2033

- Standard Purpose Grade

- Flame Retardant Grade

- Medical Grade

- Food Grade

- Others

- Asia Pacific Polycarbonate Market Outlook, by Application, Value (US$ Bn), 2020-2033

- Electrical

- Construction

- Packaging

- Automotive

- Medical Equipment

- Others

- Asia Pacific Polycarbonate Market Outlook, by Country, Value (US$ Bn), 2020-2033

- China Polycarbonate Market Outlook, by Grade, 2020-2033

- China Polycarbonate Market Outlook, by Application, 2020-2033

- Japan Polycarbonate Market Outlook, by Grade, 2020-2033

- Japan Polycarbonate Market Outlook, by Application, 2020-2033

- South Korea Polycarbonate Market Outlook, by Grade, 2020-2033

- South Korea Polycarbonate Market Outlook, by Application, 2020-2033

- India Polycarbonate Market Outlook, by Grade, 2020-2033

- India Polycarbonate Market Outlook, by Application, 2020-2033

- Southeast Asia Polycarbonate Market Outlook, by Grade, 2020-2033

- Southeast Asia Polycarbonate Market Outlook, by Application, 2020-2033

- Rest of SAO Polycarbonate Market Outlook, by Grade, 2020-2033

- Rest of SAO Polycarbonate Market Outlook, by Application, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Asia Pacific Polycarbonate Market Outlook, by Grade, Value (US$ Bn), 2020-2033

- Latin America Polycarbonate Market Outlook, 2020 - 2033

- Latin America Polycarbonate Market Outlook, by Grade, Value (US$ Bn), 2020-2033

- Standard Purpose Grade

- Flame Retardant Grade

- Medical Grade

- Food Grade

- Others

- Latin America Polycarbonate Market Outlook, by Application, Value (US$ Bn), 2020-2033

- Electrical

- Construction

- Packaging

- Automotive

- Medical Equipment

- Others

- Latin America Polycarbonate Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Brazil Polycarbonate Market Outlook, by Grade, 2020-2033

- Brazil Polycarbonate Market Outlook, by Application, 2020-2033

- Mexico Polycarbonate Market Outlook, by Grade, 2020-2033

- Mexico Polycarbonate Market Outlook, by Application, 2020-2033

- Argentina Polycarbonate Market Outlook, by Grade, 2020-2033

- Argentina Polycarbonate Market Outlook, by Application, 2020-2033

- Rest of LATAM Polycarbonate Market Outlook, by Grade, 2020-2033

- Rest of LATAM Polycarbonate Market Outlook, by Application, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Latin America Polycarbonate Market Outlook, by Grade, Value (US$ Bn), 2020-2033

- Middle East & Africa Polycarbonate Market Outlook, 2020 - 2033

- Middle East & Africa Polycarbonate Market Outlook, by Grade, Value (US$ Bn), 2020-2033

- Standard Purpose Grade

- Flame Retardant Grade

- Medical Grade

- Food Grade

- Others

- Middle East & Africa Polycarbonate Market Outlook, by Application, Value (US$ Bn), 2020-2033

- Electrical

- Construction

- Packaging

- Automotive

- Medical Equipment

- Others

- Middle East & Africa Polycarbonate Market Outlook, by Country, Value (US$ Bn), 2020-2033

- GCC Polycarbonate Market Outlook, by Grade, 2020-2033

- GCC Polycarbonate Market Outlook, by Application, 2020-2033

- South Africa Polycarbonate Market Outlook, by Grade, 2020-2033

- South Africa Polycarbonate Market Outlook, by Application, 2020-2033

- Egypt Polycarbonate Market Outlook, by Grade, 2020-2033

- Egypt Polycarbonate Market Outlook, by Application, 2020-2033

- Nigeria Polycarbonate Market Outlook, by Grade, 2020-2033

- Nigeria Polycarbonate Market Outlook, by Application, 2020-2033

- Rest of Middle East Polycarbonate Market Outlook, by Grade, 2020-2033

- Rest of Middle East Polycarbonate Market Outlook, by Application, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Middle East & Africa Polycarbonate Market Outlook, by Grade, Value (US$ Bn), 2020-2033

- Competitive Landscape

- Company Vs Segment Heatmap

- Company Market Share Analysis, 2025

- Competitive Dashboard

- Company Profiles

- Covestro

- Company Overview

- Product Portfolio

- Financial Overview

- Business Strategies and Developments

- SABIC

- LG Chem

- Teijin Limited

- Mitsubishi Engineering‑Plastics Corporation

- Lotte Chemical

- Chi Mei Corporation

- Formosa Chemicals & Fibre Corporation

- Idemitsu Kosan

- Trinseo

- Wanhua Chemical Group

- Asahi Kasei Corporation

- Sumitomo Chemical

- Kingfa Sci. & Tech. Co., Ltd.

- Mitsubishi Gas Chemical Company

- Covestro

- Appendix

- Research Methodology

- Report Assumptions

- Acronyms and Abbreviations

|

BASE YEAR |

HISTORICAL DATA |

FORECAST PERIOD |

UNITS |

|||

|

2025 |

|

2020 - 2025 |

2026 - 2033 |

Value: US$ Million |

||

| REPORT FEATURES |

DETAILS |

| Grade |

|

| Application |

|

| Geographical Coverage |

|

| Leading Companies |

|

| Report Highlights |

Key Market Indicators, Macro-micro economic impact analysis, Technological Roadmap, Key Trends, Driver, Restraints, and Future Opportunities & Revenue Pockets, Porter’s 5 Forces Analysis, Historical Trend (2019-2024), Market Estimates and Forecast, Market Dynamics, Industry Trends, Competition Landscape, Category, Region, Country-wise Trends & Analysis, COVID-19 Impact Analysis (Demand and Supply Chain) |