Industrial Power Supply Market Size, Share, and Growth Forecast 2026–2033

Key Market Highlights

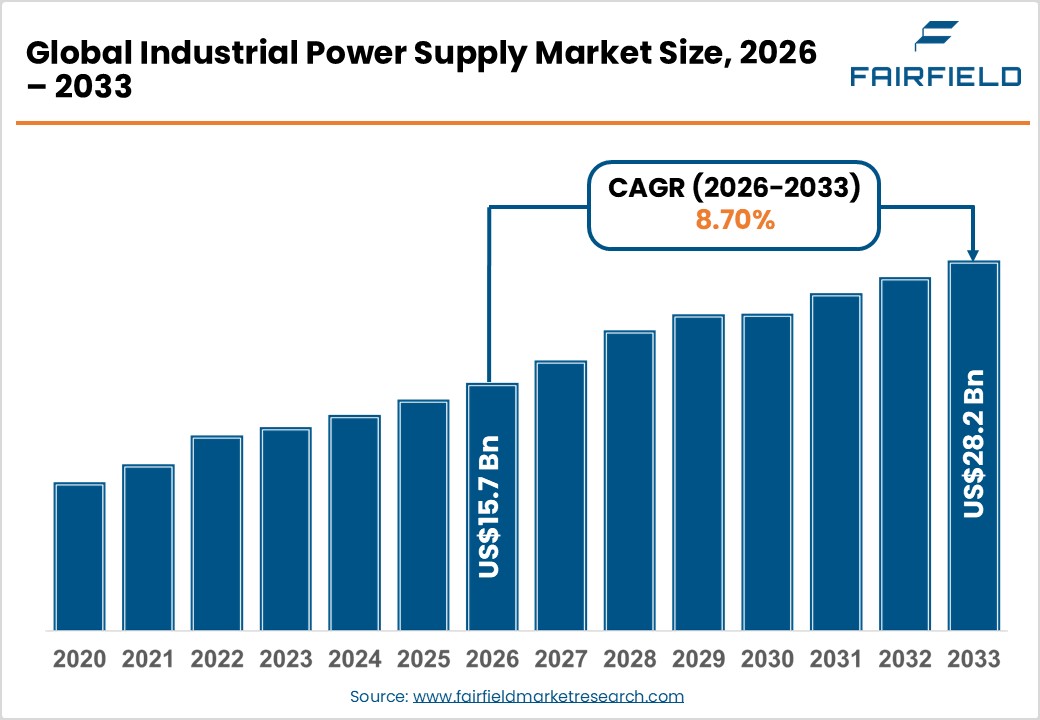

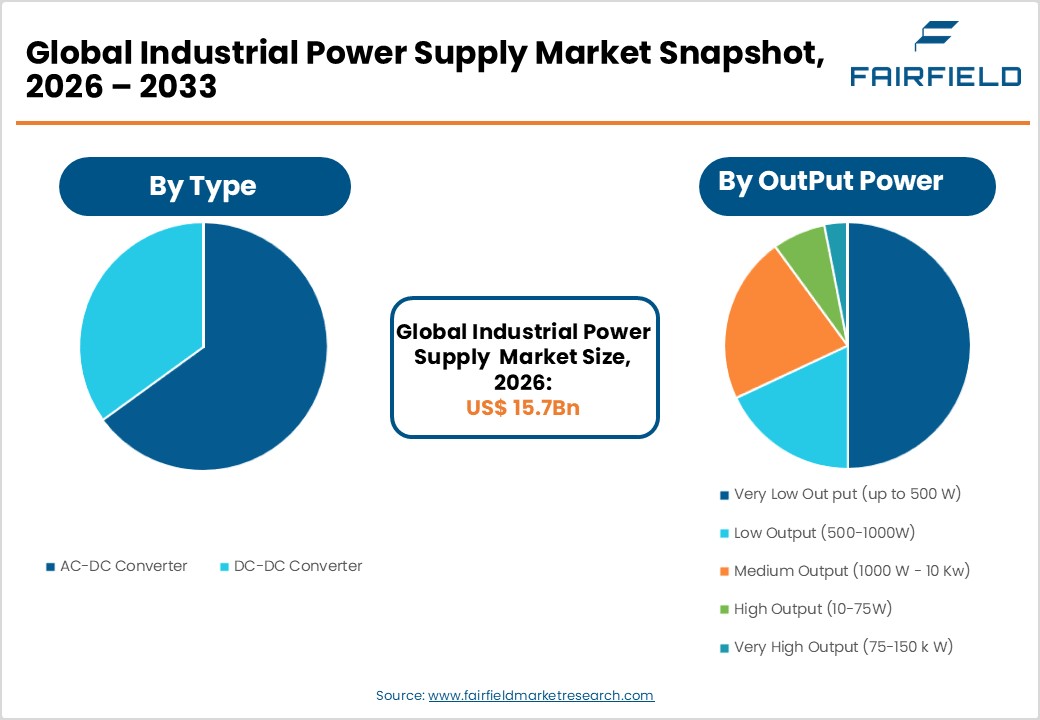

- The global Industrial Power Supply market size is likely to be valued at USD 15.7 Billion in 2026 and is expected to reach USD 28.2 Billion by 2033, growing at a CAGR of 8.70% during the forecast period from 2026 to 2033.

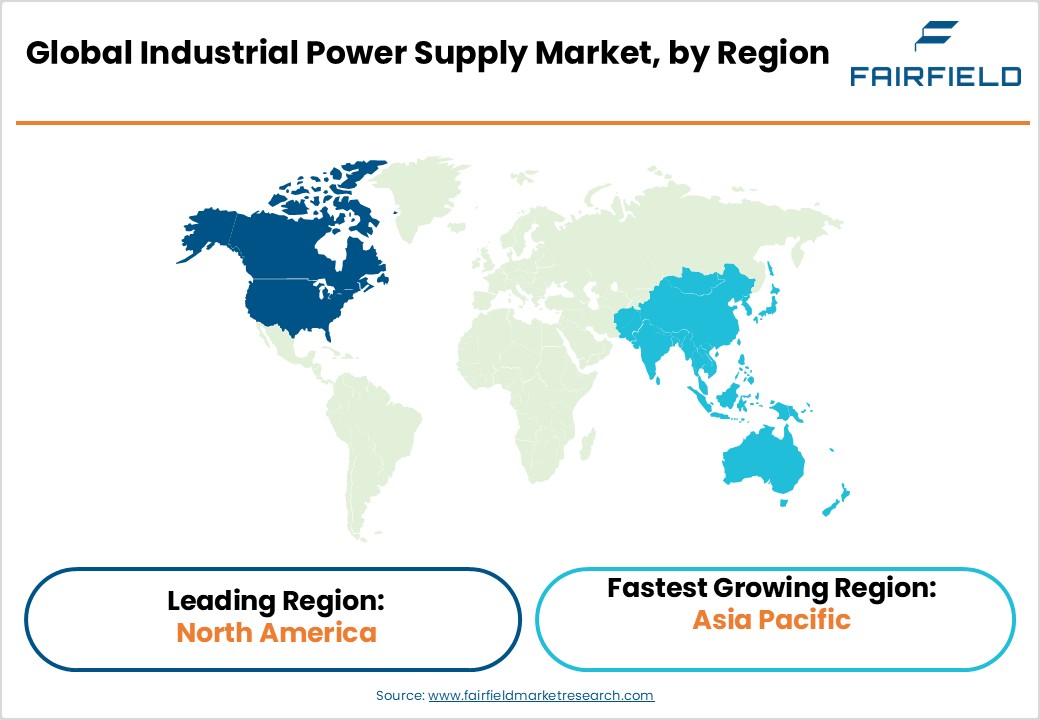

- Leading Region: North America leads the global industrial power supply market, driven by robust demand from semiconductor fabrication, data centers, defense, and EV charging infrastructure, supported by landmark federal investments under the IRA and CHIPS Act.

- Fastest Growing Region: Asia Pacific is the fastest-growing market, with China’s electronics manufacturing dominance, India’s PLI-backed industrial expansion, and ASEAN manufacturing growth accelerating demand through 2033.

- Dominant Segment: The AC–DC Converter segment dominates the by-type category with approximately 62% share, driven by its universal applicability across grid-connected industrial equipment in automation, data centers, and telecommunications verticals.

- Fastest Growing Segment: The Medium Output (1,000 W–10 kW) segment is the dominant and fastest-growing output power category, fueled by expanding smart factory deployments, EV Level 2 charging infrastructure rollout, and mid-range industrial automation investments globally.

- Key Opportunity: Hyperscale data center and edge computing proliferation, driven by AI workloads, represents the foremost market opportunity, requiring high-efficiency power supplies compliant with Open Compute Project (OCP) standards from hyperscale operators.

Market Dynamics

Market Growth Drivers

Rising Adoption of Industrial Automation and Industry 4.0

The global shift toward smart manufacturing and industrial automation is one of the strongest demand catalysts for the industrial power supply market. According to the International Federation of Robotics (IFR), global robot installations reached a record 553,052 units in 2022, with continued expansion projected through the forecast period. Automated production lines, programmable logic controllers (PLCs), servo drives, and collaborative robots all depend on precise, high-efficiency DC power sources. As manufacturers across automotive, electronics, and food & beverages sectors invest in upgrading their production infrastructure, demand for ruggedized, high-density power supply units intensifies. Governments in the U.S., EU, and China have allocated substantial industrial digitalization budgets, further propelling procurement of advanced industrial power conversion equipment.

Expanding Renewable Energy and EV Charging Infrastructure

The global energy transition toward renewables and electrified transportation is generating substantial demand for industrial-grade power supplies. The International Energy Agency (IEA) reported that renewable energy capacity additions hit a record 295 GW globally in 2022, while global EV sales surpassed 10 million units that same year. Power supplies are essential components in solar inverters, wind energy conversion systems, battery energy storage systems (BESS), and EV charging stations. High-power DC–DC and AC–DC converters are increasingly deployed in grid-tied renewable systems and fast-charging EV infrastructure. Government mandates such as the U.S. Inflation Reduction Act and the EU Green Deal are catalyzing multi-billion-dollar investments in clean energy, directly amplifying industrial power supply demand across energy and automotive verticals.

Market Restraints

Supply Chain Disruptions and Component Shortages

The industrial power supply market remains highly vulnerable to global semiconductor and passive component shortages. The COVID-19 pandemic exposed systemic fragilities in the electronics supply chain, and the global semiconductor shortage that began in 2020 continued to impact production schedules well into 2023. Key components such as MOSFETs, IGBTs, capacitors, and inductors faced extended lead times of up to 52 weeks, according to data from the Electronic Components Industry Association (ECIA). These disruptions inflate manufacturing costs, constrain output, and delay product delivery. Small and mid-size power supply manufacturers, lacking the procurement leverage of large OEMs, are disproportionately affected, hampering their ability to scale production in line with rising market demand.

Stringent Regulatory and Energy Efficiency Compliance Requirements

Industrial power supplies are subject to increasingly rigorous international standards covering energy efficiency, electromagnetic compatibility (EMC), and safety certifications. Standards such as the EU Ecodesign Directive (Regulation (EU) 2019/1782), IEC 62368-1, and the U.S. Department of Energy (DOE) Level VI efficiency requirements impose significant compliance costs on manufacturers. Meeting these standards necessitates substantial R&D investment in advanced circuit topologies and thermal management. Certification timelines can delay product launches by 12–18 months, reducing competitiveness for smaller market participants. Frequent updates to regulatory frameworks add an ongoing compliance burden disproportionately affecting companies with limited engineering resources.

Market Opportunities

Proliferation of Data Centers and Edge Computing Infrastructure

The exponential growth of hyperscale data centers and edge computing nodes is creating robust demand for high-efficiency, high-density industrial power supplies. According to the International Energy Agency (IEA), global data center electricity consumption reached approximately 200–250 TWh in 2022, a figure expected to rise sharply with the expansion of AI workloads and cloud computing. Data centers require sophisticated power distribution units (PDUs), AC–DC rectifiers, and DC–DC bus converters meeting stringent efficiency benchmarks (e.g., 80 PLUS Titanium requires ≥96% efficiency at 50% load). Power supply manufacturers delivering high-power-density solutions compliant with Open Compute Project (OCP) standards are well-positioned to secure growing contracts from hyperscale operators such as Amazon Web Services, Microsoft Azure, and Google Cloud, representing a high-value growth opportunity.

Defense Modernization and Aerospace Electrification Programs

Increased defense spending and the electrification of military and aerospace platforms present a compelling growth avenue for specialized industrial power supply manufacturers. Total NATO defense expenditure exceeded USD 1.2 trillion in 2023, with member nations accelerating procurement of next-generation unmanned aerial vehicles (UAVs), electronic warfare systems, and electrified ground vehicles all requiring ruggedized, mission-critical power supplies. The aerospace sector’s shift toward more electric aircraft (MEA) architectures demands advanced AC–DC and DC–DC power conversion systems meeting MIL-STD-704 and DO-160 standards. Companies with proven expertise in high-reliability military-grade power solutions are poised to benefit from this expanding defense and aerospace electrification trend over the forecast period.

Segmental Insights

By Type Analysis

The AC–DC Converter segment dominates the industrial power supply market by type, accounting for approximately 62% of total market revenue. AC–DC converters serve as the primary interface between utility power grids and industrial equipment, converting alternating current from the grid into regulated direct current required by electronic systems and machinery. Their widespread adoption is driven by the ubiquity of AC mains power distribution in industrial facilities worldwide. Sectors such as telecommunications, data centers, manufacturing automation, and medical equipment rely heavily on AC–DC power supplies for reliable, regulated power delivery. Advances in power factor correction (PFC) topology and GaN (Gallium Nitride) semiconductor technology are further improving efficiency and reducing form factors, reinforcing this segment’s leadership position.

By Output Power Analysis

The Medium Output (1,000 W–10 kW) segment leads the industrial power supply market by output power, representing approximately 38% of total market share. This power range optimally aligns with the requirements of the broadest array of industrial applications, including CNC machining centers, robotic systems, laboratory test equipment, industrial 3D printers, and battery test systems. Medium-output power supplies strike an ideal balance between power density, thermal management complexity, and cost efficiency making them the preferred choice for OEMs designing mid-range industrial equipment. The expansion of smart factory deployments and Industry 4.0-driven automation investments has significantly elevated demand. Growth in EV charging infrastructure (particularly Level 2 chargers) and renewable energy storage systems further reinforces the dominance of this output power segment.

By Vertical Analysis

The Semiconductor vertical leads the industrial power supply market by end-use application, contributing approximately 18% of total revenue share. Semiconductor fabrication processes are among the most power-intensive industrial applications, relying on ultra-stable, high-precision DC power sources for ion implantation, chemical vapor deposition (CVD), atomic layer deposition (ALD), and plasma etching equipment. The global semiconductor industry’s relentless capacity expansion driven by the CHIPS and Science Act in the U.S. allocating USD 52.7 billion for domestic chip manufacturing is fueling new fab construction. Taiwan Semiconductor Manufacturing Company (TSMC), Samsung Electronics, and Intel have announced combined capacity investment plans exceeding USD 300 billion through 2030, all requiring precision industrial power supply infrastructure.

Regional Insights

North America Industrial Power Supply Trends

North America maintains a dominating position in the global industrial power supply market, with the United States serving as the primary growth engine. The region benefits from robust demand across defense, semiconductor, data center, and EV charging verticals. Federal investments under the Inflation Reduction Act (IRA) and the CHIPS and Science Act have catalyzed unprecedented capital expenditure in clean energy and advanced manufacturing, generating sustained demand for high-quality industrial power conversion systems.

The U.S. Department of Energy (DOE)’s energy efficiency standards and ENERGY STAR certification programs continue to push manufacturers toward higher-efficiency power solutions, spurring product innovation. Major industrial power supply manufacturers including Emerson Electric Co. and ABB Ltd. maintain strong North American operations and distribution networks, further reinforcing the region’s competitive position in delivering advanced power supply solutions across key industrial end-markets.

Europe Industrial Power Supply Trends

Europe represents a mature yet strategically significant market for industrial power supplies, driven by stringent energy efficiency mandates and the continent’s ambitious industrial decarbonization agenda. The EU Green Deal and the REPowerEU plan are accelerating renewable energy deployment, creating new demand for power conversion systems in wind, solar, and grid storage applications. Germany remains the region’s largest market, anchored by its world-class automotive, machinery, and robotics industries, which are voracious consumers of industrial power supply equipment.

The UK, France, and Spain are notable growth contributors, with increasing investments in EV charging infrastructure and defense modernization programs. Regulatory harmonization under the EU Ecodesign Directive and the EN 61000-3-2 EMC standard ensures that products meeting European specifications command a quality premium, favoring established suppliers such as Siemens AG, Schneider Electric SE, and Phoenix Contact GmbH & Co. KG.

Asia Pacific Industrial Power Supply Trends

Asia Pacific is the fastest-growing regional market for industrial power supplies, propelled by China’s dominant electronics manufacturing base, Japan’s robotics and automotive sectors, and India’s rapidly expanding industrial and infrastructure investments. China alone accounts for over 35% of global electronics manufacturing output, according to data from the World Trade Organization (WTO), generating enormous demand for AC–DC and DC–DC power supplies across consumer electronics, telecommunications, and industrial automation verticals.

India’s Production Linked Incentive (PLI) schemes for electronics, pharmaceuticals, and solar energy manufacturing, combined with the National Infrastructure Pipeline (NIP) allocating USD 1.4 trillion for infrastructure development, are creating new demand pockets for industrial power supplies. ASEAN nations particularly Vietnam, Thailand, and Malaysia are emerging as alternative manufacturing hubs, further amplifying regional power supply consumption as production capacity scales through the forecast period.

Competitive Landscape

Market Structure Analysis

The global industrial power supply market exhibits a moderately consolidated structure, with a blend of multinational corporations and specialized niche players competing across different power ranges and verticals. Leading companies such as ABB Ltd., Siemens AG, Schneider Electric SE, and Delta Electronics, Inc. leverage extensive global distribution networks, broad product portfolios, and strong R&D capabilities to maintain competitive advantage. Key strategies include portfolio expansion through modular and configurable power supply platforms, strategic acquisitions to enter adjacent markets, and heavy investment in GaN (Gallium Nitride) and SiC (Silicon Carbide) semiconductor-based power conversion technology. Growing emphasis on digitally connected power supplies with remote monitoring and predictive maintenance capabilities is emerging as a critical competitive differentiator in the Industry 4.0 era.

Key Market Developments

- March 2025: ABB Ltd. launched its next-generation CP-S series industrial power supplies with integrated digital monitoring capabilities, targeting smart factory and Industry 4.0 applications across manufacturing and robotics sectors.

- January 2025: Schneider Electric SE announced a strategic partnership with a leading battery energy storage system (BESS) integrator to co-develop high-power AC–DC conversion solutions for grid-scale renewable energy storage, reinforcing its position in the clean energy vertical.

- September 2024: Delta Electronics, Inc. unveiled its DIN rail power supply lineup featuring SiC-based topology, achieving efficiency ratings of up to 96.5%, setting a new benchmark for industrial power density and thermal performance.

Companies Covered in Industrial Power Supply Market

- ABB Ltd.

- Siemens AG

- Schneider Electric SE

- Emerson Electric Co.

- Rockwell Automation, Inc.

- Mitsubishi Electric Corporation

- Delta Electronics, Inc.

- Mean Well Enterprises Co., Ltd.

- TDK Lambda (TDK Corporation)

- Phoenix Contact GmbH & Co. KG

- Panasonic Corporation

- Toshiba Corporation

- Murata Manufacturing Co., Ltd.

- Infineon Technologies AG

- Bel Fuse Inc.

- Cosel Co., Ltd.

- SL Power Electronics Corporation

- Vicor Corporation

Market Segmentation

By Type

- AC–DC Converter

- DC–DC Converter

By Output Power

- Very Low Output (up to 500 W)

- Low Output (500–1,000 W)

- Medium Output (1,000 W–10 kW)

- High Output (10–75 kW)

- Very High Output (75–150 kW)

By Vertical

- Transportation

- Semiconductor

- Military & Aerospace

- Robotics

- Test & Measurement

- Industrial 3D Printing

- Battery Charging & Test

- Laser

- Lighting

- Telecommunications

- Consumer Electronics

- Automotive

- Energy

- Food & Beverages

- Medical & Healthcare

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Executive Summary

- Global Industrial Power Supply Market Snapshot

- Future Projections

- Key Market Trends

- Regional Snapshot, by Value, 2026

- Analyst Recommendations

- Market Overview

- Market Definitions and Segmentations

- Market Dynamics

- Drivers

- Restraints

- Market Opportunities

- Value Chain Analysis

- COVID-19 Impact Analysis

- Porter's Five Forces Analysis

- Impact of Russia-Ukraine Conflict

- PESTLE Analysis

- Regulatory Analysis

- Price Trend Analysis

- Current Prices and Future Projections, 2025-2033

- Price Impact Factors

- Global Industrial Power Supply Market Outlook, 2020 - 2033

- Global Industrial Power Supply Market Outlook, by Type, Value (US$ Bn), 2020-2033

- AC-DC Converter

- DC-DC Converter

- Global Industrial Power Supply Market Outlook, by Out Put Power, Value (US$ Bn), 2020-2033

- Very low output (up to 500 W)

- Low output (500−1,000 W)

- Medium output (1,000 W−10 kW)

- High output (10−75 kW)

- Very high output (75−150 kW)

- Global Industrial Power Supply Market Outlook, by Vertical, Value (US$ Bn), 2020-2033

- Medical and Healthcare

- Semiconductor

- Military & Aerospace

- Robotics

- Test & Measurement

- Industrial 3-D Printing

- Battery Charging & Test

- Laser

- Lighting

- Telecommunications

- Global Industrial Power Supply Market Outlook, by Region, Value (US$ Bn), 2020-2033

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Global Industrial Power Supply Market Outlook, by Type, Value (US$ Bn), 2020-2033

- North America Industrial Power Supply Market Outlook, 2020 - 2033

- North America Industrial Power Supply Market Outlook, by Type, Value (US$ Bn), 2020-2033

- AC-DC Converter

- DC-DC Converter

- North America Industrial Power Supply Market Outlook, by Out Put Power, Value (US$ Bn), 2020-2033

- Very low output (up to 500 W)

- Low output (500−1,000 W)

- Medium output (1,000 W−10 kW)

- High output (10−75 kW)

- Very high output (75−150 kW)

- North America Industrial Power Supply Market Outlook, by Vertical, Value (US$ Bn), 2020-2033

- Medical and Healthcare

- Semiconductor

- Military & Aerospace

- Robotics

- Test & Measurement

- Industrial 3-D Printing

- Battery Charging & Test

- Laser

- Lighting

- Telecommunications

- North America Industrial Power Supply Market Outlook, by Country, Value (US$ Bn), 2020-2033

- U.S. Industrial Power Supply Market Outlook, by Type, 2020-2033

- U.S. Industrial Power Supply Market Outlook, by Out Put Power, 2020-2033

- U.S. Industrial Power Supply Market Outlook, by Vertical, 2020-2033

- Canada Industrial Power Supply Market Outlook, by Type, 2020-2033

- Canada Industrial Power Supply Market Outlook, by Out Put Power, 2020-2033

- Canada Industrial Power Supply Market Outlook, by Vertical, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- North America Industrial Power Supply Market Outlook, by Type, Value (US$ Bn), 2020-2033

- Europe Industrial Power Supply Market Outlook, 2020 - 2033

- Europe Industrial Power Supply Market Outlook, by Type, Value (US$ Bn), 2020-2033

- AC-DC Converter

- DC-DC Converter

- Europe Industrial Power Supply Market Outlook, by Out Put Power, Value (US$ Bn), 2020-2033

- Very low output (up to 500 W)

- Low output (500−1,000 W)

- Medium output (1,000 W−10 kW)

- High output (10−75 kW)

- Very high output (75−150 kW)

- Europe Industrial Power Supply Market Outlook, by Vertical, Value (US$ Bn), 2020-2033

- Medical and Healthcare

- Semiconductor

- Military & Aerospace

- Robotics

- Test & Measurement

- Industrial 3-D Printing

- Battery Charging & Test

- Laser

- Lighting

- Telecommunications

- Europe Industrial Power Supply Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Germany Industrial Power Supply Market Outlook, by Type, 2020-2033

- Germany Industrial Power Supply Market Outlook, by Out Put Power, 2020-2033

- Germany Industrial Power Supply Market Outlook, by Vertical, 2020-2033

- Italy Industrial Power Supply Market Outlook, by Type, 2020-2033

- Italy Industrial Power Supply Market Outlook, by Out Put Power, 2020-2033

- Italy Industrial Power Supply Market Outlook, by Vertical, 2020-2033

- France Industrial Power Supply Market Outlook, by Type, 2020-2033

- France Industrial Power Supply Market Outlook, by Out Put Power, 2020-2033

- France Industrial Power Supply Market Outlook, by Vertical, 2020-2033

- U.K. Industrial Power Supply Market Outlook, by Type, 2020-2033

- U.K. Industrial Power Supply Market Outlook, by Out Put Power, 2020-2033

- U.K. Industrial Power Supply Market Outlook, by Vertical, 2020-2033

- Spain Industrial Power Supply Market Outlook, by Type, 2020-2033

- Spain Industrial Power Supply Market Outlook, by Out Put Power, 2020-2033

- Spain Industrial Power Supply Market Outlook, by Vertical, 2020-2033

- Russia Industrial Power Supply Market Outlook, by Type, 2020-2033

- Russia Industrial Power Supply Market Outlook, by Out Put Power, 2020-2033

- Russia Industrial Power Supply Market Outlook, by Vertical, 2020-2033

- Rest of Europe Industrial Power Supply Market Outlook, by Type, 2020-2033

- Rest of Europe Industrial Power Supply Market Outlook, by Out Put Power, 2020-2033

- Rest of Europe Industrial Power Supply Market Outlook, by Vertical, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Europe Industrial Power Supply Market Outlook, by Type, Value (US$ Bn), 2020-2033

- Asia Pacific Industrial Power Supply Market Outlook, 2020 - 2033

- Asia Pacific Industrial Power Supply Market Outlook, by Type, Value (US$ Bn), 2020-2033

- AC-DC Converter

- DC-DC Converter

- Asia Pacific Industrial Power Supply Market Outlook, by Out Put Power, Value (US$ Bn), 2020-2033

- Very low output (up to 500 W)

- Low output (500−1,000 W)

- Medium output (1,000 W−10 kW)

- High output (10−75 kW)

- Very high output (75−150 kW)

- Asia Pacific Industrial Power Supply Market Outlook, by Vertical, Value (US$ Bn), 2020-2033

- Medical and Healthcare

- Semiconductor

- Military & Aerospace

- Robotics

- Test & Measurement

- Industrial 3-D Printing

- Battery Charging & Test

- Laser

- Lighting

- Telecommunications

- Asia Pacific Industrial Power Supply Market Outlook, by Country, Value (US$ Bn), 2020-2033

- China Industrial Power Supply Market Outlook, by Type, 2020-2033

- China Industrial Power Supply Market Outlook, by Out Put Power, 2020-2033

- China Industrial Power Supply Market Outlook, by Vertical, 2020-2033

- Japan Industrial Power Supply Market Outlook, by Type, 2020-2033

- Japan Industrial Power Supply Market Outlook, by Out Put Power, 2020-2033

- Japan Industrial Power Supply Market Outlook, by Vertical, 2020-2033

- South Korea Industrial Power Supply Market Outlook, by Type, 2020-2033

- South Korea Industrial Power Supply Market Outlook, by Out Put Power, 2020-2033

- South Korea Industrial Power Supply Market Outlook, by Vertical, 2020-2033

- India Industrial Power Supply Market Outlook, by Type, 2020-2033

- India Industrial Power Supply Market Outlook, by Out Put Power, 2020-2033

- India Industrial Power Supply Market Outlook, by Vertical, 2020-2033

- Southeast Asia Industrial Power Supply Market Outlook, by Type, 2020-2033

- Southeast Asia Industrial Power Supply Market Outlook, by Out Put Power, 2020-2033

- Southeast Asia Industrial Power Supply Market Outlook, by Vertical, 2020-2033

- Rest of SAO Industrial Power Supply Market Outlook, by Type, 2020-2033

- Rest of SAO Industrial Power Supply Market Outlook, by Out Put Power, 2020-2033

- Rest of SAO Industrial Power Supply Market Outlook, by Vertical, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Asia Pacific Industrial Power Supply Market Outlook, by Type, Value (US$ Bn), 2020-2033

- Latin America Industrial Power Supply Market Outlook, 2020 - 2033

- Latin America Industrial Power Supply Market Outlook, by Type, Value (US$ Bn), 2020-2033

- AC-DC Converter

- DC-DC Converter

- Latin America Industrial Power Supply Market Outlook, by Out Put Power, Value (US$ Bn), 2020-2033

- Very low output (up to 500 W)

- Low output (500−1,000 W)

- Medium output (1,000 W−10 kW)

- High output (10−75 kW)

- Very high output (75−150 kW)

- Latin America Industrial Power Supply Market Outlook, by Vertical, Value (US$ Bn), 2020-2033

- Medical and Healthcare

- Semiconductor

- Military & Aerospace

- Robotics

- Test & Measurement

- Industrial 3-D Printing

- Battery Charging & Test

- Laser

- Lighting

- Telecommunications

- Latin America Industrial Power Supply Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Brazil Industrial Power Supply Market Outlook, by Type, 2020-2033

- Brazil Industrial Power Supply Market Outlook, by Out Put Power, 2020-2033

- Brazil Industrial Power Supply Market Outlook, by Vertical, 2020-2033

- Mexico Industrial Power Supply Market Outlook, by Type, 2020-2033

- Mexico Industrial Power Supply Market Outlook, by Out Put Power, 2020-2033

- Mexico Industrial Power Supply Market Outlook, by Vertical, 2020-2033

- Argentina Industrial Power Supply Market Outlook, by Type, 2020-2033

- Argentina Industrial Power Supply Market Outlook, by Out Put Power, 2020-2033

- Argentina Industrial Power Supply Market Outlook, by Vertical, 2020-2033

- Rest of LATAM Industrial Power Supply Market Outlook, by Type, 2020-2033

- Rest of LATAM Industrial Power Supply Market Outlook, by Out Put Power, 2020-2033

- Rest of LATAM Industrial Power Supply Market Outlook, by Vertical, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Latin America Industrial Power Supply Market Outlook, by Type, Value (US$ Bn), 2020-2033

- Middle East & Africa Industrial Power Supply Market Outlook, 2020 - 2033

- Middle East & Africa Industrial Power Supply Market Outlook, by Type, Value (US$ Bn), 2020-2033

- AC-DC Converter

- DC-DC Converter

- Middle East & Africa Industrial Power Supply Market Outlook, by Out Put Power, Value (US$ Bn), 2020-2033

- Very low output (up to 500 W)

- Low output (500−1,000 W)

- Medium output (1,000 W−10 kW)

- High output (10−75 kW)

- Very high output (75−150 kW)

- Middle East & Africa Industrial Power Supply Market Outlook, by Vertical, Value (US$ Bn), 2020-2033

- Medical and Healthcare

- Semiconductor

- Military & Aerospace

- Robotics

- Test & Measurement

- Industrial 3-D Printing

- Battery Charging & Test

- Laser

- Lighting

- Telecommunications

- Middle East & Africa Industrial Power Supply Market Outlook, by Country, Value (US$ Bn), 2020-2033

- GCC Industrial Power Supply Market Outlook, by Type, 2020-2033

- GCC Industrial Power Supply Market Outlook, by Out Put Power, 2020-2033

- GCC Industrial Power Supply Market Outlook, by Vertical, 2020-2033

- South Africa Industrial Power Supply Market Outlook, by Type, 2020-2033

- South Africa Industrial Power Supply Market Outlook, by Out Put Power, 2020-2033

- South Africa Industrial Power Supply Market Outlook, by Vertical, 2020-2033

- Egypt Industrial Power Supply Market Outlook, by Type, 2020-2033

- Egypt Industrial Power Supply Market Outlook, by Out Put Power, 2020-2033

- Egypt Industrial Power Supply Market Outlook, by Vertical, 2020-2033

- Nigeria Industrial Power Supply Market Outlook, by Type, 2020-2033

- Nigeria Industrial Power Supply Market Outlook, by Out Put Power, 2020-2033

- Nigeria Industrial Power Supply Market Outlook, by Vertical, 2020-2033

- Rest of Middle East Industrial Power Supply Market Outlook, by Type, 2020-2033

- Rest of Middle East Industrial Power Supply Market Outlook, by Out Put Power, 2020-2033

- Rest of Middle East Industrial Power Supply Market Outlook, by Vertical, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Middle East & Africa Industrial Power Supply Market Outlook, by Type, Value (US$ Bn), 2020-2033

- Competitive Landscape

- Company Vs Segment Heatmap

- Company Market Share Analysis, 2025

- Competitive Dashboard

- Company Profiles

- ABB Ltd.

- Company Overview

- Product Portfolio

- Financial Overview

- Business Strategies and Developments

- Siemens AG

- Schneider Electric SE

- Emerson Electric Co

- Rockwell Automation, Inc.

- Mitsubishi Electric Corporation

- Mitsubishi Electric Corporation

- Delta Electronics, Inc.

- Mean Well Enterprises Co., Ltd.

- TDK Lambda (TDK Corporation)

- Phoenix Contact GmbH & Co. KG

- Panasonic Corporation

- Toshiba Corporation

- Delta Electronic, Inc.

- Murata Manufacturing Co., Ltd.

- ABB Ltd.

- Appendix

- Research Methodology

- Report Assumptions

- Acronyms and Abbreviations

|

BASE YEAR |

HISTORICAL DATA |

FORECAST PERIOD |

UNITS |

|||

|

2025 |

|

2020 - 2025 |

2026 - 2033 |

Value: US$ Million |

||

|

REPORT FEATURES |

DETAILS |

|

By Type |

|

|

By Output power |

|

|

By Vertical |

|

|

Geographical Coverage |

|

|

Leading Companies |

|

|

Report Highlights |

Key Market Indicators, Macro-micro economic impact analysis, Technological Roadmap, Key Trends, Driver, Restraints, and Future Opportunities & Revenue Pockets, Porter’s 5 Forces Analysis, Historical Trend (2019-2024), Market Estimates and Forecast, Market Dynamics, Industry Trends, Competition Landscape, Category, Region, Country-wise Trends & Analysis, COVID-19 Impact Analysis (Demand and Supply Chain) |