Boiler Control Market Size, Share, and Growth Forecast 2026 – 2033

Key Market Highlights

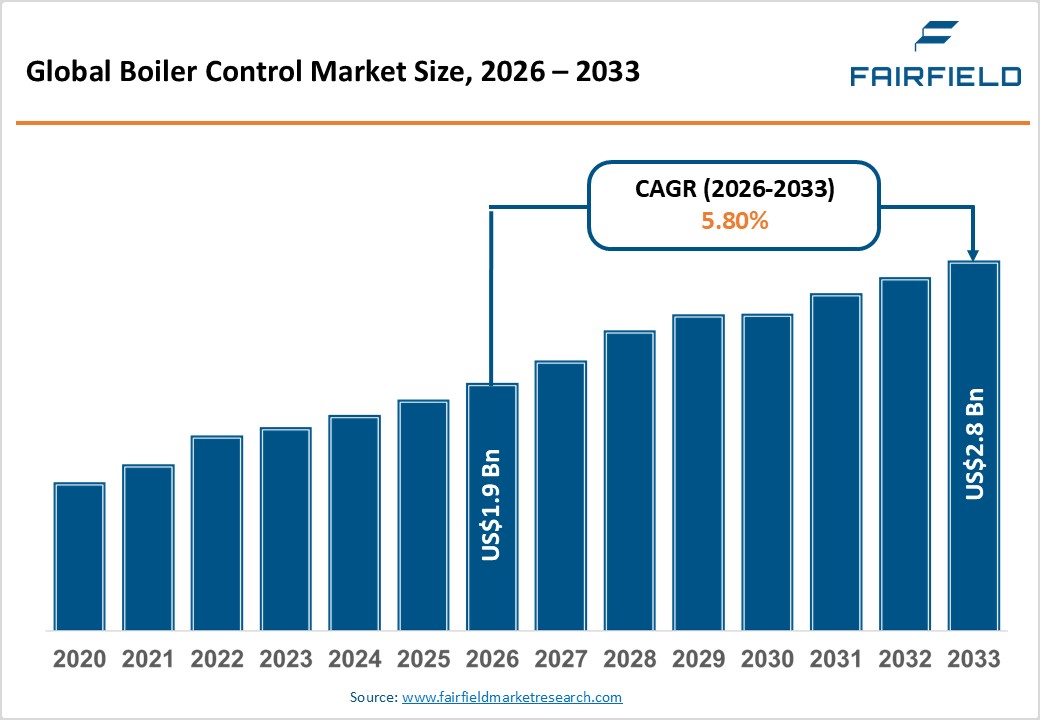

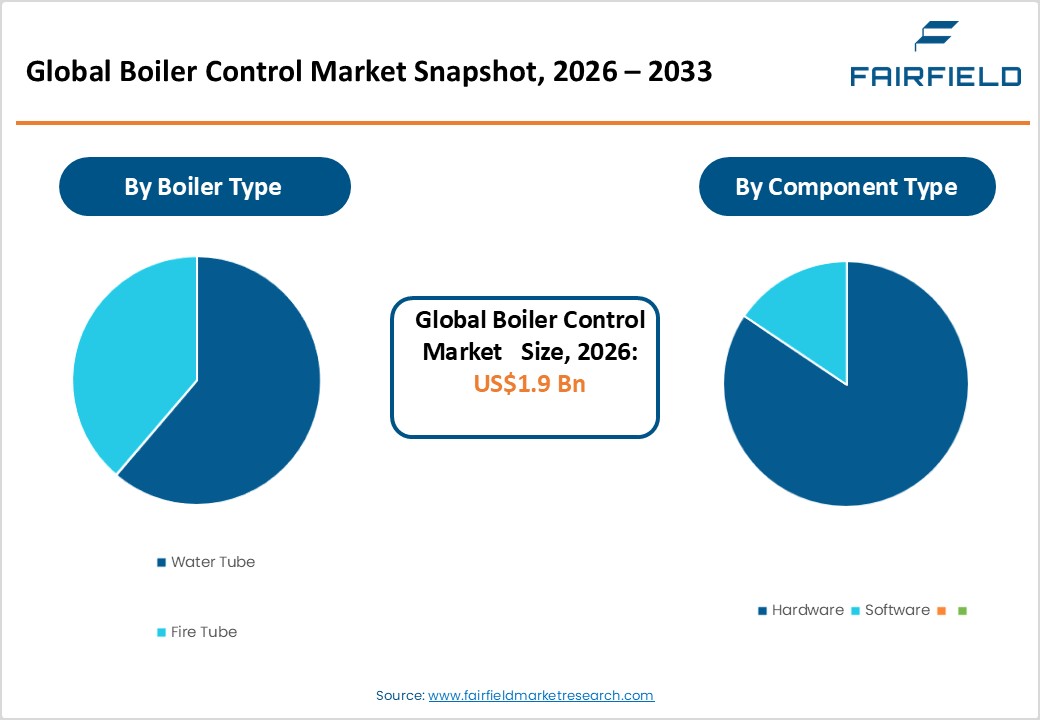

- The global Boiler Control Market size is likely to be valued at US$ 1.9 Billion in 2026 and is expected to reach US$ 2.8 Billion by 2033, growing at a CAGR of 5.80% during the forecast period from 2026 to 2033.

- Leading Region: North America leads the Boiler Control Market, supported by stringent EPA and DOE efficiency mandates, a mature industrial infrastructure, and presence of major players like Honeywell and Emerson Electric

- Fastest Growing Region: Asia Pacific is the fastest growing region, driven by China's Dual Carbon Goals, India's PAT scheme, and rapid industrial automation investments across manufacturing hubs in ASEAN

- Dominant Segment: The Industrial end-user segment dominates with ~61% share, fueled by energy-intensive sectors including chemicals, oil & gas, and food processing requiring sophisticated multi-boiler control solutions.

- Fastest Growing Segment: The Software component segment is the fastest growing, with cloud-based boiler management platforms, AI analytics, and SaaS-based predictive maintenance services gaining rapid adoption across global industrial operators.

- Key Market Opportunity: Integration of AI-powered predictive maintenance and digital twin boiler management presents the highest-potential opportunity, with platforms like Honeywell Forge and ABB Ability™ demonstrating up to 30% reduction in unplanned downtime.

Market Dynamics

Market Growth Drivers

Tightening Global Energy Efficiency Regulations Compelling Boiler Upgrades

One of the most tangible real-world forces propelling the boiler control market is the wave of legislated energy efficiency mandates across major economies. In the European Union, the Energy Efficiency Directive (EED) revised in 2023 sets binding national energy-saving targets, effectively phasing out older uncontrolled boiler systems. The U.K. government's Boiler Upgrade Scheme actively incentivizes replacement of outdated boiler installations with modern, controlled heat pump and condensing boiler systems. In the United States, the U.S. Department of Energy (DOE) mandated minimum annual fuel utilization efficiency (AFUE) for residential gas furnaces, pushing boiler manufacturers and end-users toward advanced control upgrades to meet compliance. These binding standards directly translate into procurement of high-precision modulating controls, O2 trim systems, and programmable logic controllers across commercial and industrial boiler installations worldwide.

Industrial Automation and Industry 4.0 Driving Demand for Smart Boiler Controls

The global acceleration of Industry 4.0 and smart factory initiatives is creating significant demand for intelligent boiler control solutions integrated with plant-wide automation architectures. A striking, the deployment of Siemens AG's SIMATIC control systems across petrochemical and food processing plants in Germany and South Korea, where boiler management is seamlessly integrated with enterprise-level SCADA and MES platforms. According to the International Energy Agency (IEA), industrial boilers consume a significant share of total industrial energy consumption in manufacturing-intensive economies. The International Federation of Robotics (IFR) highlighted the rapid rise in industrial robot installations globally, signalling the broader automation wave that is naturally pulling boiler monitoring, sequencing, and combustion efficiency controls into the connected factory ecosystem.

Market Restraints

High Capital Investment and Retrofitting Costs Limiting Adoption Among SMEs

Despite clear long-term efficiency gains, the significant upfront capital expenditure associated with advanced boiler control systems remains a critical barrier, particularly for small and medium-sized enterprises (SMEs). A real-world illustration is the challenge faced by mid-sized textile and food processing manufacturers, where a complete boiler control upgrade including programmable logic controllers, variable frequency drives, and remote monitoring hardware represents a substantial investment per installation. The International Finance Corporation (IFC) notes that energy efficiency financing gaps in emerging markets leave many smaller operators unable to self-fund modernization. This financial friction slows adoption in price-sensitive markets and restrains overall market penetration.

Shortage of Skilled Technical Workforce for Advanced Boiler Control Systems

The deployment and maintenance of modern boiler control systems particularly AI-driven predictive control and IoT-integrated platforms demand highly specialized engineering expertise that remains in short supply globally. In the United Kingdom, industry reports highlight a shortfall of engineering professionals required to meet demand. Utilities and industrial operators face particular challenges in sourcing qualified technicians capable of commissioning and servicing digital combustion management systems. This talent deficit increases operational risk, prolongs system downtime, and often results in suboptimal utilization of installed boiler control capabilities collectively acting as a drag on market expansion in technically underserved geographies.

Market Opportunities

AI-Enabled Predictive Maintenance and Digital Twin Integration Unlocking New Revenue Streams

The convergence of Artificial Intelligence (AI), machine learning, and digital twin technology presents a transformative opportunity for boiler control market participants. A landmark real-world case in point is Honeywell International Inc.'s Forge Industrial platform, commercially deployed across refinery and petrochemical clients, which uses AI analytics on boiler sensor data to predict failures in advance and reduce unplanned downtime. Similarly, ABB Ltd.'s ABB Ability™ Boiler Advisor uses real-time digital twin simulations to optimize combustion efficiency and reduce NOx emissions. As industries globally shift from reactive to proactive maintenance models, AI-powered boiler control platforms are positioned to capture significant incremental market value

Rapid Expansion of District Heating Networks Creating Substantial Demand in Europe and Asia

The global expansion of district heating networks (DHN) a major driver of low-carbon urban heat infrastructure is creating a high-growth opportunity for centralized boiler control system providers. China operates the world's largest district heating network, covering over 14.4 billion square meters of floor space as of 2023, with the government's 14th Five-Year Plan committing to further DHN expansion as part of its carbon neutrality strategy. In Europe, Denmark, Sweden, and Finland where district heating supplies a major share of residential heat demand are actively retrofitting heat network central plants with advanced modulating boiler control systems to integrate renewable heat sources. The European Heat Pump Association (EHPA) noted substantial growth in large heat pump installations connected to district networks, requiring sophisticated hybrid boiler–heat pump control logic. Companies offering integrated control platforms for such hybrid DHN infrastructure are uniquely positioned to capitalize on this structural shift in urban energy infrastructure.

Segmental Insights

Boiler Type Analysis

The fire tube boiler segment holds the dominant position in the Boiler Control Market, accounting for approximately 58% of the total market share. Fire tube boilers are widely preferred in commercial and light industrial applications owing to their simpler construction, lower initial investment, and ease of operation and maintenance. Real-world adoption is particularly strong across food and beverage processing, hospitality, and pharmaceutical manufacturing sectors, where steam loads are moderate and consistent. According to the U.S. Energy Information Administration (EIA), commercial buildings account for a significant share of total U.S. energy consumption, with space heating and process steam representing a substantial fraction underpinning steady demand for fire tube boiler control systems. The segment benefits from extensive installed base and ongoing retrofitting programs for energy efficiency compliance.

Control Type Analysis

The modulating control segment leads the Control Type category, commanding approximately 63% of total market share in 2026. Unlike on/off controls that operate at binary states, modulating controls continuously vary the burner firing rate to match actual heat demand delivering superior fuel efficiency, reduced thermal cycling, and longer equipment lifeA compelling real-world endorsement is the U.K. Carbon Trust's findings that modulating boiler controls can reduce fuel consumption compared to on/off systems in commercial buildings. The surge in green building certifications such as LEED and BREEAM which explicitly reward modulating control adoption further reinforces segment leadership. As energy benchmarking and ESG reporting requirements intensify across sectors globally, modulating controls will continue to outpace on/off alternatives.

Component Analysis

The hardware segment currently holds the leading position in the Component category, representing approximately 66% of the total boiler control market. Hardware components including programmable logic controllers (PLCs), sensors, actuators, burner management systems (BMS), and human-machine interfaces (HMI) form the physical backbone of every boiler control installation. The dominance of hardware is supported by the large installed base of legacy industrial boilers worldwide requiring physical control upgrades. The International Energy Agency (IEA) estimates that a substantial portion of installed industrial boilers globally are outdated, representing a significant hardware replacement and retrofit opportunity. However, the software segment is gaining momentum with the growth of cloud-based boiler management platforms and digital services.

End-User Analysis

The industrial end-user segment dominates the Boiler Control Market with an estimated share of approximately 61% in 2026. Industries such as chemicals, oil & gas, paper & pulp, food processing, and textile manufacturing are major consumers of process steam and hot water, requiring sophisticated multi-boiler sequencing and combustion optimization controls. BASF SE's Ludwigshafen complex, one of the world's largest integrated chemical production sites, relies on an intricate network of steam boilers managed by centralized control systems to maintain continuous process operations. This underscores the enormous energy management mandate that industrial boiler control systems are addressing.

Regional Insights

North America Boiler Control Market Trends

North America holds a leading position in the global Boiler Control Market, driven by a mature industrial base, strong regulatory framework, and significant technology innovation activity. In the United States, the Environmental Protection Agency (EPA)'s National Emission Standards for Hazardous Air Pollutants (NESHAP) for industrial boilers codified under the Boiler MACT Rule continue to drive comprehensive boiler control upgrades across major industrial sectors. The U.S. Department of Energy's Industrial Assessment Centers (IACs) program has conducted over 17,000 industrial energy audits, consistently identifying boiler optimization as among the top energy-saving opportunities.

The Canadian market is similarly influenced by provincial energy efficiency programs, with Natural Resources Canada reporting that industrial and commercial heating systems account for a significant share of Canada's total energy use. Leading boiler control technology companies including Honeywell International Inc., Emerson Electric Co., and Rockwell Automation, Inc. maintain significant R&D and manufacturing presence in the region, reinforcing North America's role as a global innovation hub for advanced combustion management and predictive boiler control solutions.

Europe Boiler Control Market Trends

Europe represents a major and highly regulated market for boiler controls, with the region's aggressive decarbonization agenda acting as a powerful catalyst. The European Green Deal and the Fit for 55 package targeting a 55% reduction in greenhouse gas emissions by 2030 are compelling industrial operators and building managers across Germany, France, U.K., and Spain to upgrade existing boiler fleets with precision control systems that minimize fuel consumption and emissions. Germany, as Europe's largest industrial economy, has introduced the Energieeffizienzgesetz (Energy Efficiency Act) in 2023, mandating energy audits and efficiency improvements for large energy consumers.

In the U.K., the Heat and Buildings Strategy outlines the government's roadmap to phase out new gas boiler installations, driving significant near-term demand for sophisticated hybrid heat pump–boiler control systems. France's MaPrimeRénov' scheme supports energy renovation grants, stimulating commercial and residential boiler modernization. Siemens AG, Schneider Electric SE, and Bosch Thermotechnology remain pivotal players advancing smart boiler integration with building energy management systems across the continent.

Asia Pacific Boiler Control Market Trends

Asia Pacific is the fastest growing regional market for boiler controls, propelled by rapid industrialization, expanding manufacturing capacity, and large-scale urban infrastructure development across China, India, Japan, and ASEAN nations. China the world's largest industrial energy consumer is investing heavily in boiler system modernization as part of its Dual Carbon Goals: achieving carbon peaking by 2030 and carbon neutrality by 2060. The China Ministry of Industry and Information Technology (MIIT) has listed boiler energy efficiency as a priority area under its industrial green development action plan.

In India, the Bureau of Energy Efficiency (BEE)'s PAT (Perform, Achieve and Trade) scheme has designated the boiler and steam system sector as a critical focus area, with over 800 industrial units mandated to achieve energy savings targets. Japan's sophisticated manufacturing sector continues to adopt Yokogawa Electric Corporation's and Mitsubishi Electric Corporation's advanced distributed control systems for boiler management in automotive, electronics, and chemical plants. The combination of manufacturing cost advantages, government-backed energy efficiency programs, and rapid uptake of smart factory technologies positions Asia Pacific as the most dynamic growth frontier for boiler control market participants over the forecast horizon.

Competitive Landscape

Market Structure Analysis

The global Boiler Control Market exhibits a moderately consolidated structure, with a handful of multinational automation and industrial technology conglomerates including Siemens AG, Honeywell International Inc., ABB Ltd., Emerson Electric Co., and Schneider Electric SE collectively commanding a significant share of the market. These leaders differentiate through integrated control platforms that combine hardware, software, and cloud analytics, enabling full-lifecycle boiler management. Key competitive strategies include partnerships with boiler OEMs, expansion of digital service offerings (remote diagnostics, SaaS-based monitoring), and geographic penetration into high-growth Asia Pacific and Middle East markets. Mid-tier players compete on cost and regional expertise, particularly in retrofit applications for existing industrial boiler fleets.

Key Market Developments

- February 2025: Honeywell International Inc. announced the expansion of its Honeywell Forge Energy Optimization platform to include AI-driven boiler combustion efficiency modules, targeting industrial and district heating clients across Europe and North America.

- October 2024: Siemens AG and Viessmann Group signed a strategic collaboration agreement to integrate Siemens SIMATIC control technology with Viessmann's commercial condensing boiler range, targeting the European commercial buildings segment.

- March 2024: ABB Ltd. launched an upgraded version of its ABB Ability™ Boiler Advisor with enhanced digital twin simulation capabilities, incorporating real-time emissions monitoring to support industrial clients in meeting updated EU IED (Industrial Emissions Directive) compliance requirements.

Companies Covered in Boiler Control Market

- Siemens AG

- Honeywell International Inc.

- Schneider Electric SE

- Emerson Electric Co.

- ABB Ltd.

- Rockwell Automation, Inc.

- Mitsubishi Electric Corporation

- Yokogawa Electric Corporation

- Delta Electronics, Inc.

- Johnson Controls International plc

- General Electric Company

- Bosch Thermotechnology (Robert Bosch GmbH)

- Azbil Corporation

- Honeywell Process Solutions

- KROHNE Group

- Endress+Hauser Group

- Alfa Laval AB

- Spirax-Sarco Engineering plc

Market Segmentation

The Boiler Control Market report covers the following segmentation categories:

By Boiler Type

- Water Tube

- Fire Tube

By Control Type

- Modulating

- On/Off

By Component

- Hardware

- Software

By End-User

- Industrial

- Commercial

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Executive Summary

- Global Boiler Control Market Snapshot

- Future Projections

- Key Market Trends

- Regional Snapshot, by Value, 2026

- Analyst Recommendations

- Market Overview

- Market Definitions and Segmentations

- Market Dynamics

- Drivers

- Restraints

- Market Opportunities

- Value Chain Analysis

- COVID-19 Impact Analysis

- Porter's Five Forces Analysis

- Impact of Russia-Ukraine Conflict

- PESTLE Analysis

- Regulatory Analysis

- Price Trend Analysis

- Current Prices and Future Projections, 2025-2033

- Price Impact Factors

- Global Boiler Control Market Outlook, 2020 - 2033

- Global Boiler Control Market Outlook, by Boiler Type, Value (US$ Bn), 2020-2033

- Water tube

- P11

- P12

- Fire tube

- P3

- P31

- P32

- Global Boiler Control Market Outlook, by Control Type, Value (US$ Bn), 2020-2033

- Modulating

- On/Off

- A3

- A4

- Global Boiler Control Market Outlook, by Component, Value (US$ Bn), 2020-2033

- Hardware

- Software

- Global Boiler Control Market Outlook, by Region, Value (US$ Bn), 2020-2033

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Water tube

- Global Boiler Control Market Outlook, by Boiler Type, Value (US$ Bn), 2020-2033

- North America Boiler Control Market Outlook, 2020 - 2033

- North America Boiler Control Market Outlook, by Boiler Type, Value (US$ Bn), 2020-2033

- Water tube

- P11

- P12

- Fire tube

- P3

- P31

- P32

- North America Boiler Control Market Outlook, by Control Type, Value (US$ Bn), 2020-2033

- Modulating

- On/Off

- A3

- A4

- North America Boiler Control Market Outlook, by Component, Value (US$ Bn), 2020-2033

- Hardware

- Software

- North America Boiler Control Market Outlook, by Country, Value (US$ Bn), 2020-2033

- U.S. Boiler Control Market Outlook, by Boiler Type, 2020-2033

- U.S. Boiler Control Market Outlook, by Control Type, 2020-2033

- U.S. Boiler Control Market Outlook, by Component, 2020-2033

- Canada Boiler Control Market Outlook, by Boiler Type, 2020-2033

- Canada Boiler Control Market Outlook, by Control Type, 2020-2033

- Canada Boiler Control Market Outlook, by Component, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Water tube

- North America Boiler Control Market Outlook, by Boiler Type, Value (US$ Bn), 2020-2033

- Europe Boiler Control Market Outlook, 2020 - 2033

- Europe Boiler Control Market Outlook, by Boiler Type, Value (US$ Bn), 2020-2033

- Water tube

- P11

- P12

- Fire tube

- P3

- P31

- P32

- Europe Boiler Control Market Outlook, by Control Type, Value (US$ Bn), 2020-2033

- Modulating

- On/Off

- A3

- A4

- Europe Boiler Control Market Outlook, by Component, Value (US$ Bn), 2020-2033

- Hardware

- Software

- Europe Boiler Control Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Germany Boiler Control Market Outlook, by Boiler Type, 2020-2033

- Germany Boiler Control Market Outlook, by Control Type, 2020-2033

- Germany Boiler Control Market Outlook, by Component, 2020-2033

- Italy Boiler Control Market Outlook, by Boiler Type, 2020-2033

- Italy Boiler Control Market Outlook, by Control Type, 2020-2033

- Italy Boiler Control Market Outlook, by Component, 2020-2033

- France Boiler Control Market Outlook, by Boiler Type, 2020-2033

- France Boiler Control Market Outlook, by Control Type, 2020-2033

- France Boiler Control Market Outlook, by Component, 2020-2033

- U.K. Boiler Control Market Outlook, by Boiler Type, 2020-2033

- U.K. Boiler Control Market Outlook, by Control Type, 2020-2033

- U.K. Boiler Control Market Outlook, by Component, 2020-2033

- Spain Boiler Control Market Outlook, by Boiler Type, 2020-2033

- Spain Boiler Control Market Outlook, by Control Type, 2020-2033

- Spain Boiler Control Market Outlook, by Component, 2020-2033

- Russia Boiler Control Market Outlook, by Boiler Type, 2020-2033

- Russia Boiler Control Market Outlook, by Control Type, 2020-2033

- Russia Boiler Control Market Outlook, by Component, 2020-2033

- Rest of Europe Boiler Control Market Outlook, by Boiler Type, 2020-2033

- Rest of Europe Boiler Control Market Outlook, by Control Type, 2020-2033

- Rest of Europe Boiler Control Market Outlook, by Component, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Water tube

- Europe Boiler Control Market Outlook, by Boiler Type, Value (US$ Bn), 2020-2033

- Asia Pacific Boiler Control Market Outlook, 2020 - 2033

- Asia Pacific Boiler Control Market Outlook, by Boiler Type, Value (US$ Bn), 2020-2033

- Water tube

- P11

- P12

- Fire tube

- P3

- P31

- P32

- Asia Pacific Boiler Control Market Outlook, by Control Type, Value (US$ Bn), 2020-2033

- Modulating

- On/Off

- A3

- A4

- Asia Pacific Boiler Control Market Outlook, by Component, Value (US$ Bn), 2020-2033

- Hardware

- Software

- Asia Pacific Boiler Control Market Outlook, by Country, Value (US$ Bn), 2020-2033

- China Boiler Control Market Outlook, by Boiler Type, 2020-2033

- China Boiler Control Market Outlook, by Control Type, 2020-2033

- China Boiler Control Market Outlook, by Component, 2020-2033

- Japan Boiler Control Market Outlook, by Boiler Type, 2020-2033

- Japan Boiler Control Market Outlook, by Control Type, 2020-2033

- Japan Boiler Control Market Outlook, by Component, 2020-2033

- South Korea Boiler Control Market Outlook, by Boiler Type, 2020-2033

- South Korea Boiler Control Market Outlook, by Control Type, 2020-2033

- South Korea Boiler Control Market Outlook, by Component, 2020-2033

- India Boiler Control Market Outlook, by Boiler Type, 2020-2033

- India Boiler Control Market Outlook, by Control Type, 2020-2033

- India Boiler Control Market Outlook, by Component, 2020-2033

- Southeast Asia Boiler Control Market Outlook, by Boiler Type, 2020-2033

- Southeast Asia Boiler Control Market Outlook, by Control Type, 2020-2033

- Southeast Asia Boiler Control Market Outlook, by Component, 2020-2033

- Rest of SAO Boiler Control Market Outlook, by Boiler Type, 2020-2033

- Rest of SAO Boiler Control Market Outlook, by Control Type, 2020-2033

- Rest of SAO Boiler Control Market Outlook, by Component, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Water tube

- Asia Pacific Boiler Control Market Outlook, by Boiler Type, Value (US$ Bn), 2020-2033

- Latin America Boiler Control Market Outlook, 2020 - 2033

- Latin America Boiler Control Market Outlook, by Boiler Type, Value (US$ Bn), 2020-2033

- Water tube

- P11

- P12

- Fire tube

- P3

- P31

- P32

- Latin America Boiler Control Market Outlook, by Control Type, Value (US$ Bn), 2020-2033

- Modulating

- On/Off

- A3

- A4

- Latin America Boiler Control Market Outlook, by Component, Value (US$ Bn), 2020-2033

- Hardware

- Software

- Latin America Boiler Control Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Brazil Boiler Control Market Outlook, by Boiler Type, 2020-2033

- Brazil Boiler Control Market Outlook, by Control Type, 2020-2033

- Brazil Boiler Control Market Outlook, by Component, 2020-2033

- Mexico Boiler Control Market Outlook, by Boiler Type, 2020-2033

- Mexico Boiler Control Market Outlook, by Control Type, 2020-2033

- Mexico Boiler Control Market Outlook, by Component, 2020-2033

- Argentina Boiler Control Market Outlook, by Boiler Type, 2020-2033

- Argentina Boiler Control Market Outlook, by Control Type, 2020-2033

- Argentina Boiler Control Market Outlook, by Component, 2020-2033

- Rest of LATAM Boiler Control Market Outlook, by Boiler Type, 2020-2033

- Rest of LATAM Boiler Control Market Outlook, by Control Type, 2020-2033

- Rest of LATAM Boiler Control Market Outlook, by Component, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Water tube

- Latin America Boiler Control Market Outlook, by Boiler Type, Value (US$ Bn), 2020-2033

- Middle East & Africa Boiler Control Market Outlook, 2020 - 2033

- Middle East & Africa Boiler Control Market Outlook, by Boiler Type, Value (US$ Bn), 2020-2033

- Water tube

- P11

- P12

- Fire tube

- P3

- P31

- P32

- Middle East & Africa Boiler Control Market Outlook, by Control Type, Value (US$ Bn), 2020-2033

- Modulating

- On/Off

- A3

- A4

- Middle East & Africa Boiler Control Market Outlook, by Component, Value (US$ Bn), 2020-2033

- Hardware

- Software

- Middle East & Africa Boiler Control Market Outlook, by Country, Value (US$ Bn), 2020-2033

- GCC Boiler Control Market Outlook, by Boiler Type, 2020-2033

- GCC Boiler Control Market Outlook, by Control Type, 2020-2033

- GCC Boiler Control Market Outlook, by Component, 2020-2033

- South Africa Boiler Control Market Outlook, by Boiler Type, 2020-2033

- South Africa Boiler Control Market Outlook, by Control Type, 2020-2033

- South Africa Boiler Control Market Outlook, by Component, 2020-2033

- Egypt Boiler Control Market Outlook, by Boiler Type, 2020-2033

- Egypt Boiler Control Market Outlook, by Control Type, 2020-2033

- Egypt Boiler Control Market Outlook, by Component, 2020-2033

- Nigeria Boiler Control Market Outlook, by Boiler Type, 2020-2033

- Nigeria Boiler Control Market Outlook, by Control Type, 2020-2033

- Nigeria Boiler Control Market Outlook, by Component, 2020-2033

- Rest of Middle East Boiler Control Market Outlook, by Boiler Type, 2020-2033

- Rest of Middle East Boiler Control Market Outlook, by Control Type, 2020-2033

- Rest of Middle East Boiler Control Market Outlook, by Component, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Water tube

- Middle East & Africa Boiler Control Market Outlook, by Boiler Type, Value (US$ Bn), 2020-2033

- Competitive Landscape

- Company Vs Segment Heatmap

- Company Market Share Analysis, 2025

- Competitive Dashboard

- Company Profiles

- Siemens AG

- Company Overview

- Product Portfolio

- Financial Overview

- Business Strategies and Developments

- Honeywell International Inc.

- Schneider Electric SE

- Emerson Electric Co.

- ABB Ltd.

- Rockwell Automation, Inc.

- Mitsubishi Electric Corporation

- Yokogawa Electric Corporation

- Delta Electronics, Inc.

- Johnson Controls International plc

- General Electric Company

- Bosch Thermotechnology (Robert Bosch GmbH)

- Azbil Corporation

- Honeywell Process Solutions

- KROHNE Group

- Siemens AG

- Appendix

- Research Methodology

- Report Assumptions

- Acronyms and Abbreviations

|

BASE YEAR |

HISTORICAL DATA |

FORECAST PERIOD |

UNITS |

|||

|

2025 |

|

2020 - 2025 |

2026 - 2033 |

Value: US$ Million |

||

|

REPORT FEATURES |

DETAILS |

|

By Boiler Type |

|

|

By Control Type |

|

|

By Component |

|

|

By End-User |

|

|

Geographical Coverage |

|

|

Leading Companies |

|

|

Report Highlights |

Key Market Indicators, Macro-micro economic impact analysis, Technological Roadmap, Key Trends, Driver, Restraints, and Future Opportunities & Revenue Pockets, Porter’s 5 Forces Analysis, Historical Trend (2019-2024), Market Estimates and Forecast, Market Dynamics, Industry Trends, Competition Landscape, Category, Region, Country-wise Trends & Analysis, COVID-19 Impact Analysis (Demand and Supply Chain) |