Intravitreal (IVT) Injectable Market

Global Intravitreal (IVT) Injectable Industry Analysis, Size, Share, Growth, Trends, and Forecast 2026-2033 – (By Drug Class, By Indication, By Geographic Coverage and By Company)

Global Intravitreal (IVT) Injectable Market: Comprehensive Strategic Analysis

Key Market Highlights

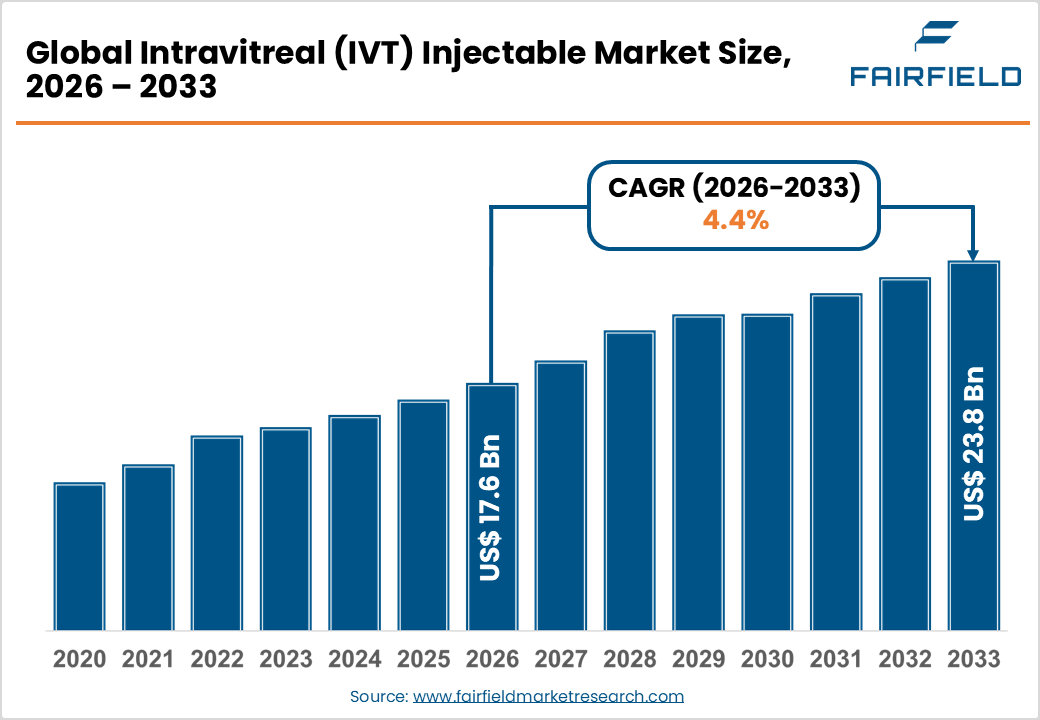

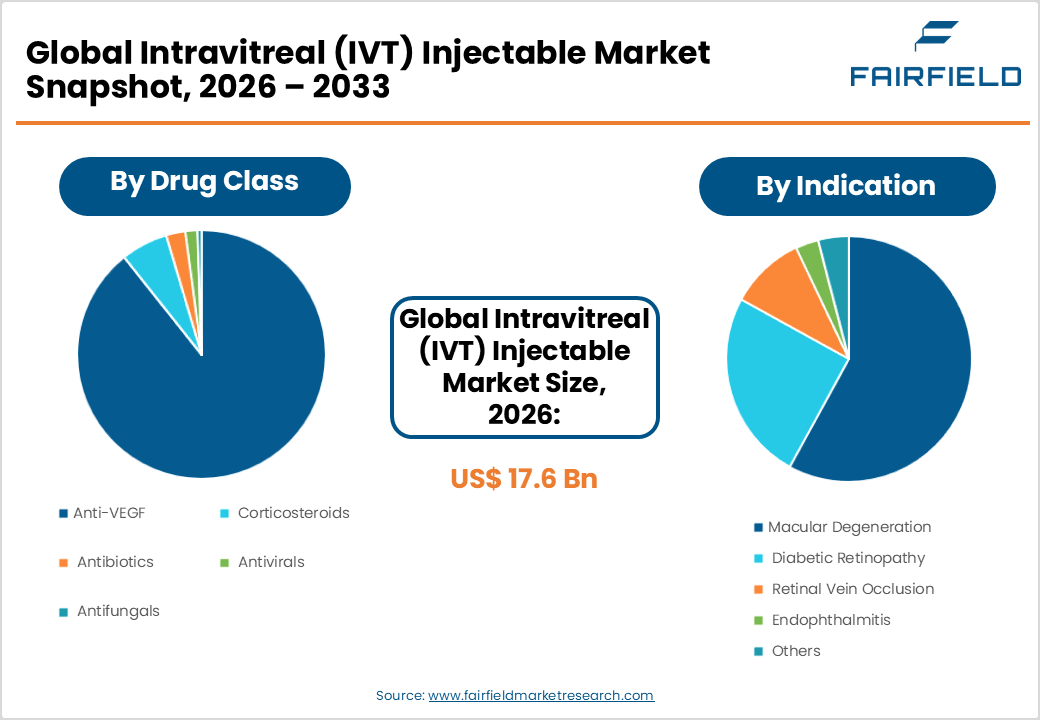

- The global intravitreal (IVT) injectable market size is likely to be valued at USD 17.6 billion in 2026 and is expected to reach USD 23.8 billion by 2033, growing at a CAGR of 4.40% during the forecast period from 2026 to 2033.

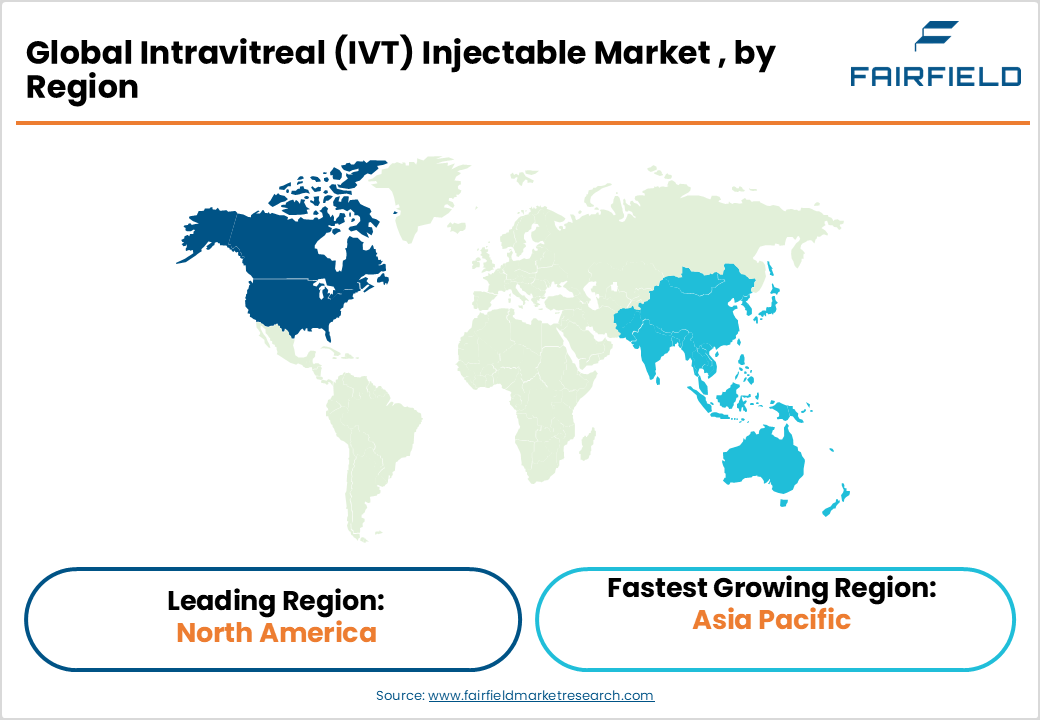

- Leading Region: Asia Pacific leads the IVT injectable market with approximately 45% global share, driven by its massive diabetic and AMD patient population across China, India, and Japan, supported by rapidly expanding ophthalmic specialty care infrastructure.

- Fastest Growing Region: North America is the fastest-growing regional market, bolstered by the U.S. FDA's accelerated approval pathways, high Medicare reimbursement coverage, and a robust ophthalmic biotech innovation ecosystem continuously delivering next-generation IVT therapies.

- Dominant Segment: Anti-VEGF dominates the drug class segment with approximately 68% market share, underpinned by its established clinical efficacy, standard-of-care status for wet AMD and diabetic macular edema, and expanding biosimilar portfolio improving global accessibility.

- Fastest Growing Segment: Diabetic Retinopathy is the fastest-growing indication segment, reflecting the global diabetes epidemic. The IDF projects diabetes prevalence to reach 783 million by 2045, directly amplifying therapeutic demand for IVT interventions.

- Key Market Opportunity: Sustained-release intravitreal implants and gene therapy platforms represent the most transformative near-term opportunity, with over 150 active clinical trials on ClinicalTrials.gov targeting extended-release and genetic correction approaches for retinal disease management.

Market Dynamics: Drivers, Restraints, and Opportunities Analysis

Market Growth Drivers

Rising Global Prevalence of Retinal Diseases

The increasing incidence of diabetic retinopathy and AMD globally remains one of the most powerful catalysts for the IVT injectable market. The International Diabetes Federation (IDF) estimates that 537 million adults were living with diabetes in 2021, a figure projected to rise to 783 million by 2045. Diabetic retinopathy affects approximately one-third of all diabetic individuals, creating a substantial and growing patient pool requiring intravitreal interventions. Similarly, AMD affects over 196 million people globally as per the Lancet Global Health estimates, with numbers expected to reach 288 million by 2040. This demographic surge is directly expanding the addressable demand for anti-VEGF and corticosteroid intravitreal injections, positioning IVT therapies as a cornerstone of modern ophthalmology.

Expanding Pipeline and Regulatory Approvals of Anti-VEGF Biologics

Robust innovation in anti-VEGF biologics continues to energize the intravitreal injectable landscape. The U.S. Food and Drug Administration (FDA) approved Faricimab (Vabysmo) by Roche/Genentech in January 2022, the first bispecific antibody for retinal conditions targeting both VEGF-A and Ang-2 pathways. This diversification of therapeutic mechanisms is broadening the clinical utility of intravitreal therapies beyond traditional VEGF inhibition. Additionally, biosimilars of landmark products such as ranibizumab (Lucentis) and aflibercept (Eylea) are entering markets, improving patient access and cost-effectiveness. According to the American Academy of Ophthalmology (AAO), growing physician comfort with IVT procedures and longer-acting formulations is expected to significantly increase treatment compliance, reinforcing sustained market growth.

Market Restraints

High Treatment Costs and Affordability Barriers

The prohibitive cost of anti-VEGF intravitreal therapies poses a significant restraint on market expansion, particularly in low- and middle-income countries. For instance, ranibizumab (Lucentis) can cost approximately US$ 1,000–US$ 2,000 per injection, and patients often require multiple injections annually, making cumulative treatment costs extremely burdensome. According to the National Eye Institute (NEI), inadequate insurance coverage for ocular therapies in several regions further limits treatment uptake. This cost burden disproportionately affects the elderly and underserved populations, dampening the overall demand potential of the IVT injectable market in price-sensitive geographies.

Risk of Procedure-Related Adverse Events

Intravitreal injections, while generally safe, carry inherent procedural risks that can deter both patients and practitioners. Clinical literature published in journals such as Ophthalmology (American Academy of Ophthalmology) cites the risk of endophthalmitis (occurring in approximately 0.019% to 0.077% of injections), retinal detachment, intraocular pressure elevation, and cataract formation as notable adverse events. Patient anxiety around intraocular needle procedures also translates to non-adherence and premature treatment discontinuation, constraining long-term therapy cycles and thereby limiting overall market penetration, especially in first-time or elderly patient cohorts who may be less receptive to recurring interventions.

Market Opportunities

Emerging Markets and Expanding Healthcare Infrastructure

Rapid improvements in healthcare infrastructure across emerging economies in Asia Pacific, Latin America, and the Middle East & Africa are unlocking substantial untapped demand for intravitreal injectable therapies, public healthcare expenditure in South and Southeast Asia has grown at over 6% annually in recent years. Governments in countries such as India, Brazil, and Indonesia are scaling up eye care programs under national blindness prevention initiatives, directly increasing patient access to IVT treatments. The entry of biosimilar anti-VEGF agents in these markets priced significantly lower than originator products is further enabling wider adoption. This democratization of retinal care represents a high-growth frontier for market participants willing to invest in localized distribution and physician education networks.

Development of Sustained-Release and Drug-Eluting Implants

The development of sustained-release intravitreal implants and gene therapy approaches represents a paradigm shift in retinal drug delivery, offering significant commercial opportunity. Products such as Ocugen's OCU400 and Adverum Biotechnologies' ADVM-022 (a gene therapy targeting VEGF for wet AMD) are in advanced clinical stages. The FDA has granted Regeneron Pharmaceuticals' Port Delivery System with ranibizumab (Susvimo) approval for extended-release delivery, reducing injection frequency from monthly to semi-annual. According to ClinicalTrials.gov, over 150 active clinical trials are currently underway for novel intravitreal formulations, reflecting robust pipeline activity that will sustain market dynamism through 2033 and beyond.

Segmentation Analysis: Category-Wise Strategic Assessment

Drug Class Analysis

The Anti-VEGF segment dominates the IVT injectable market by drug class, commanding approximately 68% of total market share. This dominance is anchored in the proven clinical efficacy of anti-VEGF agents such as bevacizumab (Avastin), ranibizumab (Lucentis), aflibercept (Eylea), and brolucizumab (Beovu) across multiple retinal indications. According to the American Journal of Ophthalmology, anti-VEGF therapies have become the standard of care for wet AMD and diabetic macular edema (DME), driving consistently high prescription volumes globally. The arrival of biosimilars and novel bispecific agents further cements anti-VEGF's position as the backbone of intravitreal treatment protocols. Corticosteroids represent the second-largest segment, utilized primarily in non-infectious uveitis and post-surgical inflammation management.

Indication Analysis

Macular Degeneration accounts for the leading share within the indication segment, representing approximately 42% of the IVT injectable market. Age-related macular degeneration remains the foremost cause of central vision loss in individuals aged over 50, particularly in developed nations. The Bright Focus Foundation estimates that wet AMD, the form most commonly treated with IVT injections, affects approximately 10–15% of AMD patients globally. The high recurrence rate of wet AMD necessitates repeated injection cycles, generating consistent and recurring revenue for manufacturers. Diabetic Retinopathy is the fastest-growing indication sub-segment, driven by the surging global diabetes burden, with increasing clinical guideline support for anti-VEGF therapy as first-line treatment for center-involving diabetic macular edema.

Regional Market Assessment: Strategic Geography Analysis

North America Intravitreal (IVT) Injectable Market Trends

North America is the fastest-growing regional market for intravitreal injectables and holds a commanding position driven by the U.S.'s robust pharmaceutical infrastructure, high disease prevalence, and a favorable regulatory environment. The U.S. FDA has consistently provided expedited approval pathways including Breakthrough Therapy Designation and Priority Review for novel retinal therapies, accelerating market entry. According to the Centers for Disease Control and Prevention (CDC), approximately 37.3 million Americans have diabetes, significantly expanding the diabetic retinopathy patient pool. The region also benefits from high insurance penetration through programs like Medicare Part B, which covers physician-administered drugs including anti-VEGF injections, making treatments financially accessible for the elderly population. Furthermore, prominent innovation hubs in California, Massachusetts, and New Jersey foster a dynamic ophthalmic biotech ecosystem that continuously delivers pipeline breakthroughs, sustaining North America's market leadership and growth momentum.

Europe Intravitreal (IVT) Injectable Market Trends

Europe represents a mature yet steadily expanding market for intravitreal injectables, underpinned by strong healthcare systems and harmonized regulatory oversight via the European Medicines Agency (EMA). Key markets include Germany, the United Kingdom, France, and Spain, which collectively account for the majority of European IVT therapy volume. The U.K.'s National Institute for Health and Care Excellence (NICE) has endorsed ranibizumab and aflibercept as first-line treatments for wet AMD, ensuring reimbursement and broad patient access within the National Health Service (NHS). Germany leads the European market, supported by its high per capita healthcare expenditure and early adoption of biosimilar anti-VEGF products following patent expirations. France and Spain are witnessing growing IVT procedure volumes, supported by national diabetic care programs. Regulatory harmonization under the EMA's centralized procedure streamlines multi-country approvals, enabling faster diffusion of novel intravitreal therapies across member states and sustaining regional market development.

Asia Pacific Intravitreal (IVT) Injectable Market Trends

Asia Pacific is the leading regional market, holding approximately 45% of the global IVT injectable market share. The region's dominance is driven by its massive population base, high and rising prevalence of diabetes-related ocular conditions, and rapidly improving healthcare access. China and India together account for over 40% of the global diabetic population according to the IDF Diabetes Atlas, directly fueling demand for diabetic retinopathy treatments. Japan represents a technologically advanced sub-market with high IVT adoption and strong domestic pharmaceutical manufacturing capacity. ASEAN nations such as Indonesia, Thailand, Vietnam, and Malaysia are emerging as high-growth sub-markets, driven by expanding ophthalmic specialty care infrastructure and increasing government investment in non-communicable disease management. China's National Medical Products Administration (NMPA) has accelerated approvals of biosimilar anti-VEGF products, enhancing affordability and adoption. The region's cost-competitive manufacturing ecosystem also offers market participants a strategic advantage in global supply chain optimization.

Competitive Landscape: Market Structure and Strategic Positioning

The global intravitreal injectable market exhibits a moderately consolidated structure, with a handful of multinational pharmaceutical corporations holding dominant market positions through proprietary anti-VEGF franchises and established distribution networks. Regeneron Pharmaceuticals, Novartis AG, Roche/Genentech, and Allergan (AbbVie) collectively capture a significant share of global IVT revenues. Key competitive strategies include pipeline diversification into gene therapy and sustained-release implants, biosimilar entry to capture cost-sensitive segments, and geographic expansion into high-growth Asia Pacific markets. Strategic licensing agreements, co-promotion partnerships, and mergers and acquisitions remain prevalent approaches for capability enhancement and market penetration across all tiers of the competitive hierarchy.

Key Players

- Novartis AG

- ThromboGenics, Inc.

- Bausch & Lomb

- Allergan

- Alimera Sciences

- Bristol-Myers Squibb Company

- Regeneron Pharmaceuticals, Inc.

- Other

Key Industry Developments

- January 2025: Regeneron Pharmaceuticals, Inc. announced positive Phase 3 trial results for high-dose aflibercept (Eylea HD) in diabetic macular edema, demonstrating non-inferior visual acuity gains with extended 16-week dosing intervals compared to standard-of-care monthly dosing regimens.

- March 2025: Novartis AG received expanded FDA approval for brolucizumab (Beovu) in diabetic macular edema, broadening its anti-VEGF portfolio's addressable indication base and reinforcing its competitive position in the U.S. retinal therapeutics market.

- October 2024: Bausch & Lomb completed its strategic acquisition of an ophthalmic drug delivery platform company, strengthening its intravitreal injectable product pipeline and enabling next-generation sustained-release formulation capabilities for retinal indications.

Global Intravitreal (IVT) Injectable Market Segmentation

By Drug Class

- Anti-VEGF

- Corticosteroids

- Antibiotics

- Antivirals

- Antifungals

By Indication

- Macular Degeneration

- Diabetic Retinopathy

- Retinal Vein Occlusion

- Endophthalmitis

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Executive Summary

- Global Intravitreal (IVT) Injectable Market Snapshot

- Future Projections

- Key Market Trends

- Regional Snapshot, by Value, 2026

- Analyst Recommendations

- Market Overview

- Market Definitions and Segmentations

- Market Dynamics

- Drivers

- Restraints

- Market Opportunities

- Value Chain Analysis

- COVID-19 Impact Analysis

- Porter's Five Forces Analysis

- Impact of Russia-Ukraine Conflict

- PESTLE Analysis

- Regulatory Analysis

- Price Trend Analysis

- Current Prices and Future Projections, 2025-2033

- Price Impact Factors

- Global Intravitreal (IVT) Injectable Market Outlook, 2020 - 2033

- Global Intravitreal (IVT) Injectable Market Outlook, by Drug Class, Value (US$ Bn), 2020-2033

- Anti-VEGF

- Corticosteroids

- Antibiotics

- Antivirals

- Antifungals

- Global Intravitreal (IVT) Injectable Market Outlook, by Indication, Value (US$ Bn), 2020-2033

- Macular Degeneration

- Diabetic Retinopathy

- Retinal Vein Occlusion

- Endophthalmitis

- Others

- Global Intravitreal (IVT) Injectable Market Outlook, by Region, Value (US$ Bn), 2020-2033

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Global Intravitreal (IVT) Injectable Market Outlook, by Drug Class, Value (US$ Bn), 2020-2033

- North America Intravitreal (IVT) Injectable Market Outlook, 2020 - 2033

- North America Intravitreal (IVT) Injectable Market Outlook, by Drug Class, Value (US$ Bn), 2020-2033

- Anti-VEGF

- Corticosteroids

- Antibiotics

- Antivirals

- Antifungals

- North America Intravitreal (IVT) Injectable Market Outlook, by Indication, Value (US$ Bn), 2020-2033

- Macular Degeneration

- Diabetic Retinopathy

- Retinal Vein Occlusion

- Endophthalmitis

- Others

- North America Intravitreal (IVT) Injectable Market Outlook, by Country, Value (US$ Bn), 2020-2033

- U.S. Intravitreal (IVT) Injectable Market Outlook, by Drug Class, 2020-2033

- U.S. Intravitreal (IVT) Injectable Market Outlook, by Indication, 2020-2033

- Canada Intravitreal (IVT) Injectable Market Outlook, by Drug Class, 2020-2033

- Canada Intravitreal (IVT) Injectable Market Outlook, by Indication, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- North America Intravitreal (IVT) Injectable Market Outlook, by Drug Class, Value (US$ Bn), 2020-2033

- Europe Intravitreal (IVT) Injectable Market Outlook, 2020 - 2033

- Europe Intravitreal (IVT) Injectable Market Outlook, by Drug Class, Value (US$ Bn), 2020-2033

- Anti-VEGF

- Corticosteroids

- Antibiotics

- Antivirals

- Antifungals

- Europe Intravitreal (IVT) Injectable Market Outlook, by Indication, Value (US$ Bn), 2020-2033

- Macular Degeneration

- Diabetic Retinopathy

- Retinal Vein Occlusion

- Endophthalmitis

- Others

- Europe Intravitreal (IVT) Injectable Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Germany Intravitreal (IVT) Injectable Market Outlook, by Drug Class, 2020-2033

- Germany Intravitreal (IVT) Injectable Market Outlook, by Indication, 2020-2033

- Italy Intravitreal (IVT) Injectable Market Outlook, by Drug Class, 2020-2033

- Italy Intravitreal (IVT) Injectable Market Outlook, by Indication, 2020-2033

- France Intravitreal (IVT) Injectable Market Outlook, by Drug Class, 2020-2033

- France Intravitreal (IVT) Injectable Market Outlook, by Indication, 2020-2033

- U.K. Intravitreal (IVT) Injectable Market Outlook, by Drug Class, 2020-2033

- U.K. Intravitreal (IVT) Injectable Market Outlook, by Indication, 2020-2033

- Spain Intravitreal (IVT) Injectable Market Outlook, by Drug Class, 2020-2033

- Spain Intravitreal (IVT) Injectable Market Outlook, by Indication, 2020-2033

- Russia Intravitreal (IVT) Injectable Market Outlook, by Drug Class, 2020-2033

- Russia Intravitreal (IVT) Injectable Market Outlook, by Indication, 2020-2033

- Rest of Europe Intravitreal (IVT) Injectable Market Outlook, by Drug Class, 2020-2033

- Rest of Europe Intravitreal (IVT) Injectable Market Outlook, by Indication, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Europe Intravitreal (IVT) Injectable Market Outlook, by Drug Class, Value (US$ Bn), 2020-2033

- Asia Pacific Intravitreal (IVT) Injectable Market Outlook, 2020 - 2033

- Asia Pacific Intravitreal (IVT) Injectable Market Outlook, by Drug Class, Value (US$ Bn), 2020-2033

- Anti-VEGF

- Corticosteroids

- Antibiotics

- Antivirals

- Antifungals

- Asia Pacific Intravitreal (IVT) Injectable Market Outlook, by Indication, Value (US$ Bn), 2020-2033

- Macular Degeneration

- Diabetic Retinopathy

- Retinal Vein Occlusion

- Endophthalmitis

- Others

- Asia Pacific Intravitreal (IVT) Injectable Market Outlook, by Country, Value (US$ Bn), 2020-2033

- China Intravitreal (IVT) Injectable Market Outlook, by Drug Class, 2020-2033

- China Intravitreal (IVT) Injectable Market Outlook, by Indication, 2020-2033

- Japan Intravitreal (IVT) Injectable Market Outlook, by Drug Class, 2020-2033

- Japan Intravitreal (IVT) Injectable Market Outlook, by Indication, 2020-2033

- South Korea Intravitreal (IVT) Injectable Market Outlook, by Drug Class, 2020-2033

- South Korea Intravitreal (IVT) Injectable Market Outlook, by Indication, 2020-2033

- India Intravitreal (IVT) Injectable Market Outlook, by Drug Class, 2020-2033

- India Intravitreal (IVT) Injectable Market Outlook, by Indication, 2020-2033

- Southeast Asia Intravitreal (IVT) Injectable Market Outlook, by Drug Class, 2020-2033

- Southeast Asia Intravitreal (IVT) Injectable Market Outlook, by Indication, 2020-2033

- Rest of SAO Intravitreal (IVT) Injectable Market Outlook, by Drug Class, 2020-2033

- Rest of SAO Intravitreal (IVT) Injectable Market Outlook, by Indication, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Asia Pacific Intravitreal (IVT) Injectable Market Outlook, by Drug Class, Value (US$ Bn), 2020-2033

- Latin America Intravitreal (IVT) Injectable Market Outlook, 2020 - 2033

- Latin America Intravitreal (IVT) Injectable Market Outlook, by Drug Class, Value (US$ Bn), 2020-2033

- Anti-VEGF

- Corticosteroids

- Antibiotics

- Antivirals

- Antifungals

- Latin America Intravitreal (IVT) Injectable Market Outlook, by Indication, Value (US$ Bn), 2020-2033

- Macular Degeneration

- Diabetic Retinopathy

- Retinal Vein Occlusion

- Endophthalmitis

- Others

- Latin America Intravitreal (IVT) Injectable Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Brazil Intravitreal (IVT) Injectable Market Outlook, by Drug Class, 2020-2033

- Brazil Intravitreal (IVT) Injectable Market Outlook, by Indication, 2020-2033

- Mexico Intravitreal (IVT) Injectable Market Outlook, by Drug Class, 2020-2033

- Mexico Intravitreal (IVT) Injectable Market Outlook, by Indication, 2020-2033

- Argentina Intravitreal (IVT) Injectable Market Outlook, by Drug Class, 2020-2033

- Argentina Intravitreal (IVT) Injectable Market Outlook, by Indication, 2020-2033

- Rest of LATAM Intravitreal (IVT) Injectable Market Outlook, by Drug Class, 2020-2033

- Rest of LATAM Intravitreal (IVT) Injectable Market Outlook, by Indication, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Latin America Intravitreal (IVT) Injectable Market Outlook, by Drug Class, Value (US$ Bn), 2020-2033

- Middle East & Africa Intravitreal (IVT) Injectable Market Outlook, 2020 - 2033

- Middle East & Africa Intravitreal (IVT) Injectable Market Outlook, by Drug Class, Value (US$ Bn), 2020-2033

- Anti-VEGF

- Corticosteroids

- Antibiotics

- Antivirals

- Antifungals

- Middle East & Africa Intravitreal (IVT) Injectable Market Outlook, by Indication, Value (US$ Bn), 2020-2033

- Macular Degeneration

- Diabetic Retinopathy

- Retinal Vein Occlusion

- Endophthalmitis

- Others

- Middle East & Africa Intravitreal (IVT) Injectable Market Outlook, by Country, Value (US$ Bn), 2020-2033

- GCC Intravitreal (IVT) Injectable Market Outlook, by Drug Class, 2020-2033

- GCC Intravitreal (IVT) Injectable Market Outlook, by Indication, 2020-2033

- South Africa Intravitreal (IVT) Injectable Market Outlook, by Drug Class, 2020-2033

- South Africa Intravitreal (IVT) Injectable Market Outlook, by Indication, 2020-2033

- Egypt Intravitreal (IVT) Injectable Market Outlook, by Drug Class, 2020-2033

- Egypt Intravitreal (IVT) Injectable Market Outlook, by Indication, 2020-2033

- Nigeria Intravitreal (IVT) Injectable Market Outlook, by Drug Class, 2020-2033

- Nigeria Intravitreal (IVT) Injectable Market Outlook, by Indication, 2020-2033

- Rest of Middle East Intravitreal (IVT) Injectable Market Outlook, by Drug Class, 2020-2033

- Rest of Middle East Intravitreal (IVT) Injectable Market Outlook, by Indication, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Middle East & Africa Intravitreal (IVT) Injectable Market Outlook, by Drug Class, Value (US$ Bn), 2020-2033

- Competitive Landscape

- Company Vs Segment Heatmap

- Company Market Share Analysis, 2025

- Competitive Dashboard

- Company Profiles

- Novartis AG

- Company Overview

- Product Portfolio

- Financial Overview

- Business Strategies and Developments

- ThromboGenics, Inc.

- Bausch & Lomb

- Allergan

- Alimera Sciences

- Bristol-Myers Squibb Company

- Regeneron Pharmaceuticals, Inc.

- Other

- Novartis AG

- Appendix

- Research Methodology

- Report Assumptions

- Acronyms and Abbreviations

|

BASE YEAR |

HISTORICAL DATA |

FORECAST PERIOD |

UNITS |

|||

|

2025 |

|

2019 - 2025 |

2026 - 2033 |

Value: US$ Billion |

||

|

REPORT FEATURES |

DETAILS |

|

By Drug Class Coverage |

|

|

By Indication Coverage |

|

|

Geographical Coverage |

|

|

Leading Companies |

|

|

Report Highlights |

Key Market Indicators, Macro-micro economic impact analysis, Technological Roadmap, Key Trends, Driver, Restraints, and Future Opportunities & Revenue Pockets, Porter’s 5 Forces Analysis, Historical Trend (2019-2024), Market Estimates and Forecast, Market Dynamics, Industry Trends, Competition Landscape, Category, Region, Country-wise Trends & Analysis, COVID-19 Impact Analysis (Demand and Supply Chain) |

Our Research Methodology

Considering the volatility of business today, traditional approaches to strategizing a game plan can be unfruitful if not detrimental. True ambiguity is no way to determine a forecast. A myriad of predetermined factors must be accounted for such as the degree of risk involved, the magnitude of circumstances, as well as conditions or consequences that are not known or unpredictable. To circumvent binary views that cast uncertainty, the application of market research intelligence to strategically posture, move, and enable actionable outcomes is necessary.

View Methodology

Quality Assured

Rigorous Validation Process

Confidentiality Assured

End-to-end Data Security

Custom Research Services

Tailored To Your Objectives

FAQs

The global Intravitreal (IVT) Injectable Market size is USD 17.6 billion in 2026.

The global Intravitreal (IVT) Injectable Market is projected 4.4% CAGR by 2033.

The global Intravitreal (IVT) Injectable Market growth drivers include rising retinal disease prevalence, aging populations, and delivery innovations.

North America is a dominating region for global Intravitreal (IVT) Injectable Market.

Regeneron, Roche, Novartis, EyePoint Pharmaceuticals, and Kanghong are some leading industry players in the global Intravitreal (IVT) Injectable Market.

Related Reports

Analgesics Market Insights, Competitive Landscape, and Market Forecast 2033

The analgesics market is expected to reach US$93.01 billion by 2033 from US$58.30 billion in 2026, driven by a steady 6.9% CAGR over the forecast period.

Sleep Apnea Implants Market Insights, Competitive Landscape, and Market Forecast 2033

The sleep apnea implants market is forecast to expand at a 4.0% CAGR, reaching US$ 632.31 Mn by 2033, amid increasing demand for advanced treatments.

DNA Polymerase Market Insights, Competitive Landscape, and Market Forecast - 2033

DNA Polymerase Market is growing with rising genomics research, PCR adoption, gene therapy, NGS demand, and advances in molecular diagnostics.

Sleep Apnea Diagnostic Systems Market Insights, Competitive Landscape, and Market Forecast - 2033

Sleep Apnea Diagnostic Systems Market to reach US$5.77 Bn by 2033 from US$4.60 Bn in 2026, growing at a 3.3% CAGR.

CMO/CDMO Market Insights, Competitive Landscape, and Market Forecast - 2033

CMO/CDMO Market is projected to reach US$128.29 Bn by 2033, driven by pharma outsourcing, biologics demand, and cell & gene therapy growth.

Teleradiology Market Insights, Competitive Landscape, and Market Forecast - 2033

Teleradiology Market is projected to reach US$125.10 billion by 2033, growing at a 26.6% CAGR with rising demand for remote imaging.