Executive Summary & Key Highlights of Global Skin Boosters Market

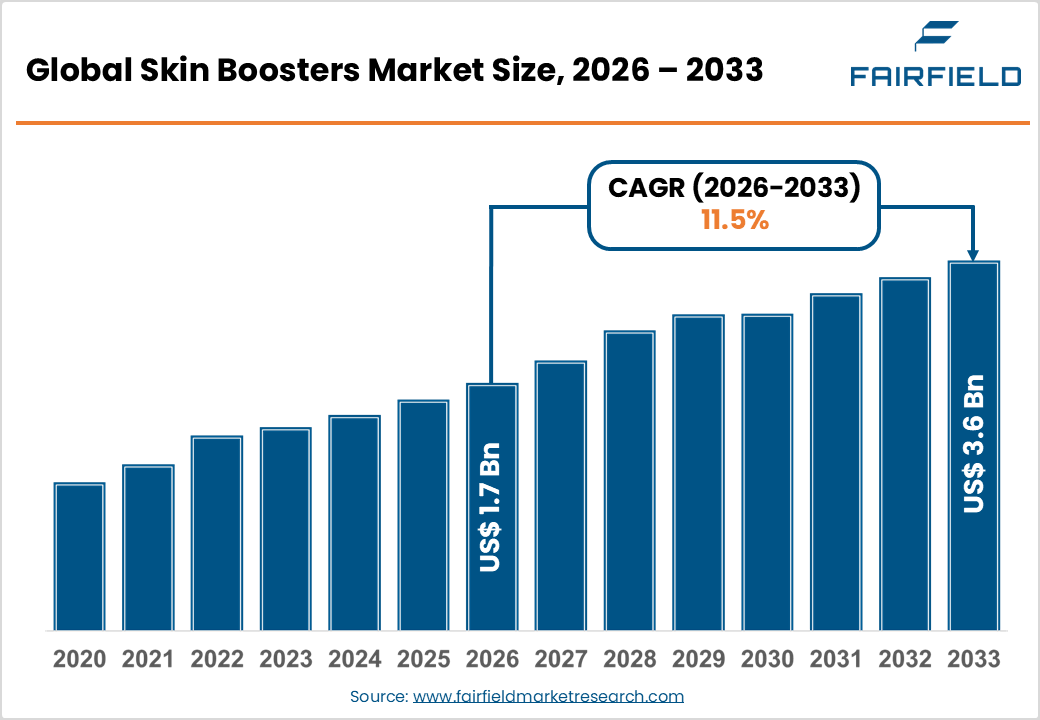

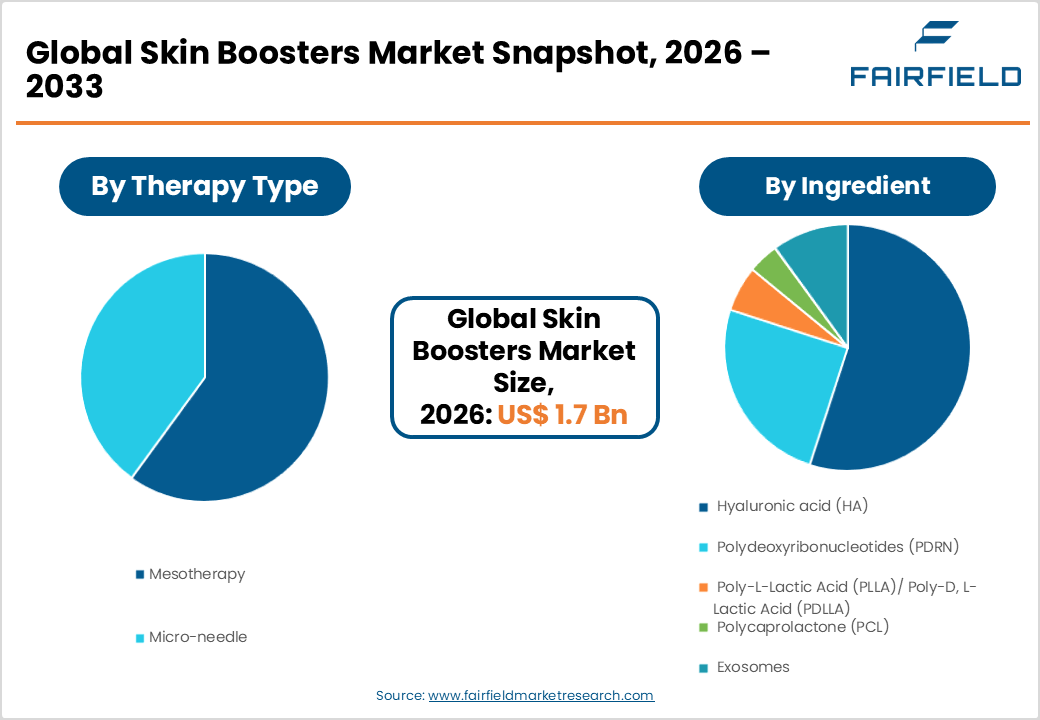

- The global skin boosters market size is likely to be valued at USD 1.7 billion in 2026 and is expected to reach USD 3.6 billion by 2033, growing at a CAGR of 11.50% during the forecast period from 2026 to 2033.

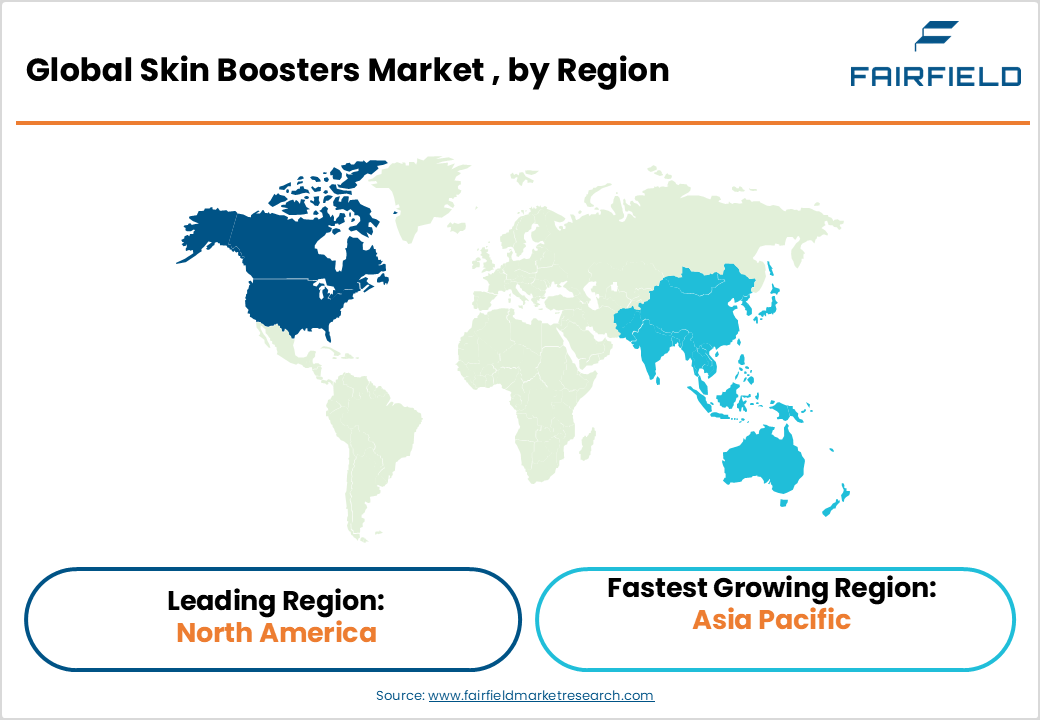

- North America leads the global skin boosters market, accounting for approximately 45% of total revenue, driven by strong U.S. FDA regulatory infrastructure, high aesthetic awareness, and dominant player presence including Galderma and AbbVie.

- Asia Pacific is the fastest growing region in the skin boosters market, fueled by South Korea's innovative biotechnology sector, expanding middle-class consumers in China and India, and thriving medical aesthetics tourism across ASEAN nations.

- Hyaluronic acid (HA) commands approximately 55% ingredient segment share in the skin boosters market, driven by superior hydration capacity, extensive clinical validation, and broad regulatory approval across major geographies.

- Exosome-based skin booster formulations represent the fastest-growing ingredient segment, propelled by growing clinical evidence of regenerative efficacy, active R&D from South Korean biotechnology firms, and increasing global regulatory engagement.

- The expansion of medical aesthetics tourism in Asia Pacific and the rising male aesthetic awareness globally present significant untapped growth opportunities for skin booster market participants to diversify consumer base and geographic revenue streams.

Market Dynamics: Drivers, Restraints, and Opportunities Analysis

Market Growth Drivers

- Rising Demand for Minimally Invasive Aesthetic Procedures

The global aesthetics industry has experienced a profound shift in consumer behavior, with patients consistently favoring minimally invasive solutions over surgical interventions. According to the International Society of Aesthetic Plastic Surgery (ISAPS), non-surgical procedures accounted for over 50% of all cosmetic interventions performed globally in recent years. Skin boosters, delivering targeted dermal hydration and rejuvenation without surgical risks or prolonged recovery, align precisely with this consumer trend. Hyaluronic acid-based injectable formulations have gained particular traction among patients seeking natural-looking, long-lasting skin quality improvements. This increasing procedural volume is directly propelling demand for advanced skin booster products across medical spas and dermatology clinics worldwide, thereby reinforcing sustained market growth.

- Aging Global Population and Growing Aesthetic Awareness

The global population aged 60 years and above is projected to reach approximately 2.1 billion by 2050. Older demographics increasingly seek aesthetic interventions to address skin laxity, volume loss, and chronic dehydration conditions effectively managed by skin booster therapies. Concurrently, heightened awareness through digital and social media platforms has normalized cosmetic procedures across younger consumer segments, expanding the addressable patient population. The growing number of trained aesthetic practitioners globally, supported by expanding dermatological education programs and professional certifications from bodies such as the American Academy of Dermatology (AAD), is further strengthening procedural volumes and driving consistent demand growth across the skin boosters market.

Market Restraints

- High Treatment Costs and Limited Insurance Coverage

Skin booster treatments remain predominantly out-of-pocket expenses, as most health insurance providers globally do not cover elective cosmetic procedures. A single skin booster session can range from USD 300 to USD 1,000 or more depending on the product, number of syringes, and geographic location, with multiple sessions typically required for optimal results. This financial barrier significantly limits adoption among price-sensitive consumer segments. In lower-income populations and developing economies where healthcare expenditure is already constrained, the affordability gap substantially curtails market penetration of premium skin booster formulations, posing a persistent restraint on overall market growth.

- Stringent Regulatory Approval Processes

Skin boosters, classified as medical devices or injectable dermal fillers in most jurisdictions, are subject to rigorous regulatory scrutiny. In the United States, the U.S. Food and Drug Administration (FDA) classifies dermal fillers as Class III medical devices, requiring substantial clinical evidence for market authorization. Similarly, the European Medicines Agency (EMA) and national regulatory bodies enforce strict CE marking requirements under the EU Medical Device Regulation (MDR 2017/745). These lengthy and costly approval pathways significantly increase time-to-market and entry barriers, particularly for companies developing novel ingredient-based formulations such as exosomes and PDRN-derived injectables, thereby constraining the overall pace of product innovation.

Market Opportunities

- Expanding Adoption of Exosome and PDRN-Based Skin Boosters

Exosome-based therapies represent one of the most promising frontiers in regenerative aesthetics. Exosomes, nano-sized extracellular vesicles have demonstrated significant potential in promoting tissue repair, collagen synthesis, and anti-inflammatory activity in peer-reviewed publications in journals such as the Journal of Dermatological Science. Companies such as ExoCoBio Inc. have been actively advancing exosome-based aesthetic platforms, with their flagship ASCE+ product receiving regulatory engagement from South Korean Ministry of Food and Drug Safety (MFDS) authorities. PDRN (Polydeoxyribonucleotides), derived from salmon DNA, has an established clinical evidence base in Asia for wound healing and skin regeneration. As scientific validation deepens and regulatory pathways become more defined, these next-generation ingredients offer significant market expansion opportunities for industry participants.

- Growth in Medical Aesthetics Tourism and Emerging Markets

Medical aesthetics tourism is emerging as a powerful market growth driver, with international patients traveling to South Korea, Thailand, Turkey, and India for high-quality, cost-effective cosmetic procedures. According to the Medical Tourism Association, aesthetic procedures remain among the most sought-after services in global medical tourism. Asia Pacific benefits from a combination of competitive treatment pricing, high clinical expertise, and a regulatory environment supportive of aesthetic innovation. The rising middle-class populations in Southeast Asia, Brazil, and Gulf Cooperation Council (GCC) countries present substantial untapped demand for skin booster treatments. Companies that establish commercial partnerships with regional clinic networks or launch market-adapted product offerings can unlock considerable incremental revenue across these high-growth geographies.

Segmentation Analysis: Category-Wise Strategic Assessment

- Therapy Type Analysis

Mesotherapy dominates the therapy type segment, accounting for approximately 60% of the skin boosters market in 2026. This technique involves the intradermal or subcutaneous injection of active substances including vitamins, minerals, amino acids, and hyaluronic acid directly into the dermis. Its popularity stems from its exceptional versatility, enabling practitioners to customize formulations for each patient's unique skin condition and treatment goal. Mesotherapy's comparatively lower procedural complexity relative to micro-needle-based approaches facilitates broader accessibility in both med spa and clinical settings. Clinical studies published in the Journal of Cosmetic Dermatology have documented its efficacy in improving skin hydration, elasticity, and radiance, reinforcing sustained patient and practitioner preference for this therapy modality.

- Ingredient Analysis

Hyaluronic acid (HA) remains the dominant ingredient in the skin boosters market, commanding approximately 55% of market share in 2026. HA's unparalleled capacity to retain up to 1,000 times its weight in water makes it the gold standard for skin hydration and volumization. Extensively studied and clinically validated, HA-based skin boosters such as Galderma's Restylane Skin Boosters and Teoxane's RHA products have demonstrated long-term improvements in skin elasticity and moisture retention. Both the U.S. FDA and European regulatory authorities have granted approvals to multiple HA-based injectable formulations. The ingredient's excellent safety profile and high biocompatibility continue to contribute to exceptional patient satisfaction rates, sustaining its dominant position over emerging alternatives including PDRN, PLLA, and PCL.

- Gender Analysis

The female segment dominates the gender category, accounting for approximately 80% of the skin boosters market. Women represent the primary consumer base for aesthetic procedures globally, driven by elevated aesthetic awareness, proactive preventive skincare behavior, and the influence of beauty and wellness media. Data from the International Society of Aesthetic Plastic Surgery (ISAPS) consistently confirm that women account for the vast majority of non-surgical aesthetic procedures performed worldwide. However, the male segment is gradually gaining momentum, fueled by the global growth of male grooming culture, reduced social stigma around male cosmetic treatments, and targeted marketing initiatives by aesthetic brands. Dermatology clinics and medical spas are increasingly developing male-specific aesthetic programs, which may progressively recalibrate the gender composition of the market over the forecast period.

- End-use Analysis

Dermatology clinics represent the leading end-use segment, capturing approximately 58% of the skin boosters market in 2025. The clinical environment provides medically supervised care, offering patients reassurance regarding procedural safety and outcome quality. Dermatologists and aesthetic physicians possess the clinical expertise to manage complex cases, recommend evidence-based product combinations, and handle adverse events. Regulatory mandates in several jurisdictions including the U.K. , following MHRA reforms introduced in 2023 require that injectable aesthetic procedures be performed exclusively by licensed medical practitioners in approved clinical settings, further reinforcing the dominance of dermatology clinics. The expanding global base of board-certified aesthetic dermatologists continues to sustain this segment's market leadership.

Regional Market Assessment: Strategic Geography Analysis

- North America Skin Boosters Market Trends

North America leads the global skin boosters market, accounting for approximately 45% of total global revenue, underpinned by the United States' well-established medical aesthetics industry and rigorous regulatory framework. The U.S. FDA's stringent approval processes lend significant credibility to authorized skin booster products, driving strong clinician and patient confidence. The American Society for Dermatologic Surgery (ASDS) has consistently reported year-over-year growth in injectable non-surgical procedures, reflecting robust underlying consumer demand for aesthetic skin treatments.

The U.S. market benefits from a highly developed network of medical spas, licensed dermatology clinics, and aesthetic training institutions that support widespread procedural adoption. Leading global players including Galderma and AbbVie, Inc. (Allergan) maintain significant commercial operations in North America, continuously launching next-generation hyaluronic acid and biopolymer-based skin booster products to sustain competitive momentum in this highly developed regional market.

- Europe Skin Boosters Market Trends

Europe represents a significant contributor to the global skin boosters market, supported by a sophisticated regulatory ecosystem and high consumer awareness of advanced aesthetic treatments. The European Union's Medical Device Regulation (MDR 2017/745) governs dermal fillers and skin booster injectables across member states, ensuring harmonized product safety and quality standards. Germany, the United Kingdom, France, and Spain constitute the primary sub-regional markets, supported by established aesthetic medicine practices and high-density physician networks.

The U.K. has been advancing its cosmetic procedure regulatory reforms post-Brexit, with the Medicines and Healthcare products Regulatory Agency (MHRA) implementing stricter practitioner licensing requirements in 2023 aimed at improving patient safety outcomes. France and Germany continue to function as key innovation hubs, fostering R&D collaborations between pharmaceutical companies, including IBSA Farmaceutici Italia Srl and Sinclair, and academic dermatology research centers across the continent.

- Asia Pacific Skin Boosters Market Trends

Asia Pacific is the fastest-growing region in the global skin boosters market, driven by a convergence of demographic, cultural, and economic growth factors. South Korea, widely regarded as the global hub of aesthetic innovation, is home to key skin booster manufacturers including VAIM Co., Ltd., Medytox, Inc., PharmaResearch Co., Ltd., and Dexlevo Co., Ltd. The Korean Ministry of Food and Drug Safety (MFDS) has established streamlined regulatory pathways that have enabled rapid commercialization of advanced formulations including PDRN and PLLA-based injectable skin boosters.

China and India are rapidly emerging as high-growth markets within Asia Pacific, driven by expanding middle-class populations, rising disposable incomes, and accelerating aesthetic awareness among urban consumer cohorts. Japan's aging population and deeply rooted dermatological culture continue to support high procedural volumes. ASEAN markets, particularly Thailand and Vietnam, are experiencing rapid growth through the expansion of medical aesthetics tourism, attracting international patients seeking premium-quality, cost-effective skin booster treatments, further reinforcing the region's fastest-growing market status.

Competitive Landscape: Market Structure and Strategic Positioning

The global skin boosters market exhibits a moderately consolidated competitive structure, characterized by a mix of established multinational pharmaceutical corporations and specialized aesthetic biotechnology firms. Leading players such as Galderma, AbbVie, Inc. (Allergan), and Merz Pharma dominate through extensive product portfolios, strong physician engagement networks, and significant R&D investments. South Korean innovators including Medytox, Inc., PharmaResearch Co., Ltd., and ExoCoBio Inc. are disrupting the market through next-generation biologics-based formulations. Key competitive strategies include targeted geographic expansion into Asia Pacific and Latin America, strategic alliances with aesthetic training academies, and accelerated pipeline development in exosome and PCL-based skin booster technologies.

Key Players

- Galderma

- AbbVie, Inc (Allergen)

- VAIM Co., Ltd

- Sinclair

- Merz Pharma

- Teoxane

- Medytox, Inc.

- PharmaResearch Co., Ltd.

- Dexlevo Co., Ltd.

- Bloomage Biotechnology

- IBSA Farmaceutici Italia Srl

- ExoCoBio Inc.

- LINKUS GLOBAL Co., Ltd.

Key Industry Developments

- March, 2024: Galderma announced the global expansion of its Restylane skin booster line with next-generation hyaluronic acid formulations targeting advanced skin hydration and elasticity improvement across key Asian markets.

- January, 2025: ExoCoBio Inc. received regulatory clearance in South Korea for its exosome-based aesthetic platform, ASCE+, marking a significant milestone in the commercialization of next-generation regenerative skin booster therapies.

- September, 2023: Teoxane expanded its RHA (Resilient Hyaluronic Acid) technology portfolio with new skin booster indications, strengthening its position across European and North American aesthetic markets through advanced injectable formulations.

Global Skin Boosters Market Segmentation-

By Therapy Type

- Mesotherapy

- Micro-needle

By Ingredient

- Hyaluronic acid (HA)

- Polydeoxyribonucleotides (PDRN)

- Poly-L-Lactic Acid (PLLA)/ Poly-D, L-Lactic Acid (PDLLA)

- Polycaprolactone (PCL)

- Exosomes

By Gender

- Female

- Male

By End-use

- Med spas

- Dermatology Clinics

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Executive Summary

- Global Skin Boosters Market Snapshot

- Future Projections

- Key Market Trends

- Regional Snapshot, by Value, 2026

- Analyst Recommendations

- Market Overview

- Market Definitions and Segmentations

- Market Dynamics

- Drivers

- Restraints

- Market Opportunities

- Value Chain Analysis

- COVID-19 Impact Analysis

- Porter's Five Forces Analysis

- Impact of Russia-Ukraine Conflict

- PESTLE Analysis

- Regulatory Analysis

- Price Trend Analysis

- Current Prices and Future Projections, 2025-2033

- Price Impact Factors

- Global Skin Boosters Market Outlook, 2020 - 2033

- Global Skin Boosters Market Outlook, by Therapy Type, Value (US$ Bn), 2020-2033

- Mesotherapy

- Micro-needle

- Global Skin Boosters Market Outlook, by Ingredient, Value (US$ Bn), 2020-2033

- Hyaluronic acid (HA)

- Polydeoxyribonucleotides (PDRN)

- Poly-L-Lactic Acid (PLLA)/ Poly-D, L-Lactic Acid (PDLLA)

- Polycaprolactone (PCL)

- Exosomes

- Global Skin Boosters Market Outlook, by Gender, Value (US$ Bn), 2020-2033

- Female

- Male

- Global Skin Boosters Market Outlook, by End-user, Value (US$ Bn), 2020-2033

- Med spas

- Dermatology Clinics

- Global Skin Boosters Market Outlook, by Region, Value (US$ Bn), 2020-2033

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Global Skin Boosters Market Outlook, by Therapy Type, Value (US$ Bn), 2020-2033

- North America Skin Boosters Market Outlook, 2020 - 2033

- North America Skin Boosters Market Outlook, by Therapy Type, Value (US$ Bn), 2020-2033

- Mesotherapy

- Micro-needle

- North America Skin Boosters Market Outlook, by Ingredient, Value (US$ Bn), 2020-2033

- Hyaluronic acid (HA)

- Polydeoxyribonucleotides (PDRN)

- Poly-L-Lactic Acid (PLLA)/ Poly-D, L-Lactic Acid (PDLLA)

- Polycaprolactone (PCL)

- Exosomes

- North America Skin Boosters Market Outlook, by Gender, Value (US$ Bn), 2020-2033

- Female

- Male

- North America Skin Boosters Market Outlook, by End-user, Value (US$ Bn), 2020-2033

- Med spas

- Dermatology Clinics

- North America Skin Boosters Market Outlook, by Country, Value (US$ Bn), 2020-2033

- U.S. Skin Boosters Market Outlook, by Therapy Type, 2020-2033

- U.S. Skin Boosters Market Outlook, by Ingredient, 2020-2033

- U.S. Skin Boosters Market Outlook, by Gender, 2020-2033

- U.S. Skin Boosters Market Outlook, by End-user, 2020-2033

- Canada Skin Boosters Market Outlook, by Therapy Type, 2020-2033

- Canada Skin Boosters Market Outlook, by Ingredient, 2020-2033

- Canada Skin Boosters Market Outlook, by Gender, 2020-2033

- Canada Skin Boosters Market Outlook, by End-user, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- North America Skin Boosters Market Outlook, by Therapy Type, Value (US$ Bn), 2020-2033

- Europe Skin Boosters Market Outlook, 2020 - 2033

- Europe Skin Boosters Market Outlook, by Therapy Type, Value (US$ Bn), 2020-2033

- Mesotherapy

- Micro-needle

- Europe Skin Boosters Market Outlook, by Ingredient, Value (US$ Bn), 2020-2033

- Hyaluronic acid (HA)

- Polydeoxyribonucleotides (PDRN)

- Poly-L-Lactic Acid (PLLA)/ Poly-D, L-Lactic Acid (PDLLA)

- Polycaprolactone (PCL)

- Exosomes

- Europe Skin Boosters Market Outlook, by Gender, Value (US$ Bn), 2020-2033

- Female

- Male

- Europe Skin Boosters Market Outlook, by End-user, Value (US$ Bn), 2020-2033

- Med spas

- Dermatology Clinics

- Europe Skin Boosters Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Germany Skin Boosters Market Outlook, by Therapy Type, 2020-2033

- Germany Skin Boosters Market Outlook, by Ingredient, 2020-2033

- Germany Skin Boosters Market Outlook, by Gender, 2020-2033

- Germany Skin Boosters Market Outlook, by End-user, 2020-2033

- Italy Skin Boosters Market Outlook, by Therapy Type, 2020-2033

- Italy Skin Boosters Market Outlook, by Ingredient, 2020-2033

- Italy Skin Boosters Market Outlook, by Gender, 2020-2033

- Italy Skin Boosters Market Outlook, by End-user, 2020-2033

- France Skin Boosters Market Outlook, by Therapy Type, 2020-2033

- France Skin Boosters Market Outlook, by Ingredient, 2020-2033

- France Skin Boosters Market Outlook, by Gender, 2020-2033

- France Skin Boosters Market Outlook, by End-user, 2020-2033

- U.K. Skin Boosters Market Outlook, by Therapy Type, 2020-2033

- U.K. Skin Boosters Market Outlook, by Ingredient, 2020-2033

- U.K. Skin Boosters Market Outlook, by Gender, 2020-2033

- U.K. Skin Boosters Market Outlook, by End-user, 2020-2033

- Spain Skin Boosters Market Outlook, by Therapy Type, 2020-2033

- Spain Skin Boosters Market Outlook, by Ingredient, 2020-2033

- Spain Skin Boosters Market Outlook, by Gender, 2020-2033

- Spain Skin Boosters Market Outlook, by End-user, 2020-2033

- Russia Skin Boosters Market Outlook, by Therapy Type, 2020-2033

- Russia Skin Boosters Market Outlook, by Ingredient, 2020-2033

- Russia Skin Boosters Market Outlook, by Gender, 2020-2033

- Russia Skin Boosters Market Outlook, by End-user, 2020-2033

- Rest of Europe Skin Boosters Market Outlook, by Therapy Type, 2020-2033

- Rest of Europe Skin Boosters Market Outlook, by Ingredient, 2020-2033

- Rest of Europe Skin Boosters Market Outlook, by Gender, 2020-2033

- Rest of Europe Skin Boosters Market Outlook, by End-user, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Europe Skin Boosters Market Outlook, by Therapy Type, Value (US$ Bn), 2020-2033

- Asia Pacific Skin Boosters Market Outlook, 2020 - 2033

- Asia Pacific Skin Boosters Market Outlook, by Therapy Type, Value (US$ Bn), 2020-2033

- Mesotherapy

- Micro-needle

- Asia Pacific Skin Boosters Market Outlook, by Ingredient, Value (US$ Bn), 2020-2033

- Hyaluronic acid (HA)

- Polydeoxyribonucleotides (PDRN)

- Poly-L-Lactic Acid (PLLA)/ Poly-D, L-Lactic Acid (PDLLA)

- Polycaprolactone (PCL)

- Exosomes

- Asia Pacific Skin Boosters Market Outlook, by Gender, Value (US$ Bn), 2020-2033

- Female

- Male

- Asia Pacific Skin Boosters Market Outlook, by End-user, Value (US$ Bn), 2020-2033

- Med spas

- Dermatology Clinics

- Asia Pacific Skin Boosters Market Outlook, by Country, Value (US$ Bn), 2020-2033

- China Skin Boosters Market Outlook, by Therapy Type, 2020-2033

- China Skin Boosters Market Outlook, by Ingredient, 2020-2033

- China Skin Boosters Market Outlook, by Gender, 2020-2033

- China Skin Boosters Market Outlook, by End-user, 2020-2033

- Japan Skin Boosters Market Outlook, by Therapy Type, 2020-2033

- Japan Skin Boosters Market Outlook, by Ingredient, 2020-2033

- Japan Skin Boosters Market Outlook, by Gender, 2020-2033

- Japan Skin Boosters Market Outlook, by End-user, 2020-2033

- South Korea Skin Boosters Market Outlook, by Therapy Type, 2020-2033

- South Korea Skin Boosters Market Outlook, by Ingredient, 2020-2033

- South Korea Skin Boosters Market Outlook, by Gender, 2020-2033

- South Korea Skin Boosters Market Outlook, by End-user, 2020-2033

- India Skin Boosters Market Outlook, by Therapy Type, 2020-2033

- India Skin Boosters Market Outlook, by Ingredient, 2020-2033

- India Skin Boosters Market Outlook, by Gender, 2020-2033

- India Skin Boosters Market Outlook, by End-user, 2020-2033

- Southeast Asia Skin Boosters Market Outlook, by Therapy Type, 2020-2033

- Southeast Asia Skin Boosters Market Outlook, by Ingredient, 2020-2033

- Southeast Asia Skin Boosters Market Outlook, by Gender, 2020-2033

- Southeast Asia Skin Boosters Market Outlook, by End-user, 2020-2033

- Rest of SAO Skin Boosters Market Outlook, by Therapy Type, 2020-2033

- Rest of SAO Skin Boosters Market Outlook, by Ingredient, 2020-2033

- Rest of SAO Skin Boosters Market Outlook, by Gender, 2020-2033

- Rest of SAO Skin Boosters Market Outlook, by End-user, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Asia Pacific Skin Boosters Market Outlook, by Therapy Type, Value (US$ Bn), 2020-2033

- Latin America Skin Boosters Market Outlook, 2020 - 2033

- Latin America Skin Boosters Market Outlook, by Therapy Type, Value (US$ Bn), 2020-2033

- Mesotherapy

- Micro-needle

- Latin America Skin Boosters Market Outlook, by Ingredient, Value (US$ Bn), 2020-2033

- Hyaluronic acid (HA)

- Polydeoxyribonucleotides (PDRN)

- Poly-L-Lactic Acid (PLLA)/ Poly-D, L-Lactic Acid (PDLLA)

- Polycaprolactone (PCL)

- Exosomes

- Latin America Skin Boosters Market Outlook, by Gender, Value (US$ Bn), 2020-2033

- Female

- Male

- Latin America Skin Boosters Market Outlook, by End-user, Value (US$ Bn), 2020-2033

- Med spas

- Dermatology Clinics

- Latin America Skin Boosters Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Brazil Skin Boosters Market Outlook, by Therapy Type, 2020-2033

- Brazil Skin Boosters Market Outlook, by Ingredient, 2020-2033

- Brazil Skin Boosters Market Outlook, by Gender, 2020-2033

- Brazil Skin Boosters Market Outlook, by End-user, 2020-2033

- Mexico Skin Boosters Market Outlook, by Therapy Type, 2020-2033

- Mexico Skin Boosters Market Outlook, by Ingredient, 2020-2033

- Mexico Skin Boosters Market Outlook, by Gender, 2020-2033

- Mexico Skin Boosters Market Outlook, by End-user, 2020-2033

- Argentina Skin Boosters Market Outlook, by Therapy Type, 2020-2033

- Argentina Skin Boosters Market Outlook, by Ingredient, 2020-2033

- Argentina Skin Boosters Market Outlook, by Gender, 2020-2033

- Argentina Skin Boosters Market Outlook, by End-user, 2020-2033

- Rest of LATAM Skin Boosters Market Outlook, by Therapy Type, 2020-2033

- Rest of LATAM Skin Boosters Market Outlook, by Ingredient, 2020-2033

- Rest of LATAM Skin Boosters Market Outlook, by Gender, 2020-2033

- Rest of LATAM Skin Boosters Market Outlook, by End-user, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Latin America Skin Boosters Market Outlook, by Therapy Type, Value (US$ Bn), 2020-2033

- Middle East & Africa Skin Boosters Market Outlook, 2020 - 2033

- Middle East & Africa Skin Boosters Market Outlook, by Therapy Type, Value (US$ Bn), 2020-2033

- Mesotherapy

- Micro-needle

- Middle East & Africa Skin Boosters Market Outlook, by Ingredient, Value (US$ Bn), 2020-2033

- Hyaluronic acid (HA)

- Polydeoxyribonucleotides (PDRN)

- Poly-L-Lactic Acid (PLLA)/ Poly-D, L-Lactic Acid (PDLLA)

- Polycaprolactone (PCL)

- Exosomes

- Middle East & Africa Skin Boosters Market Outlook, by Gender, Value (US$ Bn), 2020-2033

- Female

- Male

- Middle East & Africa Skin Boosters Market Outlook, by End-user, Value (US$ Bn), 2020-2033

- Med spas

- Dermatology Clinics

- Middle East & Africa Skin Boosters Market Outlook, by Country, Value (US$ Bn), 2020-2033

- GCC Skin Boosters Market Outlook, by Therapy Type, 2020-2033

- GCC Skin Boosters Market Outlook, by Ingredient, 2020-2033

- GCC Skin Boosters Market Outlook, by Gender, 2020-2033

- GCC Skin Boosters Market Outlook, by End-user, 2020-2033

- South Africa Skin Boosters Market Outlook, by Therapy Type, 2020-2033

- South Africa Skin Boosters Market Outlook, by Ingredient, 2020-2033

- South Africa Skin Boosters Market Outlook, by Gender, 2020-2033

- South Africa Skin Boosters Market Outlook, by End-user, 2020-2033

- Egypt Skin Boosters Market Outlook, by Therapy Type, 2020-2033

- Egypt Skin Boosters Market Outlook, by Ingredient, 2020-2033

- Egypt Skin Boosters Market Outlook, by Gender, 2020-2033

- Egypt Skin Boosters Market Outlook, by End-user, 2020-2033

- Nigeria Skin Boosters Market Outlook, by Therapy Type, 2020-2033

- Nigeria Skin Boosters Market Outlook, by Ingredient, 2020-2033

- Nigeria Skin Boosters Market Outlook, by Gender, 2020-2033

- Nigeria Skin Boosters Market Outlook, by End-user, 2020-2033

- Rest of Middle East Skin Boosters Market Outlook, by Therapy Type, 2020-2033

- Rest of Middle East Skin Boosters Market Outlook, by Ingredient, 2020-2033

- Rest of Middle East Skin Boosters Market Outlook, by Gender, 2020-2033

- Rest of Middle East Skin Boosters Market Outlook, by End-user, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Middle East & Africa Skin Boosters Market Outlook, by Therapy Type, Value (US$ Bn), 2020-2033

- Competitive Landscape

- Company Vs Segment Heatmap

- Company Market Share Analysis, 2025

- Competitive Dashboard

- Company Profiles

- Galderma

- Company Overview

- Product Portfolio

- Financial Overview

- Business Strategies and Developments

- AbbVie, Inc (Allergen)

- VAIM Co., Ltd

- Sinclair

- Merz Pharma

- Teoxane

- Medytox, Inc.

- PharmaResearch Co., Ltd.

- Dexlevo Co., Ltd.

- Bloomage Biotechnology

- IBSA Farmaceutici Italia Srl

- ExoCoBio Inc.

- LINKUS GLOBAL Co., Ltd.

- Galderma

- Appendix

- Research Methodology

- Report Assumptions

- Acronyms and Abbreviations

|

BASE YEAR |

HISTORICAL DATA |

FORECAST PERIOD |

UNITS |

|||

|

2025 |

|

2019 - 2024 |

2026 - 2033 |

Value: US$ Billion |

||

|

REPORT FEATURES |

DETAILS |

|

By Therapy Type Coverage |

|

|

By Ingredient Coverage |

|

|

Geographical Coverage |

|

|

Leading Companies |

|

|

Report Highlights |

Key Market Indicators, Macro-micro economic impact analysis, Technological Roadmap, Key Trends, Driver, Restraints, and Future Opportunities & Revenue Pockets, Porter’s 5 Forces Analysis, Historical Trend (2019-2024), Market Estimates and Forecast, Market Dynamics, Industry Trends, Competition Landscape, Category, Region, Country-wise Trends & Analysis, COVID-19 Impact Analysis (Demand and Supply Chain) |