Respiratory Diagnostics Market

Global Respiratory Diagnostics Industry Analysis, Size, Share, Growth, Trends, and Forecast 2023-2030 - (By Product Coverage, By Test Type Coverage, By Disease Coverage, By End User Coverage, By Geographic Coverage and By Company)

Global Respiratory Diagnostics Market Forecast

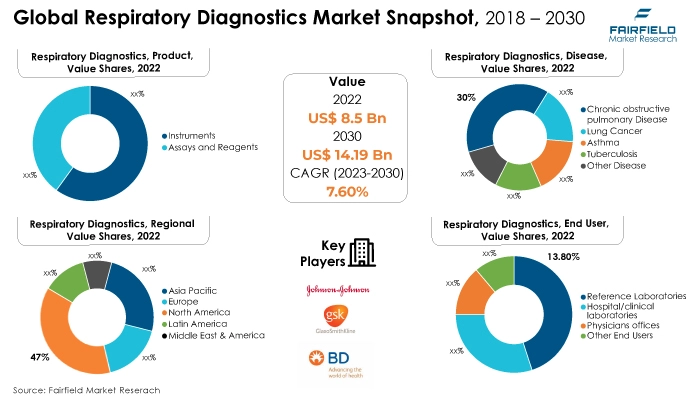

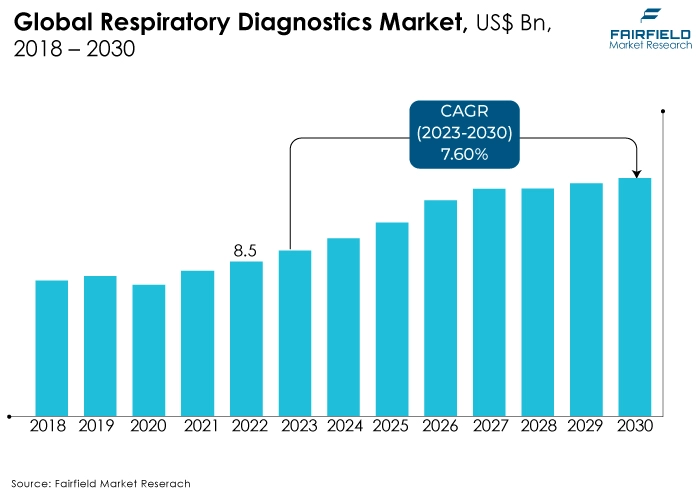

- The respiratory diagnostics market size to jump from US$8.5 Bn (2022) to US$14.19 Bn by 2030-end

- Respiratory diagnostics market revenue projected to witness a CAGR of 7.6% between 2023 and 2030

Quick Report Digest

A Look Back and a Look Forward - Comparative Analysis

The market for respiratory diagnostics is being driven by an increase in demand for respiratory diagnostics devices in various privately owned hospitals and healthcare facilities, as well as initiatives by both government and non-governmental organisations (NGOs) to make quality healthcare facilities available to everyone. Improved research and development (R&D), a growing elderly population, rapid urbanisation, the expansion of industrial facilities, and rising pollution levels globally are other drivers driving the market's growth.

The market witnessed staggered growth during the historical period 2018 - 2022. The market need for sophisticated respiratory diagnostic procedures has increased because of the rising prevalence of respiratory illnesses among people. Smoking and other unhealthy lifestyle habits, which are practiced by people all over the world, have significantly impeded people's ability to breathe easily, which was another significant factor in boosting the market’s growth.

Technology has quickly improved in respiratory ailment testing, which now provides accurate results, mobility, and cost. These are expected to be the market-driving elements that could have the greatest impact on respiratory diagnostics. Increased public-private partnerships and strategic collaborations for funding and implementing new and improved technology will also unlock attractive market prospects.

Key Growth Determinants

- Rise in Geriatric Population

The rise in the number of older people around the world is one of the major factors boosting the market for respiratory diagnostics. According to the World Health Organisation, 8.7 million people globally have tuberculosis, while 50 million people worldwide struggle with occupational lung disease. With advancing age, the respiratory system experiences multiple anatomical, physiological, and immunological changes.

On the other hand, multi-pathologies, and illnesses affect the elderly more frequently. Image diagnostics is a crucial component in the deciphering of sometimes hazy clinical images, which may enable early diagnosis, a major benefit to prompt treatment. The third most common cause of death worldwide now is pulmonary illness.

- Growing Medicinal Cases of Respiratory Disorders

The increased frequency of various types of respiratory illnesses is expected to fuel growth in the global market for respiratory diagnostics. Patients with respiratory diseases like asthma, tuberculosis, and lung cancer, among others, must make sure that the condition remains under control while receiving treatment. Such conditions, even in their mildest versions, can significantly lower one's overall quality of life and, in certain circumstances, even result in death.

One of the most common respiratory conditions, asthma, makes the airways tighten and swell, which increases mucus production. Since there is no known treatment for the condition, patients are limited to treating its symptoms, which might include chest pain or tightness, wheezing during exhalation, shortness of breath, and other more serious signs and symptoms. The demand for efficient diagnostic tools is expected to rise at the same time as the number of persons with numerous respiratory disorders grows.

- Growing Rates of Tobacco Smoking

A surge in disposable money and fast-paced lifestyles have led to an increase in demand for cigarettes because consumers believe that smoking reduces stress and anxiety. Cigarettes may be consumed fast, are simpler to dispose of, and have less odour than other tobacco products.

The increased popularity of flavoured cigarettes, which come in a range of flavours, is expected to enhance demand for combustible cigarettes during the projected period. Another important component in keeping the business alive has been the large companies' overzealous marketing activities. Thus, with the increased prevalence of smoking, the rate of respiratory disorders will increase, driving the market’s growth.

Major Growth Barriers

- Insufficient Medical Reimbursement Policies

There are only a few medical insurance companies or programs that offer compensation for medical diagnoses. Globally, a lot of patients rely heavily on the advantages of payment because, in certain places, including affluent nations, getting a diagnosis can be very expensive.

As the cost of therapy often surpasses the individual's income and, in some cases, the revenue of their entire family, the lack of favourable medical reimbursement may operate as a growth inhibitor for the respiratory diagnostics business. For instance, the cost of treating lung cancer, which requires a precise diagnosis, might reach US$16,000.

- Managing Costs of Research and Product Innovation

The expense of product development and innovation is one of the main issues that the worldwide respiratory diagnostics market participants must deal with. Due to shifting political dynamics, which have a significant impact on transportation costs and variable raw material prices, the world trade situation has been greatly altered.

Furthermore, the escalating circumstances that hint at a looming recession in the next years may also add new difficulties for market players to overcome.

Key Trends and Opportunities to Look at

The increasing investments in the global healthcare sector are expected to help the market for respiratory diagnostics worldwide. Regardless of social, political, or economic background, regional governments and international healthcare organisations work to deliver top-notch medical care to the general people across income ranges.

For instance, the US government spent more than US$4 trillion on healthcare in 2021, an increase of about 2.7%. Similarly, several developing countries have stepped up their efforts to recognise and get around obstacles in the healthcare system.

- Technological Advancements

- Growing Demand for Point-of-Care Diagnostic Devices

Innovation in the respiratory diagnostic system and technical improvements are driving the market's growth. The utilisation of cutting-edge inventions like electronic inhalers and monitoring devices is assisting the rise. Additionally, throughout the projection period, this respiratory diagnostics industry's growth is being supported by rising treatment awareness in both developed and developing countries.

The point-of-care sector is expected to pick up steam in the upcoming years due to the growth in funding from various sources, the rising frequency of the target diseases, and the requirement to deal with the recent coronavirus outbreak. The incorporation of digital technology is expected to have a significant impact on the expansion of POC solutions in areas with limited resources. For POCT players, adopting telehealth as the new norm requires a crucial go-to-market strategy.

How Does the Regulatory Scenario Shape this Industry?

A report titled Respiratory Disease in the World: Realities of Today—Opportunities for Tomorrow was published by the Forum of International Respiratory Societies. The study presents an action plan to prevent and treat the five disorders (chronic obstructive pulmonary disease, tuberculosis, asthma, acute respiratory infections, and lung cancer) that are the main causes of the worldwide burden of respiratory disease.

It educates political decision-makers on the fact that respiratory illnesses are a major contributor to childhood illness and have long-term detrimental effects on adult health, which has repercussions for the national economy.

Prior to the COVID-19 pandemic, respiratory illnesses (those that affect the airways and lungs) were the third leading cause of mortality in England, with 1 in 5 persons having a diagnosis. The British government consequently announced the All Our Health program. A structure of data to direct healthcare workers in illness prevention, health protection, and well-being promotion.

Similarly, the Global Alliance against CRDs (GARD) of the WHO envisions "a world where everyone can breathe easily." GARD focuses on the needs of people with CRDs in low- and middle-income countries.

Fairfield’s Ranking Board

Top Segments

The instruments and devices segment dominated the market in 2022. The healthcare sector must use current technology and gadgets due to the sharp rise in the number of diagnostic procedures performed globally to determine which course of treatment must be taken for a speedier recovery.

Furthermore, the assays and reagents category is projected to experience the fastest market growth. Increased demand for assays in drug discovery, increased funding for research, and an increase in the number of drug discovery businesses are some of the causes driving the assays and reagents industry's expansion.

- Spirometry Tests Continue to Surge Ahead

- Tuberculosis Expected to be the Leading Segment

- Hospitals/Clinical Laboratories Maintain the Lead

Spirometry assists in diagnosing various respiratory conditions such as chronic obstructive pulmonary disease (COPD), asthma, pulmonary fibrosis, and other lung diseases. It helps physicians evaluate lung capacity, airflow limitations, and severity of respiratory conditions.

Additionally, spirometry is crucial in monitoring disease progression and assessing the effectiveness of treatment. By detecting abnormalities in lung function at an early stage, spirometry aids in preventive healthcare. It enables healthcare providers to identify lung diseases even before noticeable symptoms appear, facilitating timely interventions and preventive measures.

The tuberculosis segment dominated the market in 2022. The prevalence of tuberculosis has increased because of numerous regular behaviours, such as smoking and using tobacco, which has greatly fuelled sector expansion.

The lung cancer category is expected to experience the fastest growth within the forecast time frame. As a result of greater cancer awareness in both established and emerging countries, as well as the advent of new medical diagnostic technologies and improved medicines, growth in lung cancer is moving forward in the diagnosis of lung cancer sector.

In 2022, the hospitals/clinical laboratories category led the market growth because the healthcare industry is seeing a growing need for respiratory diagnostic facilities. The expansion of the clinical laboratories sector has emerged as the fastest among all the other rivals because a majority of patients with respiratory ailments present themselves at a hospital.

Moreover, the reference laboratories category is expected to grow fastest in the respiratory diagnostic market during the forecast period. The market technique and penetration volumes are significant, there are many laboratories around the world, and these factors together account for a substantial share.

Regional Frontrunners

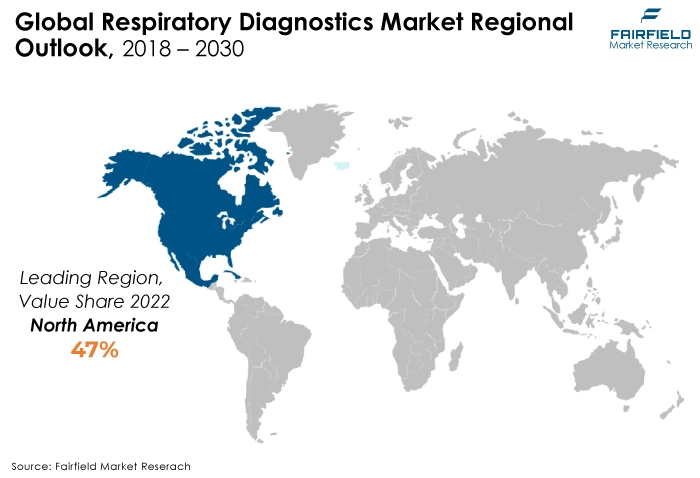

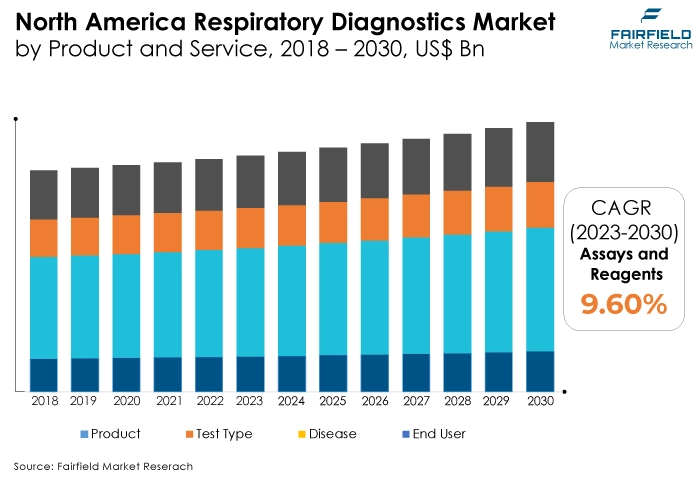

North America Secures the Top Position Globally

North America has emerged as the market with the highest pace of growth for respiratory diagnostics due to the widespread nature of chronic respiratory illnesses in this area. Additionally, a large portion of the population is elderly, which has increased demand for improved respiratory diagnostics services.

Further, the market for respiratory diagnostics has been significantly influenced by the rapid climate change and rising pollution caused by the quick economic growth. The healthcare systems and technical advancements in North America also contribute to this region's dominance. The government's offering of cutting-edge healthcare services to the people has expanded the size of the market for respiratory diagnostics.

Asia Pacific Represents a Lucrative Pocket for Investors

In the upcoming years, the Asia Pacific region is also anticipated to expand. The need for a diagnosis will expand as the region of Asia and the Pacific's healthcare infrastructure continues to advance, and consumer awareness has grown recently.

Due to the rise in the number of respiratory disorders, the market for respiratory diagnostics will expand over the coming years. As a result, numerous businesses are investing significantly in developing the market, and they will be crucial to the development of Asia Pacific throughout the projection period.

Fairfield’s Competitive Landscape Analysis

The global market for respiratory diagnostics is consolidated, with fewer significant companies present worldwide. To increase their global footprint, the major firms are launching new items and enhancing their distribution networks. In addition, Fairfield Market Research anticipates that during the next few years, there will be further market consolidation.

Who are the Leaders in Global Respiratory Diagnostics Space?

- Medtronic

- COSMED SRL

- GENERAL ELECTRIC COMPANY

- Koninklijke Philips N.V.

- Hoffmann-La Roche Ltd

- NIHON KOHDEN CORPORATION

- GC Diagnostics Corporation

- Masimo

- Drägerwerk AG & Co. KGaA

- Bio-Rad Laboratories Inc.

- bioMérieux SA

- Carestream Health

- Abbott

- Johnson & Johnson Services Inc.

- Thermo Fisher Scientific Inc.

Significant Company Developments

New Product Launch

- May 2022: QuantuMDx Group Limited, a UK-based producer of transformative point-of-care diagnostics, announces the release of the Q-POCTM SARS-CoV-2, Flu A/B, and RSV Assay.

- The Q-POC respiratory panel test expands on the Q-POCTM SARS-CoV-2 test, which was introduced in 2021, significantly increasing the Q-POCTM platform and its multiplex capabilities and offering clients with quick, point-of-care testing in a variety of healthcare settings.

- September 2021: Roche introduced three molecular polymerase chain reaction (PCR) diagnostic test panels to identify and distinguish common respiratory illnesses simultaneously. Among the most common respiratory infections are adenovirus (ADV), human metapneumovirus (hMPV), enterovirus/rhinovirus (EV/RV), influenza B, influenza A, respiratory syncytial virus (RSV), and parainfluenza 1, 2, and 3. A single nasopharyngeal swab specimen can be used to run one of the new respiratory test panels designed to screen for influenza and other common respiratory illnesses.

- July 2020: BATM, a leading developer of real-time technology for networking solutions and medical laboratory systems, announced the release of three new diagnostic kits to accelerate COVID-19 and other respiratory disorders detection greatly. The Group anticipates that sales and production of the kits will begin at its Adaltis factory in Italy by the end of Q3/beginning of Q4 2020.

- June 2020: GE Healthcare released Thoracic Care Suite, a collection of eight artificial intelligence (AI) algorithms designed to detect anomalies on chest X-rays, including indications of pneumonia that could indicate COVID-19. Thoracic Care Suite is a suite of eight artificial intelligence (AI) applications developed by the South Korean AI start-up Lunit that are intended to indicate problems for additional assessment by radiologists.

Partnership Agreement

- January 2022: Highmark Health and Bosch announced research cooperation at the CES 2022 convention in Las Vegas, NV, that would investigate the application of novel sensor technologies to capture audio that will be analysed using artificial intelligence to detect paediatric pulmonary disorders such as asthma. The Bosch SoundSee technology was deployed to the International Space Station (ISS) in late 2019 and is now being used to assess system operations aboard the station.

From the Analyst's Perspective

Demand and Future Growth

As per Fairfield’s Analysis, an increase in consumer awareness regarding tuberculosis and lung cancer is driving the market. The rising prevalence of smoking may result in a growth in respiratory disorders, where respiratory diagnostics is favoured, increasing the need for respiratory diagnostics.

Furthermore, technological developments have greatly aided the growth and development of various respiratory diagnostics. However, the respiratory diagnostic market is expected to face considerable challenges because of high initial expenses and difficult reimbursement policies.

Supply Side of the Market

According to our analysis, the manufacturers present in the respiratory diagnostics market are focusing on enhancing test accuracy and competencies by introducing new models in the imaging test sector, which will help doctors identify the disease more efficiently and accurately. Most of respiratory diagnostics equipment is produced and exported by the US.

Furthermore, other activities are happening, such as product launches and approvals, partnerships, collaborations, mergers, and acquisitions that might expand the regional market. For instance, Luisa, a cutting-edge ventilator designed for use in homes, institutions, hospitals, or portable applications for both invasive and non-invasive ventilation, was reportedly released in the US in November 2021, according to Movair.

Additionally, China is the top supplier of respiratory diagnostics devices in Asia and the Pacific. For instance, China supplied about 3,800 tonnes of pharmaceuticals and medical supplies to India in May 2021, along with over 26,000 ventilators and oxygen concentrators, over 15,000 patient monitors, and over 26,000 patient monitors. Indian customers ordered more than 70,000 oxygen concentrators from Chinese manufacturers.

Global Respiratory Diagnostic Market is Segmented as Below:

By Product:

- Instruments

- Assays and Reagents

By Test Type:

- Spirometry

- Peak Flow Measurement

- Pulse Oximetry

- Arterial Blood Gas (ABG) Test

- Chest X-ray

- CT (Computed Tomography) Scan

- MRI (Magnetic Resonance Imaging)

- Bronchoscopy

- Pulmonary Function Tests (PFTs)

- Methacholine Challenge Test

- Nasal Smear or Swab

By Disease:

- Chronic Obstructive Pulmonary Disease

- Lung Cancer

- Asthma

- Tuberculosis

- Other Disease

By End User:

- Hospitals/Clinical Laboratories

- Physician Offices

- Reference Laboratories

- Other End Users

By Geographic Coverage:

- North America

- U.S.

- Canada

- Europe

- Germany

- U.K.

- France

- Italy

- Turkey

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Egypt

- Nigeria

- Rest of Middle East & Africa

1. Executive Summary

1.1. Global Respiratory Diagnostics Market Snapshot

1.2. Future Projections

1.3. Key Market Trends

1.4. Regional Snapshot, by Value, 2022

1.5. Analyst Recommendations

2. Market Overview

2.1. Market Definitions and Segmentations

2.2. Market Dynamics

2.2.1. Drivers

2.2.2. Restraints

2.2.3. Market Opportunities

2.3. Value Chain Analysis

2.4. Porter’s Five Forces Analysis

2.5. Covid-19 Impact Analysis

2.5.1. Supply

2.5.2. Demand

2.6. Impact of Ukraine-Russia Conflict

2.7. Economic Overview

2.7.1. World Economic Projections

2.8. PESTLE Analysis

3. Global Respiratory Diagnostics Market Outlook, 2018 - 2030

3.1. Global Respiratory Diagnostics Market Outlook, by Product, Value (US$ Bn), 2018 - 2030

3.1.1. Key Highlights

3.1.1.1. Instruments

3.1.1.2. Assays and Reagents

3.2. Global Respiratory Diagnostics Market Outlook, by Test Type, Value (US$ Bn), 2018 - 2030

3.2.1. Key Highlights

3.2.1.1. Spirometry

3.2.1.2. Peak Flow Measurement

3.2.1.3. Pulse Oximetry

3.2.1.4. Arterial Blood Gas (ABG) Test

3.2.1.5. Chest X-ray

3.2.1.6. CT (Computed Tomography) Scan

3.2.1.7. MRI (Magnetic Resonance Imaging)

3.2.1.8. Bronchoscopy

3.2.1.9. Pulmonary Function Tests (PFTs)

3.2.1.10. Methacholine Challenge Test

3.2.1.11. Nasal Smear or Swab

3.3. Global Respiratory Diagnostics Market Outlook, by Disease, Value (US$ Bn), 2018 - 2030

3.3.1. Key Highlights

3.3.1.1. Chronic Obstructive Pulmonary Disease

3.3.1.2. Lung Cancer

3.3.1.3. Asthma

3.3.1.4. Tuberculosis

3.3.1.5. Other Disease

3.4. Global Respiratory Diagnostics Market Outlook, by End User, Value (US$ Bn), 2018 - 2030

3.4.1. Key Highlights Snacks

3.4.1.1. Hospitals/Clinical Laboratories

3.4.1.2. Physician Offices

3.4.1.3. Reference Laboratories

3.4.1.4. Other End Users

3.5. Global Respiratory Diagnostics Market Outlook, by Region, Value (US$ Bn), 2018 - 2030

3.5.1. Key Highlights

3.5.1.1. North America

3.5.1.2. Europe

3.5.1.3. Asia Pacific

3.5.1.4. Latin America

3.5.1.5. Middle East & Africa

4. North America Respiratory Diagnostics Market Outlook, 2018 - 2030

4.1. North America Respiratory Diagnostics Market Outlook, by Product, Value (US$ Bn), 2018 - 2030

4.1.1. Key Highlights

4.1.1.1. Instruments

4.1.1.2. Assays and Reagents

4.2. North America Respiratory Diagnostics Market Outlook, by Test Type, Value (US$ Bn), 2018 - 2030

4.2.1. Key Highlights

4.2.1.1. Spirometry

4.2.1.2. Peak Flow Measurement

4.2.1.3. Pulse Oximetry

4.2.1.4. Arterial Blood Gas (ABG) Test

4.2.1.5. Chest X-ray

4.2.1.6. CT (Computed Tomography) Scan

4.2.1.7. MRI (Magnetic Resonance Imaging)

4.2.1.8. Bronchoscopy

4.2.1.9. Pulmonary Function Tests (PFTs)

4.2.1.10. Methacholine Challenge Test

4.2.1.11. Nasal Smear or Swab

4.3. North America Respiratory Diagnostics Market Outlook, by Disease, Value (US$ Bn), 2018 - 2030

4.3.1. Key Highlights

4.3.1.1. Chronic Obstructive Pulmonary Disease

4.3.1.2. Lung Cancer

4.3.1.3. Asthma

4.3.1.4. Tuberculosis

4.3.1.5. Other Disease

4.4. North America Respiratory Diagnostics Market Outlook, by End User, Value (US$ Bn), 2018 - 2030

4.4.1. Key Highlights

4.4.1.1. Hospitals/Clinical Laboratories

4.4.1.2. Physician Offices

4.4.1.3. Reference Laboratories

4.4.1.4. Other End Users

4.4.2. BPS Analysis/Market Attractiveness Analysis

4.5. North America Respiratory Diagnostics Market Outlook, by Country, Value (US$ Bn), 2018 - 2030

4.5.1. Key Highlights

4.5.1.1. U.S. Respiratory Diagnostics Market by Product, Value (US$ Bn), 2018 - 2030

4.5.1.2. U.S. Respiratory Diagnostics Market by Test Type, Value (US$ Bn), 2018 - 2030

4.5.1.3. U.S. Respiratory Diagnostics Market by Disease, Value (US$ Bn), 2018 - 2030

4.5.1.4. U.S. Respiratory Diagnostics Market by End User, Value (US$ Bn), 2018 - 2030

4.5.1.5. Canada Respiratory Diagnostics Market by Product, Value (US$ Bn), 2018 - 2030

4.5.1.6. Canada Respiratory Diagnostics Market by Test Type, Value (US$ Bn), 2018 - 2030

4.5.1.7. Canada Respiratory Diagnostics Market by Disease, Value (US$ Bn), 2018 - 2030

4.5.1.8. Canada Respiratory Diagnostics Market by End User, Value (US$ Bn), 2018 - 2030

4.5.2. BPS Analysis/Market Attractiveness Analysis

5. Europe Respiratory Diagnostics Market Outlook, 2018 - 2030

5.1. Europe Respiratory Diagnostics Market Outlook, by Product, Value (US$ Bn), 2018 - 2030

5.1.1. Key Highlights

5.1.1.1. Instruments

5.1.1.2. Assays and Reagents

5.2. Europe Respiratory Diagnostics Market Outlook, by Test Type, Value (US$ Bn), 2018 - 2030

5.2.1. Key Highlights

5.2.1.1. Spirometry

5.2.1.2. Peak Flow Measurement

5.2.1.3. Pulse Oximetry

5.2.1.4. Arterial Blood Gas (ABG) Test

5.2.1.5. Chest X-ray

5.2.1.6. CT (Computed Tomography) Scan

5.2.1.7. MRI (Magnetic Resonance Imaging)

5.2.1.8. Bronchoscopy

5.2.1.9. Pulmonary Function Tests (PFTs)

5.2.1.10. Methacholine Challenge Test

5.2.1.11. Nasal Smear or Swab

5.3. Europe Respiratory Diagnostics Market Outlook, by Disease, Value (US$ Bn), 2018 - 2030

5.3.1. Key Highlights

5.3.1.1. Chronic Obstructive Pulmonary Disease

5.3.1.2. Lung Cancer

5.3.1.3. Asthma

5.3.1.4. Tuberculosis

5.3.1.5. Other Disease

5.4. Europe Respiratory Diagnostics Market Outlook, by End User, Value (US$ Bn), 2018 - 2030

5.4.1. Key Highlights

5.4.1.1. Hospitals/Clinical Laboratories

5.4.1.2. Physician Offices

5.4.1.3. Reference Laboratories

5.4.1.4. Other End Users

5.4.2. BPS Analysis/Market Attractiveness Analysis

5.5. Europe Respiratory Diagnostics Market Outlook, by Country, Value (US$ Bn), 2018 - 2030

5.5.1. Key Highlights

5.5.1.1. Germany Respiratory Diagnostics Market by Product, Value (US$ Bn), 2018 - 2030

5.5.1.2. Germany Respiratory Diagnostics Market by Test Type, Value (US$ Bn), 2018 - 2030

5.5.1.3. Germany Respiratory Diagnostics Market by Disease, Value (US$ Bn), 2018 - 2030

5.5.1.4. Germany Respiratory Diagnostics Market by End User, Value (US$ Bn), 2018 - 2030

5.5.1.5. U.K. Respiratory Diagnostics Market by Product, Value (US$ Bn), 2018 - 2030

5.5.1.6. U.K. Respiratory Diagnostics Market by Test Type, Value (US$ Bn), 2018 - 2030

5.5.1.7. U.K. Respiratory Diagnostics Market by Disease, Value (US$ Bn), 2018 - 2030

5.5.1.8. U.K. Respiratory Diagnostics Market by End User, Value (US$ Bn), 2018 - 2030

5.5.1.9. France Respiratory Diagnostics Market by Product, Value (US$ Bn), 2018 - 2030

5.5.1.10. France Respiratory Diagnostics Market by Test Type, Value (US$ Bn), 2018 - 2030

5.5.1.11. France Respiratory Diagnostics Market by Disease, Value (US$ Bn), 2018 - 2030

5.5.1.12. France Respiratory Diagnostics Market by End User, Value (US$ Bn), 2018 - 2030

5.5.1.13. Italy Respiratory Diagnostics Market by Product, Value (US$ Bn), 2018 - 2030

5.5.1.14. Italy Respiratory Diagnostics Market by Test Type, Value (US$ Bn), 2018 - 2030

5.5.1.15. Italy Respiratory Diagnostics Market by Disease, Value (US$ Bn), 2018 - 2030

5.5.1.16. Italy Respiratory Diagnostics Market by End User, Value (US$ Bn), 2018 - 2030

5.5.1.17. Turkey Respiratory Diagnostics Market by Product, Value (US$ Bn), 2018 - 2030

5.5.1.18. Turkey Respiratory Diagnostics Market by Test Type, Value (US$ Bn), 2018 - 2030

5.5.1.19. Turkey Respiratory Diagnostics Market by Disease, Value (US$ Bn), 2018 - 2030

5.5.1.20. Turkey Respiratory Diagnostics Market by End User, Value (US$ Bn), 2018 - 2030

5.5.1.21. Russia Respiratory Diagnostics Market by Product, Value (US$ Bn), 2018 - 2030

5.5.1.22. Russia Respiratory Diagnostics Market by Test Type, Value (US$ Bn), 2018 - 2030

5.5.1.23. Russia Respiratory Diagnostics Market by Disease, Value (US$ Bn), 2018 - 2030

5.5.1.24. Russia Respiratory Diagnostics Market by End User, Value (US$ Bn), 2018 - 2030

5.5.1.25. Rest of Europe Respiratory Diagnostics Market by Product, Value (US$ Bn), 2018 - 2030

5.5.1.26. Rest of Europe Respiratory Diagnostics Market by Test Type, Value (US$ Bn), 2018 - 2030

5.5.1.27. Rest of Europe Respiratory Diagnostics Market by Disease, Value (US$ Bn), 2018 - 2030

5.5.1.28. Rest of Europe Respiratory Diagnostics Market by End User, Value (US$ Bn), 2018 - 2030

5.5.2. BPS Analysis/Market Attractiveness Analysis

6. Asia Pacific Respiratory Diagnostics Market Outlook, 2018 - 2030

6.1. Asia Pacific Respiratory Diagnostics Market Outlook, by Product, Value (US$ Bn), 2018 - 2030

6.1.1. Key Highlights

6.1.1.1. Instruments

6.1.1.2. Assays and Reagents

6.2. Asia Pacific Respiratory Diagnostics Market Outlook, by Test Type, Value (US$ Bn), 2018 - 2030

6.2.1. Key Highlights

6.2.1.1. Spirometry

6.2.1.2. Peak Flow Measurement

6.2.1.3. Pulse Oximetry

6.2.1.4. Arterial Blood Gas (ABG) Test

6.2.1.5. Chest X-ray

6.2.1.6. CT (Computed Tomography) Scan

6.2.1.7. MRI (Magnetic Resonance Imaging)

6.2.1.8. Bronchoscopy

6.2.1.9. Pulmonary Function Tests (PFTs)

6.2.1.10. Methacholine Challenge Test

6.2.1.11. Nasal Smear or Swab

6.3. Asia Pacific Respiratory Diagnostics Market Outlook, by Disease, Value (US$ Bn), 2018 - 2030

6.3.1. Key Highlights

6.3.1.1. Chronic Obstructive Pulmonary Disease

6.3.1.2. Lung Cancer

6.3.1.3. Asthma

6.3.1.4. Tuberculosis

6.3.1.5. Other Disease

6.4. Asia Pacific Respiratory Diagnostics Market Outlook, by End User, Value (US$ Bn), 2018 - 2030

6.4.1. Key Highlights

6.4.1.1. Hospitals/Clinical Laboratories

6.4.1.2. Physician Offices

6.4.1.3. Reference Laboratories

6.4.1.4. Other End Users

6.4.2. BPS Analysis/Market Attractiveness Analysis

6.5. Asia Pacific Respiratory Diagnostics Market Outlook, by Country, Value (US$ Bn), 2018 - 2030

6.5.1. Key Highlights

6.5.1.1. China Respiratory Diagnostics Market by Product, Value (US$ Bn), 2018 - 2030

6.5.1.2. China Respiratory Diagnostics Market by Test Type, Value (US$ Bn), 2018 - 2030

6.5.1.3. China Respiratory Diagnostics Market by Disease, Value (US$ Bn), 2018 - 2030

6.5.1.4. China Respiratory Diagnostics Market by End User, Value (US$ Bn), 2018 - 2030

6.5.1.5. Japan Respiratory Diagnostics Market by Product, Value (US$ Bn), 2018 - 2030

6.5.1.6. Japan Respiratory Diagnostics Market by Test Type, Value (US$ Bn), 2018 - 2030

6.5.1.7. Japan Respiratory Diagnostics Market by Disease, Value (US$ Bn), 2018 - 2030

6.5.1.8. Japan Respiratory Diagnostics Market by End User, Value (US$ Bn), 2018 - 2030

6.5.1.9. South Korea Respiratory Diagnostics Market by Product, Value (US$ Bn), 2018 - 2030

6.5.1.10. South Korea Respiratory Diagnostics Market by Test Type, Value (US$ Bn), 2018 - 2030

6.5.1.11. South Korea Respiratory Diagnostics Market by Disease, Value (US$ Bn), 2018 - 2030

6.5.1.12. South Korea Respiratory Diagnostics Market by End User, Value (US$ Bn), 2018 - 2030

6.5.1.13. India Respiratory Diagnostics Market by Product, Value (US$ Bn), 2018 - 2030

6.5.1.14. India Respiratory Diagnostics Market by Test Type, Value (US$ Bn), 2018 - 2030

6.5.1.15. India Respiratory Diagnostics Market by Disease, Value (US$ Bn), 2018 - 2030

6.5.1.16. India Respiratory Diagnostics Market by End User, Value (US$ Bn), 2018 - 2030

6.5.1.17. Southeast Asia Respiratory Diagnostics Market by Product, Value (US$ Bn), 2018 - 2030

6.5.1.18. Southeast Asia Respiratory Diagnostics Market by Test Type, Value (US$ Bn), 2018 - 2030

6.5.1.19. Southeast Asia Respiratory Diagnostics Market by Disease, Value (US$ Bn), 2018 - 2030

6.5.1.20. Southeast Asia Respiratory Diagnostics Market by End User, Value (US$ Bn), 2018 - 2030

6.5.1.21. Rest of Asia Pacific Respiratory Diagnostics Market by Product, Value (US$ Bn), 2018 - 2030

6.5.1.22. Rest of Asia Pacific Respiratory Diagnostics Market by Test Type, Value (US$ Bn), 2018 - 2030

6.5.1.23. Rest of Asia Pacific Respiratory Diagnostics Market by Disease, Value (US$ Bn), 2018 - 2030

6.5.1.24. Rest of Asia Pacific Respiratory Diagnostics Market by End User, Value (US$ Bn), 2018 - 2030

6.5.2. BPS Analysis/Market Attractiveness Analysis

7. Latin America Respiratory Diagnostics Market Outlook, 2018 - 2030

7.1. Latin America Respiratory Diagnostics Market Outlook, by Product, Value (US$ Bn), 2018 - 2030

7.1.1. Key Highlights

7.1.1.1. Instruments

7.1.1.2. Assays and Reagents

7.2. Latin America Respiratory Diagnostics Market Outlook, by Test Type, Value (US$ Bn), 2018 - 2030

7.2.1. Key Highlights

7.2.1.1. Spirometry

7.2.1.2. Peak Flow Measurement

7.2.1.3. Pulse Oximetry

7.2.1.4. Arterial Blood Gas (ABG) Test

7.2.1.5. Chest X-ray

7.2.1.6. CT (Computed Tomography) Scan

7.2.1.7. MRI (Magnetic Resonance Imaging)

7.2.1.8. Bronchoscopy

7.2.1.9. Pulmonary Function Tests (PFTs)

7.2.1.10. Methacholine Challenge Test

7.2.1.11. Nasal Smear or Swab

7.3. Latin America Respiratory Diagnostics Market Outlook, by Disease, Value (US$ Bn), 2018 - 2030

7.3.1. Key Highlights

7.3.1.1. Chronic Obstructive Pulmonary Disease

7.3.1.2. Lung Cancer

7.3.1.3. Asthma

7.3.1.4. Tuberculosis

7.3.1.5. Other Disease

7.4. Latin America Respiratory Diagnostics Market Outlook, by End User, Value (US$ Bn), 2018 - 2030

7.4.1. Key Highlights

7.4.1.1. Hospitals/Clinical Laboratories

7.4.1.2. Physician Offices

7.4.1.3. Reference Laboratories

7.4.1.4. Other End Users

7.4.2. BPS Analysis/Market Attractiveness Analysis

7.5. Latin America Respiratory Diagnostics Market Outlook, by Country, Value (US$ Bn), 2018 - 2030

7.5.1. Key Highlights

7.5.1.1. Brazil Respiratory Diagnostics Market by Product, Value (US$ Bn), 2018 - 2030

7.5.1.2. Brazil Respiratory Diagnostics Market by Test Type, Value (US$ Bn), 2018 - 2030

7.5.1.3. Brazil Respiratory Diagnostics Market by Disease, Value (US$ Bn), 2018 - 2030

7.5.1.4. Brazil Respiratory Diagnostics Market by End User, Value (US$ Bn), 2018 - 2030

7.5.1.5. Mexico Respiratory Diagnostics Market by Product, Value (US$ Bn), 2018 - 2030

7.5.1.6. Mexico Respiratory Diagnostics Market by Test Type, Value (US$ Bn), 2018 - 2030

7.5.1.7. Mexico Respiratory Diagnostics Market by Disease, Value (US$ Bn), 2018 - 2030

7.5.1.8. Mexico Respiratory Diagnostics Market by End User, Value (US$ Bn), 2018 - 2030

7.5.1.9. Argentina Respiratory Diagnostics Market by Product, Value (US$ Bn), 2018 - 2030

7.5.1.10. Argentina Respiratory Diagnostics Market by Test Type, Value (US$ Bn), 2018 - 2030

7.5.1.11. Argentina Respiratory Diagnostics Market by Disease, Value (US$ Bn), 2018 - 2030

7.5.1.12. Argentina Respiratory Diagnostics Market by End User, Value (US$ Bn), 2018 - 2030

7.5.1.13. Rest of Latin America Respiratory Diagnostics Market by Product, Value (US$ Bn), 2018 - 2030

7.5.1.14. Rest of Latin America Respiratory Diagnostics Market by Test Type, Value (US$ Bn), 2018 - 2030

7.5.1.15. Rest of Latin America Respiratory Diagnostics Market by Disease, Value (US$ Bn), 2018 - 2030

7.5.1.16. Rest of Latin America Respiratory Diagnostics Market by End User, Value (US$ Bn), 2018 - 2030

7.5.2. BPS Analysis/Market Attractiveness Analysis

8. Middle East & Africa Respiratory Diagnostics Market Outlook, 2018 - 2030

8.1. Middle East & Africa Respiratory Diagnostics Market Outlook, by Product, Value (US$ Bn), 2018 - 2030

8.1.1. Key Highlights

8.1.1.1. Instruments

8.1.1.2. Assays and Reagents

8.2. Middle East & Africa Respiratory Diagnostics Market Outlook, by Test Type, Value (US$ Bn), 2018 - 2030

8.2.1. Key Highlights

8.2.1.1. Spirometry

8.2.1.2. Peak Flow Measurement

8.2.1.3. Pulse Oximetry

8.2.1.4. Arterial Blood Gas (ABG) Test

8.2.1.5. Chest X-ray

8.2.1.6. CT (Computed Tomography) Scan

8.2.1.7. MRI (Magnetic Resonance Imaging)

8.2.1.8. Bronchoscopy

8.2.1.9. Pulmonary Function Tests (PFTs)

8.2.1.10. Methacholine Challenge Test

8.2.1.11. Nasal Smear or Swab

8.3. Middle East & Africa Respiratory Diagnostics Market Outlook, by Disease, Value (US$ Bn), 2018 - 2030

8.3.1. Key Highlights

8.3.1.1. Chronic Obstructive Pulmonary Disease

8.3.1.2. Lung Cancer

8.3.1.3. Asthma

8.3.1.4. Tuberculosis

8.3.1.5. Other Disease

8.4. Middle East & Africa Respiratory Diagnostics Market Outlook, by End User, Value (US$ Bn), 2018 - 2030

8.4.1. Key Highlights

8.4.1.1. Hospitals/Clinical Laboratories

8.4.1.2. Physician Offices

8.4.1.3. Reference Laboratories

8.4.1.4. Other End Users

8.4.2. BPS Analysis/Market Attractiveness Analysis

8.5. Middle East & Africa Respiratory Diagnostics Market Outlook, by Country, Value (US$ Bn), 2018 - 2030

8.5.1. Key Highlights

8.5.1.1. GCC Respiratory Diagnostics Market by Product, Value (US$ Bn), 2018 - 2030

8.5.1.2. GCC Respiratory Diagnostics Market by Test Type, Value (US$ Bn), 2018 - 2030

8.5.1.3. GCC Respiratory Diagnostics Market by Disease, Value (US$ Bn), 2018 - 2030

8.5.1.4. GCC Respiratory Diagnostics Market by End User, Value (US$ Bn), 2018 - 2030

8.5.1.5. South Africa Respiratory Diagnostics Market by Product, Value (US$ Bn), 2018 - 2030

8.5.1.6. South Africa Respiratory Diagnostics Market by Test Type, Value (US$ Bn), 2018 - 2030

8.5.1.7. South Africa Respiratory Diagnostics Market by Disease, Value (US$ Bn), 2018 - 2030

8.5.1.8. South Africa Respiratory Diagnostics Market by End User, Value (US$ Bn), 2018 - 2030

8.5.1.9. Egypt Respiratory Diagnostics Market by Product, Value (US$ Bn), 2018 - 2030

8.5.1.10. Egypt Respiratory Diagnostics Market by Test Type, Value (US$ Bn), 2018 - 2030

8.5.1.11. Egypt Respiratory Diagnostics Market by Disease, Value (US$ Bn), 2018 - 2030

8.5.1.12. Egypt Respiratory Diagnostics Market by End User, Value (US$ Bn), 2018 - 2030

8.5.1.13. Nigeria Respiratory Diagnostics Market by Product, Value (US$ Bn), 2018 - 2030

8.5.1.14. Nigeria Respiratory Diagnostics Market by Test Type, Value (US$ Bn), 2018 - 2030

8.5.1.15. Nigeria Respiratory Diagnostics Market by Disease, Value (US$ Bn), 2018 - 2030

8.5.1.16. Nigeria Respiratory Diagnostics Market by End User, Value (US$ Bn), 2018 - 2030

8.5.1.17. Rest of Middle East & Africa Respiratory Diagnostics Market by Product, Value (US$ Bn), 2018 - 2030

8.5.1.18. Rest of Middle East & Africa Respiratory Diagnostics Market by Test Type, Value (US$ Bn), 2018 - 2030

8.5.1.19. Rest of Middle East & Africa Respiratory Diagnostics Market by Disease, Value (US$ Bn), 2018 - 2030

8.5.1.20. Rest of Middle East & Africa Respiratory Diagnostics Market by End User, Value (US$ Bn), 2018 - 2030

8.5.2. BPS Analysis/Market Attractiveness Analysis

9. Competitive Landscape

9.1. Capacity vs Application Heatmap

9.2. Manufacturer vs Application Heatmap

9.3. Company Market Share Analysis, 2022

9.4. Competitive Dashboard

9.5. Company Profiles

9.5.1. Medtronic (Ireland)

9.5.1.1. Company Overview

9.5.1.2. Product Portfolio

9.5.1.3. Financial Overview

9.5.1.4. Business Strategies and Development

9.5.2. COSMED srl (Italy)

9.5.2.1. Company Overview

9.5.2.2. Product Portfolio

9.5.2.3. Financial Overview

9.5.2.4. Business Strategies and Development

9.5.3. GENERAL ELECTRIC COMPANY (US)

9.5.3.1. Company Overview

9.5.3.2. Product Portfolio

9.5.3.3. Financial Overview

9.5.3.4. Business Strategies and Development

9.5.4. Koninklijke Philips N.V. (Netherlands)

9.5.4.1. Company Overview

9.5.4.2. Product Portfolio

9.5.4.3. Financial Overview

9.5.4.4. Business Strategies and Development

9.5.5. Hoffmann-La Roche Ltd (Switzerland)

9.5.5.1. Company Overview

9.5.5.2. Product Portfolio

9.5.5.3. Financial Overview

9.5.5.4. Business Strategies and Development

9.5.6. NIHON KOHDEN CORPORATION (Japan)

9.5.6.1. Company Overview

9.5.6.2. Product Portfolio

9.5.6.3. Financial Overview

9.5.6.4. Business Strategies and Development

9.5.7. GC Diagnostics Corporation (South Korea)

9.5.7.1. Company Overview

9.5.7.2. Product Portfolio

9.5.7.3. Financial Overview

9.5.7.4. Business Strategies and Development

9.5.8. Masimo (US)

9.5.8.1. Company Overview

9.5.8.2. Product Portfolio

9.5.8.3. Financial Overview

9.5.8.4. Business Strategies and Development

9.5.9. Drägerwerk AG & Co. KGaA (Germany)

9.5.9.1. Company Overview

9.5.9.2. Product Portfolio

9.5.9.3. Financial Overview

9.5.9.4. Business Strategies and Development

9.5.10. Bio-Rad Laboratories Inc. (US)

9.5.10.1. Company Overview

9.5.10.2. Product Portfolio

9.5.10.3. Financial Overview

9.5.10.4. Business Strategies and Development

9.5.11. bioMérieux SA (France)

9.5.11.1. Company Overview

9.5.11.2. Product Portfolio

9.5.11.3. Financial Overview

9.5.11.4. Business Strategies and Development

9.5.12. Carestream Health (US)

9.5.12.1. Company Overview

9.5.12.2. Product Portfolio

9.5.12.3. Financial Overview

9.5.12.4. Business Strategies and Development

9.5.13. Abbott (US)

9.5.13.1. Company Overview

9.5.13.2. Product Portfolio

9.5.13.3. Financial Overview

9.5.13.4. Business Strategies and Development

9.5.14. Johnson & Johnson Services Inc. (US)

9.5.14.1. Company Overview

9.5.14.2. Product Portfolio

9.5.14.3. Financial Overview

9.5.14.4. Business Strategies and Development

9.5.15. Thermo Fisher Scientific Inc. (US)

9.5.15.1. Company Overview

9.5.15.2. Product Portfolio

9.5.15.3. Financial Overview

9.5.15.4. Business Strategies and Development

10. Appendix

10.1. Research Methodology

10.2. Report Assumptions

10.3. Acronyms and Abbreviations

|

BASE YEAR |

HISTORICAL DATA |

FORECAST PERIOD |

UNITS |

|||

|

2022 |

|

2018 - 2022 |

2023 - 2030 |

Value: US$ Million |

||

|

REPORT FEATURES |

DETAILS |

|

Product Coverage |

|

|

Test Type Coverage |

|

|

Disease Coverage |

|

|

End User Coverage |

|

|

Geographical Coverage |

|

|

Leading Companies |

|

|

Report Highlights |

Key Market Indicators, Macro-micro economic impact analysis, Technological Roadmap, Key Trends, Driver, Restraints, and Future Opportunities & Revenue Pockets, Porter’s 5 Forces Analysis, Historical Trend (2019-2021), Market Estimates and Forecast, Market Dynamics, Industry Trends, Competition Landscape, Category, Region, Country-wise Trends & Analysis, COVID-19 Impact Analysis (Demand and Supply Chain) |

Our Research Methodology

Considering the volatility of business today, traditional approaches to strategizing a game plan can be unfruitful if not detrimental. True ambiguity is no way to determine a forecast. A myriad of predetermined factors must be accounted for such as the degree of risk involved, the magnitude of circumstances, as well as conditions or consequences that are not known or unpredictable. To circumvent binary views that cast uncertainty, the application of market research intelligence to strategically posture, move, and enable actionable outcomes is necessary.

View Methodology

Quality Assured

Rigorous Validation Process

Confidentiality Assured

End-to-end Data Security

Custom Research Services

Tailored To Your Objectives

FAQs

In 2022, the global respiratory diagnostic market achieved a size of US$8.5 Bn.

North America holds the largest share in the global respiratory diagnostic market.

The market is expanding on the back of the factors including the rise in geriatric population, lung-related disorders and infections, and technological advancements.

In 2022, the instruments and devices category held a major share of the global market.

The tuberculosis segment constitutes a major share of the global respiratory diagnostics market.

Related Reports

Aortic Stent Grafts Market Insights, Competitive Landscape, and Market Forecast 2033

The aortic stent grafts market is forecast to reach US$5.45 billion by 2033 from US$3.80 billion in 2026, registering a 5.3% CAGR over the forecast period.

Fructosamine Test Market Insights, Competitive Landscape, and Market Forecast - 2033

The Fructosamine Test Market is projected to grow from USD 382.2 Million in 2026 to USD 545 Million by 2033, at a CAGR of 5.2%

Urothelial Carcinoma Diagnostics Market Insights, Competitive Landscape, and Market Forecast - 2033

The Urothelial Carcinoma Diagnostics Market is expected to grow from USD 2.1 Billion in 2026 to USD 4 Billion by 2033, registering a CAGR of 9.8%

Prefilled Syringes Market Insights, Competitive Landscape, and Market Forecast - 2033

The Prefilled Syringes Market is expected to grow from USD 2.8 Billion in 2026 to USD 5.1 Billion by 2033, registering a CAGR of 8.8%

Biofilm Treatment Market Insights, Competitive Landscape, and Market Forecast - 2033

The Biofilm Treatment Market is expected to grow from USD 2.5 Billion in 2026 to USD 4.4 Billion by 2033, registering a CAGR of 8.5%

Elastomeric Infusion Pumps Market Insights, Competitive Landscape, and Market Forecast - 2033

The Elastomeric Infusion Pumps Market is expected to grow from USD 1.3 Billion in 2026 to USD 2.1 Billion by 2033, registering a CAGR of 7.3%