Vegan Mayonnaise Market

Global Vegan Mayonnaise Industry Analysis, Size, Share, Growth, Trends, and Forecast 2026-2033 – (By Product Type ,By End-user, By Distribution Channel, By Geographic Coverage and By Company)

Global Vegan Mayonnaise Market: Strategic Analysis 2026-2033

Executive Summary & Key Highlights

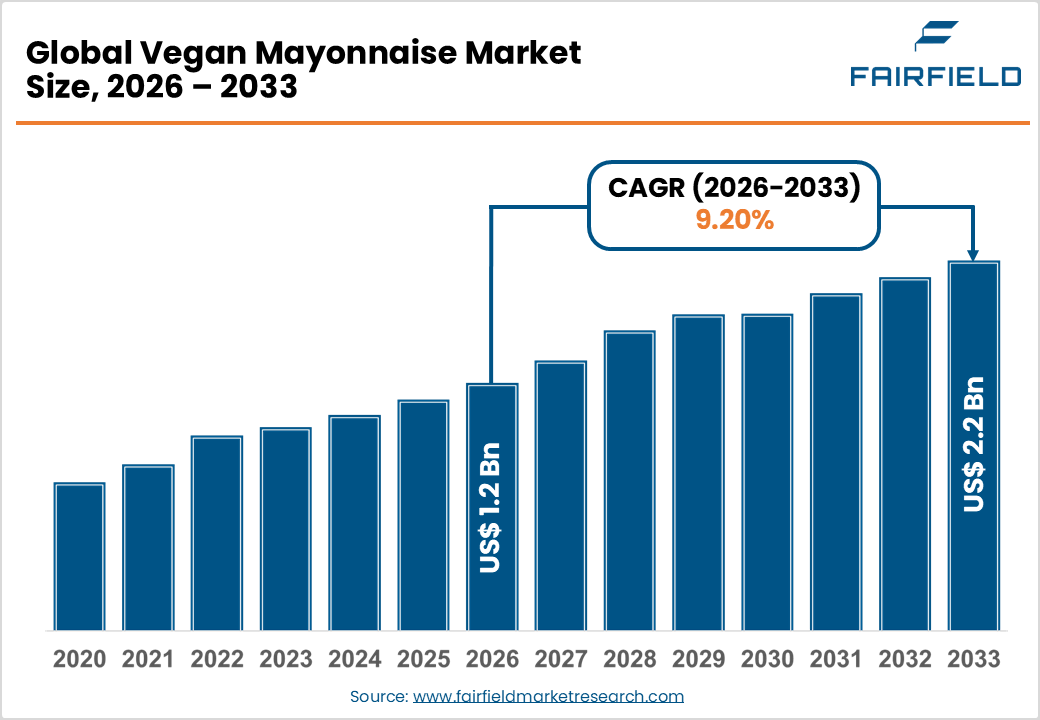

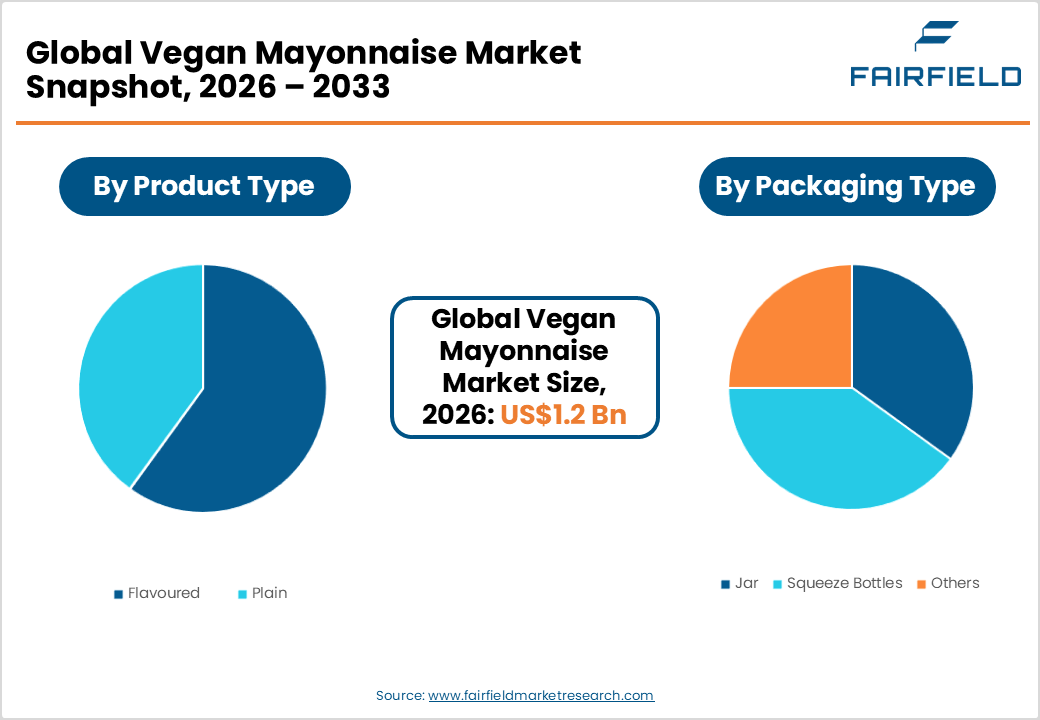

- The global Vegan Mayonnaise market size is likely to be valued at US$1.2 billion in 2026 and is expected to reach US$2.2 billion by 2033, growing at a CAGR of 9.20% during the forecast period from 2026 to 2033.

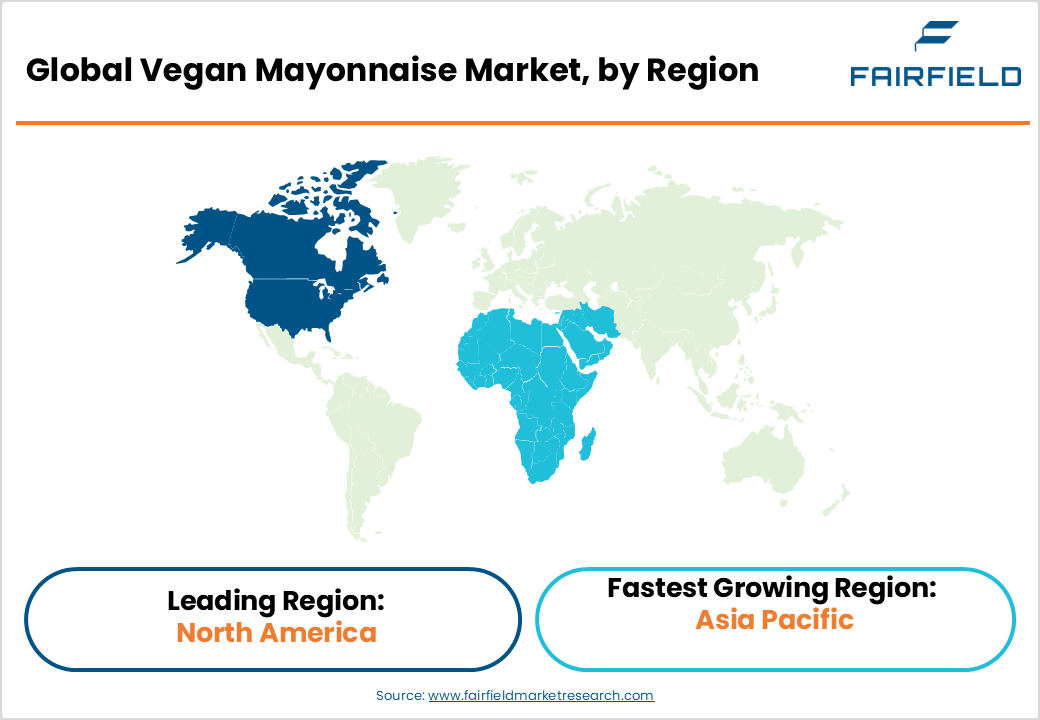

- North America leads the global Vegan Mayonnaise market with approximately 38% share, driven by the U.S.'s mature plant-based food ecosystem, strong health awareness, and established specialty retail infrastructure.

- Asia Pacific is the fastest-growing region, propelled by India's large vegetarian population, China's expanding middle class, and rising e-commerce penetration, enabling broad product accessibility.

- The Plain product type commands approximately 62% of market share, driven by its universal culinary versatility, clean-label appeal, and dominant position in both retail and B2B foodservice procurement.

- Online retail is the fastest-growing distribution sub-channel, fueled by expanding e-grocery platforms, plant-based food subscription services, and DTC brand models reaching health-conscious consumers directly.

- The rapid proliferation of vegan and flexitarian restaurant menus globally presents a high-volume, recurring demand opportunity for manufacturers offering bulk formats, private labels, and customized vegan condiment solutions.

Market Dynamics: Drivers, Restraints, and Opportunities Analysis

Market Growth Drivers

- Accelerating Global Shift Toward Plant-Based Diets

The global plant-based food movement has gained substantial mainstream momentum, directly boosting demand for vegan mayonnaise. According to the Good Food Institute (GFI), plant-based food retail sales in the U.S. exceeded USD 8 billion in recent years, reflecting a sustained consumer pivot toward animal-free products. The number of self-identified vegans in the U.K. quadrupled over the past decade, per The Vegan Society, and similar trends are observed across Germany, Australia, and India. Vegan mayonnaise, as a versatile condiment with broad culinary applications sandwiches, dips, salads, and sauces benefits directly from this dietary evolution. The trend toward clean-label, minimally processed condiments further reinforces consumer preference for transparent, plant-based alternatives over conventional egg-based mayonnaise.

- Rising Health Consciousness and Food Allergy Awareness

Growing consumer awareness of cholesterol management, cardiovascular health, and dietary allergies is a significant demand catalyst for vegan mayonnaise. Traditional mayonnaise is a high-cholesterol product due to egg yolk content; in contrast, plant-based variants are typically cholesterol-free and lower in saturated fats. According to the World Health Organization (WHO), cardiovascular diseases remain the leading cause of death globally, accounting for approximately 17.9 million deaths annually, prompting widespread dietary modification. Additionally, egg allergy is among the most common food allergies, affecting approximately 1-2% of children globally according to the American Academy of Allergy, Asthma & Immunology (AAAAI). Vegan mayonnaise provides a safe, allergen-friendly alternative, expanding its addressable consumer base and fueling adoption across health-focused and allergy-sensitive households.

Market Restraints

- Higher Price Point Compared to Conventional Mayonnaise

One of the primary barriers to mass adoption of vegan mayonnaise is its premium pricing relative to conventional egg-based mayonnaise. Plant-based emulsifiers such as aquafaba, pea protein isolates, and specialty oils involve higher input costs and more complex manufacturing processes. As a result, vegan mayonnaise products are typically priced 30-60% higher than conventional counterparts in major retail markets. According to studies, price sensitivity remains the top purchase barrier for plant-based food adoption among mainstream consumers globally. This premium price gap limits penetration in price-conscious markets, particularly in Latin America, Southeast Asia, and lower-income demographic segments in developed economies.

- Taste and Texture Gap Versus Conventional Mayonnaise

Despite significant formulation improvements, a persistent taste and texture gap between vegan and conventional mayonnaise continues to deter switching behavior among mainstream consumers. Consumer research published in the Journal of Food Science indicates that sensory attributes particularly creaminess, mouthfeel, and flavor complexity remain critical purchase drivers for condiments. Many commercially available vegan mayonnaise products still receive lower sensory scores compared to egg-based variants in blind taste tests. This perception challenge limits repeat purchase rates and creates a barrier to trial in households with no specific dietary motivation, constraining the market's ability to move beyond its core vegan and allergen-conscious consumer base.

Market Opportunities

- Rapid Expansion of Online Retail and Direct-to-Consumer Channels

The explosive growth of e-commerce and online grocery platforms presents a compelling opportunity for vegan mayonnaise brands to reach health-conscious consumers beyond the constraints of traditional retail shelf space. According to the U.S. Department of Agriculture (USDA), online grocery sales in the U.S. are projected to account for over 20% of total grocery sales by 2026. Platforms such as Amazon Fresh, Thrive Market, and BigBasket in India have created dedicated plant-based food categories, dramatically improving discoverability. Direct-to-consumer models additionally allow brands like Chosen Foods LLC and Eat Just, Inc. to build subscription-based recurring revenue streams and gather consumer data for targeted product innovation, creating a sustainable growth engine beyond traditional distribution channels.

- Growing Foodservice and B2B Demand from Vegan and Flexitarian Restaurants

The rapid proliferation of vegan, vegetarian, and flexitarian dining establishments represents an untapped high-volume demand channel for vegan mayonnaise manufacturers. The Plant Based Foods Association (PBFA) reports that plant-based menu items in U.S. restaurants grew by over 30% between 2019 and 2023. Major quick-service restaurant chains, including Subway, Burger King, and McDonald's, have expanded plant-based menu offerings globally, creating institutional demand for vegan condiments including mayonnaise. Additionally, corporate cafeterias, airline catering, and hotel chains are increasingly adopting plant-based menus to cater to diverse dietary preferences. Manufacturers targeting the B2B foodservice segment with bulk packaging, private-label solutions, and customized flavor profiles are well-positioned to capitalize on this structural shift in the out-of-home dining landscape.

Segmentation Analysis: Category-Wise Strategic Assessment

- By Product Type Analysis

The Plain vegan mayonnaise segment holds the leading share in the market by product type, accounting for approximately 62% of total revenues. Plain vegan mayonnaise serves as the foundational condiment and ingredient across both household and foodservice applications used in sandwiches, salads, dips, and cooking making it a universal SKU demanded by nearly all consumer segments. Its versatility and compatibility with a wide range of cuisines drive consistently high purchase frequency. Retailers stock plain vegan mayonnaise as the primary category entry point, and it is the preferred format for bulk B2B procurement by restaurants and institutional buyers. The segment's dominance is further reinforced by the growing consumer preference for clean-label, unflavored base condiments that allow culinary customization, particularly among health-conscious and allergen-sensitive households globally.

- By Packaging Type Analysis

The Jar packaging format leads the Vegan Mayonnaise market by packaging type, commanding approximately 55% of the total segment share. Jar packaging has long been the dominant format for mayonnaise globally due to its strong consumer familiarity, resealability, and perceived premium quality association. Glass and PET jar formats allow consumers to visually assess product consistency an important trust signal for premium plant-based products. Jar packaging is also the preferred format for retail shelf placement across hypermarkets, supermarkets, and specialty stores, enabling prominent product visibility. Furthermore, for premium and artisan vegan mayonnaise brands such as Biona Organic and Chosen Foods LLC the glass jar format reinforces the natural, eco-conscious positioning that resonates strongly with their core target demographic.

- By Distribution Channel Analysis

The B2C distribution channel is the dominant segment, accounting for approximately 67% of total market share, with Hypermarket/Supermarket representing the leading sub-channel within B2C. Supermarkets and hypermarkets remain the primary purchase point for vegan mayonnaise due to their extensive product assortment, high consumer footfall, and strong promotional infrastructure. Chains such as Walmart, Tesco, Carrefour, and Woolworths have significantly expanded their plant-based food aisles in response to growing consumer demand. According to the Food Marketing Institute (FMI), supermarkets account for over 50% of total packaged food purchases in North America, providing vegan mayonnaise brands with unmatched reach and visibility among mainstream shoppers.

Regional Market Assessment: Strategic Geography Analysis

- North America Vegan Mayonnaise Trends

North America is the leading regional market for vegan mayonnaise, holding approximately 38% of global market share. The United States dominates regional demand, driven by a highly developed plant-based food ecosystem, strong consumer health awareness, and a well-established retail infrastructure for specialty and natural foods. The U.S. Food and Drug Administration (FDA) has clarified labeling standards for egg-free mayonnaise products, enabling clearer shelf communication that supports consumer confidence. Leading brands such as Chosen Foods LLC and Hain Celestial have their largest operations in the U.S., continuously innovating with avocado oil-based and organic vegan formulations.

Canada is a growing sub-market, benefiting from the Canadian government's food labeling modernization initiatives and increasing retailer commitment to expanding plant-based product ranges. The Plant Based Foods of Canada association has reported double-digit growth in plant-based food retail sales for multiple consecutive years. Across North America, the proliferation of meal kit services such as HelloFresh and Green Chef, which increasingly include vegan condiments in their kits, is also amplifying awareness and trial of vegan mayonnaise among new consumer segments.

- Europe Vegan Mayonnaise Trends

Europe represents a significant and innovation-driven market for vegan mayonnaise, with Germany, the U.K., France, and the Netherlands as the most mature sub-markets. The U.K. leads European adoption, where The Vegan Society estimates over 600,000 vegans in the country, alongside a much larger flexitarian population actively reducing animal product consumption. Unilever's Hellmann's vegan mayonnaise range launched across European markets exemplifies how mainstream food companies are responding to this structural demand shift.

Germany has one of Europe's most robust plant-based food markets, supported by a strong organic food retail tradition and the influence of ProVeg International, a leading food awareness organization headquartered in Berlin. France and Spain are emerging as growth markets, with foodservice chains and supermarkets expanding plant-based condiment ranges. The EU's Farm to Fork Strategy, targeting a 25% organic agriculture share by 2030, further supports the regulatory and policy environment that encourages plant-based food production and labeling transparency across the region.

- Asia Pacific Vegan Mayonnaise Trends

Asia Pacific is the fastest-growing regional market for vegan mayonnaise, driven by rapid urbanization, rising disposable incomes, growing Western dietary influences, and a naturally large vegetarian consumer base across India, China, and Southeast Asia. In India, the National Family Health Survey (NFHS) data indicates a significant proportion of the population maintains vegetarian or semi-vegetarian diets, representing a structurally large and receptive market for egg-free condiments. Brands such as Veeba Foods have capitalized on this by launching widely distributed vegan condiment lines tailored to Indian taste preferences.

Japan presents a unique opportunity, as Kewpie Corporation, the country's dominant mayonnaise brand, has developed plant-based variants to cater to health-conscious urban consumers. China's rapidly growing middle class and increasing exposure to global food trends through social media platforms such as Douyin (TikTok) are driving awareness of vegan lifestyles. ASEAN markets, particularly Singapore, Thailand, and Indonesia, are witnessing increased vegan food product launches, supported by growing e-commerce penetration that improves product accessibility across geographically dispersed populations.

Competitive Landscape: Market Structure and Strategic Positioning

The global Vegan Mayonnaise market is moderately fragmented, featuring a blend of multinational food conglomerates and agile specialty plant-based brands. Unilever (Hellmann's), Kraft Heinz, and Nestlé leverage their global distribution networks and brand equity to compete at scale, while companies such as Chosen Foods LLC, Biona Organic, and Eat Just, Inc. differentiate through premium positioning, clean-label formulations, and niche channel strategies. Key competitive differentiators include ingredient innovation (aquafaba, avocado oil, pea protein), sustainability certifications (vegan, organic, non-GMO), and packaging eco-credentials. Competitive dynamics are intensifying as conventional food majors aggressively expand their plant-based portfolios, compressing margin space for smaller independents. Private-label vegan mayonnaise from major retailers is also emerging as a formidable competitive force.

Key Players

- Nestlé SA

- Kewpie Corporation

- Kraft Heinz

- Unilever

- Sauer Brands

- Goodman Fielder

- Danone

- Edlyn Foods Pty Ltd.

- Veeba Foods

- Hain Celestial

- Biona Organic

- Eat Just, Inc.

- Dr. Oetker

- Birch & Waite Foods Pty Ltd

- Chosen Foods LLC

- Sir Kensington's (Unilever)

- Follow Your Heart (Earth Island)

- Primal Kitchen

- The Vegan Pantry

Key Industry Developments

- March 2025: Unilever announced the global expansion of the Hellmann's Vegan range into 12 new markets across Asia Pacific and Latin America, supported by reformulation for local taste profiles and new squeeze bottle packaging formats.

- November 2024: Eat Just, Inc. launched its JUST Mayo plant-based mayonnaise in partnership with a major European retail chain, marking its first significant European retail distribution push with an emphasis on clean-label ingredients.

- June 2024: Kewpie Corporation introduced a new plant-based mayonnaise line in Japan using a proprietary egg-free emulsification technology, targeting health-conscious urban consumers and expanding the brand's product portfolio beyond conventional mayonnaise.

Segmentation

By Product Type

- Flavored

- Plain

By Packaging Type

- Jar

- Squeeze Bottles

- Others

By Distribution Channel

- B2B

- B2C

- Hypermarket/ Supermarket

- Convenience Store

- Specialty Store

- Online Retail

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Executive Summary

- Global Vegan Mayonnaise Market Snapshot

- Future Projections

- Key Market Trends

- Regional Snapshot, by Value, 2026

- Analyst Recommendations

- Market Overview

- Market Definitions and Segmentations

- Market Dynamics

- Drivers

- Restraints

- Market Opportunities

- Value Chain Analysis

- COVID-19 Impact Analysis

- Porter's Five Forces Analysis

- Impact of Russia-Ukraine Conflict

- PESTLE Analysis

- Regulatory Analysis

- Price Trend Analysis

- Current Prices and Future Projections, 2025-2033

- Price Impact Factors

- Global Vegan Mayonnaise Market Outlook, 2020 - 2033

- Global Vegan Mayonnaise Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Flavored

- Plain

- Global Vegan Mayonnaise Market Outlook, by Packaging Type, Value (US$ Bn), 2020-2033

- Jar

- Squeeze Bottles

- Others

- Global Vegan Mayonnaise Market Outlook, by Distribution Channel, Value (US$ Bn), 2020-2033

- B2B

- B2C

- Global Vegan Mayonnaise Market Outlook, by Region, Value (US$ Bn), 2020-2033

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Global Vegan Mayonnaise Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- North America Vegan Mayonnaise Market Outlook, 2020 - 2033

- North America Vegan Mayonnaise Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Flavored

- Plain

- North America Vegan Mayonnaise Market Outlook, by Packaging Type, Value (US$ Bn), 2020-2033

- Jar

- Squeeze Bottles

- Others

- North America Vegan Mayonnaise Market Outlook, by Distribution Channel, Value (US$ Bn), 2020-2033

- B2B

- B2C

- North America Vegan Mayonnaise Market Outlook, by Country, Value (US$ Bn), 2020-2033

- U.S. Vegan Mayonnaise Market Outlook, by Product Type, 2020-2033

- U.S. Vegan Mayonnaise Market Outlook, by Packaging Type, 2020-2033

- U.S. Vegan Mayonnaise Market Outlook, by Distribution Channel, 2020-2033

- Canada Vegan Mayonnaise Market Outlook, by Product Type, 2020-2033

- Canada Vegan Mayonnaise Market Outlook, by Packaging Type, 2020-2033

- Canada Vegan Mayonnaise Market Outlook, by Distribution Channel, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- North America Vegan Mayonnaise Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Europe Vegan Mayonnaise Market Outlook, 2020 - 2033

- Europe Vegan Mayonnaise Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Flavored

- Plain

- Europe Vegan Mayonnaise Market Outlook, by Packaging Type, Value (US$ Bn), 2020-2033

- Jar

- Squeeze Bottles

- Others

- Europe Vegan Mayonnaise Market Outlook, by Distribution Channel, Value (US$ Bn), 2020-2033

- B2B

- B2C

- Europe Vegan Mayonnaise Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Germany Vegan Mayonnaise Market Outlook, by Product Type, 2020-2033

- Germany Vegan Mayonnaise Market Outlook, by Packaging Type, 2020-2033

- Germany Vegan Mayonnaise Market Outlook, by Distribution Channel, 2020-2033

- Italy Vegan Mayonnaise Market Outlook, by Product Type, 2020-2033

- Italy Vegan Mayonnaise Market Outlook, by Packaging Type, 2020-2033

- Italy Vegan Mayonnaise Market Outlook, by Distribution Channel, 2020-2033

- France Vegan Mayonnaise Market Outlook, by Product Type, 2020-2033

- France Vegan Mayonnaise Market Outlook, by Packaging Type, 2020-2033

- France Vegan Mayonnaise Market Outlook, by Distribution Channel, 2020-2033

- U.K. Vegan Mayonnaise Market Outlook, by Product Type, 2020-2033

- U.K. Vegan Mayonnaise Market Outlook, by Packaging Type, 2020-2033

- U.K. Vegan Mayonnaise Market Outlook, by Distribution Channel, 2020-2033

- Spain Vegan Mayonnaise Market Outlook, by Product Type, 2020-2033

- Spain Vegan Mayonnaise Market Outlook, by Packaging Type, 2020-2033

- Spain Vegan Mayonnaise Market Outlook, by Distribution Channel, 2020-2033

- Russia Vegan Mayonnaise Market Outlook, by Product Type, 2020-2033

- Russia Vegan Mayonnaise Market Outlook, by Packaging Type, 2020-2033

- Russia Vegan Mayonnaise Market Outlook, by Distribution Channel, 2020-2033

- Rest of Europe Vegan Mayonnaise Market Outlook, by Product Type, 2020-2033

- Rest of Europe Vegan Mayonnaise Market Outlook, by Packaging Type, 2020-2033

- Rest of Europe Vegan Mayonnaise Market Outlook, by Distribution Channel, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Europe Vegan Mayonnaise Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Asia Pacific Vegan Mayonnaise Market Outlook, 2020 - 2033

- Asia Pacific Vegan Mayonnaise Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Flavored

- Plain

- Asia Pacific Vegan Mayonnaise Market Outlook, by Packaging Type, Value (US$ Bn), 2020-2033

- Jar

- Squeeze Bottles

- Others

- Asia Pacific Vegan Mayonnaise Market Outlook, by Distribution Channel, Value (US$ Bn), 2020-2033

- B2B

- B2C

- Asia Pacific Vegan Mayonnaise Market Outlook, by Country, Value (US$ Bn), 2020-2033

- China Vegan Mayonnaise Market Outlook, by Product Type, 2020-2033

- China Vegan Mayonnaise Market Outlook, by Packaging Type, 2020-2033

- China Vegan Mayonnaise Market Outlook, by Distribution Channel, 2020-2033

- Japan Vegan Mayonnaise Market Outlook, by Product Type, 2020-2033

- Japan Vegan Mayonnaise Market Outlook, by Packaging Type, 2020-2033

- Japan Vegan Mayonnaise Market Outlook, by Distribution Channel, 2020-2033

- South Korea Vegan Mayonnaise Market Outlook, by Product Type, 2020-2033

- South Korea Vegan Mayonnaise Market Outlook, by Packaging Type, 2020-2033

- South Korea Vegan Mayonnaise Market Outlook, by Distribution Channel, 2020-2033

- India Vegan Mayonnaise Market Outlook, by Product Type, 2020-2033

- India Vegan Mayonnaise Market Outlook, by Packaging Type, 2020-2033

- India Vegan Mayonnaise Market Outlook, by Distribution Channel, 2020-2033

- Southeast Asia Vegan Mayonnaise Market Outlook, by Product Type, 2020-2033

- Southeast Asia Vegan Mayonnaise Market Outlook, by Packaging Type, 2020-2033

- Southeast Asia Vegan Mayonnaise Market Outlook, by Distribution Channel, 2020-2033

- Rest of SAO Vegan Mayonnaise Market Outlook, by Product Type, 2020-2033

- Rest of SAO Vegan Mayonnaise Market Outlook, by Packaging Type, 2020-2033

- Rest of SAO Vegan Mayonnaise Market Outlook, by Distribution Channel, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Asia Pacific Vegan Mayonnaise Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Latin America Vegan Mayonnaise Market Outlook, 2020 - 2033

- Latin America Vegan Mayonnaise Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Flavored

- Plain

- Latin America Vegan Mayonnaise Market Outlook, by Packaging Type, Value (US$ Bn), 2020-2033

- Jar

- Squeeze Bottles

- Others

- Latin America Vegan Mayonnaise Market Outlook, by Distribution Channel, Value (US$ Bn), 2020-2033

- B2B

- B2C

- Latin America Vegan Mayonnaise Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Brazil Vegan Mayonnaise Market Outlook, by Product Type, 2020-2033

- Brazil Vegan Mayonnaise Market Outlook, by Packaging Type, 2020-2033

- Brazil Vegan Mayonnaise Market Outlook, by Distribution Channel, 2020-2033

- Mexico Vegan Mayonnaise Market Outlook, by Product Type, 2020-2033

- Mexico Vegan Mayonnaise Market Outlook, by Packaging Type, 2020-2033

- Mexico Vegan Mayonnaise Market Outlook, by Distribution Channel, 2020-2033

- Argentina Vegan Mayonnaise Market Outlook, by Product Type, 2020-2033

- Argentina Vegan Mayonnaise Market Outlook, by Packaging Type, 2020-2033

- Argentina Vegan Mayonnaise Market Outlook, by Distribution Channel, 2020-2033

- Rest of LATAM Vegan Mayonnaise Market Outlook, by Product Type, 2020-2033

- Rest of LATAM Vegan Mayonnaise Market Outlook, by Packaging Type, 2020-2033

- Rest of LATAM Vegan Mayonnaise Market Outlook, by Distribution Channel, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Latin America Vegan Mayonnaise Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Middle East & Africa Vegan Mayonnaise Market Outlook, 2020 - 2033

- Middle East & Africa Vegan Mayonnaise Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Flavored

- Plain

- Middle East & Africa Vegan Mayonnaise Market Outlook, by Packaging Type, Value (US$ Bn), 2020-2033

- Jar

- Squeeze Bottles

- Others

- Middle East & Africa Vegan Mayonnaise Market Outlook, by Distribution Channel, Value (US$ Bn), 2020-2033

- B2B

- B2C

- Middle East & Africa Vegan Mayonnaise Market Outlook, by Country, Value (US$ Bn), 2020-2033

- GCC Vegan Mayonnaise Market Outlook, by Product Type, 2020-2033

- GCC Vegan Mayonnaise Market Outlook, by Packaging Type, 2020-2033

- GCC Vegan Mayonnaise Market Outlook, by Distribution Channel, 2020-2033

- South Africa Vegan Mayonnaise Market Outlook, by Product Type, 2020-2033

- South Africa Vegan Mayonnaise Market Outlook, by Packaging Type, 2020-2033

- South Africa Vegan Mayonnaise Market Outlook, by Distribution Channel, 2020-2033

- Egypt Vegan Mayonnaise Market Outlook, by Product Type, 2020-2033

- Egypt Vegan Mayonnaise Market Outlook, by Packaging Type, 2020-2033

- Egypt Vegan Mayonnaise Market Outlook, by Distribution Channel, 2020-2033

- Nigeria Vegan Mayonnaise Market Outlook, by Product Type, 2020-2033

- Nigeria Vegan Mayonnaise Market Outlook, by Packaging Type, 2020-2033

- Nigeria Vegan Mayonnaise Market Outlook, by Distribution Channel, 2020-2033

- Rest of Middle East Vegan Mayonnaise Market Outlook, by Product Type, 2020-2033

- Rest of Middle East Vegan Mayonnaise Market Outlook, by Packaging Type, 2020-2033

- Rest of Middle East Vegan Mayonnaise Market Outlook, by Distribution Channel, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Middle East & Africa Vegan Mayonnaise Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Competitive Landscape

- Company Vs Segment Heatmap

- Company Market Share Analysis, 2025

- Competitive Dashboard

- Company Profiles

- Nestlé SA

- Company Overview

- Product Portfolio

- Financial Overview

- Business Strategies and Developments

- Kewpie Corporation

- Kraft Heinz

- Unilever

- Sauer Brands

- Goodman Fielder

- Danone

- Edlyn Foods Pty Ltd.

- Veeba Foods

- Hain Celestial

- Biona Organic

- Eat Just, Inc.

- Oetker

- Birch & Waite Foods Pty Ltd

- Other

- Nestlé SA

- Appendix

- Research Methodology

- Report Assumptions

- Acronyms and Abbreviations

|

BASE YEAR |

HISTORICAL DATA |

FORECAST PERIOD |

UNITS |

|||

|

2025 |

|

2019 - 2025 |

2026 - 2033 |

Value: US$ Billion |

||

|

REPORT FEATURES |

DETAILS |

|

By Product-Type Coverage |

|

|

By Packaging Type Coverage |

|

|

Geographical Coverage |

|

|

Leading Companies |

|

|

Report Highlights |

Key Market Indicators, Macro-micro economic impact analysis, Technological Roadmap, Key Trends, Driver, Restraints, and Future Opportunities & Revenue Pockets, Porter’s 5 Forces Analysis, Historical Trend (2019-2024), Market Estimates and Forecast, Market Dynamics, Industry Trends, Competition Landscape, Category, Region, Country-wise Trends & Analysis, COVID-19 Impact Analysis (Demand and Supply Chain) |

Our Research Methodology

Considering the volatility of business today, traditional approaches to strategizing a game plan can be unfruitful if not detrimental. True ambiguity is no way to determine a forecast. A myriad of predetermined factors must be accounted for such as the degree of risk involved, the magnitude of circumstances, as well as conditions or consequences that are not known or unpredictable. To circumvent binary views that cast uncertainty, the application of market research intelligence to strategically posture, move, and enable actionable outcomes is necessary.

View Methodology

Quality Assured

Rigorous Validation Process

Confidentiality Assured

End-to-end Data Security

Custom Research Services

Tailored To Your Objectives

FAQs

The Vegan Mayonnaise market size is US$1.2 billion in 2026.

The Vegan Mayonnaise market is projected 9.2% CAGR by 2033.

The Vegan Mayonnaise market growth drivers include plant-based diet adoption, health-conscious consumer trends, and vegan population expansion.

North America is the dominating region for Vegan Mayonnaise market.

Unilever (Hellmann's), Kraft Heinz, Del Monte Foods, Hampton Creek, and Dr. Oetker are some leading industry players in the Vegan Mayonnaise market.

Related Reports

Tortilla Market Insights, Competitive Landscape, and Market Forecast 2033

The tortilla market is projected to reach US$75.36 billion by 2033 growing at a 5.1% CAGR, driven by rising demand for convenient and ready-to-eat foods.

RTD Canned Cocktail Market Insights, Competitive Landscape, and Market Forecast 2033

RTD Canned Cocktail Market to reach US$11.15 Bn by 2033 at 14.2% CAGR, driven by premium RTDs, e-commerce growth, and consumer demand.

Avocado Oil Market Insights, Competitive Landscape, and Market Forecast 2033

The analgesics market is projected to grow from US$58.30 billion in 2026 to US$93.01 billion by 2033, registering a CAGR of 6.9% during the forecast period.

Soda Ash Market Insights, Competitive Landscape, and Market Forecast 2033

The soda ash market is projected to grow from US$15.90 billion in 2026 to US$24.87 billion by 2033, registering a CAGR of 6.6% over the forecast period.

Customized Premixes Market Insights, Competitive Landscape, and Market Forecast 2033

The customized premixes market is forecast to reach US$14.77 Bn by 2033 from US$8.90 Bn in 2026, growing at a CAGR of 7.5% over the forecast period.

Almond Ingredients Market Insights, Competitive Landscape, and Market Forecast 2033

The almond ingredients market is projected to grow from US$ 18.90 billion in 2026 to US$ 33.03 billion by 2033, at an 8.3% CAGR over the forecast period.