Global Dietary Supplements Market: Strategic Analysis 2026-2033

Executive Summary & Key Highlights

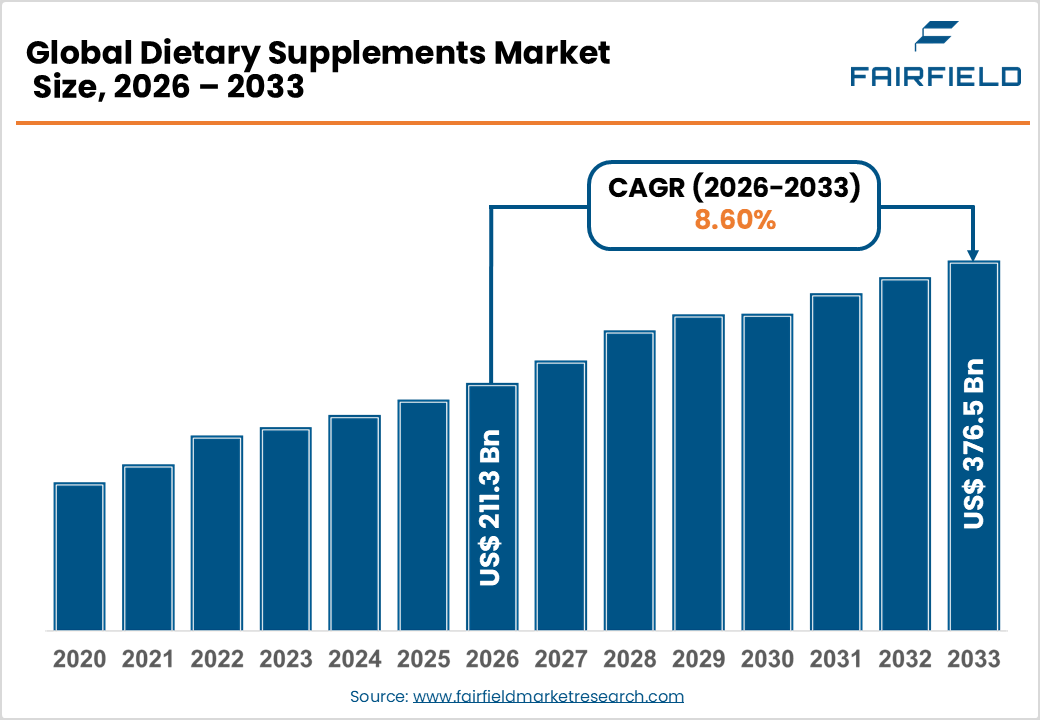

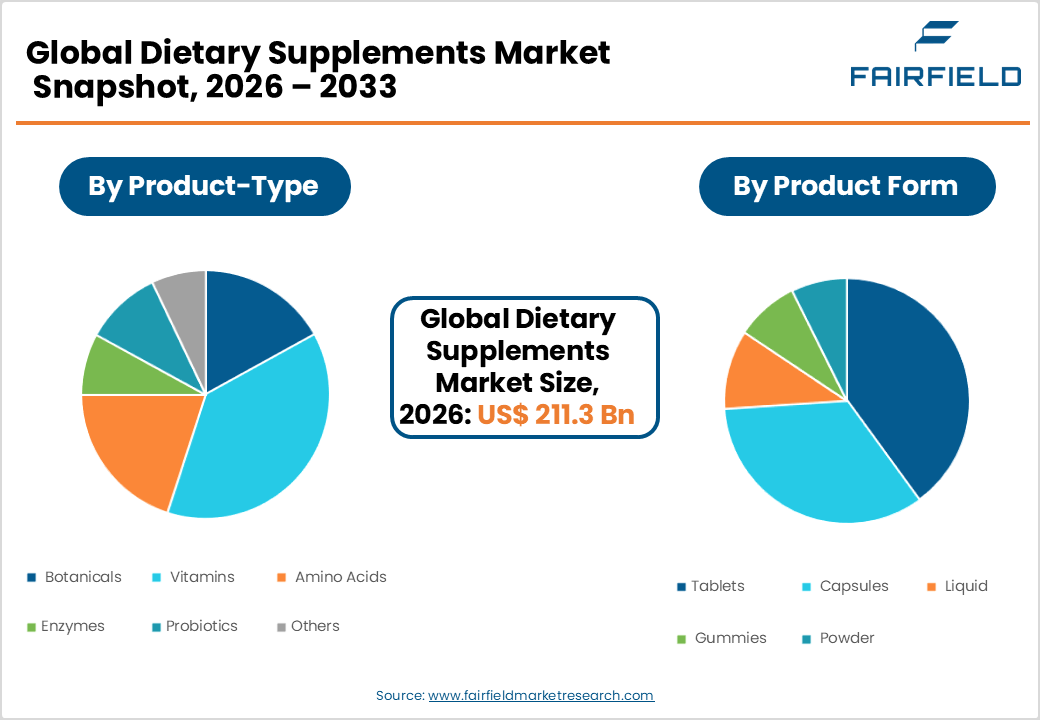

- The global dietary supplements market size is likely to be valued at USD 211.3 billion in 2026 and is expected to reach USD 376.5 billion by 2033, growing at a CAGR of 8.60% during the forecast period from 2026 to 2033.

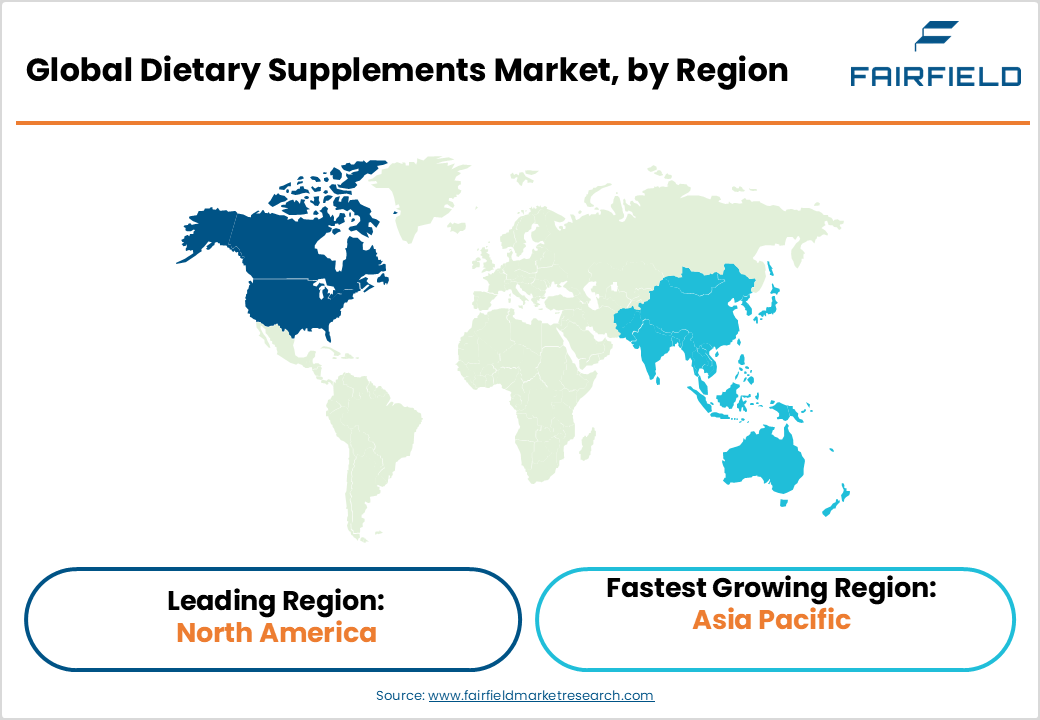

- North America leads the global dietary supplements market with approximately 36% revenue share, driven by record 74% adult supplement usage in the U.S., a mature FDA/DSHEA regulatory framework, and a highly innovative nutraceutical industry ecosystem.

- Asia Pacific is the fastest-growing dietary supplements market, propelled by China's dominant nutraceutical manufacturing base, India's post-pandemic wellness boom, and rapidly expanding e-commerce and digital health supplement channels across ASEAN nations.

- Vitamins dominate the type segment with approximately 35% market share, underpinned by broad global consumption of Vitamin D, C, and B-complex, widespread micronutrient deficiency recognition, and extensive clinical endorsement from healthcare professionals worldwide.

- Probiotics represent the fastest-growing type segment, driven by mounting clinical evidence supporting gut-brain axis health, a surge in gut microbiome research publications, and rapidly growing consumer adoption of probiotic supplements across immune, digestive, and mental wellness functions.

- Personalized nutrition platforms integrating genomics, microbiome analysis, and wearable health data represent the defining growth opportunity, enabling premium, science-backed supplement formulations and high-retention direct-to-consumer subscription business models across global markets.

Market Dynamics: Drivers, Restraints, and Opportunities Analysis

Market Growth Drivers

- Post-Pandemic Surge in Preventive Healthcare and Immunity Supplementation

The COVID-19 pandemic has fundamentally reshaped consumer health behavior, accelerating a structural shift toward preventive healthcare and daily nutritional supplementation. According to the Council for Responsible Nutrition (CRN), its 2023 Consumer Survey on Dietary Supplements found that 74% of U.S. adults reported using dietary supplements in a record high with immune health supplements ranking among the top purchased categories. Vitamin D, Vitamin C, zinc, and probiotic products experienced significant volume growth during and after the pandemic. The World Health Organization (WHO) has highlighted micronutrient deficiencies as a critical public health concern globally, further validating supplement use. This heightened health awareness continues to drive consistent, broad-based consumer demand across vitamins, minerals, and immune-function supplements worldwide.

- Aging Global Population and Growing Chronic Disease Burden

The United Nations projects that the global population aged 60 and above may reach approximately 2.1 billion by 2050. Aging populations are disproportionately susceptible to nutritional deficiencies and chronic conditions including osteoporosis, cardiovascular disease, and cognitive decline conditions where dietary supplements play a clinically recognized supportive role. The World Health Organization (WHO) reports that chronic non-communicable diseases (NCDs) account for approximately 74% of all global deaths annually. This demographic reality is driving sustained demand for bone and joint, cardiovascular, cognitive, and metabolic health supplements. Pharmaceutical companies and nutraceutical brands are investing significantly in evidence-based, age-specific supplement formulations to address the rapidly expanding senior consumer segment globally.

Market Restraints

- Regulatory Complexity and Product Safety Concerns

The dietary supplements industry operates under a complex and inconsistent global regulatory landscape. In the United States, the U.S. Food and Drug Administration (FDA) regulates dietary supplements under the Dietary Supplement Health and Education Act (DSHEA) of 1994, which does not require pre-market approval for a framework frequently criticized for enabling substandard products to reach consumers. The European Food Safety Authority (EFSA) enforces stricter maximum permitted levels for vitamins and minerals under EU Directive 2002/46/EC. High-profile product recalls and contamination cases have periodically eroded consumer confidence, increasing compliance costs for producers and creating market access barriers that particularly disadvantage smaller supplement manufacturers.

- Prevalence of Adulteration and Counterfeit Products

Product adulteration and the proliferation of counterfeit dietary supplements represent significant market restraints. The U.S. FDA has issued numerous warning letters and product recalls related to undeclared pharmaceutical ingredients in supplements particularly in sports nutrition and weight management categories. A study published in the Journal of the American Medical Association (JAMA) found that a significant proportion of sports supplements contained undisclosed synthetic compounds. The rise of unverified online marketplaces has amplified counterfeit product circulation, undermining brand trust and exposing consumers to health risks. These challenges impose additional quality assurance burdens on legitimate producers and may dampen consumer confidence in supplement categories most affected by adulteration.

Market Opportunities

- Personalized Nutrition and Genomics-Driven Supplement Innovation

Personalized nutrition represents one of the most transformative emerging opportunities in the dietary supplements market. Advances in nutrigenomics, microbiome analysis, and wearable health monitoring are enabling companies to develop highly tailored supplement regimens based on individual genetic profiles, lifestyle data, and biomarker assessments. Companies such as Herbalife Nutrition Ltd. and Amway Corp. (through its Nutrilite brand) are investing in personalized wellness platforms. According to the European Nutrigenomics Organisation, personalized nutrition could fundamentally alter how dietary recommendations and supplement prescriptions are made. The convergence of direct-to-consumer genetic testing with companies processing millions of kits annually globally and supplement subscription business models creates a compelling commercial opportunity for market participants to drive premium product pricing and high customer lifetime value.

- Explosive Growth of Online and Direct-to-Consumer Sales Channels

The rapid expansion of e-commerce and direct-to-consumer (DTC) sales channels is reshaping the dietary supplements distribution landscape, particularly in the Asia Pacific, the fastest-growing regional market. According to the International Trade Centre, online sales of health and wellness products including dietary supplements, have grown at double-digit rates post-2020 across major markets. Platforms such as Amazon, Tmall, Flipkart, and brand-owned DTC websites now command a growing share of supplement transactions. Social media marketing, influencer-driven health content, and subscription-based supplement delivery models are significantly lowering customer acquisition costs while enabling personalized engagement. Companies investing in robust digital commerce infrastructure, mobile-first marketing, and AI-powered product recommendation engines are positioned to capture outsized growth from this accelerating channel shift.

Segmentation Analysis: Category-Wise Strategic Assessment

- Type Analysis

Vitamins dominate the dietary supplements market by type, accounting for approximately 35% of total market share. Vitamins including Vitamin D, Vitamin C, Vitamin B-complex, and Vitamin E are among the most universally consumed supplement categories globally, supported by extensive clinical evidence and broad physician recommendation. The Council for Responsible Nutrition (CRN) consistently identifies vitamins as the most frequently used supplement category among U.S. adults, with Vitamin D topping consumption lists for multiple consecutive years. Widespread recognition of micronutrient deficiency with the WHO estimating that approximately billions of people globally are Vitamin D deficient further drives consumer demand. Vitamins are available across all major retail and online channels, reinforcing their category leadership in the dietary supplements market.

- Form Analysis

Tablets represent the leading form segment, accounting for approximately 38% of the dietary supplements market. Tablets offer significant manufacturing advantages including extended shelf life, precise dosage standardization, cost-efficient production, and high consumer familiarity across both prescription pharmaceutical and OTC supplement categories. The U.S. Pharmacopeia (USP) and comparable international quality standards have well-established monographs for tablet-form supplements, facilitating regulatory compliance and quality assurance. Tablets are particularly dominant in the vitamins and minerals sub-categories, where mass-market consumer products from brands including Nature's Bounty, NOW Foods, and Bayer AG (Berocca, One-A-Day) command substantial retail shelf space globally. Despite the rapid growth of gummies and liquid formats, tablets retain their dominant position through price competitiveness and dosage reliability.

- Function Analysis

Immune health is the leading functional segment in the dietary supplements market, commanding approximately 25% of total market share. The COVID-19 pandemic created a lasting structural uplift in consumer demand for immune-supporting supplements, including Vitamin C, Vitamin D, zinc, elderberry, and echinacea. The Council for Responsible Nutrition (CRN) reported a sustained elevation in immune supplement usage among U.S. adults well beyond the acute pandemic period, reflecting a durable behavioral shift toward immune health management. The WHO's ongoing documentation of micronutrient deficiency as a public health priority further legitimizes immune health supplementation. Market participants including GlaxoSmithKline plc (Centrum), Pfizer Inc., and Abbott have expanded their immune health supplement portfolios to capitalize on this sustained functional category leadership.

- Sales Channel Analysis

Offline channels collectively represent the leading sales channel, accounting for approximately 62% of the dietary supplements market. Within offline, Pharmacies and Drugstores hold the largest sub-channel share, leveraging their established positioning as trusted health retail destinations and pharmacist recommendation influence. Chains such as CVS Health, Walgreens, and Boots maintain extensive supplement ranges and loyalty programs that drive repeat purchase behavior. Hypermarkets and Supermarkets including Walmart, Costco, and Tesco serve mass-market supplement consumers seeking value formats and convenient co-purchase with grocery shopping. The National Association of Chain Drug Stores (NACDS) notes that pharmacies remain a primary destination for supplement purchases, particularly among older demographics. Online channels, however, represent the fastest growing sales channel and are gaining significant share rapidly.

Regional Market Assessment: Strategic Geography Analysis

- North America Dietary Supplements Market Trends

North America leads the global dietary supplements market, accounting for approximately 36% of total revenue, underpinned by the U.S. deeply embedded supplement consumption culture, a mature regulatory framework, and a highly innovative industry ecosystem. The Council for Responsible Nutrition (CRN) reports that 74% of U.S. adults consumed dietary supplements in 2023 being the highest recorded usage rate. The market is governed by the U.S. FDA under DSHEA, with the Federal Trade Commission (FTC) overseeing supplement advertising standards, creating a structured compliance environment.

The U.S. market benefits from a robust innovation ecosystem, with companies including Abbott, Pfizer Inc., Nature's Bounty, NOW Foods, and Amway Corp. continuously launching science-backed formulations. Canada's dietary supplement market, governed by Health Canada under the Natural Health Products Regulations, is also expanding steadily. Growing consumer interest in sports nutrition, personalized wellness, and functional gummies is driving premiumization trends across the North American market.

- Europe Dietary Supplements Market Trends

Europe is a significant and well-regulated dietary supplements market, shaped by harmonized European Union regulatory frameworks and growing consumer focus on preventive health and clean-label nutrition. The European Food Safety Authority (EFSA) oversees health claims substantiation under EC Regulation 1924/2006, ensuring scientific rigor in supplement marketing. Germany, the United Kingdom, France, and Spain are the leading national markets, each characterized by distinct consumer preferences and well-developed pharmacy and health food retail channels.

Germany leads European supplement consumption, with a strong preference for standardized phytomedicine and vitamins sold through pharmacies. The U.K. market demonstrates growing demand for sports nutrition and gut health supplements, with brands including GlaxoSmithKline plc (Centrum, Berocca) maintaining significant market presence. France's well-established pharmacy culture drives supplement uptake particularly in vitamins and probiotics. Spain is recording increasing demand for sports nutrition and collagen-based beauty supplements, aligned with broader European wellness lifestyle trends.

- Asia Pacific Dietary Supplements Market Trends

Asia Pacific is the fastest-growing regional market for dietary supplements, driven by a convergence of rapid urbanization, a rising health-conscious middle class, expanding e-commerce penetration, and government-supported preventive healthcare initiatives. China represents the dominant sub-regional market, accounting for a substantial share of Asia Pacific supplement revenue, with its domestic nutraceuticals industry supported by significant manufacturing infrastructure and a growing regulatory framework under the National Medical Products Administration (NMPA).

Japan's long-standing functional food and supplement culture supported by the government's Foods with Function Claims (FFC) regulatory system maintains high per-capita supplement consumption. India is emerging as a high-growth market, driven by post-pandemic health awareness, expanding urban middle-class disposable incomes, and digital health platforms driving supplement discovery and e-commerce purchases. ASEAN markets particularly Indonesia, Thailand, and Vietnam are experiencing robust growth fueled by young, digitally connected consumer demographics and rapidly expanding modern retail and e-commerce channels.

Competitive Landscape: Market Structure and Strategic Positioning

The global dietary supplements market is highly fragmented, with thousands of local, regional, and multinational participants competing across product types, functional categories, and distribution channels. Leading players including Abbott, Bayer AG, GlaxoSmithKline plc, Pfizer Inc., Herbalife Nutrition Ltd., Amway Corp., and Glanbia plc leverage brand equity, clinical research investments, and expansive distribution networks to maintain market leadership. Key competitive strategies encompass personalized nutrition platform development, clean-label and organic product differentiation, strategic acquisitions of specialist nutraceutical brands, and omnichannel digital commerce expansion. Private-label supplement brands from major retailers are also intensifying competitive pressure on branded manufacturers across volume-driven vitamin and mineral categories.

Key Industry Developments

- February, 2025: Abbott launched its expanded Ensure nutrition supplement range targeting healthy aging adults in Asia Pacific markets, incorporating advanced protein and micronutrient formulations designed for muscle preservation and metabolic health in seniors.

- November, 2024: Glanbia plc announced a strategic acquisition of a personalized sports nutrition platform, strengthening its Optimum Nutrition and BSN brand portfolios and accelerating its direct-to-consumer digital supplement commerce capabilities globally.

- June, 2023: Bayer AG expanded its Berocca and Elevit supplement brands into new Southeast Asian markets through enhanced e-commerce partnerships with regional platforms, targeting rapidly growing health-conscious consumer demographics in the ASEAN region.

Key Players

- Abbott

- Bayer AG

- Amway Corp.

- Glanbia plc

- Pfizer Inc.

- Archer Daniels Midland

- NU SKIN

- GlaxoSmithKline plc.

- Herbalife Nutrition Ltd.

- Nature's Sunshine Products, Inc.

- XanGo, LLC

- RBK Nutraceuticals Pty Ltd

- American Health

- DuPont de Nemours, Inc.

- Nature's Bounty

- NOW Foods

- Good Health New Zealand

Global Dietary Supplements Market Segmentation

By Product Type

- Botanicals

- Vitamins

- Amino Acids

- Amino Acids

- Enzymes

- Probiotics

- Others

By Product Form

- Tablets

- Capsules

- Liquid

- Gummies

- Powder

By Product Function

- Gut Health

- Immune Health

- Sports Nutrition

- Skin Health

- Metabolic Health

- Weight Management

- Bone & Joint Health

- Others

By Sales Channel

- Online

- Offline

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Executive Summary

- Global Dietary Supplements Market Snapshot

- Future Projections

- Key Market Trends

- Regional Snapshot, by Value, 2026

- Analyst Recommendations

- Market Overview

- Market Definitions and Segmentations

- Market Dynamics

- Drivers

- Restraints

- Market Opportunities

- Value Chain Analysis

- COVID-19 Impact Analysis

- Porter's Five Forces Analysis

- Impact of Russia-Ukraine Conflict

- PESTLE Analysis

- Regulatory Analysis

- Price Trend Analysis

- Current Prices and Future Projections, 2025-2033

- Price Impact Factors

- Global Dietary Supplements Market Outlook, 2020 - 2033

- Global Dietary Supplements Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Botanicals

- Vitamins

- Amino Acids

- Enzymes

- Probiotics

- Others

- Global Dietary Supplements Market Outlook, by Product Form, Value (US$ Bn), 2020-2033

- Tablets

- Capsules

- Liquid

- Gummies

- Powder

- Global Dietary Supplements Market Outlook, by Function, Value (US$ Bn), 2020-2033

- Gut Health

- Immune Health

- Sports Nutrition

- Skin Health

- Metabolic Health

- Weight Management

- Bone & Joint Health

- Others

- Global Dietary Supplements Market Outlook, by Sales Channel, Value (US$ Bn), 2020-2033

- Online

- Offline

- Global Dietary Supplements Market Outlook, by Region, Value (US$ Bn), 2020-2033

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Global Dietary Supplements Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- North America Dietary Supplements Market Outlook, 2020 - 2033

- North America Dietary Supplements Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Botanicals

- Vitamins

- Amino Acids

- Enzymes

- Probiotics

- Others

- North America Dietary Supplements Market Outlook, by Product Form, Value (US$ Bn), 2020-2033

- Tablets

- Capsules

- Liquid

- Gummies

- Powder

- North America Dietary Supplements Market Outlook, by Function, Value (US$ Bn), 2020-2033

- Gut Health

- Immune Health

- Sports Nutrition

- Skin Health

- Metabolic Health

- Weight Management

- Bone & Joint Health

- Others

- North America Dietary Supplements Market Outlook, by Sales Channel, Value (US$ Bn), 2020-2033

- Online

- Offline

- North America Dietary Supplements Market Outlook, by Country, Value (US$ Bn), 2020-2033

- U.S. Dietary Supplements Market Outlook, by Product Type, 2020-2033

- U.S. Dietary Supplements Market Outlook, by Product Form, 2020-2033

- U.S. Dietary Supplements Market Outlook, by Function, 2020-2033

- U.S. Dietary Supplements Market Outlook, by Sales Channel, 2020-2033

- Canada Dietary Supplements Market Outlook, by Product Type, 2020-2033

- Canada Dietary Supplements Market Outlook, by Product Form, 2020-2033

- Canada Dietary Supplements Market Outlook, by Function, 2020-2033

- Canada Dietary Supplements Market Outlook, by Sales Channel, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- North America Dietary Supplements Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Europe Dietary Supplements Market Outlook, 2020 - 2033

- Europe Dietary Supplements Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Botanicals

- Vitamins

- Amino Acids

- Enzymes

- Probiotics

- Others

- Europe Dietary Supplements Market Outlook, by Product Form, Value (US$ Bn), 2020-2033

- Tablets

- Capsules

- Liquid

- Gummies

- Powder

- Europe Dietary Supplements Market Outlook, by Function, Value (US$ Bn), 2020-2033

- Gut Health

- Immune Health

- Sports Nutrition

- Skin Health

- Metabolic Health

- Weight Management

- Bone & Joint Health

- Others

- Europe Dietary Supplements Market Outlook, by Sales Channel, Value (US$ Bn), 2020-2033

- Online

- Offline

- Europe Dietary Supplements Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Germany Dietary Supplements Market Outlook, by Product Type, 2020-2033

- Germany Dietary Supplements Market Outlook, by Product Form, 2020-2033

- Germany Dietary Supplements Market Outlook, by Function, 2020-2033

- Germany Dietary Supplements Market Outlook, by Sales Channel, 2020-2033

- Italy Dietary Supplements Market Outlook, by Product Type, 2020-2033

- Italy Dietary Supplements Market Outlook, by Product Form, 2020-2033

- Italy Dietary Supplements Market Outlook, by Function, 2020-2033

- Italy Dietary Supplements Market Outlook, by Sales Channel, 2020-2033

- France Dietary Supplements Market Outlook, by Product Type, 2020-2033

- France Dietary Supplements Market Outlook, by Product Form, 2020-2033

- France Dietary Supplements Market Outlook, by Function, 2020-2033

- France Dietary Supplements Market Outlook, by Sales Channel, 2020-2033

- U.K. Dietary Supplements Market Outlook, by Product Type, 2020-2033

- U.K. Dietary Supplements Market Outlook, by Product Form, 2020-2033

- U.K. Dietary Supplements Market Outlook, by Function, 2020-2033

- U.K. Dietary Supplements Market Outlook, by Sales Channel, 2020-2033

- Spain Dietary Supplements Market Outlook, by Product Type, 2020-2033

- Spain Dietary Supplements Market Outlook, by Product Form, 2020-2033

- Spain Dietary Supplements Market Outlook, by Function, 2020-2033

- Spain Dietary Supplements Market Outlook, by Sales Channel, 2020-2033

- Russia Dietary Supplements Market Outlook, by Product Type, 2020-2033

- Russia Dietary Supplements Market Outlook, by Product Form, 2020-2033

- Russia Dietary Supplements Market Outlook, by Function, 2020-2033

- Russia Dietary Supplements Market Outlook, by Sales Channel, 2020-2033

- Rest of Europe Dietary Supplements Market Outlook, by Product Type, 2020-2033

- Rest of Europe Dietary Supplements Market Outlook, by Product Form, 2020-2033

- Rest of Europe Dietary Supplements Market Outlook, by Function, 2020-2033

- Rest of Europe Dietary Supplements Market Outlook, by Sales Channel, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Europe Dietary Supplements Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Asia Pacific Dietary Supplements Market Outlook, 2020 - 2033

- Asia Pacific Dietary Supplements Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Botanicals

- Vitamins

- Amino Acids

- Enzymes

- Probiotics

- Others

- Asia Pacific Dietary Supplements Market Outlook, by Product Form, Value (US$ Bn), 2020-2033

- Tablets

- Capsules

- Liquid

- Gummies

- Powder

- Asia Pacific Dietary Supplements Market Outlook, by Function, Value (US$ Bn), 2020-2033

- Gut Health

- Immune Health

- Sports Nutrition

- Skin Health

- Metabolic Health

- Weight Management

- Bone & Joint Health

- Others

- Asia Pacific Dietary Supplements Market Outlook, by Sales Channel, Value (US$ Bn), 2020-2033

- Online

- Offline

- Asia Pacific Dietary Supplements Market Outlook, by Country, Value (US$ Bn), 2020-2033

- China Dietary Supplements Market Outlook, by Product Type, 2020-2033

- China Dietary Supplements Market Outlook, by Product Form, 2020-2033

- China Dietary Supplements Market Outlook, by Function, 2020-2033

- China Dietary Supplements Market Outlook, by Sales Channel, 2020-2033

- Japan Dietary Supplements Market Outlook, by Product Type, 2020-2033

- Japan Dietary Supplements Market Outlook, by Product Form, 2020-2033

- Japan Dietary Supplements Market Outlook, by Function, 2020-2033

- Japan Dietary Supplements Market Outlook, by Sales Channel, 2020-2033

- South Korea Dietary Supplements Market Outlook, by Product Type, 2020-2033

- South Korea Dietary Supplements Market Outlook, by Product Form, 2020-2033

- South Korea Dietary Supplements Market Outlook, by Function, 2020-2033

- South Korea Dietary Supplements Market Outlook, by Sales Channel, 2020-2033

- India Dietary Supplements Market Outlook, by Product Type, 2020-2033

- India Dietary Supplements Market Outlook, by Product Form, 2020-2033

- India Dietary Supplements Market Outlook, by Function, 2020-2033

- India Dietary Supplements Market Outlook, by Sales Channel, 2020-2033

- Southeast Asia Dietary Supplements Market Outlook, by Product Type, 2020-2033

- Southeast Asia Dietary Supplements Market Outlook, by Product Form, 2020-2033

- Southeast Asia Dietary Supplements Market Outlook, by Function, 2020-2033

- Southeast Asia Dietary Supplements Market Outlook, by Sales Channel, 2020-2033

- Rest of SAO Dietary Supplements Market Outlook, by Product Type, 2020-2033

- Rest of SAO Dietary Supplements Market Outlook, by Product Form, 2020-2033

- Rest of SAO Dietary Supplements Market Outlook, by Function, 2020-2033

- Rest of SAO Dietary Supplements Market Outlook, by Sales Channel, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Asia Pacific Dietary Supplements Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Latin America Dietary Supplements Market Outlook, 2020 - 2033

- Latin America Dietary Supplements Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Botanicals

- Vitamins

- Amino Acids

- Enzymes

- Probiotics

- Others

- Latin America Dietary Supplements Market Outlook, by Product Form, Value (US$ Bn), 2020-2033

- Tablets

- Capsules

- Liquid

- Gummies

- Powder

- Latin America Dietary Supplements Market Outlook, by Function, Value (US$ Bn), 2020-2033

- Gut Health

- Immune Health

- Sports Nutrition

- Skin Health

- Metabolic Health

- Weight Management

- Bone & Joint Health

- Others

- Latin America Dietary Supplements Market Outlook, by Sales Channel, Value (US$ Bn), 2020-2033

- Online

- Offline

- Latin America Dietary Supplements Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Brazil Dietary Supplements Market Outlook, by Product Type, 2020-2033

- Brazil Dietary Supplements Market Outlook, by Product Form, 2020-2033

- Brazil Dietary Supplements Market Outlook, by Function, 2020-2033

- Brazil Dietary Supplements Market Outlook, by Sales Channel, 2020-2033

- Mexico Dietary Supplements Market Outlook, by Product Type, 2020-2033

- Mexico Dietary Supplements Market Outlook, by Product Form, 2020-2033

- Mexico Dietary Supplements Market Outlook, by Function, 2020-2033

- Mexico Dietary Supplements Market Outlook, by Sales Channel, 2020-2033

- Argentina Dietary Supplements Market Outlook, by Product Type, 2020-2033

- Argentina Dietary Supplements Market Outlook, by Product Form, 2020-2033

- Argentina Dietary Supplements Market Outlook, by Function, 2020-2033

- Argentina Dietary Supplements Market Outlook, by Sales Channel, 2020-2033

- Rest of LATAM Dietary Supplements Market Outlook, by Product Type, 2020-2033

- Rest of LATAM Dietary Supplements Market Outlook, by Product Form, 2020-2033

- Rest of LATAM Dietary Supplements Market Outlook, by Function, 2020-2033

- Rest of LATAM Dietary Supplements Market Outlook, by Sales Channel, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Latin America Dietary Supplements Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Middle East & Africa Dietary Supplements Market Outlook, 2020 - 2033

- Middle East & Africa Dietary Supplements Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Botanicals

- Vitamins

- Amino Acids

- Enzymes

- Probiotics

- Others

- Middle East & Africa Dietary Supplements Market Outlook, by Product Form, Value (US$ Bn), 2020-2033

- Tablets

- Capsules

- Liquid

- Gummies

- Powder

- Middle East & Africa Dietary Supplements Market Outlook, by Function, Value (US$ Bn), 2020-2033

- Gut Health

- Immune Health

- Sports Nutrition

- Skin Health

- Metabolic Health

- Weight Management

- Bone & Joint Health

- Others

- Middle East & Africa Dietary Supplements Market Outlook, by Sales Channel, Value (US$ Bn), 2020-2033

- Online

- Offline

- Middle East & Africa Dietary Supplements Market Outlook, by Country, Value (US$ Bn), 2020-2033

- GCC Dietary Supplements Market Outlook, by Product Type, 2020-2033

- GCC Dietary Supplements Market Outlook, by Product Form, 2020-2033

- GCC Dietary Supplements Market Outlook, by Function, 2020-2033

- GCC Dietary Supplements Market Outlook, by Sales Channel, 2020-2033

- South Africa Dietary Supplements Market Outlook, by Product Type, 2020-2033

- South Africa Dietary Supplements Market Outlook, by Product Form, 2020-2033

- South Africa Dietary Supplements Market Outlook, by Function, 2020-2033

- South Africa Dietary Supplements Market Outlook, by Sales Channel, 2020-2033

- Egypt Dietary Supplements Market Outlook, by Product Type, 2020-2033

- Egypt Dietary Supplements Market Outlook, by Product Form, 2020-2033

- Egypt Dietary Supplements Market Outlook, by Function, 2020-2033

- Egypt Dietary Supplements Market Outlook, by Sales Channel, 2020-2033

- Nigeria Dietary Supplements Market Outlook, by Product Type, 2020-2033

- Nigeria Dietary Supplements Market Outlook, by Product Form, 2020-2033

- Nigeria Dietary Supplements Market Outlook, by Function, 2020-2033

- Nigeria Dietary Supplements Market Outlook, by Sales Channel, 2020-2033

- Rest of Middle East Dietary Supplements Market Outlook, by Product Type, 2020-2033

- Rest of Middle East Dietary Supplements Market Outlook, by Product Form, 2020-2033

- Rest of Middle East Dietary Supplements Market Outlook, by Function, 2020-2033

- Rest of Middle East Dietary Supplements Market Outlook, by Sales Channel, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Middle East & Africa Dietary Supplements Market Outlook, by Product Type, Value (US$ Bn), 2020-2033

- Competitive Landscape

- Company Vs Segment Heatmap

- Company Market Share Analysis, 2025

- Competitive Dashboard

- Company Profiles

- Abbott

- Company Overview

- Product Portfolio

- Financial Overview

- Business Strategies and Developments

- Bayer AG

- Amway Corp.

- Glanbia plc

- Pfizer Inc.

- Archer Daniels Midland

- NU SKIN

- GlaxoSmithKline plc.

- Herbalife Nutrition Ltd.

- Nature's Sunshine Products, Inc.

- XanGo, LLC

- RBK Nutraceuticals Pty Ltd

- American Health

- DuPont de Nemours, Inc.

- Others

- Abbott

- Appendix

- Research Methodology

- Report Assumptions

- Acronyms and Abbreviations

|

BASE YEAR |

HISTORICAL DATA |

FORECAST PERIOD |

UNITS |

|||

|

2025 |

|

2019 - 2024 |

2026 - 2033 |

Value: US$ Billion |

||

|

REPORT FEATURES |

DETAILS |

|

By Product Coverage |

|

|

By Application Coverage |

|

|

Geographical Coverage |

|

|

Leading Companies |

|

|

Report Highlights |

Key Market Indicators, Macro-micro economic impact analysis, Technological Roadmap, Key Trends, Driver, Restraints, and Future Opportunities & Revenue Pockets, Porter’s 5 Forces Analysis, Historical Trend (2019-2024), Market Estimates and Forecast, Market Dynamics, Industry Trends, Competition Landscape, Category, Region, Country-wise Trends & Analysis, COVID-19 Impact Analysis (Demand and Supply Chain) |