Pigments Market

Pigments Market Insights, Competitive Landscape, and Market Forecast - 2033

Pigments Market Outlook

The Pigments Market is valued at USD 34.7 Bn in 2026 and is projected to reach USD 51.2 Bn, growing at a CAGR of 6% by 2033.

Market Analysis in Brief

A steady rise in global population, higher penetration of emerging markets, as well as greater urbanization and industrialization, have all collectively led to the augmentation of the global pigments market. The market is slated to grow at a projected CAGR of 4.6% over the forecast period. The increasing demand for these products from continually growing end-use industries such as the paints and coatings, plastics, paper, and leather sectors, are expected to further boost the growth trajectory of the global pigments industry in the years ahead.

Key Report Findings

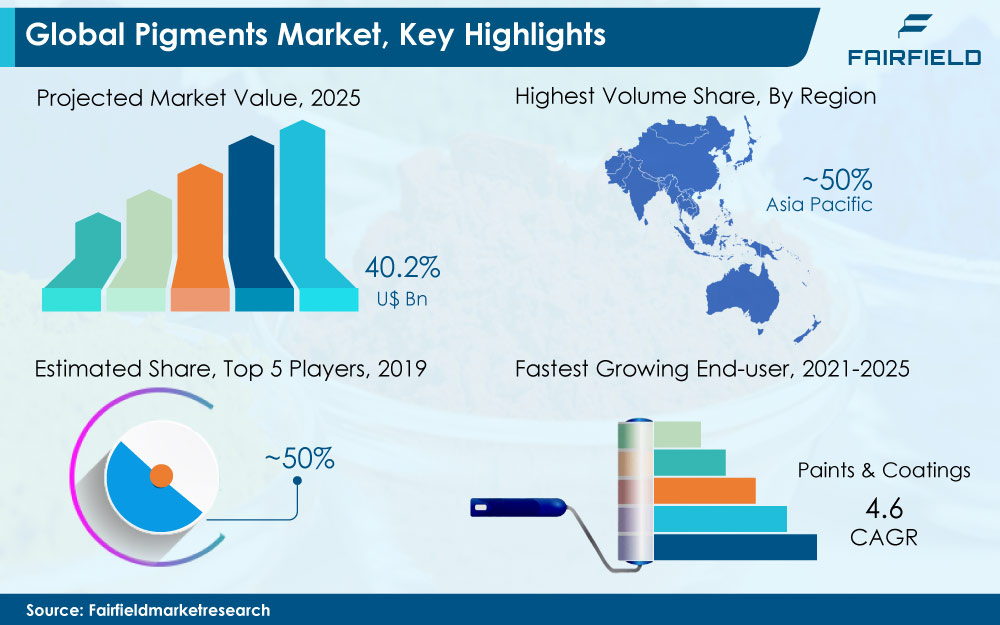

- The global pigments market is projected to achieve a valuation of US$40.2 Bn by 2025

- BASF SE is the largest pigments company in the world, with sales over €3.3 billion in 2020

- Titanium dioxide (TiO2) segment accounted for over 65% of the total pigment demand in 2018

- Asia Pacific to remain a regional frontrunner over the forecast period

Growth Drivers

Consumer Inclination Toward Vibrant, Bright, and Eco-friendly Color Shades

Pigments are extensively used in the production of paints & coatings to achieve a desired colour and finish. Pigments also enable paints to protect surfaces against corrosion and extreme weather conditions. Growing urbanization and infrastructure activities have created new growth avenues for players in the paints & coatings, plastics, and building materials spaces. The demand for pigments is expected to grow significantly in the coming years owing to a shift towards sustainable and eco-friendly products in mature pigments markets such as Europe, and North America.

Consumer preferences for vibrant, bright, and eco-friendly colour shades have compelled manufacturers to develop and innovate new chemistries. Furthermore, this market has also observed an upward trend in the consumption of complex and specialty pigments for building products in the last few years. The use of nanoparticles and nanotechnology is also expected to improve pigment performance. Very bright colours such as peacock feather and blue tarantula are created from nanostructures. Nanostructures are likely to create a unique, dynamic effect while ensuring exceptional durability. This is expected to lead to higher adoption of pigment products by consumers in the coming years, in turn boosting pigments market revenue.

Booming Synergies and Expansion Strategies

The pigment market in Europe is expected to go through a restructuring phase in the coming years, with BASF, and Clariant looking to divest their respective pigment businesses. Stiff competition from Asia-based pigment manufacturers, especially from China, and India, has forced companies in developed economies to divest their lower margin businesses in the pigments market space. Companies in Europe will also focus on high performance pigments, especially for the automotive industry.

Companies are also looking to launch new products to align their given portfolios with changing consumer preferences, new legislations, and to ensure that they still are environmentally efficient. For instance, Venator launched pigments to boost solar reflectance and for ultra-low moisture applications in the plastics industry. Croda launched an effect pigment to meet changing consumer preferences in the personal care sector.

The implementation of various strategies to ensure industry players keep or improve their market standing by developing novel products or by boosting operational efficiency is expected to have a positive influence on the growth trajectory of the global pigments market.

Growth Challenges

Pigments Market Hindered by Regulatory Roadblocks

The steady rise in energy costs and raw material prices are key challenges that are expected to hamper growth prospects for the global pigment market. Furthermore, in the last few years, the pigment industry has been under intense scrutiny by environmental and regulatory authorities for the emission of toxic pollutants. These regulations might result in the mushrooming of small non-compliant producers, particularly in the Asia Pacific region.

The pigments market of Asia is heavily dependent on China for intermediaries and finished products. Recently, the Chinese government had taken strict measures to deter polluters resulting in a substantial price rise for organic pigments. Obstacles such as this are expected to negatively affect the projected growth of the global pigments industry.

Growth Opportunities Across Regions

Asia Pacific to Strike a Lead with the Highest Production and Consumption

Asia Pacific is the largest producer and consumer in the global pigments market. Over the last couple of decades, the production of pigments has migrated to the Asia Pacific region, with China and India becoming major producers. Companies are expecting optimal growth in decorative coatings as disposable incomes in emerging economies continue to improve. This trend is expected to be fuelled by manufacturers complying with regulations, especially in the production of lead chromate and VOCs.

On the other hand, opportunities in North America and Europe are slated to be highlighted by the growing demand for industrial coatings, where high-performance pigments are required to meet standards. Multinational companies no longer have patent protection for their high-value pigments resulting in the migration of production bases to China.

Recently, there has been a downward trend in the production of pigments in North America, Europe, and Japan resulting in market restructuring and subsequent plant closures owing to lower margins. Furthermore, intense competition from Asia-based producers has compelled manufacturers in the mature pigments market to employ strategic decisions for their pigment businesses, thus transitioning toward higher value and customer-oriented pigment demand.

Key Market Players – Pigments Landscape

Some key companies in the global pigments market include BASF SE, Clariant AG, DIC Corporation, Ferro Corporation, Huntsman Corporation, Lanxess AG, the Chemours Company, Heubach GmbH, Merck KGaA, Sun Chemical Corporation, Dainichiseika Color & Chemicals Mfg. Co. Ltd., Sudarshan Chemical Industries Limited, KRONOS Worldwide Inc., Shepherd Color Company, and Cathay Industries Group, to name a few. To gain a competitive edge, various established industry players are now more focused on new product launches, partnerships, collaborations, acquisitions, and alliances.

Recent Notable Developments

- In August 2022, Chemours commenced mining its newest sand mine in Florida, allowing it to boost TiO2 outputs, which is used in white pigments.

- In October 2021, KRONOS introduced 9900 Digital White pigment, a newly developed aqueous pigment concentrate designed to fulfil the demands of the digital printing industry.

- In 2019, Tronox acquired the TiO2 business of Crystal to become the world’s largest vertically integrated TiO2 Furthermore, INEOS acquired Crystal’s North American business from Tronox in the same year. The acquisition will help Tronox strengthen its foothold in emerging and other developed markets.

The Global Pigments Market is Segmented as Below:

Product Coverage

- Inorganic

- Titanium Dioxide

- Iron Oxide

- Carbon Black

- Chromium Compounds

- Misc.

- Organic

- Azo

- Phthalocyanine

- Quinacridone

- Misc.

- Specialty

- Classic Organic

- Metallic

- High performance organic

- Light Interference

- Complex Inorganic

- Fluorescent

- Luminescent/phosphorescent

- Thermochromic

- Misc.

Application Coverage

- Paints & Coatings

- Printing Inks

- Plastics

- Commodity

- Engineered

- Construction Materials

- Misc.

Geographical Coverage

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- Egypt

- Rest of Middle East & Africa

Leading Companies

- Chemours

- TRONOX Holding PLC

- Venator

- Lomon Billions Group

- KRONOS Worldwide Inc.

- LANXESS

- DIC Corporation

- Altana AG

- Heubach GmbH

- Ferro Corporation

- Cathay Industries Group

Inside This Report You Will Find:

1. Executive Summary

2. Market Overview

3. Production Output and Trade Statistics, 2018 - 2020

4. Price Trends Analysis and Future Projects, 2017 - 2025

5. Global Pigments Market Outlook, 2017 - 2025

6. North America Pigments Market Outlook, 2017 - 2025

7. Europe Pigments Market Outlook, 2017 - 2025

8. Asia Pacific Pigments Market Outlook, 2017 - 2025

9. Latin America Pigments Market Outlook, 2017 - 2025

10. Middle East & AfricaPigments Market Outlook, 2017 - 2025

11. Competitive Landscape

12. Appendix

Post Sale Support, Research Updates & Offerings:

We value the trust shown by our customers in Fairfield Market Research. We support our clients through our post sale support, research updates and offerings.

- The report will be prepared in a PPT format and will be delivered in a PDF format.

- Additionally, Market Estimation and Forecast numbers will be shared in Excel Workbook.

- If a report being sold was published over a year ago, we will offer a complimentary copy of the updated research report along with Market Estimation and Forecast numbers within 2-3 weeks’ time of the sale.

- If we update this research study within the next 2 quarters, post purchase of the report, we will offer a Complimentary copy of the updated Market Estimation and Forecast numbers in Excel Workbook.

- If there is a geopolitical conflict, pandemic, recession, and the like which can impact global economic scenario and business activity, which might entirely alter the market dynamics or future projections in the industry, we will create a Research Update upon your request at a nominal charge.

- Executive Summary

- Global Pigments Market Snapshot

- Future Projections

- Key Market Trends

- Regional Snapshot, by Value, 2026

- Analyst Recommendations

- Market Overview

- Market Definitions and Segmentations

- Market Dynamics

- Drivers

- Restraints

- Market Opportunities

- Value Chain Analysis

- COVID-19 Impact Analysis

- Porter's Fiver Forces Analysis

- Impact of Russia-Ukraine Conflict

- PESTLE Analysis

- Regulatory Analysis

- Price Trend Analysis

- Current Prices and Future Projections, 2025-2033

- Price Impact Factors

- Global Pigments Market Outlook, 2020 - 2033

- Global Pigments Market Outlook, by Product Coverage, Value (US$ Bn), 2020-2033

- Inorganic

- Titanium Dioxide

- Iron Oxide

- Carbon Black

- Chromium Compounds

- Organic

- Azo

- Phthalocyanine

- Quinacridone

- Specialty

- Classic Organic

- Metallic

- High performance organic

- Light Interference

- Complex Inorganic

- Fluorescent

- Global Pigments Market Outlook, by Application Coverage, Value (US$ Bn), 2020-2033

- Paints & Coatings

- Printing Inks

- Plastics

- Commodity

- Engineered

- Construction Materials

- Global Pigments Market Outlook, by Region, Value (US$ Bn), 2020-2033

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Inorganic

- Global Pigments Market Outlook, by Product Coverage, Value (US$ Bn), 2020-2033

- North America Pigments Market Outlook, 2020 - 2033

- North America Pigments Market Outlook, by Product Coverage, Value (US$ Bn), 2020-2033

- Inorganic

- Titanium Dioxide

- Iron Oxide

- Carbon Black

- Chromium Compounds

- Organic

- Azo

- Phthalocyanine

- Quinacridone

- Specialty

- Classic Organic

- Metallic

- High performance organic

- Light Interference

- Complex Inorganic

- Fluorescent

- North America Pigments Market Outlook, by Application Coverage, Value (US$ Bn), 2020-2033

- Paints & Coatings

- Printing Inks

- Plastics

- Commodity

- Engineered

- Construction Materials

- North America Pigments Market Outlook, by Country, Value (US$ Bn), 2020-2033

- S. Pigments Market Outlook, by Product Coverage, 2020-2033

- S. Pigments Market Outlook, by Application Coverage, 2020-2033

- Canada Pigments Market Outlook, by Product Coverage, 2020-2033

- Canada Pigments Market Outlook, by Application Coverage, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Inorganic

- North America Pigments Market Outlook, by Product Coverage, Value (US$ Bn), 2020-2033

- Europe Pigments Market Outlook, 2020 - 2033

- Europe Pigments Market Outlook, by Product Coverage, Value (US$ Bn), 2020-2033

- Inorganic

- Titanium Dioxide

- Iron Oxide

- Carbon Black

- Chromium Compounds

- Organic

- Azo

- Phthalocyanine

- Quinacridone

- Specialty

- Classic Organic

- Metallic

- High performance organic

- Light Interference

- Complex Inorganic

- Fluorescent

- Europe Pigments Market Outlook, by Application Coverage, Value (US$ Bn), 2020-2033

- Paints & Coatings

- Printing Inks

- Plastics

- Commodity

- Engineered

- Construction Materials

- Europe Pigments Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Germany Pigments Market Outlook, by Product Coverage, 2020-2033

- Germany Pigments Market Outlook, by Application Coverage, 2020-2033

- Italy Pigments Market Outlook, by Product Coverage, 2020-2033

- Italy Pigments Market Outlook, by Application Coverage, 2020-2033

- France Pigments Market Outlook, by Product Coverage, 2020-2033

- France Pigments Market Outlook, by Application Coverage, 2020-2033

- K. Pigments Market Outlook, by Product Coverage, 2020-2033

- K. Pigments Market Outlook, by Application Coverage, 2020-2033

- Spain Pigments Market Outlook, by Product Coverage, 2020-2033

- Spain Pigments Market Outlook, by Application Coverage, 2020-2033

- Russia Pigments Market Outlook, by Product Coverage, 2020-2033

- Russia Pigments Market Outlook, by Application Coverage, 2020-2033

- Rest of Europe Pigments Market Outlook, by Product Coverage, 2020-2033

- Rest of Europe Pigments Market Outlook, by Application Coverage, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Inorganic

- Europe Pigments Market Outlook, by Product Coverage, Value (US$ Bn), 2020-2033

- Asia Pacific Pigments Market Outlook, 2020 - 2033

- Asia Pacific Pigments Market Outlook, by Product Coverage, Value (US$ Bn), 2020-2033

- Inorganic

- Titanium Dioxide

- Iron Oxide

- Carbon Black

- Chromium Compounds

- Organic

- Azo

- Phthalocyanine

- Quinacridone

- Specialty

- Classic Organic

- Metallic

- High performance organic

- Light Interference

- Complex Inorganic

- Fluorescent

- Asia Pacific Pigments Market Outlook, by Application Coverage, Value (US$ Bn), 2020-2033

- Paints & Coatings

- Printing Inks

- Plastics

- Commodity

- Engineered

- Construction Materials

- Asia Pacific Pigments Market Outlook, by Country, Value (US$ Bn), 2020-2033

- China Pigments Market Outlook, by Product Coverage, 2020-2033

- China Pigments Market Outlook, by Application Coverage, 2020-2033

- Japan Pigments Market Outlook, by Product Coverage, 2020-2033

- Japan Pigments Market Outlook, by Application Coverage, 2020-2033

- South Korea Pigments Market Outlook, by Product Coverage, 2020-2033

- South Korea Pigments Market Outlook, by Application Coverage, 2020-2033

- India Pigments Market Outlook, by Product Coverage, 2020-2033

- India Pigments Market Outlook, by Application Coverage, 2020-2033

- Southeast Asia Pigments Market Outlook, by Product Coverage, 2020-2033

- Southeast Asia Pigments Market Outlook, by Application Coverage, 2020-2033

- Rest of SAO Pigments Market Outlook, by Product Coverage, 2020-2033

- Rest of SAO Pigments Market Outlook, by Application Coverage, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Inorganic

- Asia Pacific Pigments Market Outlook, by Product Coverage, Value (US$ Bn), 2020-2033

- Latin America Pigments Market Outlook, 2020 - 2033

- Latin America Pigments Market Outlook, by Product Coverage, Value (US$ Bn), 2020-2033

- Inorganic

- Titanium Dioxide

- Iron Oxide

- Carbon Black

- Chromium Compounds

- Organic

- Azo

- Phthalocyanine

- Quinacridone

- Specialty

- Classic Organic

- Metallic

- High performance organic

- Light Interference

- Complex Inorganic

- Fluorescent

- Latin America Pigments Market Outlook, by Application Coverage, Value (US$ Bn), 2020-2033

- Paints & Coatings

- Printing Inks

- Plastics

- Commodity

- Engineered

- Construction Materials

- Latin America Pigments Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Brazil Pigments Market Outlook, by Product Coverage, 2020-2033

- Brazil Pigments Market Outlook, by Application Coverage, 2020-2033

- Mexico Pigments Market Outlook, by Product Coverage, 2020-2033

- Mexico Pigments Market Outlook, by Application Coverage, 2020-2033

- Argentina Pigments Market Outlook, by Product Coverage, 2020-2033

- Argentina Pigments Market Outlook, by Application Coverage, 2020-2033

- Rest of LATAM Pigments Market Outlook, by Product Coverage, 2020-2033

- Rest of LATAM Pigments Market Outlook, by Application Coverage, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Inorganic

- Latin America Pigments Market Outlook, by Product Coverage, Value (US$ Bn), 2020-2033

- Middle East & Africa Pigments Market Outlook, 2020 - 2033

- Middle East & Africa Pigments Market Outlook, by Product Coverage, Value (US$ Bn), 2020-2033

- Inorganic

- Titanium Dioxide

- Iron Oxide

- Carbon Black

- Chromium Compounds

- Organic

- Azo

- Phthalocyanine

- Quinacridone

- Specialty

- Classic Organic

- Metallic

- High performance organic

- Light Interference

- Complex Inorganic

- Fluorescent

- Middle East & Africa Pigments Market Outlook, by Application Coverage, Value (US$ Bn), 2020-2033

- Paints & Coatings

- Printing Inks

- Plastics

- Commodity

- Engineered

- Construction Materials

- Middle East & Africa Pigments Market Outlook, by Country, Value (US$ Bn), 2020-2033

- GCC Pigments Market Outlook, by Product Coverage, 2020-2033

- GCC Pigments Market Outlook, by Application Coverage, 2020-2033

- South Africa Pigments Market Outlook, by Product Coverage, 2020-2033

- South Africa Pigments Market Outlook, by Application Coverage, 2020-2033

- Egypt Pigments Market Outlook, by Product Coverage, 2020-2033

- Egypt Pigments Market Outlook, by Application Coverage, 2020-2033

- Nigeria Pigments Market Outlook, by Product Coverage, 2020-2033

- Nigeria Pigments Market Outlook, by Application Coverage, 2020-2033

- Rest of Middle East Pigments Market Outlook, by Product Coverage, 2020-2033

- Rest of Middle East Pigments Market Outlook, by Application Coverage, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Inorganic

- Middle East & Africa Pigments Market Outlook, by Product Coverage, Value (US$ Bn), 2020-2033

- Competitive Landscape

- Company Vs Segment Heatmap

- Company Market Share Analysis, 2025

- Competitive Dashboard

- Company Profiles

- Chemours

- Company Overview

- Product Portfolio

- Financial Overview

- Business Strategies and Developments

- TRONOX Holding PLC

- Venator

- Lomon Billions Group

- KRONOS Worldwide Inc.

- LANXESS

- DIC Corporation

- Altana AG

- Heubach GmbH

- Ferro Corporation

- Chemours

- Appendix

- Research Methodology

- Report Assumptions

- Acronyms and Abbreviations

|

BASE YEAR |

HISTORICAL DATA |

FORECAST PERIOD |

UNITS |

|||

|

2025 |

|

2019 - 2024 |

|

2026 - 2033 |

Value: US$ Billion

|

|

REPORT FEATURES |

DETAILS |

|

Product Coverage |

|

|

Application Coverage |

|

|

Geographical Coverage |

|

|

Leading Companies |

|

|

Report Highlights |

Market Estimates and Forecast, Market Dynamics, Industry Trends, Competition Landscape, Product-, Application-, Region-, Country-wise Trends & Analysis, COVID-19 Impact Analysis (Demand and Supply Chain), Key Trends |

Our Research Methodology

Considering the volatility of business today, traditional approaches to strategizing a game plan can be unfruitful if not detrimental. True ambiguity is no way to determine a forecast. A myriad of predetermined factors must be accounted for such as the degree of risk involved, the magnitude of circumstances, as well as conditions or consequences that are not known or unpredictable. To circumvent binary views that cast uncertainty, the application of market research intelligence to strategically posture, move, and enable actionable outcomes is necessary.

View Methodology

Quality Assured

Rigorous Validation Process

Confidentiality Assured

End-to-end Data Security

Custom Research Services

Tailored To Your Objectives

FAQs

Growing urbanization and infrastructure activities is anticipated to lift market growth for paints & coatings, printing inks, and plastics. Furthermore, shift in consumer preferences towards vibrant and eco-friendly colors is also driving the growth.

The global pigments market is expected to be valued at US$ 40 Bn by the end of 2025, wherein inorganic pigments accounts for the major portion of the market.

With a market share of more than 50%, Asia Pacific is anticipated to hold the highest volume share by 2025. It also projected to be largest production hub across all pigment categories by 2025.

In the inorganic pigments market, top 5 players accounted for more than 50% of the value share in 2019; while in organic & specialty segment, DIC held the highest market share in 2019.

Fairfield Market Research projects the global pigment market to grow with a CAGR of 3.6% by 2025, chiefly driven by robust outlook for specialty pigments.

Related Reports

Carbon-Negative Building Materials Market Insights, Competitive Landscape, and Market Forecast 2033

The carbon-negative building materials market, projected to grow from US$ 18.50 Billion in 2026 to US$ 32.75 Billion by 2033 at a CAGR of 8.5%

Redispersible Polymer Powder Market Insights, Competitive Landscape, and Market Forecast 2033

The redispersible polymer powder market to grow from US$ 2.40 Bn in 2026 to US$ 3.58 Bn by 2033, registering a CAGR of 5.9% during the forecast period.

Thermosetting Plastics Market Insights, Competitive Landscape, and Market Forecast 2033

The Thermosetting Plastics Market, projected to grow from US$92.10 Bn in 2026 to US$132.21 Bn by 2033 at a CAGR of 5.3%, with key trends and insights

EV Battery Materials Market Insights, Competitive Landscape, and Market Forecast 2033

EV battery materials market valued at US$ 60.10 Bn in 2026, projected to reach US$ 132.03 Bn by 2033, growing at a CAGR of 11.9% during 2026–2033.

Elastomeric Membrane Market Insights, Competitive Landscape, and Market Forecast 2033

Elastomeric membrane market is projected to grow from US$25.60 billion in 2026 to US$34.84 billion by 2033, registering a 4.5% CAGR during the forecast period.

Water Recycle and Reuse Market Insights, Competitive Landscape, and Market Forecast 2033

The global water recycle and reuse market is projected to reach US$ 41.66 Bn by 2033, at a 9.2% CAGR, driven by growing water conservation efforts