High Voltage Equipment Market Size, Share, and Growth Forecast 2026 - 2033

Key Market Highlights

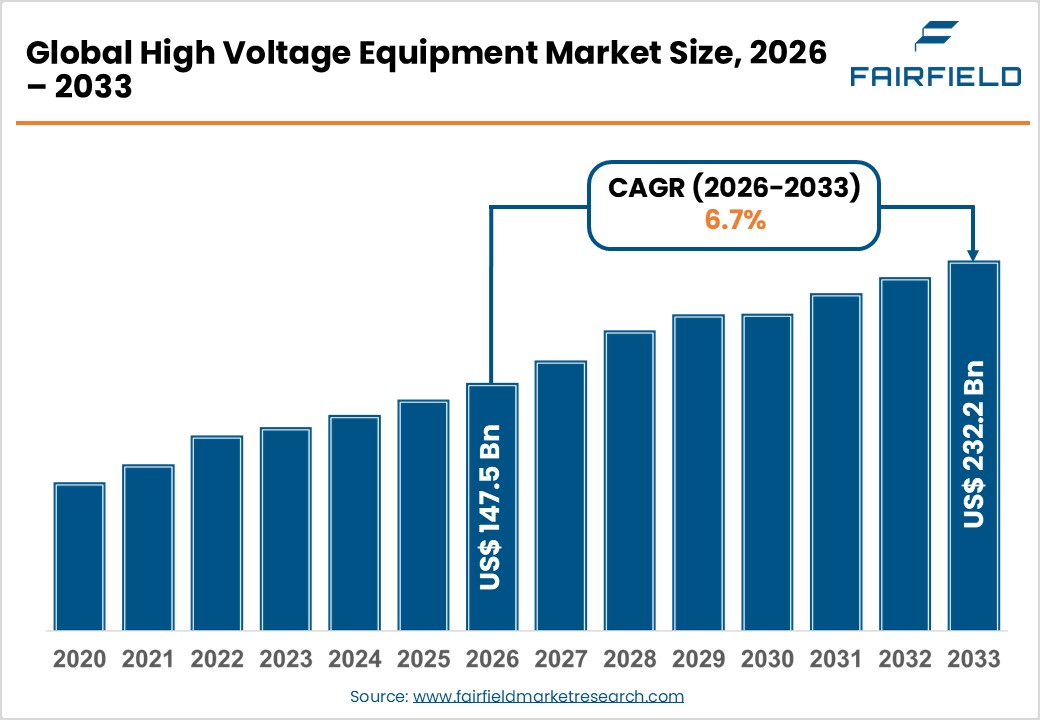

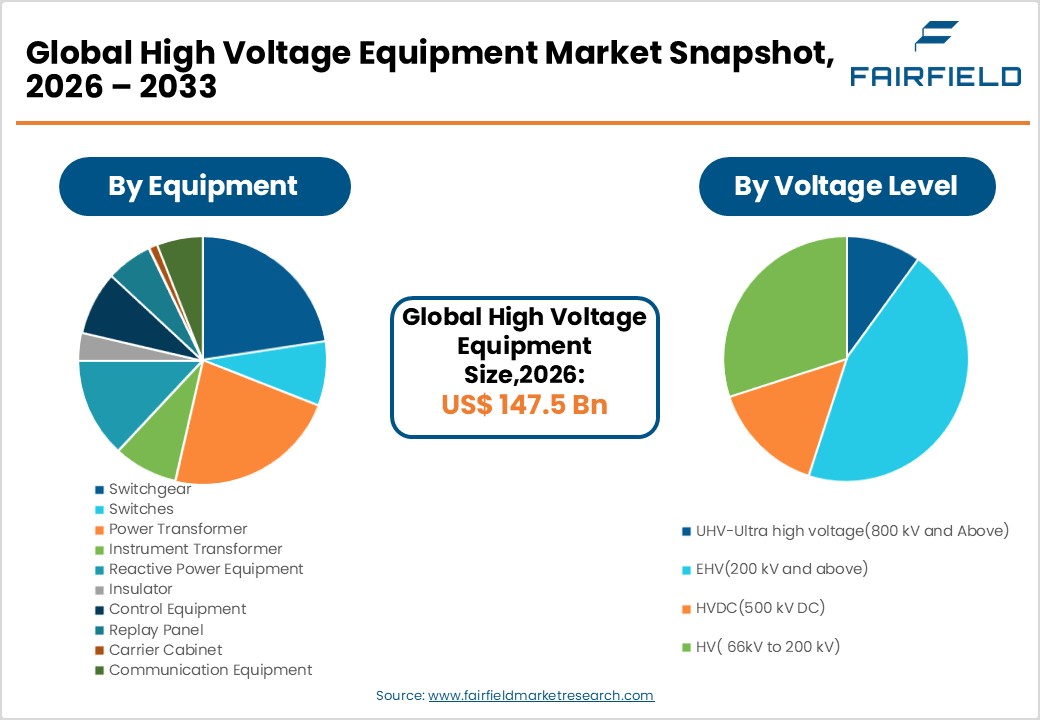

- The global High Voltage Equipment market size is likely to be valued at US$D 147.5 billion in 2026 and is expected to reach USD 232.2 billion by 2033, growing at a CAGR of 6.70% during the forecast period from 2026 to 2033.

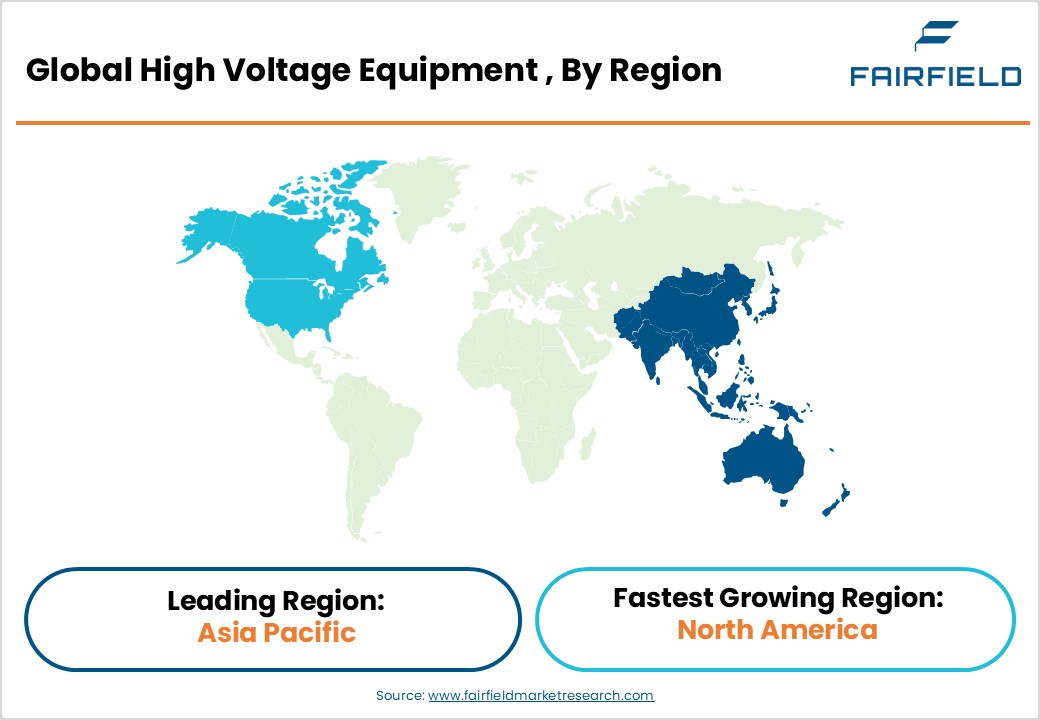

- Leading Region Market: Asia Pacific leads the global High Voltage Equipment market with approximately 30% revenue share in 2026, driven by massive grid investments in China and India and accelerating renewable energy capacity additions across the region’s major economies.

- Fastest growing Region Market: North America is the fastest-growing regional market, propelled by the S. Inflation Reduction Act (IRA) and the Building a Better Grid Initiative, which collectively target the construction and upgrade of over 100,000 miles of high-voltage transmission lines in the coming decade.

- Power Transformer is the dominant equipment segment, holding approximately 32% of market share in 2026, supported by sustained global infrastructure investment programs and an ongoing aging transformer replacement cycle in North America and Western Europe.

- The EHV (Extra High Voltage, 200 kV and above) voltage level segment leads with approximately 38% market share, driven by long-distance transmission expansion in China, India, and Brazil to connect remote renewable energy parks to national demand centers.

- The growing global deployment of HVDC technology for offshore wind connections and cross-border power interconnections represents the foremost market opportunity, with over 200 HVDC projects under active development worldwide offering substantial long-term revenue potential for equipment providers.

Market Dynamics

Market Growth Drivers

Accelerating Grid Modernization and Electrification Initiatives

The global push for grid modernization is a significant catalyst for the high voltage equipment market. Aging transmission infrastructure in developed economies, combined with surging electricity demand in developing nations, is compelling utilities to upgrade their networks at an accelerating paceIn the United States, the Department of Energy (DOE) is funding the Grid Resilience and Innovation Partnerships (GRIP) program to strengthen grid infrastructure against climate-related disruptions. Similarly, China’s State Grid Corporation is committing to major annual investments in grid upgrades. These massive capital expenditure programs drive demand for switchgear, power transformers, advanced protection relays, and control systems key components within the high voltage equipment ecosystem, reinforcing a positive long-term market outlook.

Rapid Expansion of Renewable Energy Integration

The unprecedented scale-up of renewable energy capacity worldwide is fundamentally reshaping demand for high voltage equipment. Solar and wind energy installations are predominantly located far from load centers, necessitating extensive high-voltage transmission networks to deliver power reliably. According to the International Renewable Energy Agency (IRENA), global renewable power capacity additions reached a record 295 GW in 2022, with over 3,400 GW of total installed capacity globally. The integration of variable renewable energy into power grids demands sophisticated reactive power equipment, HVDC systems, and advanced protection relays. The European Union under the REPowerEU plan targets 1,236 GW of renewable capacity by 2030, requiring extensive transmission upgrades, new substation deployments, and grid balancing infrastructure investments across member states.

Market Restraints

High Capital Expenditure and Extended Project Lead Times

The high voltage equipment market faces a significant restraint in the form of extremely high upfront capital requirements and prolonged project cycles. Large power transformers typically require lead times of 18 to 36 months and can cost millions per unit, depending on voltage rating and design specs. For utilities in developing economies operating under constrained public budgets, these costs represent a formidable barrier to procurement. Additionally, obtaining environmental clearances, right-of-way permissions, and regulatory approvals for high-voltage transmission projects can extend timelines by 2 to 5 years, creating funding gaps and project delays that materially impede market expansion, particularly in South Asia, Sub-Saharan Africa, and parts of Latin America where financing ecosystems are less mature.

Supply Chain Disruptions and Raw Material Price Volatility

The manufacturing of high voltage equipment is heavily dependent on key raw materials such as copper, silicon steel, and transformer oil, all of which are subject to significant price volatility. Copper prices surged sharply in recent years, directly impacting production costs for transformers, switchgear, and high-voltage cables, according to the London Metal Exchange (LME), copper prices have remained elevated amid persistent global supply-demand imbalances. Geopolitical tensions and pandemic-induced logistics disruptions have further compounded component shortages and delivery delays, adding margin pressure on equipment manufacturers and creating procurement uncertainty for utilities procuring high voltage assets across global project pipelines.

Market Opportunities

HVDC Technology Deployment for Long-Distance Transmission

High Voltage Direct Current (HVDC) technology represents a transformative growth opportunity for the high voltage equipment market. HVDC systems offer significantly lower transmission losses over long distances compared to conventional alternating current infrastructure, making them ideal for intercontinental power grids and offshore wind farm grid connections. ABB (Hitachi Energy) and Siemens Energy are pioneering next-generation Voltage Source Converter (VSC)-based HVDC platforms with modular, scalable designs. The North Sea Wind Power Hub project, designed to connect offshore wind capacity across the North Sea to multiple European countries, is expected to require HVDC infrastructure investment of over € 30 Billion. With over 200 HVDC projects currently under development globally, this high-growth segment offers market participants exceptional opportunities for technology monetization, long-term service contracts, and strategic project partnerships.

Digital Substation and Smart Grid Infrastructure Development

The transition toward digital substations and smart grid architectures presents a compelling market opportunity for high voltage equipment providers. Digital substations utilizing IEC 61850 communications standards replace conventional copper wiring with fiber-optic Ethernet networks, significantly reducing installation costs and enabling real-time condition monitoring and predictive maintenance. India’s National Smart Grid Mission (NSGM) has allocated INR 22,000 Crore for smart grid development across the country, while China continues to invest heavily in intelligent grid management systems. The European Commission’s smart grid action plan mandates deployment of digital grid technologies across EU member states. This digital transformation wave creates growing demand for advanced SCADA systems, intelligent electronic devices, and communication equipment key high-value segments within the high voltage equipment market.

Segmental Insights

Equipment Analysis

The Power Transformer segment dominates the high voltage equipment market by equipment type, accounting for approximately 32% share in 2026. Power transformers are the cornerstone of electrical transmission and distribution networks, essential for stepping up voltage for long-distance transmission and stepping down for safe distribution to end-users. The scale of global transmission infrastructure investments particularly in China, India, and the United States has driven sustained demand for large-format transformers rated at 220 kV and above, U.S. electric utilities are investing heavily in infrastructure. The replacement cycle for aging transformer fleets in North America and Western Europe where many units have exceeded their 30- to 40-year design life creates steady, long-term demand. Power transformers lead in market revenue, closely followed by switchgear and reactive power equipment.

Voltage Level Analysis

The EHV (Extra High Voltage, 200 kV and above) segment commands the leading position in the high voltage equipment market by voltage level, accounting for approximately 38% of total market share in 2026. EHV transmission systems offer superior power transfer capability over long distances with minimal transmission losses, making them the preferred choice for national and regional transmission backbone networks. Major economies including China, India, the United States, and Brazil have extensively deployed EHV infrastructure as part of their inter-state and inter-regional transmission expansion programs. India’s Power Grid Corporation (POWERGRID) operates one of the world’s largest EHV transmission networks, with over 170,000 circuit kilometers of high-voltage transmission lines. The growing integration of large-scale renewable energy parks in remote areas necessitates dedicated EHV transmission corridors, further reinforcing this segment’s dominant market position.

Regional Insights

North America High Voltage Equipment Market Trends

North America leads as the fastest-growing region for high voltage equipment, driven by huge federal investments in grid resilience and clean energy shifts. The U.S. Inflation Reduction Act (IRA) of 2022 pours funds into clean energy and climate efforts, spurring demand for transmission infrastructure and high voltage gear. The U.S. Department of Energy's Building a Better Grid Initiative also pushes for building and upgrading tens of thousands of miles of high-voltage lines over the next decade to modernize the grid..

In Canada, Natural Resources Canada has prioritized grid interconnection projects under the Clean Electricity Regulations, requiring substantial capital investment in high voltage switchgear and transformers. The region’s robust regulatory framework, combined with a well-established innovation ecosystem anchored by leading research universities and national laboratories, continues to accelerate the adoption of advanced high voltage technologies including digital substations, HVDC systems, and SF6-free gas-insulated switchgear (GIS). Major utilities such as American Electric Power (AEP) and Duke Energy are committing multi-billion-dollar capital programs to upgrade aging transmission assets.

Europe High Voltage Equipment Market Trends

Europe represents a mature yet highly dynamic market for high voltage equipment, underpinned by the European Union’s ambitious climate targets under the European Green Deal and REPowerEU plan. Germany, as Europe’s largest economy, leads regional investment with its Energiewende (Energy Transition) program requiring extensive grid expansion. Bundesnetzagentur (Federal Network Agency) approved over 14,000 km of new transmission lines under the Federal Network Development Plan to accommodate renewable energy flows from north to south. France and Spain are expanding cross-border power interconnections to enhance energy security, creating significant additional demand for HVDC equipment.

The United Kingdom’s National Grid Electricity System Operator has committed to achieving a fully decarbonized electricity system by 2035, requiring substantial investment in offshore wind grid connections and onshore transmission upgrades. Regulatory harmonization through ENTSO-E (European Network of Transmission System Operators for Electricity) frameworks and IEC technical standards is fostering a more integrated high voltage equipment market across EU member states, benefiting multinational equipment suppliers and accelerating deployment of standardized digital substation and smart grid solutions.

Asia Pacific High Voltage Equipment Market Trends

Asia Pacific dominates the global high voltage equipment market with approximately 30% of total market share in 2026, driven primarily by China, India, Japan, and the rapidly growing ASEAN economies. China is by far the world’s largest single market for high voltage equipment, with State Grid Corporation of China (SGCC) and China Southern Power Grid (CSG) executing multi-trillion-yuan grid investment programs. China has pioneered UHV (Ultra High Voltage) transmission at ±800 kV DC and 1,000 kV AC to deliver power from remote renewable energy bases in the west to densely populated eastern load centers, creating unique and demanding equipment specifications.

India is the fastest-growing major market within the region, with the government targeting 500 GW of non-fossil fuel-based energy capacity by 2030 under the National Electricity Plan. Japan’s grid operators are investing in offshore wind infrastructure and HVDC interconnectors as part of the post-Fukushima (2011) energy sector restructuring. ASEAN nations, backed by Asian Development Bank (ADB) financing under the ASEAN Power Grid initiative, are rapidly developing regional power interconnections that drive significant demand for high voltage transformers, switchgear, and associated substation equipment across the region.

Competitive Landscape

The global high voltage equipment market exhibits a moderately consolidated structure, with the top five players Siemens Energy, ABB (Hitachi Energy), GE Vernova, Schneider Electric, and Mitsubishi Electric collectively accounting for approximately 45–50% of total market revenue. Market leaders differentiate through technological innovation, particularly in HVDC, digital substation, and eco-friendly gas-insulated switchgear (GIS) technologies utilizing SF6-free alternatives in response to EU environmental regulations. Strategic acquisitions, joint ventures with regional manufacturers, and localization of production in high-growth markets such as India, Southeast Asia, and the Middle East represent core expansion strategies. Companies are also investing in digital asset management platforms and lifecycle service contracts to generate predictable recurring revenue streams alongside traditional equipment sales.

Key Market Developments

- January, 2025: Siemens Energy secured a landmark contract to supply HVDC transmission equipment for the SuedLink underground cable project in Germany, valued at over € 3 Billion, reinforcing its leading market position in European grid infrastructure modernization.

- March, 2024: Hitachi Energy announced the successful commissioning of its advanced HVDC Light converter station in Australia, enhancing power transfer capacity between New South Wales and Victoria to support the country’s renewable energy transition objectives.

- October, 2023: GE Vernova inaugurated a new high-voltage switchgear manufacturing facility in Vadodara, India, expanding production capacity to address the surge in domestic demand driven by India’s national grid modernization and renewable energy integration programs.

Companies Covered in High Voltage Equipment Market

- Siemens Energy

- GE Vernova

- ABB (Hitachi Energy)

- Schneider Electric

- Hitachi Energy

- Mitsubishi Electric

- Toshiba

- Eaton

- Larsen & Toubro (L&T)

- TBEA

- Fuji Electric

- Hyundai Electric

- Bharat Heavy Electricals Limited (BHEL)

- Crompton Greaves Power and Industrial Solutions

- Xi’an XD High Voltage Apparatus Co., Ltd.

- SPX Transformer Solutions

Market Segmentation

By Equipment

- Switchgear

- Switches

- Power Transformer

- Instrument Transformer

- Reactive Power Equipment

- Insulator

- Control Equipment

- Relay Panel

- Carrier Cabinet

- Communication Equipment

- SCADA

- Earthing Material

- Battery Set

By Voltage Level

- UHV – Ultra High Voltage (800 kV and Above)

- EHV (200 kV and Above)

- HVDC (500 kV DC)

- HV (66 kV to 200 kV)

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Executive Summary

- Global High Voltage Equipment Market Snapshot

- Future Projections

- Key Market Trends

- Regional Snapshot, by Value, 2026

- Analyst Recommendations

- Market Overview

- Market Definitions and Segmentations

- Market Dynamics

- Drivers

- Restraints

- Market Opportunities

- Value Chain Analysis

- COVID-19 Impact Analysis

- Porter's Five Forces Analysis

- Impact of Russia-Ukraine Conflict

- PESTLE Analysis

- Regulatory Analysis

- Price Trend Analysis

- Current Prices and Future Projections, 2025-2033

- Price Impact Factors

- Global High Voltage Equipment Market Outlook, 2020 - 2033

- Global High Voltage Equipment Market Outlook, by Equipment, Value (US$ Bn), 2020-2033

- Switchgear

- Switches

- Power Transformer

- Instrument Transformer

- Reactive Power Equipment

- Insulator

- Control Equipment

- Replay Panel

- Carrier Cabinet

- Communication Equipment

- Global High Voltage Equipment Market Outlook, by Voltage level, Value (US$ Bn), 2020-2033

- UHV-Ultra high voltage(800 kV and Above)

- EHV(200 kV and above)

- HVDC(500 kV DC)

- HV( 66kV to 200 kV)

- Global High Voltage Equipment Market Outlook, by Region, Value (US$ Bn), 2020-2033

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Global High Voltage Equipment Market Outlook, by Equipment, Value (US$ Bn), 2020-2033

- North America High Voltage Equipment Market Outlook, 2020 - 2033

- North America High Voltage Equipment Market Outlook, by Equipment, Value (US$ Bn), 2020-2033

- Switchgear

- Switches

- Power Transformer

- Instrument Transformer

- Reactive Power Equipment

- Insulator

- Control Equipment

- Replay Panel

- Carrier Cabinet

- Communication Equipment

- North America High Voltage Equipment Market Outlook, by Voltage level, Value (US$ Bn), 2020-2033

- UHV-Ultra high voltage(800 kV and Above)

- EHV(200 kV and above)

- HVDC(500 kV DC)

- HV( 66kV to 200 kV)

- North America High Voltage Equipment Market Outlook, by Country, Value (US$ Bn), 2020-2033

- U.S. High Voltage Equipment Market Outlook, by Equipment, 2020-2033

- U.S. High Voltage Equipment Market Outlook, by Voltage level, 2020-2033

- Canada High Voltage Equipment Market Outlook, by Equipment, 2020-2033

- Canada High Voltage Equipment Market Outlook, by Voltage level, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- North America High Voltage Equipment Market Outlook, by Equipment, Value (US$ Bn), 2020-2033

- Europe High Voltage Equipment Market Outlook, 2020 - 2033

- Europe High Voltage Equipment Market Outlook, by Equipment, Value (US$ Bn), 2020-2033

- Switchgear

- Switches

- Power Transformer

- Instrument Transformer

- Reactive Power Equipment

- Insulator

- Control Equipment

- Replay Panel

- Carrier Cabinet

- Communication Equipment

- Europe High Voltage Equipment Market Outlook, by Voltage level, Value (US$ Bn), 2020-2033

- UHV-Ultra high voltage(800 kV and Above)

- EHV(200 kV and above)

- HVDC(500 kV DC)

- HV( 66kV to 200 kV)

- Europe High Voltage Equipment Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Germany High Voltage Equipment Market Outlook, by Equipment, 2020-2033

- Germany High Voltage Equipment Market Outlook, by Voltage level, 2020-2033

- Italy High Voltage Equipment Market Outlook, by Equipment, 2020-2033

- Italy High Voltage Equipment Market Outlook, by Voltage level, 2020-2033

- France High Voltage Equipment Market Outlook, by Equipment, 2020-2033

- France High Voltage Equipment Market Outlook, by Voltage level, 2020-2033

- U.K. High Voltage Equipment Market Outlook, by Equipment, 2020-2033

- U.K. High Voltage Equipment Market Outlook, by Voltage level, 2020-2033

- Spain High Voltage Equipment Market Outlook, by Equipment, 2020-2033

- Spain High Voltage Equipment Market Outlook, by Voltage level, 2020-2033

- Russia High Voltage Equipment Market Outlook, by Equipment, 2020-2033

- Russia High Voltage Equipment Market Outlook, by Voltage level, 2020-2033

- Rest of Europe High Voltage Equipment Market Outlook, by Equipment, 2020-2033

- Rest of Europe High Voltage Equipment Market Outlook, by Voltage level, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Europe High Voltage Equipment Market Outlook, by Equipment, Value (US$ Bn), 2020-2033

- Asia Pacific High Voltage Equipment Market Outlook, 2020 - 2033

- Asia Pacific High Voltage Equipment Market Outlook, by Equipment, Value (US$ Bn), 2020-2033

- Switchgear

- Switches

- Power Transformer

- Instrument Transformer

- Reactive Power Equipment

- Insulator

- Control Equipment

- Replay Panel

- Carrier Cabinet

- Communication Equipment

- Asia Pacific High Voltage Equipment Market Outlook, by Voltage level, Value (US$ Bn), 2020-2033

- UHV-Ultra high voltage(800 kV and Above)

- EHV(200 kV and above)

- HVDC(500 kV DC)

- HV( 66kV to 200 kV)

- Asia Pacific High Voltage Equipment Market Outlook, by Country, Value (US$ Bn), 2020-2033

- China High Voltage Equipment Market Outlook, by Equipment, 2020-2033

- China High Voltage Equipment Market Outlook, by Voltage level, 2020-2033

- Japan High Voltage Equipment Market Outlook, by Equipment, 2020-2033

- Japan High Voltage Equipment Market Outlook, by Voltage level, 2020-2033

- South Korea High Voltage Equipment Market Outlook, by Equipment, 2020-2033

- South Korea High Voltage Equipment Market Outlook, by Voltage level, 2020-2033

- India High Voltage Equipment Market Outlook, by Equipment, 2020-2033

- India High Voltage Equipment Market Outlook, by Voltage level, 2020-2033

- Southeast Asia High Voltage Equipment Market Outlook, by Equipment, 2020-2033

- Southeast Asia High Voltage Equipment Market Outlook, by Voltage level, 2020-2033

- Rest of SAO High Voltage Equipment Market Outlook, by Equipment, 2020-2033

- Rest of SAO High Voltage Equipment Market Outlook, by Voltage level, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Asia Pacific High Voltage Equipment Market Outlook, by Equipment, Value (US$ Bn), 2020-2033

- Latin America High Voltage Equipment Market Outlook, 2020 - 2033

- Latin America High Voltage Equipment Market Outlook, by Equipment, Value (US$ Bn), 2020-2033

- Switchgear

- Switches

- Power Transformer

- Instrument Transformer

- Reactive Power Equipment

- Insulator

- Control Equipment

- Replay Panel

- Carrier Cabinet

- Communication Equipment

- Latin America High Voltage Equipment Market Outlook, by Voltage level, Value (US$ Bn), 2020-2033

- UHV-Ultra high voltage(800 kV and Above)

- EHV(200 kV and above)

- HVDC(500 kV DC)

- HV( 66kV to 200 kV)

- Latin America High Voltage Equipment Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Brazil High Voltage Equipment Market Outlook, by Equipment, 2020-2033

- Brazil High Voltage Equipment Market Outlook, by Voltage level, 2020-2033

- Mexico High Voltage Equipment Market Outlook, by Equipment, 2020-2033

- Mexico High Voltage Equipment Market Outlook, by Voltage level, 2020-2033

- Argentina High Voltage Equipment Market Outlook, by Equipment, 2020-2033

- Argentina High Voltage Equipment Market Outlook, by Voltage level, 2020-2033

- Rest of LATAM High Voltage Equipment Market Outlook, by Equipment, 2020-2033

- Rest of LATAM High Voltage Equipment Market Outlook, by Voltage level, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Latin America High Voltage Equipment Market Outlook, by Equipment, Value (US$ Bn), 2020-2033

- Middle East & Africa High Voltage Equipment Market Outlook, 2020 - 2033

- Middle East & Africa High Voltage Equipment Market Outlook, by Equipment, Value (US$ Bn), 2020-2033

- Switchgear

- Switches

- Power Transformer

- Instrument Transformer

- Reactive Power Equipment

- Insulator

- Control Equipment

- Replay Panel

- Carrier Cabinet

- Communication Equipment

- Middle East & Africa High Voltage Equipment Market Outlook, by Voltage level, Value (US$ Bn), 2020-2033

- UHV-Ultra high voltage(800 kV and Above)

- EHV(200 kV and above)

- HVDC(500 kV DC)

- HV( 66kV to 200 kV)

- Middle East & Africa High Voltage Equipment Market Outlook, by Country, Value (US$ Bn), 2020-2033

- GCC High Voltage Equipment Market Outlook, by Equipment, 2020-2033

- GCC High Voltage Equipment Market Outlook, by Voltage level, 2020-2033

- South Africa High Voltage Equipment Market Outlook, by Equipment, 2020-2033

- South Africa High Voltage Equipment Market Outlook, by Voltage level, 2020-2033

- Egypt High Voltage Equipment Market Outlook, by Equipment, 2020-2033

- Egypt High Voltage Equipment Market Outlook, by Voltage level, 2020-2033

- Nigeria High Voltage Equipment Market Outlook, by Equipment, 2020-2033

- Nigeria High Voltage Equipment Market Outlook, by Voltage level, 2020-2033

- Rest of Middle East High Voltage Equipment Market Outlook, by Equipment, 2020-2033

- Rest of Middle East High Voltage Equipment Market Outlook, by Voltage level, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Middle East & Africa High Voltage Equipment Market Outlook, by Equipment, Value (US$ Bn), 2020-2033

- Competitive Landscape

- Company Vs Segment Heatmap

- Company Market Share Analysis, 2025

- Competitive Dashboard

- Company Profiles

- Sinopec

- Company Overview

- Product Portfolio

- Financial Overview

- Business Strategies and Developments

- ExxonMobil

- LyondellBasell

- SABIC

- Dow

- Formosa Plastics

- INEOS

- BASF

- LG Chem

- Sumitomo Chemical

- Mitsubishi Chemical

- Borealis

- PetroChina

- Sinopec

- Appendix

- Research Methodology

- Report Assumptions

- Acronyms and Abbreviations

|

BASE YEAR |

HISTORICAL DATA |

FORECAST PERIOD |

UNITS |

|||

|

2025 |

|

2020 - 2025 |

2026 - 2033 |

Value: US$ Million |

||

|

REPORT FEATURES |

DETAILS |

|

By Equipment Coverage |

|

|

By Voltage level Coverage |

|

|

Geographical Coverage |

|

|

Leading Companies |

|

|

Report Highlights |

Key Market Indicators, Macro-micro economic impact analysis, Technological Roadmap, Key Trends, Driver, Restraints, and Future Opportunities & Revenue Pockets, Porter’s 5 Forces Analysis, Historical Trend (2019-2024), Market Estimates and Forecast, Market Dynamics, Industry Trends, Competition Landscape, Category, Region, Country-wise Trends & Analysis, COVID-19 Impact Analysis (Demand and Supply Chain) |