Vegan Food Market

Global Industry Analysis, Size, Share, Growth, Trends, and Forecast 2023-2030 - By Product, Technology, Grade, Application, End-user, Region: (North America, Europe, Asia Pacific, Latin America and Middle East and Africa)

This study intends to unfurl the multiple facets of global vegan food market. The insights offered in the report aid in market growth examination during the forecast period.

Market Analysis in Brief

Veganism is a lifestyle movement that has been gaining momentum, leading to a growing number of prominent individuals making the transition to this type of way of life, particularly in recent years. As such, apart from the personal consumption of vegan food, several commercial establishments are also beginning to adopt and implement this type of cuisine among their existing repertoire of offerings. The increasing prevalence of various chronic diseases has also led to many switching from being non-vegetarians or pescatarians to a vegan diet, due to the many benefits associated with this type of living. Despite the inflated costs associated with this type of food and the lack of overall variation, more heightened globalization and urbanization are also leading to greater availability and higher consumption of vegan products. The vegan food market is slated to grow promisingly in the years to come.

Key Report Findings:

- Vegan food market receives strong tailwinds from rising accessibility of non-dairy alternatives

- Adoption of healthier lifestyles to fuel opportunities in vegan food industry

- Crucial market growth role – methane emissions increased by 50% (1961-2018)

- Nearly 65% of the global population is lactose intolerant

- North America to retain its dominant positioning in market for vegan food

Growth Drivers

Increasing Adoption of a Vegan Lifestyle

The adoption of sedentary lifestyles has resulted in an increase in health complications such as obesity, diabetes, and cardiovascular disorders. This pushed the consumption of healthy, nutrition-rich food that promotes effective weight management. Apart from eating in intervals, more consumers are now switching to vegan food owing to the health benefits associated with that lifestyle. Vegan food helps in lowering fat content and reducing weight, enhancing blood flow, and in providing fibrous nutrition along with essential minerals and vitamins needed for cell development. It has been a popular consumer perception that vegans have a higher life expectancy as compared to individuals that consumed a meat-based diet. Consumption of vegan food also regulates body metabolism thus enhancing immunity. With this as a backdrop, the consumption of vegan food is expected to increase, bolstering growth for this global market for vegan food in the process.

GHG Emissions by Animal-based Products under Scrutiny

Additionally, the curbing of greenhouse gas (GHG) emissions emitted through dairy and meat livestock has been a more significant concern recently. According to the Food and Agriculture Organization (UN FAO), methane emissions from livestock, increased by 50% between 1961-2018, and this is likely to grow further owing to the demand for animal-based products. By adopting veganism, animal exploitation is prevented along with significantly reducing GHG emissions, thus supporting environmental wellbeing. These aspects are expected to have a major influence on market for vegan food in the coming years.

Vegan Milk Grows Popular Among Lactose Intolerant Population

There has been an increasing demand for dairy product alternatives globally. This can be attributed mainly due to a growing lactose intolerant population. For instance, according to the analysis by the National Centre for Biotechnology Information (NCBI), about 65% of the global population is lactose intolerant. This has led to an exponential increase in the number of individuals consuming or looking to consume alternatives to dairy products like milk. The availability of vegan milk products derived from oats, soy, almonds, among other sources, coupled with the growing inclination towards such alternatives are elements expected to boost the growth trajectory of the market for vegan food in the coming years. In addition to this, health-conscious individuals are also opting for vegan milk due to its perceived benefits such as weight management, adequate nutritional value, and overall body maintenance. This increasing demand for vegan milk is expected to contribute significantly towards the market value of the vegan food industry.

Growth Challenges

Expensive Costs, and Potentially Associated Deficiencies

Owing to the relatively short commercial lifespan of the vegan food industry, more research and development is needed to create products that have greater mass appeal. Manufacturers presently aim to offer plant-based alternatives to the general populace; however, the pricing of these products tends to be much higher than conventional consumables. Taste and texture also differ immensely. This has led to the slower adoption of vegan food among many consumers worldwide. Additionally, vegan food products have been found to be nutritionally deficient in certain cases, having a low protein content level for example, and this can lead to various disorders such as hormonal imbalance, anaemia, and vitamin B12 deficiency. Factors such as this are expected to potentially hinder growth prospects for the global market for vegan food in the future.

COVID-19 Impact

The onset of the COVID-19 pandemic resulted in the imposing of restrictions by respective governments on the movement of people and goods, as well as the hampered supply of necessary raw materials, among other operational hurdles. This led to a significant decline in generated revenues for many industries and this was no different for the global vegan food industry. However, as restrictions were gradually relaxed, post the 3rd and 4th waves, this global vegan food market regressed to its pre-COVID-19 state of operations, with projections of exponential growth expected to be achieved over a short length of time.

Growth Opportunities Across Regions

North America to Flex Dominance

North America is expected to account for the majority share of the global vegan food market over the forecast period. This can be attributed to a higher adoption rate of vegan products here, as well as a higher level of awareness concerning the benefits associated with a vegan lifestyle. According to the Vegetarian Resource Group (VRG), more than 2% of the overall population in the United States is vegan and this is likely to increase further in the coming years. Additionally, increasing GDP per capita across countries in this region is also expected to further fuel the consumption of vegan food, albeit it’s higher pricing.

On the other hand, the Asia Pacific region is expected to index significant growth in the coming years. For instance, according to the UN FAO, the lowest meat consumption has been observed in India, from a global perspective. In 2020, out of approximately 500 million vegetarians, around 1% individuals were vegans, and this trend is rapidly proliferating in India. These factors are expected to generate significant opportunities for industry players, in turn fuelling growth for the global vegan food market.

Competitive Landscape

Key players in this market include DANONE S.A., Archer Daniels Midland Company, Conagra Inc., Axiom Foods Inc., Beyond Meat, Alpro, Tofutti Brands Inc., and Kellogg Company. To gain a competitive edge, various established industry players are now more focused on new product launches, partnerships, collaborations, acquisitions, and alliances.

Recent Notable Developments:

- In February 2021, Danone S.A. acquired Follow Your Heart, a plant-based pioneer, for US$6 million. This move is expected to aid Danone in improving its capabilities of developing and launching novel vegan products

- In May 2021, Target launched Good & Gather, a new plant-based sub-brand, with a portfolio offering of 30 plant-based products

- In May 2021, Nestle, a food conglomerate, launched Wunda, a new vegan milk brand, specifically focused for release in Portugal, the Netherlands, and France

- In July 2021, Upfield launched Violife, a new vegan cheese brand in the Middle East. This brand’s range is an allergen-free alternative to dairy products, and is available in slices, cubes, and grated form, in two flavours – Cheddar and Mozzarella

Regional Classification of the Global Vegan Food Market is Listed Below:

North America

- U.S.

- Canada

Europe

- Germany

- France

- Spain

- U.K.

- Italy

- Russia

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- Southeast Asia

- Rest of Asia Pacific

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East & Africa

1. Executive Summary

1.1. Global Vegan Food Market: Snapshot

1.2. Future Projections, 2022 - 2030, (US$ Mn)

1.3. Key Segment Analysis and Competitive Insights

1.4. Analyst Recommendations

2. Market Overview

2.1. Market Definitions and Segmentations

2.2. Market Dynamics

2.2.1. Drivers

2.2.1.1. Driver A

2.2.1.2. Driver B

2.2.1.3. Driver C

2.2.2. Restraints

2.2.2.1. Restraint 1

2.2.2.2. Restraint 2

2.2.3. Market Opportunities Matrix

2.3. Value Chain Analysis

2.4. Porter’s Five Forces Analysis

2.5. Covid-19 Impact Analysis

2.5.1. Supply

2.5.2. Demand

2.6. Government Regulations

2.7. Vegan Trends: Key Regions

2.8. Recent Industry Developments

2.9. Economic Analysis

2.10. PESTLE Analysis

3. Global Vegan Food Market Outlook, 2019 - 2030

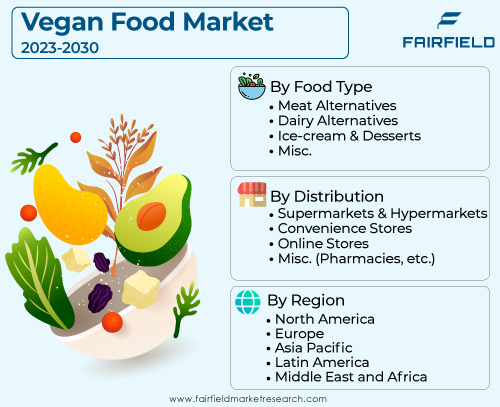

3.1. Global Vegan Food Market Outlook, by Food Type, Value (US$ Mn), 2019 - 2030

3.1.1. Key Highlights

3.1.1.1. Meat Alternatives

3.1.1.2. Dairy Alternatives

3.1.1.3. Ice-cream & Desserts

3.1.1.4. Misc.

3.1.2. Market Attractiveness Analysis

3.2. Global Vegan Food Market Outlook, by Distribution Channels, Value (US$ Mn), 2019 - 2030

3.2.1. Key Highlights

3.2.1.1. Supermarkets & Hypermarkets

3.2.1.2. Convenience Stores

3.2.1.3. Online Stores

3.2.1.4. Misc. (Pharmacies, etc.)

3.2.2. Market Attractiveness Analysis

3.3. Global Vegan Food Market Outlook, by Region, Value (US$ Mn), 2019 - 2030

3.3.1. Key Highlights

3.3.1.1. North America

3.3.1.2. Europe

3.3.1.3. Asia Pacific

3.3.1.4. Latin America

3.3.1.5. Middle East & Africa

3.3.2. Market Attractiveness Analysis

4. North America Vegan Food Market Outlook, 2019 - 2030

4.1. North America Vegan Food Market Outlook, by Food Type, Value (US$ Mn), 2019 - 2030

4.1.1. Key Highlights

4.1.1.1. Meat Alternatives

4.1.1.2. Dairy Alternatives

4.1.1.3. Ice-cream & Desserts

4.1.1.4. Misc.

4.2. North America Vegan Food Market Outlook, by Distribution Channels, Value (US$ Mn), 2019 - 2030

4.2.1. Key Highlights

4.2.1.1. Supermarkets & Hypermarkets

4.2.1.2. Convenience Stores

4.2.1.3. Online Stores

4.2.1.4. Misc. (Pharmacies, etc.)

4.3. North America Vegan Food Market Outlook, by Country, Value (US$ Mn), 2019 - 2030

4.3.1. Key Highlights

4.3.1.1. U.S.

4.3.1.2. Canada

5. Europe Vegan Food Market Outlook, 2019 - 2030

5.1. Europe Vegan Food Market Outlook, by Food Type, Value (US$ Mn), 2019 - 2030

5.1.1. Key Highlights

5.1.1.1. Meat Alternatives

5.1.1.2. Dairy Alternatives

5.1.1.3. Ice-cream & Desserts

5.1.1.4. Misc.

5.2. Europe Vegan Food Market Outlook, by Distribution Channels, Value (US$ Mn), 2019 - 2030

5.2.1. Key Highlights

5.2.1.1. Supermarkets & Hypermarkets

5.2.1.2. Convenience Stores

5.2.1.3. Online Stores

5.2.1.4. Misc. (Pharmacies, etc.)

5.3. Europe Vegan Food Market Outlook, by Country, Value (US$ Mn), 2019 - 2030

5.3.1. Key Highlights

5.3.1.1. Germany

5.3.1.2. France

5.3.1.3. U.K.

5.3.1.4. Italy

5.3.1.5. Spain

5.3.1.6. Turkey

5.3.1.7. Russia

5.3.1.8. Rest of Europe

5.3.2. BPS Analysis/Market Attractiveness Analysis

6. Asia Pacific Vegan Food Market Outlook, 2019 - 2030

6.1. Asia Pacific Vegan Food Market Outlook, by Food Type, Value (US$ Mn), 2019 - 2030

6.1.1. Key Highlights

6.1.1.1. Meat Alternatives

6.1.1.2. Dairy Alternatives

6.1.1.3. Ice-cream & Desserts

6.1.1.4. Misc.

6.2. Asia Pacific Vegan Food Market Outlook, by Distribution Channels, Value (US$ Mn), 2019 - 2030

6.2.1. Key Highlights

6.2.1.1. Supermarkets & Hypermarkets

6.2.1.2. Convenience Stores

6.2.1.3. Online Stores

6.2.1.4. Misc. (Pharmacies, etc.)

6.3. Asia Pacific Vegan Food Market Outlook, by Country, Value (US$ Mn), 2019 - 2030

6.3.1. Key Highlights

6.3.1.1. China

6.3.1.2. Japan

6.3.1.3. South Korea

6.3.1.4. India

6.3.1.5. Southeast Asia

6.3.1.6. Rest of Asia Pacific

6.3.2. BPS Analysis/Market Attractiveness Analysis

7. Latin America Vegan Food Market Outlook, 2019 - 2030

7.1. Latin America Vegan Food Market Outlook, by Food Type, Value (US$ Mn), 2019 - 2030

7.1.1. Key Highlights

7.1.1.1. Meat Alternatives

7.1.1.2. Dairy Alternatives

7.1.1.3. Ice-cream & Desserts

7.1.1.4. Misc.

7.2. Latin America Vegan Food Market Outlook, by Distribution Channels, Value (US$ Mn), 2019 - 2030

7.2.1. Key Highlights

7.2.1.1. Supermarkets & Hypermarkets

7.2.1.2. Convenience Stores

7.2.1.3. Online Stores

7.2.1.4. Misc. (Pharmacies, etc.)

7.3. Latin America Vegan Food Market Outlook, by Country, Value (US$ Mn), 2019 - 2030

7.3.1. Key Highlights

7.3.1.1. Brazil

7.3.1.2. Mexico

7.3.1.3. Rest of Latin America

7.3.2. BPS Analysis/Market Attractiveness Analysis

8. Middle East & Africa Vegan Food Market Outlook, 2019 - 2030

8.1. Middle East & Africa Vegan Food Market Outlook, by Food Type, Value (US$ Mn), 2019 - 2030

8.1.1. Key Highlights

8.1.1.1. Meat Alternatives

8.1.1.2. Dairy Alternatives

8.1.1.3. Ice-cream & Desserts

8.1.1.4. Misc.

8.2. Middle East & Africa Vegan Food Market Outlook, by Distribution Channels, Value (US$ Mn), 2019 - 2030

8.2.1. Key Highlights

8.2.1.1. Supermarkets & Hypermarkets

8.2.1.2. Convenience Stores

8.2.1.3. Online Stores

8.2.1.4. Misc. (Pharmacies, etc.)

8.3. Middle East & Africa Vegan Food Market Outlook, by Country, Value (US$ Mn), 2019 - 2030

8.3.1. Key Highlights

8.3.1.1. GCC

8.3.1.2. South Africa

8.3.1.3. Egypt

8.3.1.4. Rest of Middle East & Africa

8.3.2. BPS Analysis/Market Attractiveness Analysis

9. Competitive Landscape

9.1. Company Market Share Analysis, 2021

9.2. Competition Matrix (By Tier and Size of companies)

9.3. Strategic Collaborations

9.4. Company Profiles

9.4.1. Danone S.A.

9.4.1.1. Company Overview

9.4.1.2. Product Portfolio

9.4.1.3. Financial Overview

9.4.1.4. Business Strategies and Development

(*Note: Above details would be available for below list of companies based on availability)

9.4.2. Conagra Inc.

9.4.3. Beyond Meat

9.4.4. Archer Daniel Midland Company

9.4.5. Daiya Foods Inc.

9.4.6. Hain Celestial Group

9.4.7. Impossible Foods Inc.

9.4.8. Tofutti Brands Inc.

9.4.9. Eden Foods Inc.

9.4.10. Amy's Kitchen

9.4.11. VITASOY International Holdings Ltd.

9.4.12. Plamil Foods Ltd.

10. Appendix

10.1. Acronyms and Abbreviations

10.2. Research Scope & Assumptions

10.3. Research Methodology and Information Sources

|

BASE YEAR |

HISTORICAL DATA |

FORECAST PERIOD |

UNITS |

|||

|

2022 |

|

2018 - 2022 |

2023 - 2030 |

Value: US$ Million |

||

|

REPORT FEATURES |

DETAILS |

|

Food Coverage |

|

|

Distribution Channel Coverage |

|

|

Geographical Coverage |

|

|

Leading Companies |

|

|

Report Highlights |

Market Estimates and Forecast, Market Dynamics, Industry Trends, Competition Landscape, Food -, Distribution Channel-, Region-, Country-wise Trends & Analysis, COVID-19 Impact Analysis (Demand and Supply), Key Market Trends |

Our Research Methodology

Considering the volatility of business today, traditional approaches to strategizing a game plan can be unfruitful if not detrimental. True ambiguity is no way to determine a forecast. A myriad of predetermined factors must be accounted for such as the degree of risk involved, the magnitude of circumstances, as well as conditions or consequences that are not known or unpredictable. To circumvent binary views that cast uncertainty, the application of market research intelligence to strategically posture, move, and enable actionable outcomes is necessary.

View Methodology

Quality Assured

Rigorous Validation Process

Confidentiality Assured

End-to-end Data Security

Custom Research Services

Tailored To Your Objectives

Related Reports

Vegan Supplements Market Insights, Competitive Landscape, and Market Forecast 2033

Vegan Supplements Market is valued at US$ 11.70 Bn in 2026 and is projected to reach US$ 18.42 Bn by 2033, growing at a CAGR of 6.7% from 2026 to 2033.

Infant Formula Market Insights, Competitive Landscape, and Market Forecast 2033

Infant Formula Market valued at US$ 75.30 Bn in 2026, projected to reach US$ 151.47 Bn by 2033, growing at a CAGR of 10.5% from 2026 to 2033.

Green Banana Flour Market Insights, Competitive Landscape, and Market Forecast 2033

Green Banana Flour Market is valued at US$ 750 Mn in 2026 and projected to reach US$ 1,302.12 Mn by 2033, growing at a CAGR of 8.2% through 2033.

Nutraceutical Excipients Market Insights, Competitive Landscape, and Market Forecast 2033

The nutraceutical excipients market will grow from US$5.20 billion in 2026 to US$8.68 billion by 2033, driven by growing demand for dietary supplements.

Tortilla Market Insights, Competitive Landscape, and Market Forecast 2033

The tortilla market is projected to reach US$75.36 billion by 2033 growing at a 5.1% CAGR, driven by rising demand for convenient and ready-to-eat foods.

RTD Canned Cocktail Market Insights, Competitive Landscape, and Market Forecast 2033

RTD Canned Cocktail Market to reach US$11.15 Bn by 2033 at 14.2% CAGR, driven by premium RTDs, e-commerce growth, and consumer demand.