Industrial Pump Market Size, Share, and Growth Forecast 2026 – 2033

Key Market Highlights

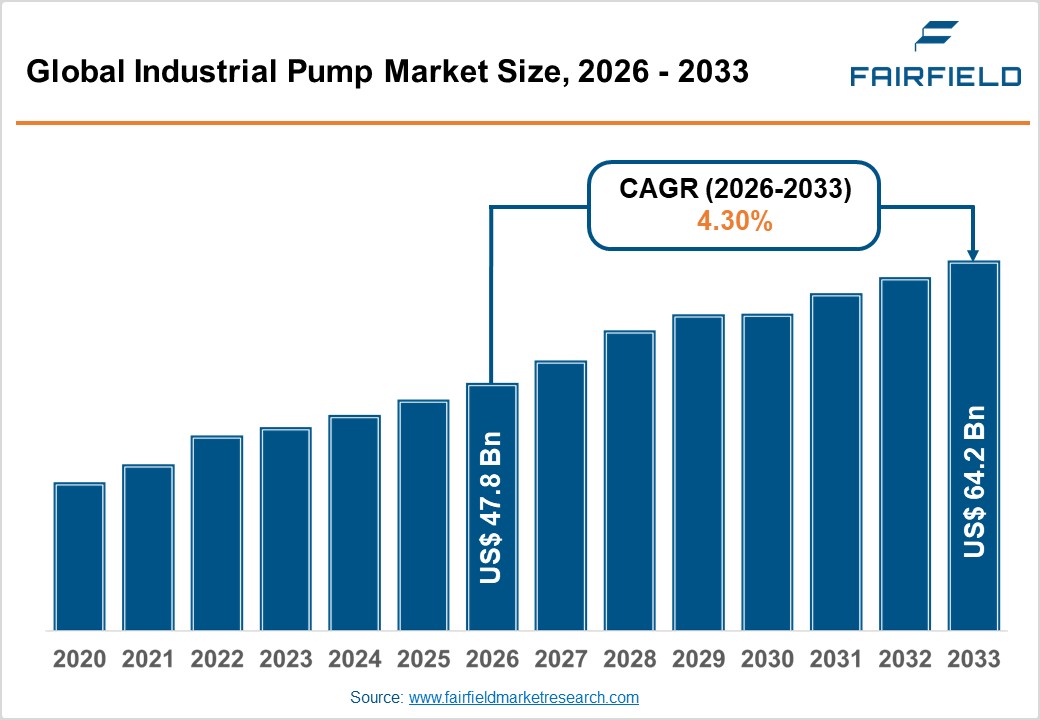

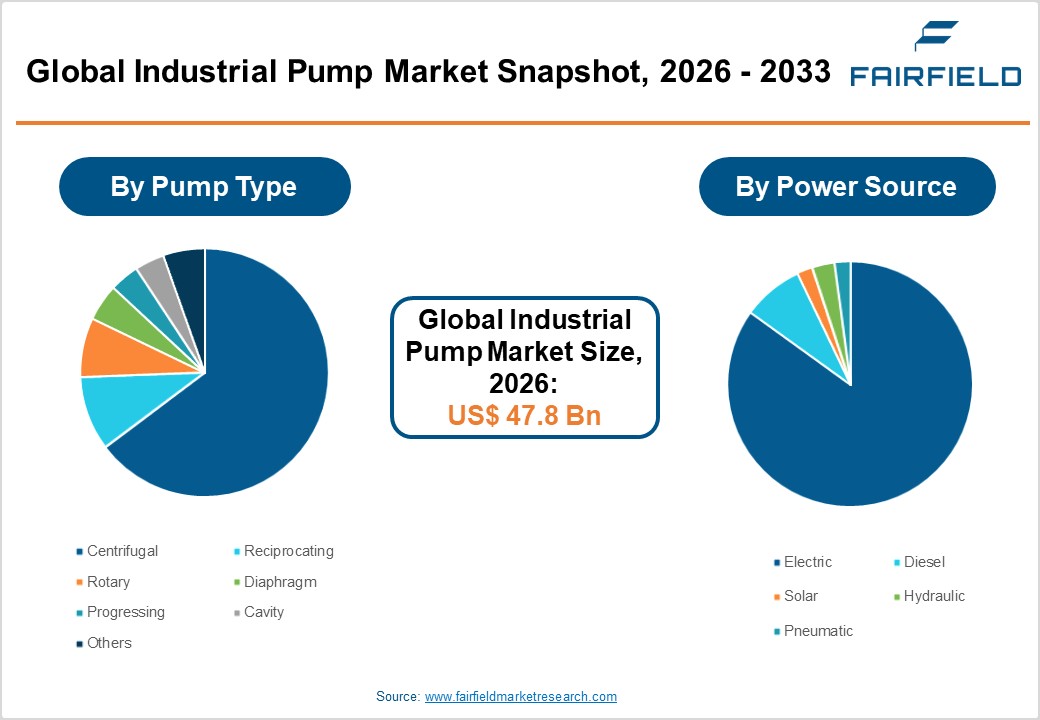

- The global Industrial Pump Market size is likely to be valued at USD 47.8 billion in 2026 and is expected to reach USD 64.2 billion by 2033, growing at a CAGR of 4.30% during the forecast period from 2026 to 2033.

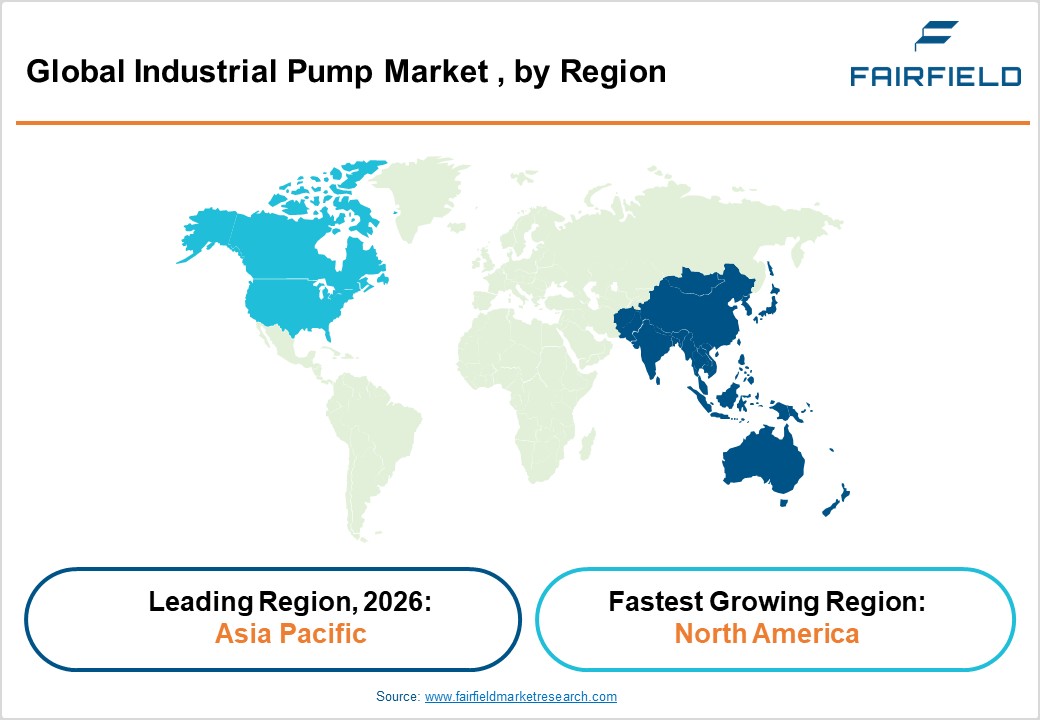

- Asia Pacific dominates the industrial pump market with approximately 46% revenue share, underpinned by China's large-scale infrastructure investments, India's Jal Jeevan Mission, and rapid industrialization across ASEAN economies.

- North America is the fastest-growing market, driven by the U.S. Infrastructure Investment and Jobs Act, LNG sector expansion, semiconductor fab construction, and accelerating replacement of aging pump infrastructure.

- Centrifugal pumps lead the pump type segment with approximately 60% market share, owing to their versatility, low maintenance requirements, and broad applicability across water, oil and gas, and chemical processing industries.

- Solar-powered pumps represent the fastest-growing power source segment, driven by India's PM-KUSUM scheme, declining solar costs, and rapid expansion of off-grid agricultural irrigation in Africa and Southeast Asia.

- Smart pump and IIoT-integrated platforms enabling predictive maintenance and energy optimization represent the most significant commercial opportunity, with potential maintenance cost reductions of up to 25% attracting strong interest from global industrial operators.

Market Dynamics

Market Growth Drivers

- Expanding Global Water and Wastewater Infrastructure Investment

The global imperative to address water scarcity and upgrade aging water infrastructure is a fundamental driver for the industrial pump market. The United Nations estimates that over 2 billion people currently lack access to safe drinking water, prompting governments worldwide to commit substantial capital to water supply and treatment networks. The U.S. Infrastructure Investment and Jobs Act allocated USD 55 billion specifically for water infrastructure upgrades. Industrial centrifugal and submersible pumps are critical components in municipal water supply, irrigation systems, and industrial effluent treatment. The World Bank projects that global water sector investment will need to exceed trillions of money annually by 2030, creating sustained long-term demand for pump solutions across the water value chain.

- Rising Oil and Gas Exploration and Production Activities

The sustained global demand for hydrocarbons continues to drive substantial capital expenditure in upstream oil and gas operations, directly benefiting the industrial pump market. Reciprocating and progressing cavity pumps are essential in upstream drilling, crude oil transfer, and enhanced oil recovery applications. According to the International Energy Agency (IEA), global upstream oil and gas capital expenditure is projected to exceed billions in 2025, reflecting a sustained investment cycle. The expansion of liquefied natural gas (LNG) terminals globally, particularly in the Middle East and North America, further intensifies demand for high-pressure, corrosion-resistant pump technologies capable of handling volatile and abrasive fluid streams under extreme operating conditions.

Market Restraints

- High Energy Consumption and Escalating Operational Costs

Industrial pumps account for a disproportionately large share of industrial energy consumption. According to the U.S. Department of Energy (DOE), pumping systems consume approximately 20% of the world's electrical energy and up to 50% of energy in certain process industries. Rising global electricity prices with industrial electricity costs increasing by an average of 15-20% across major economies between 2021 and 2024 are placing significant pressure on end-users' total cost of ownership. This dynamic constrains procurement budgets, particularly among small and mid-sized industrial operators, and slows the uptake of large-scale pump installations.

- Supply Chain Disruptions and Raw Material Price Volatility

Industrial pump manufacturing relies on a range of metallic raw materials including cast iron, stainless steel, and specialized alloys. Persistent volatility in steel and nickel prices with London Metal Exchange (LME) nickel prices experiencing swings exceeding 40% between 2022 and 2024 has directly inflated pump manufacturing costs and compressed margins for producers. Ongoing geopolitical uncertainties and logistics disruptions affecting global shipping have further extended lead times for pump components, delaying project execution for end-users in construction, oil and gas, and municipal water sectors. These supply-side pressures remain a structural restraint on market growth.

Market Opportunities

- Solar-Powered Pump Adoption in Emerging Economies

Solar-powered pumping systems represent one of the most compelling growth opportunities in the industrial pump market, particularly in agricultural irrigation and rural water supply applications across Africa, South Asia, and Southeast Asia. India's PM-KUSUM scheme targeting the installation of over 3.5 million solar pumps for agricultural use has already catalyzed significant procurement activity. The International Renewable Energy Agency (IRENA) reports that solar pump costs have declined by over 80% in the past decade, making off-grid solar pumping economically competitive with diesel alternatives. Manufacturers that develop integrated solar pump systems with remote monitoring, IoT connectivity, and modular design are well-positioned to capture this rapidly expanding addressable market in regions with limited grid infrastructure.

- Smart Pump Technologies and Industrial IoT Integration

The integration of Industrial Internet of Things (IIoT) capabilities into pump systems is creating a significant new value creation opportunity for market participants. Smart pumps embedded with sensors for real-time condition monitoring, predictive maintenance, and energy optimization are enabling end-users to achieve substantial reductions in unplanned downtime and lifecycle costs. The European Commission's Industry 5.0 initiative and the U.S. Advanced Manufacturing National Program Office (AMNPO) are both promoting digital integration in industrial process equipment. Industry data indicates that predictive maintenance enabled by smart pump technologies can reduce maintenance costs by up to 25% and extend equipment life by 30-40%. Pump manufacturers offering intelligent pump-as-a-service (PaaS) business models and digital service platforms are emerging as the most differentiated players in the evolving industrial pump landscape.

Segmental Insights

- By Pump Type Analysis

Among all pump types, Centrifugal pumps hold the dominant position in the global industrial pump market, commanding approximately 60% of total revenue. Centrifugal pumps are preferred across a wide spectrum of industries including water and wastewater treatment, oil and gas, power generation, and chemicals owing to their simple design, high flow rate capability, low maintenance requirements, and cost effectiveness relative to positive displacement alternatives. The Hydraulic Institute estimates that centrifugal pumps account for the majority of pump installations in industrial water and process fluid handling globally. Their scalability from small circulating duties to large-scale slurry and cooling water applications makes them the default choice across most industrial segments, reinforcing their market leadership through the forecast horizon.

- By Power Source Analysis

Electric-powered pumps represent the leading segment by power source, accounting for approximately 65% of the global industrial pump market. The dominance of electric pumps is driven by their higher operational efficiency, lower emissions profile, precise speed control via variable frequency drives (VFDs), and compatibility with automated industrial processes. The global expansion of electricity grid infrastructure including significant grid investment programs in China and India is steadily extending the reach of grid-connected pump operations. Growing regulatory pressure on diesel pump emissions, particularly in the European Union and North America, is also accelerating the replacement of diesel-powered units with electric alternatives in both municipal and industrial process applications.

- By Pump Orientation Analysis

Surface pumps lead the pump orientation segment, accounting for approximately 62% of overall market revenue. Surface-mounted pump installations are dominant in most industrial process environments including chemical plants, power stations, refineries, and manufacturing facilities, where they offer advantages in accessibility, ease of maintenance, and scalability. The World Resources Institute (WRI) identifies that large-scale industrial water use, a primary application for surface pumps that accounts for over 19% of global freshwater withdrawals, underscoring the broad deployment base. However, submersible pumps are witnessing faster growth driven by expanding groundwater extraction programs, offshore oil operations, and municipal sewage lift stations, particularly across rapidly urbanizing Asia Pacific and African markets.

Regional Insights

- North America Industrial Pump Market Trends

North America is the fastest-growing region in the global industrial pump market, propelled by aggressive infrastructure reinvestment, reshoring of manufacturing activities, and the rapid expansion of the liquefied natural gas (LNG) export sector. The U.S. Infrastructure Investment and Jobs Act is catalyzing significant pump procurement across water utilities, wastewater treatment, and municipal irrigation systems. The U.S. Army Corps of Engineers alone oversees thousands of water infrastructure projects requiring industrial pump systems.

The CHIPS and Science Act and Inflation Reduction Act (IRA) are driving new semiconductor fab and clean energy facility construction across the U.S., each requiring advanced cooling, chemical delivery, and fluid handling pump systems. Regulatory frameworks from the U.S. EPA on pump energy efficiency are accelerating the replacement of legacy pump installations with energy-efficient models, creating an active near-term replacement market.

- Europe Industrial Pump Market Trends

Europe represents a mature but innovation-driven industrial pump market, with Germany, France, and the United Kingdom as leading national markets. Germany's role as a global hub for chemical engineering and mechanical process equipment manufacturing, a home to world-class pump producers ensures it remains the center of industrial pump innovation in Europe. The EU Industrial Emissions Directive (IED) and Energy Efficiency Directive (EED) are mandating stricter energy performance benchmarks for industrial fluid handling equipment.

Spain and France are expanding desalination and water recycling infrastructure under the EU Water Framework Directive, creating demand for high-efficiency pump solutions in water-stressed regions. The European Green Deal's mandate to achieve carbon neutrality by 2050 is pushing European pump manufacturers toward developing CO₂-neutral production processes and launching next-generation magnetically coupled and canned motor pumps that eliminate mechanical seals and minimize leakage, aligning with the EU's zero-pollution ambition.

- Asia Pacific Industrial Pump Market Trends

Asia Pacific is the leading regional market, commanding approximately 46% of global industrial pump revenue. China remains the dominant national market, driven by massive investment in chemical parks, petrochemical complexes, thermal power plants, and municipal water networks. China's 14th Five-Year Plan (2021–2025) allocated substantial funding for water conservancy infrastructure, with continued prioritization expected in the 15th Five-Year Plan. Japan's precision manufacturing sector and aging water infrastructure replacement programs are sustaining steady demand for high-specification pump technologies.

India is emerging as a high-growth market, supported by the Jal Jeevan Mission targeting piped water supply to all 191 million rural households and rapid expansion in oil refining, petrochemical, and pharmaceutical manufacturing. ASEAN economies including Vietnam, Indonesia, and Thailand are attracting diversifying manufacturing investment, generating incremental pump demand across food processing, chemicals, and mining sectors. The convergence of strong domestic demand and cost-competitive manufacturing positions Asia Pacific as the central growth engine of the global industrial pump market.

Competitive Landscape

The global industrial pump market is moderately fragmented, featuring a mix of large multinational manufacturers and a vast base of regional and application-specific producers. Leading players such as Flowserve Corporation, Xylem Inc., KSB SE & Co. KGaA, and Sulzer Ltd. differentiate through broad product portfolios, global service networks, and advanced engineering capabilities. Key competitive strategies include capacity expansion in Asia Pacific, development of energy-efficient and smart pump platforms, and strategic acquisitions to expand application reach. Service-oriented business models, including long-term maintenance contracts and digital pump monitoring subscriptions, are gaining traction as key revenue diversification channels among market leaders.

Key Market Developments

- In February 2025, Xylem Inc. launched its next-generation Lowara e-SV series electric submersible pump platform with integrated IoT connectivity, targeting water utilities and industrial process applications across Europe and North America.

- In October 2024, Flowserve Corporation announced a strategic expansion of its pump service and repair center network across the Middle East and Southeast Asia, enhancing aftermarket capabilities in response to growing oil and gas and water infrastructure demand.

- In May 2024, KSB SE & Co. KGaA introduced its PumpDrive 2 Eco variable speed drive system, delivering up to 30% energy savings on centrifugal pump installations in building services and water supply applications.

Companies Covered in Industrial Pump Market

- Flowserve Corporation

- Xylem Inc.

- KSB SE & Co. KGaA

- Sulzer Ltd.

- Grundfos Holding A/S

- ITT Inc.

- Ebara Corporation

- Wilo SE

- Atlas Copco AB

- Weir Group PLC

- Gardner Denver Holdings (Ingersoll Rand)

- IDEX Corporation

- Dover Corporation

- SPX FLOW Inc.

Market Segmentation

By Pump Type

- Centrifugal

- Reciprocating

- Rotary

- Diaphragm

- Progressing Cavity

- Others

By Power Source

- Electric

- Diesel

- Solar

- Hydraulic

- Pneumatic

By Pump Orientation

- Submersible

- Surface

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Executive Summary

- Global Industrial Pump Market Snapshot

- Future Projections

- Key Market Trends

- Regional Snapshot, by Value, 2026

- Analyst Recommendations

- Market Overview

- Market Definitions and Segmentations

- Market Dynamics

- Drivers

- Restraints

- Market Opportunities

- Value Chain Analysis

- COVID-19 Impact Analysis

- Porter's Five Forces Analysis

- Impact of Russia-Ukraine Conflict

- PESTLE Analysis

- Regulatory Analysis

- Price Trend Analysis

- Current Prices and Future Projections, 2025-2033

- Price Impact Factors

- Global Industrial Pump Market Outlook, 2020 - 2033

- Global Industrial Pump Market Outlook, By Pump Type , Value (US$ Bn), 2020-2033

- Centrifugal

- Reciprocating

- Rotary

- Diaphragm

- Progressing

- Cavity

- Others

- Global Industrial Pump Market Outlook, By Power Source , Value (US$ Bn), 2020-2033

- Electric

- Diesel

- Solar

- Hydraulic

- Pneumatic

- Global Industrial Pump Market Outlook, by Pump Orientation , Value (US$ Bn), 2020-2033

- Submersible

- Surface

- Global Industrial Pump Market Outlook, by Region, Value (US$ Bn), 2020-2033

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Global Industrial Pump Market Outlook, By Pump Type , Value (US$ Bn), 2020-2033

- North America Industrial Pump Market Outlook, 2020 - 2033

- North America Industrial Pump Market Outlook, By Pump Type , Value (US$ Bn), 2020-2033

- Centrifugal

- Reciprocating

- Rotary

- Diaphragm

- Progressing

- Cavity

- Others

- North America Industrial Pump Market Outlook, By Power Source , Value (US$ Bn), 2020-2033

- Electric

- Diesel

- Solar

- Hydraulic

- Pneumatic

- North America Industrial Pump Market Outlook, by Pump Orientation , Value (US$ Bn), 2020-2033

- Submersible

- Surface

- North America Industrial Pump Market Outlook, by Country, Value (US$ Bn), 2020-2033

- U.S. Industrial Pump Market Outlook, By Pump Type , 2020-2033

- U.S. Industrial Pump Market Outlook, By Power Source , 2020-2033

- U.S. Industrial Pump Market Outlook, by Pump Orientation , 2020-2033

- Canada Industrial Pump Market Outlook, By Pump Type , 2020-2033

- Canada Industrial Pump Market Outlook, By Power Source , 2020-2033

- Canada Industrial Pump Market Outlook, by Pump Orientation , 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- North America Industrial Pump Market Outlook, By Pump Type , Value (US$ Bn), 2020-2033

- Europe Industrial Pump Market Outlook, 2020 - 2033

- Europe Industrial Pump Market Outlook, By Pump Type , Value (US$ Bn), 2020-2033

- Centrifugal

- Reciprocating

- Rotary

- Diaphragm

- Progressing

- Cavity

- Others

- Europe Industrial Pump Market Outlook, By Power Source , Value (US$ Bn), 2020-2033

- Electric

- Diesel

- Solar

- Hydraulic

- Pneumatic

- Europe Industrial Pump Market Outlook, by Pump Orientation , Value (US$ Bn), 2020-2033

- Submersible

- Surface

- Europe Industrial Pump Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Germany Industrial Pump Market Outlook, By Pump Type , 2020-2033

- Germany Industrial Pump Market Outlook, By Power Source , 2020-2033

- Germany Industrial Pump Market Outlook, by Pump Orientation , 2020-2033

- Italy Industrial Pump Market Outlook, By Pump Type , 2020-2033

- Italy Industrial Pump Market Outlook, By Power Source , 2020-2033

- Italy Industrial Pump Market Outlook, by Pump Orientation , 2020-2033

- France Industrial Pump Market Outlook, By Pump Type , 2020-2033

- France Industrial Pump Market Outlook, By Power Source , 2020-2033

- France Industrial Pump Market Outlook, by Pump Orientation , 2020-2033

- U.K. Industrial Pump Market Outlook, By Pump Type , 2020-2033

- U.K. Industrial Pump Market Outlook, By Power Source , 2020-2033

- U.K. Industrial Pump Market Outlook, by Pump Orientation , 2020-2033

- Spain Industrial Pump Market Outlook, By Pump Type , 2020-2033

- Spain Industrial Pump Market Outlook, By Power Source , 2020-2033

- Spain Industrial Pump Market Outlook, by Pump Orientation , 2020-2033

- Russia Industrial Pump Market Outlook, By Pump Type , 2020-2033

- Russia Industrial Pump Market Outlook, By Power Source , 2020-2033

- Russia Industrial Pump Market Outlook, by Pump Orientation , 2020-2033

- Rest of Europe Industrial Pump Market Outlook, By Pump Type , 2020-2033

- Rest of Europe Industrial Pump Market Outlook, By Power Source , 2020-2033

- Rest of Europe Industrial Pump Market Outlook, by Pump Orientation , 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Europe Industrial Pump Market Outlook, By Pump Type , Value (US$ Bn), 2020-2033

- Asia Pacific Industrial Pump Market Outlook, 2020 - 2033

- Asia Pacific Industrial Pump Market Outlook, By Pump Type , Value (US$ Bn), 2020-2033

- Centrifugal

- Reciprocating

- Rotary

- Diaphragm

- Progressing

- Cavity

- Others

- Asia Pacific Industrial Pump Market Outlook, By Power Source , Value (US$ Bn), 2020-2033

- Electric

- Diesel

- Solar

- Hydraulic

- Pneumatic

- Asia Pacific Industrial Pump Market Outlook, by Pump Orientation , Value (US$ Bn), 2020-2033

- Submersible

- Surface

- Asia Pacific Industrial Pump Market Outlook, by Country, Value (US$ Bn), 2020-2033

- China Industrial Pump Market Outlook, By Pump Type , 2020-2033

- China Industrial Pump Market Outlook, By Power Source , 2020-2033

- China Industrial Pump Market Outlook, by Pump Orientation , 2020-2033

- Japan Industrial Pump Market Outlook, By Pump Type , 2020-2033

- Japan Industrial Pump Market Outlook, By Power Source , 2020-2033

- Japan Industrial Pump Market Outlook, by Pump Orientation , 2020-2033

- South Korea Industrial Pump Market Outlook, By Pump Type , 2020-2033

- South Korea Industrial Pump Market Outlook, By Power Source , 2020-2033

- South Korea Industrial Pump Market Outlook, by Pump Orientation , 2020-2033

- India Industrial Pump Market Outlook, By Pump Type , 2020-2033

- India Industrial Pump Market Outlook, By Power Source , 2020-2033

- India Industrial Pump Market Outlook, by Pump Orientation , 2020-2033

- Southeast Asia Industrial Pump Market Outlook, By Pump Type , 2020-2033

- Southeast Asia Industrial Pump Market Outlook, By Power Source , 2020-2033

- Southeast Asia Industrial Pump Market Outlook, by Pump Orientation , 2020-2033

- Rest of SAO Industrial Pump Market Outlook, By Pump Type , 2020-2033

- Rest of SAO Industrial Pump Market Outlook, By Power Source , 2020-2033

- Rest of SAO Industrial Pump Market Outlook, by Pump Orientation , 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Asia Pacific Industrial Pump Market Outlook, By Pump Type , Value (US$ Bn), 2020-2033

- Latin America Industrial Pump Market Outlook, 2020 - 2033

- Latin America Industrial Pump Market Outlook, By Pump Type , Value (US$ Bn), 2020-2033

- Centrifugal

- Reciprocating

- Rotary

- Diaphragm

- Progressing

- Cavity

- Others

- Latin America Industrial Pump Market Outlook, By Power Source , Value (US$ Bn), 2020-2033

- Electric

- Diesel

- Solar

- Hydraulic

- Pneumatic

- Latin America Industrial Pump Market Outlook, by Pump Orientation , Value (US$ Bn), 2020-2033

- Submersible

- Surface

- Latin America Industrial Pump Market Outlook, by Country, Value (US$ Bn), 2020-2033

- Brazil Industrial Pump Market Outlook, By Pump Type , 2020-2033

- Brazil Industrial Pump Market Outlook, By Power Source , 2020-2033

- Brazil Industrial Pump Market Outlook, by Pump Orientation , 2020-2033

- Mexico Industrial Pump Market Outlook, By Pump Type , 2020-2033

- Mexico Industrial Pump Market Outlook, By Power Source , 2020-2033

- Mexico Industrial Pump Market Outlook, by Pump Orientation , 2020-2033

- Argentina Industrial Pump Market Outlook, By Pump Type , 2020-2033

- Argentina Industrial Pump Market Outlook, By Power Source , 2020-2033

- Argentina Industrial Pump Market Outlook, by Pump Orientation , 2020-2033

- Rest of LATAM Industrial Pump Market Outlook, By Pump Type , 2020-2033

- Rest of LATAM Industrial Pump Market Outlook, By Power Source , 2020-2033

- Rest of LATAM Industrial Pump Market Outlook, by Pump Orientation , 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Latin America Industrial Pump Market Outlook, By Pump Type , Value (US$ Bn), 2020-2033

- Middle East & Africa Industrial Pump Market Outlook, 2020 - 2033

- Middle East & Africa Industrial Pump Market Outlook, By Pump Type , Value (US$ Bn), 2020-2033

- Centrifugal

- Reciprocating

- Rotary

- Diaphragm

- Progressing

- Cavity

- Others

- Middle East & Africa Industrial Pump Market Outlook, By Power Source , Value (US$ Bn), 2020-2033

- Electric

- Diesel

- Solar

- Hydraulic

- Pneumatic

- Middle East & Africa Industrial Pump Market Outlook, by Pump Orientation , Value (US$ Bn), 2020-2033

- Submersible

- Surface

- Middle East & Africa Industrial Pump Market Outlook, by Country, Value (US$ Bn), 2020-2033

- GCC Industrial Pump Market Outlook, By Pump Type , 2020-2033

- GCC Industrial Pump Market Outlook, By Power Source , 2020-2033

- GCC Industrial Pump Market Outlook, by Pump Orientation , 2020-2033

- South Africa Industrial Pump Market Outlook, By Pump Type , 2020-2033

- South Africa Industrial Pump Market Outlook, By Power Source , 2020-2033

- South Africa Industrial Pump Market Outlook, by Pump Orientation , 2020-2033

- Egypt Industrial Pump Market Outlook, By Pump Type , 2020-2033

- Egypt Industrial Pump Market Outlook, By Power Source , 2020-2033

- Egypt Industrial Pump Market Outlook, by Pump Orientation , 2020-2033

- Nigeria Industrial Pump Market Outlook, By Pump Type , 2020-2033

- Nigeria Industrial Pump Market Outlook, By Power Source , 2020-2033

- Nigeria Industrial Pump Market Outlook, by Pump Orientation , 2020-2033

- Rest of Middle East Industrial Pump Market Outlook, By Pump Type , 2020-2033

- Rest of Middle East Industrial Pump Market Outlook, By Power Source , 2020-2033

- Rest of Middle East Industrial Pump Market Outlook, by Pump Orientation , 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Middle East & Africa Industrial Pump Market Outlook, By Pump Type , Value (US$ Bn), 2020-2033

- Competitive Landscape

- Company Vs Segment Heatmap

- Company Market Share Analysis, 2025

- Competitive Dashboard

- Company Profiles

- SABIC

- Company Overview

- Product Portfolio

- Financial Overview

- Business Strategies and Developments

- Mitsubishi Chemical Group

- Asahi Kasei Corporation

- Sumitomo Chemical

- Evonik Industries

- Solvay SA

- Polyplastics Co.,Ltd.

- Celanese Corporation

- Entegris

- DIC Corporation

- BASF

- Ensinger

- SABIC

- Appendix

- Research Methodology

- Report Assumptions

- Acronyms and Abbreviations

|

BASE YEAR |

HISTORICAL DATA |

FORECAST PERIOD |

UNITS |

|||

|

2025 |

|

2020 - 2025 |

2026 - 2033 |

Value: US$ Million |

||

|

REPORT FEATURES |

DETAILS |

|

By Pump Type Coverage |

|

|

By Power Source Coverage |

|

By Pump Orientation

|

|

|

Geographical Coverage |

|

|

Leading Companies |

|

|

Report Highlights |

Key Market Indicators, Macro-micro economic impact analysis, Technological Roadmap, Key Trends, Driver, Restraints, and Future Opportunities & Revenue Pockets, Porter’s 5 Forces Analysis, Historical Trend (2019-2024), Market Estimates and Forecast, Market Dynamics, Industry Trends, Competition Landscape, Category, Region, Country-wise Trends & Analysis, COVID-19 Impact Analysis (Demand and Supply Chain) |