Magnetic Separator Market Size, Share, and Growth Forecast 2026 – 2033

Key Market Highlights

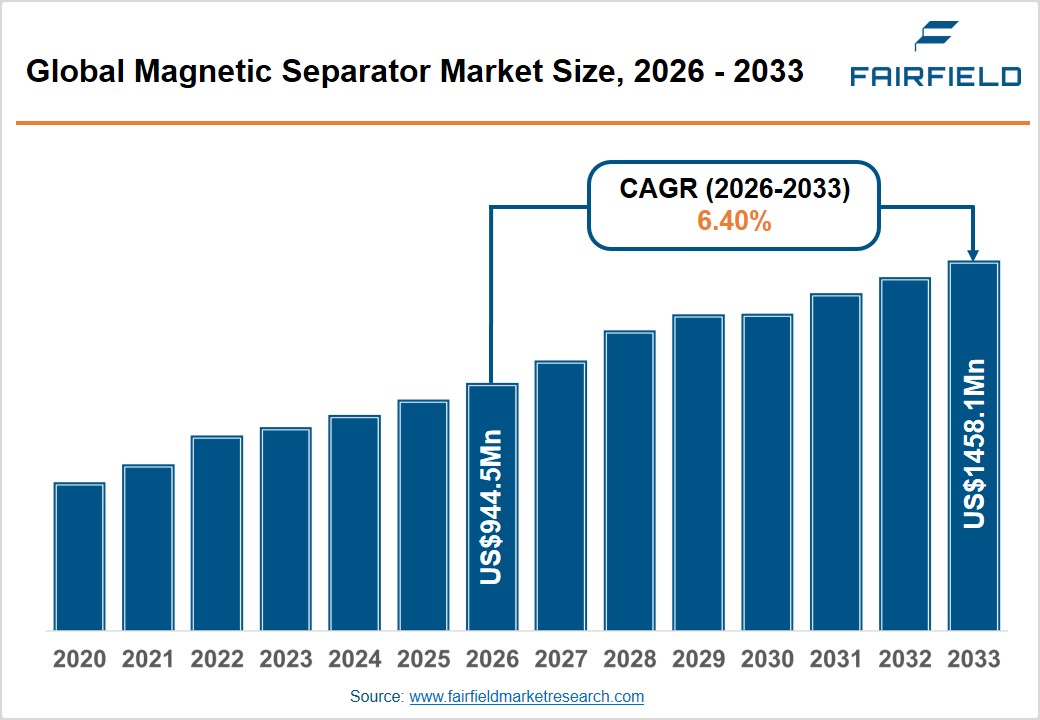

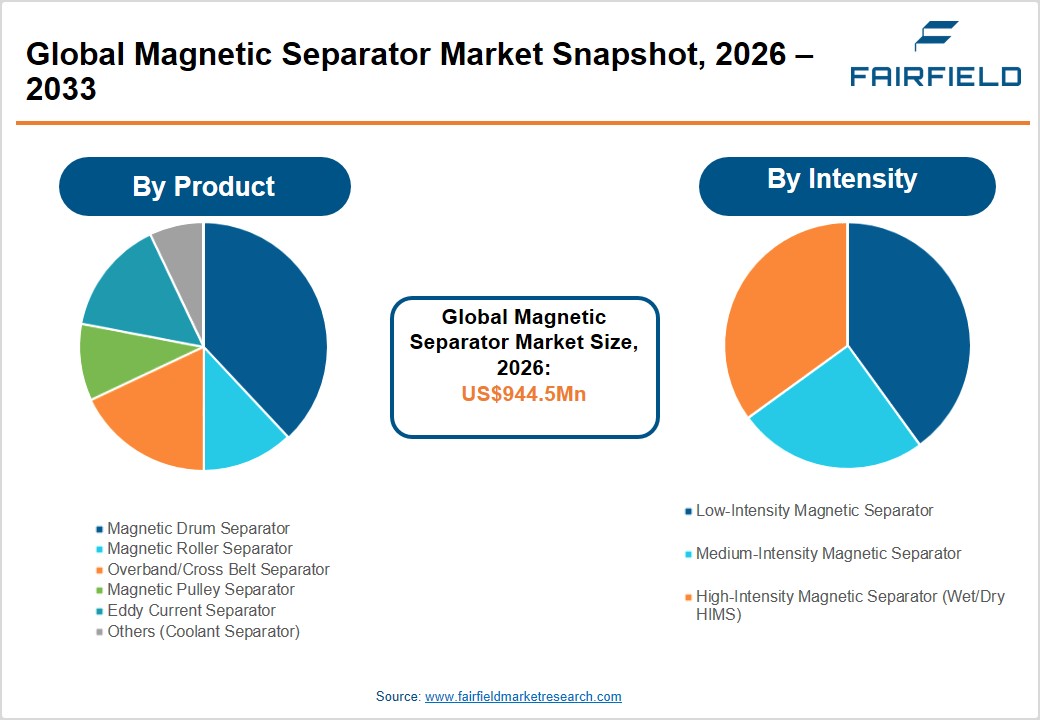

- The global Magnetic Separator Market size is likely to be valued at USD 944.5 million in 2026 and is expected to reach USD 1,458.1 million by 2033, growing at a CAGR of 6.40% during the forecast period from 2026 to 2033.

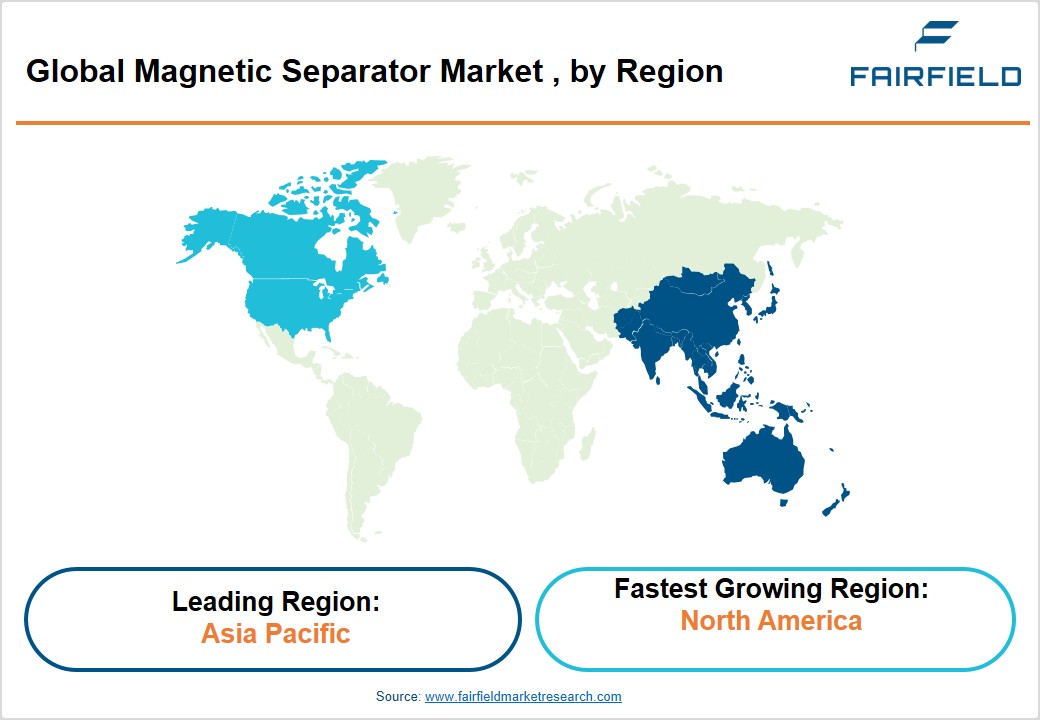

- Leading Region Market: Asia Pacific dominates with approximately 45% share in 2026 global revenue share, supported by the world's largest iron ore processing and steel manufacturing ecosystem, combined with rapidly growing e-waste recycling infrastructure and cost-competitive domestic separator manufacturers.

- Fastest Growing Region Market: North America leads regional growth, propelled by the S. Inflation Reduction Act, DOE critical mineral funding, and expanding smart magnetic separator adoption in rare earth processing and industrial metal recycling facilities.

- Dominant Product Segment: The Magnetic Drum Separator leads By Product with 30% share in 2026, driven by its high throughput capacity, wet and dry processing versatility, and widespread deployment in large-scale iron ore beneficiation globally.

- Fastest Growing Segment: High-Intensity Magnetic Separator (HIMS) is the fastest-growing intensity segment, driven by surging critical mineral extraction demand, with the IEA projecting up to 6x growth in critical mineral demand by 2040 under net-zero transition scenarios.

- Key Market Opportunity – Smart IIoT-Enabled Magnetic Separators: Integration of Industrial IoT sensors and AI-assisted automation into separator systems creates a premium product opportunity, with digital transformation projected to reduce operational costs by 15–20% in automated mineral processing plants (World Economic Forum).

Market Dynamics

Market Growth Drivers

Surging Mineral Processing Demand Driven by Global Iron Ore and Critical Mineral Extraction

The global mining sector remains the most dominant end-use driver for magnetic separators. Iron ore production reaches massive volumes annually, and a significant share requires wet low-intensity magnetic drum separators (LIMS) to boost iron content before smelting. The extraction of critical minerals including magnetite, ilmenite, chromite, and manganese essential for clean energy technologies and steel manufacturing, further amplifies demand for both wet and dry high-intensity magnetic separators (HIMS). Tightening purity standards in global steel production, combined with surging mineral demand for electric vehicle (EV) batteries and wind turbine components, reinforce magnetic separation as a non-negotiable step in modern ore beneficiation plants across both established and emerging mining economies.

Expanding Global E-Waste and Metal Recycling Industry Mandated by Regulatory Frameworks

The recycling sector represents one of the fastest-growing demand channels for magnetic separators, particularly eddy current separators and overband/crossbelt magnetic separators. According to the Global E-waste Monitor 2024 published by the United Nations Institute for Training and Research (UNITAR), global e-waste generation reached a record 62 million metric tonnes in 2023, projected to rise to 82 million metric tonnes by 2030. Municipal solid waste (MSW) facilities and automotive shredder residue (ASR) processing plants are increasingly deploying magnetic separation units to extract ferrous and non-ferrous metals before downstream processing. Extended producer responsibility (EPR) regulations enforced through the Basel Convention and national waste legislation are compelling higher metal recovery rates, directly driving capital expenditure in magnetic separation infrastructure at recycling facilities globally.

Market Restraints

High Capital and Installation Costs of High-Intensity and Superconducting Magnetic Separators

Despite robust demand, the elevated procurement and installation costs of high-intensity magnetic separators (HIMS) particularly superconducting or rare earth permanent magnet-based systems represent a significant adoption barrier for small and medium-sized mining enterprises. A single superconducting magnetic separator can cost upwards of US$ 500,000 to US$ 2 million, depending on capacity and configuration. The International Finance Corporation (IFC) has noted persistent capital access challenges for mid-tier miners in developing economies, limiting their ability to upgrade separation infrastructure, extending replacement cycles for aging low-intensity equipment, and slowing penetration of technologically advanced separator systems in price-sensitive markets.

Operational Complexity and Frequent Maintenance Requirements in Wet Processing Environments

Wet high-intensity magnetic separators (WHIMS) are prone to matrix clogging, slurry leakage, and magnetic matrix degradation when processing fine, abrasive mineral slurries. Research published in the Journal of Minerals Engineering indicates that matrix clogging in WHIMS units operating on oxidized iron ore can reduce throughput efficiency by 20–35% without proper flushing intervals. Kaolin clay processing and coal washery operations frequently encounter unplanned downtime from particle buildup within separator matrices. These challenges increase total cost of ownership (TCO) and demand skilled maintenance personnel a resource that remains scarce in remote mining regions restraining broader market penetration.

Market Opportunities

Rare Earth Element (REE) Processing Boom Fueled by Energy Transition and Government Policy Support

The global clean energy transition and electric vehicle (EV) industry surge have triggered unprecedented demand for rare earth elements (REEs) including neodymium, dysprosium, and praseodymium all of which require specialized high-gradient magnetic separation (HGMS) and dry high-intensity magnetic separation during ore beneficiation. The International Energy Agency (IEA)'s Critical Minerals Outlook 2024 projects REE demand to increase by three to seven times by 2040 under net-zero scenarios. Policy mandates including the European Union's Critical Raw Materials Act (2024) are accelerating domestic REE supply chain investments across industrial economies. Leading separation equipment manufacturers such as SLon Magnetic Separator Ltd. have developed vertical ring pulsating HGMS units specifically for bastnäsite and monazite ore processing, highlighting a clear commercialization pathway for advanced magnetic separation equipment in this rapidly expanding critical minerals segment.

Industrial Automation and Smart Magnetic Separator Adoption for Predictive Maintenance and Precision Separation

The accelerating deployment of Industry 4.0 technologies across mining, metal recycling, and chemical processing is creating a high-value growth frontier for smart magnetic separator systems integrated with embedded sensors, IoT connectivity, and real-time condition monitoring capabilities. According to the International Federation of Robotics (IFR), global industrial robot installations reached a record 553,052 units in 2022, reflecting the rapid factory automation pace that demands precision material separation and zero-tolerance contamination control. Smart magnetic separators equipped with pressure, temperature, and magnetic field intensity sensors enable predictive maintenance by transmitting live performance data to centralized SCADA or CMMS platforms, helping operators detect separator degradation before failure reducing unplanned downtime costs estimated at US$ 50 billion annually across global process industries per Emerson Automation Solutions. Companies such as STEINERT GmbH and Eriez Manufacturing Co. are already commercializing AI-assisted and sensor-integrated separation systems, enabling manufacturers to command significantly higher margins through premium smart product lines and long-term service contracts.

Segmental Insights

By Product Analysis

The Magnetic Drum Separator segment holds the leading position in the By Product category, commanding approximately 30%share in 2026. Magnetic drum separators are among the most widely deployed separation technologies in mineral processing and recycling due to their high throughput capacity, continuous operation capability, and adaptability to both wet and dry processing conditions. In the iron ore mining sector, wet low-intensity magnetic drum separators (LIMS) are indispensable for processing magnetite ores at large-scale beneficiation plants. The USGS Mineral Commodity Summaries 2023 confirm that magnetite remains a dominant iron ore type globally, reinforcing consistent procurement demand for drum separators. Their robust design and lower maintenance requirements compared to matrix-type separators further consolidate their dominant market position in high-volume industrial applications.

By Intensity Analysis

The High-Intensity Magnetic Separator (HIMS) segment leads the By Intensity category, accounting for an estimated 42%share in 2026. HIMS encompassing both Wet HIMS (WHIMS) and Dry HIMS (DHIMS) are critical for processing weakly magnetic minerals such as hematite, ilmenite, chromite, and rare earth ores that cannot be recovered using low-intensity equipment. The growing importance of critical mineral extraction for clean energy applications has significantly amplified HIMS demand. According to the IEA Critical Minerals Outlook 2024, global demand for minerals including lithium, cobalt, and rare earths could grow by up to 6x by 2040, directly expanding the addressable opportunity for HIMS equipment across mining and advanced material processing applications worldwide.

By Industry Analysis

The Mining industry segment dominates the By Industry category, representing approximately 62% share in 2026. Mining operations spanning iron ore, coal, mineral sands, rare earth ores, and industrial minerals rely on a broad portfolio of magnetic separation equipment across multiple processing stages, from primary concentration to final purification. The World Steel Association reports that global crude steel production exceeded 1.87 billion metric tons in 2023, sustaining robust upstream demand for iron ore beneficiation using magnetic drum and roller separators. Furthermore, the accelerating extraction of battery-critical minerals such as lithium, cobalt, and nickel is expanding the scope of magnetic separation applications within the broader mining value chain, reinforcing this segment's dominant and structurally resilient revenue contribution.

Regional Insights

North America Magnetic Separator Market Trends

North America represents the fastest-growing regional market for magnetic separators, driven by a convergence of regulatory support, critical mineral investment programs, and advanced recycling infrastructure. The U.S. Inflation Reduction Act (IRA, 2022) and subsequent U.S. Department of Energy (DOE) critical mineral funding initiatives have catalyzed domestic investments in rare earth and battery mineral processing directly amplifying demand for high-intensity and high-gradient magnetic separation systems. The region's established mining sector, encompassing iron ore operations in the Great Lakes region and mineral sands processing along the Atlantic seaboard, continues to generate steady procurement of magnetic drum and roller separators.

The recycling sector further reinforces North America's growth trajectory. The U.S. Environmental Protection Agency (EPA) reported a national metal recycling rate of 34.1% in its latest municipal solid waste data, with active investment in new material recovery facilities (MRFs) deploying eddy current and overband magnetic separators. Technology innovation from leading regional manufacturers including Eriez Manufacturing Co. and Bunting Magnetics Co. sustains the region's strong innovation ecosystem and export competitiveness in magnetic separation technology.

Europe Magnetic Separator Market Trends

Europe maintains a technologically mature and regulatory-driven magnetic separator market, anchored by stringent environmental legislation and a strong industrial base in recycling and mineral processing. The European Union's Circular Economy Action Plan (CEAP) and the Critical Raw Materials Act (2024) compel industries across the region's 27 member states to enhance metal recovery efficiencies, driving procurement of advanced eddy current, overband, and high-intensity separator systems. Industrially advanced economies in Western and Central Europe account for the bulk of recycling facility investments incorporating magnetic separation equipment, with Germany's extensive automotive and steel scrap recycling sector being a particularly significant contributor.

Regional manufacturers STEINERT GmbH (Cologne), Sesotec GmbH (Bavaria), and Goudsmit Magnetics Group (Netherlands) are globally recognized technology leaders reinforcing Europe's competitive positioning. The EU Waste Framework Directive mandates member states achieve minimum 70% recycling rates for construction and demolition waste a regulatory target that continues to drive equipment investment in magnetic separation across the region's waste management and scrap metal processing sectors, maintaining sustained procurement momentum through the forecast period.

Asia Pacific Magnetic Separator Market Trends

Asia Pacific commands the leading share of approximately 45% share in 2026, driven by the region's unparalleled scale of mining activity, steel manufacturing, and rapidly expanding recycling infrastructure. Asia Pacific dominates global crude steel output, generating enormous continuous demand for wet low-intensity magnetic drum separators in iron ore beneficiation plants. The growing extraction of mineral sands, rare earths, and industrial minerals across the region further fuels demand for high-intensity separation systems, reinforcing Asia Pacific's structurally dominant revenue contribution to the global magnetic separator market.

The region's e-waste challenge is equally a significant demand driver: the Global E-waste Monitor 2024 identifies Asia as the world's largest generator of e-waste, with volumes increasing year-on-year, driving investment in magnetic separation-equipped MRFs. Government-led initiatives promoting domestic rare earth processing and EV supply chain localization are accelerating adoption of advanced separator technologies. Regional manufacturers including LONGi Magnet Co., Ltd., Shandong Huate Magnet Technology Co., Ltd., and SLon Magnetic Separator Ltd. maintain cost manufacturing advantages, serving both domestic markets and global export demand effectively.

Competitive Landscape

The global magnetic separator market exhibits a moderately fragmented competitive structure, with a few globally dominant players coexisting alongside a large base of regional and niche manufacturers. Market leaders including Eriez Manufacturing Co., Metso Corporation, STEINERT GmbH, and LONGi Magnet Co., Ltd. differentiate through proprietary magnet technologies, integrated service models, and digital monitoring capabilities. Product innovation particularly in rare earth permanent magnet-based separators and IIoT-enabled smart separator platforms remains the primary competitive differentiator. Companies are increasingly adopting long-term service and maintenance contract (SMC) business models to secure recurring revenues. Strategic capacity expansions, joint ventures with regional mining operators, and R&D investments in sensor-integrated and AI-assisted separation systems define the dominant growth strategies among leading participants.

Key Market Developments

- March 2025: STEINERT GmbH unveiled its next-generation sensor-based metal sorting and magnetic separation system at IFAT Munich 2025, integrating real-time NIR and AI-assisted detection for improved non-ferrous metal recovery in industrial recycling applications.

- November 2024: Eriez Manufacturing Co. announced an expanded Wet High-Intensity Magnetic Separator (WHIMS) product line targeting rare earth and mineral sands processing, specifically designed for critical mineral beneficiation projects across North America and Australia.

- August 2024: Metso Corporation secured a major equipment supply contract for high-intensity magnetic separators for a large-scale iron ore beneficiation project in Brazil, reinforcing its presence in the Latin American mining equipment market.

Companies Covered in Magnetic Separator Market

- Eriez Manufacturing Co.

- Metso Corporation

- LONGi Magnet Co., Ltd.

- Nippon Magnetics Inc.

- STEINERT GmbH

- Bunting Magnetics Co.

- Goudsmit Magnetics Group

- Kanetec Co., Ltd.

- Multotec Pty Ltd.

- Shandong Huate Magnet Technology Co., Ltd.

- SLon Magnetic Separator Ltd.

- Sesotec GmbH

- Douglas Manufacturing Co., Inc.

- Permanent Magnets Ltd.

- A & A Magnetics, Inc.

- Master Magnets Ltd.

- Sollau s.r.o.

- Magnetic Products Inc. (MPI)

- IFE Aufbereitungstechnik GmbH

Market Segmentation

By Product

- Magnetic Drum Separator

- Magnetic Roller Separator

- Overband / Cross Belt Separator

- Magnetic Pulley Separator

- Eddy Current Separator

- Others (Coolant Separator)

By Intensity

- High-Intensity Magnetic Separator (HIMS) – Wet HIMS (WHIMS), Dry HIMS (DHIMS)

- Medium-Intensity Magnetic Separator

- Low-Intensity Magnetic Separator (LIMS)

By Industry

- Mining

- Recycling

By Regions

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Executive Summary

- Global Magnetic Separator Market Snapshot

- Future Projections

- Key Market Trends

- Regional Snapshot, by Value, 2026

- Analyst Recommendations

- Market Overview

- Market Definitions and Segmentations

- Market Dynamics

- Drivers

- Restraints

- Market Opportunities

- Value Chain Analysis

- COVID-19 Impact Analysis

- Porter's Five Forces Analysis

- Impact of Russia-Ukraine Conflict

- PESTLE Analysis

- Regulatory Analysis

- Price Trend Analysis

- Current Prices and Future Projections, 2025-2033

- Price Impact Factors

- Global Magnetic Separator Market Outlook, 2020 - 2033

- Global Magnetic Separator Market Outlook, by Product, Value (US$ Mn), 2020-2033

- Magnetic Drum Separator

- Magnetic Roller Separator

- Over band/Cross Belt Separator

- Magnetic Pulley Separator

- Eddy Current Separator

- Others (Coolant Separator)

- Global Magnetic Separator Market Outlook, by Intensity, Value (US$ Mn), 2020-2033

- High-Intensity Magnetic Separator

- Wet HIMS

- Dry HIMS

- Medium-Intensity Magnetic Separator

- Low-Intensity Magnetic Separator

- High-Intensity Magnetic Separator

- Global Magnetic Separator Market Outlook, by Industry, Value (US$ Mn), 2020-2033

- Mining

- Recycling

- Global Magnetic Separator Market Outlook, by Region, Value (US$ Mn), 2020-2033

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

- Global Magnetic Separator Market Outlook, by Product, Value (US$ Mn), 2020-2033

- North America Magnetic Separator Market Outlook, 2020 - 2033

- North America Magnetic Separator Market Outlook, by Product, Value (US$ Mn), 2020-2033

- Magnetic Drum Separator

- Magnetic Roller Separator

- Over band/Cross Belt Separator

- Magnetic Pulley Separator

- Eddy Current Separator

- Others (Coolant Separator)

- North America Magnetic Separator Market Outlook, by Intensity, Value (US$ Mn), 2020-2033

- High-Intensity Magnetic Separator

- Wet HIMS

- Dry HIMS

- Medium-Intensity Magnetic Separator

- Low-Intensity Magnetic Separator

- High-Intensity Magnetic Separator

- North America Magnetic Separator Market Outlook, by Industry, Value (US$ Mn), 2020-2033

- Mining

- Recycling

- North America Magnetic Separator Market Outlook, by Country, Value (US$ Mn), 2020-2033

- U.S. Magnetic Separator Market Outlook, by Product, 2020-2033

- U.S. Magnetic Separator Market Outlook, by Intensity, 2020-2033

- U.S. Magnetic Separator Market Outlook, by Industry, 2020-2033

- Canada Magnetic Separator Market Outlook, by Product, 2020-2033

- Canada Magnetic Separator Market Outlook, by Intensity, 2020-2033

- Canada Magnetic Separator Market Outlook, by Industry, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- North America Magnetic Separator Market Outlook, by Product, Value (US$ Mn), 2020-2033

- Europe Magnetic Separator Market Outlook, 2020 - 2033

- Europe Magnetic Separator Market Outlook, by Product, Value (US$ Mn), 2020-2033

- Magnetic Drum Separator

- Magnetic Roller Separator

- Over band/Cross Belt Separator

- Magnetic Pulley Separator

- Eddy Current Separator

- Others (Coolant Separator)

- Europe Magnetic Separator Market Outlook, by Intensity, Value (US$ Mn), 2020-2033

- High-Intensity Magnetic Separator

- Wet HIMS

- Dry HIMS

- Medium-Intensity Magnetic Separator

- Low-Intensity Magnetic Separator

- High-Intensity Magnetic Separator

- Europe Magnetic Separator Market Outlook, by Industry, Value (US$ Mn), 2020-2033

- Mining

- Recycling

- Europe Magnetic Separator Market Outlook, by Country, Value (US$ Mn), 2020-2033

- Germany Magnetic Separator Market Outlook, by Product, 2020-2033

- Germany Magnetic Separator Market Outlook, by Intensity, 2020-2033

- Germany Magnetic Separator Market Outlook, by Industry, 2020-2033

- Italy Magnetic Separator Market Outlook, by Product, 2020-2033

- Italy Magnetic Separator Market Outlook, by Intensity, 2020-2033

- Italy Magnetic Separator Market Outlook, by Industry, 2020-2033

- France Magnetic Separator Market Outlook, by Product, 2020-2033

- France Magnetic Separator Market Outlook, by Intensity, 2020-2033

- France Magnetic Separator Market Outlook, by Industry, 2020-2033

- U.K. Magnetic Separator Market Outlook, by Product, 2020-2033

- U.K. Magnetic Separator Market Outlook, by Intensity, 2020-2033

- U.K. Magnetic Separator Market Outlook, by Industry, 2020-2033

- Spain Magnetic Separator Market Outlook, by Product, 2020-2033

- Spain Magnetic Separator Market Outlook, by Intensity, 2020-2033

- Spain Magnetic Separator Market Outlook, by Industry, 2020-2033

- Russia Magnetic Separator Market Outlook, by Product, 2020-2033

- Russia Magnetic Separator Market Outlook, by Intensity, 2020-2033

- Russia Magnetic Separator Market Outlook, by Industry, 2020-2033

- Rest of Europe Magnetic Separator Market Outlook, by Product, 2020-2033

- Rest of Europe Magnetic Separator Market Outlook, by Intensity, 2020-2033

- Rest of Europe Magnetic Separator Market Outlook, by Industry, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Europe Magnetic Separator Market Outlook, by Product, Value (US$ Mn), 2020-2033

- Asia Pacific Magnetic Separator Market Outlook, 2020 - 2033

- Asia Pacific Magnetic Separator Market Outlook, by Product, Value (US$ Mn), 2020-2033

- Magnetic Drum Separator

- Magnetic Roller Separator

- Over band/Cross Belt Separator

- Magnetic Pulley Separator

- Eddy Current Separator

- Others (Coolant Separator)

- Asia Pacific Magnetic Separator Market Outlook, by Intensity, Value (US$ Mn), 2020-2033

- High-Intensity Magnetic Separator

- Wet HIMS

- Dry HIMS

- Medium-Intensity Magnetic Separator

- Low-Intensity Magnetic Separator

- High-Intensity Magnetic Separator

- Asia Pacific Magnetic Separator Market Outlook, by Industry, Value (US$ Mn), 2020-2033

- Mining

- Recycling

- Asia Pacific Magnetic Separator Market Outlook, by Country, Value (US$ Mn), 2020-2033

- China Magnetic Separator Market Outlook, by Product, 2020-2033

- China Magnetic Separator Market Outlook, by Intensity, 2020-2033

- China Magnetic Separator Market Outlook, by Industry, 2020-2033

- Japan Magnetic Separator Market Outlook, by Product, 2020-2033

- Japan Magnetic Separator Market Outlook, by Intensity, 2020-2033

- Japan Magnetic Separator Market Outlook, by Industry, 2020-2033

- South Korea Magnetic Separator Market Outlook, by Product, 2020-2033

- South Korea Magnetic Separator Market Outlook, by Intensity, 2020-2033

- South Korea Magnetic Separator Market Outlook, by Industry, 2020-2033

- India Magnetic Separator Market Outlook, by Product, 2020-2033

- India Magnetic Separator Market Outlook, by Intensity, 2020-2033

- India Magnetic Separator Market Outlook, by Industry, 2020-2033

- Southeast Asia Magnetic Separator Market Outlook, by Product, 2020-2033

- Southeast Asia Magnetic Separator Market Outlook, by Intensity, 2020-2033

- Southeast Asia Magnetic Separator Market Outlook, by Industry, 2020-2033

- Rest of SAO Magnetic Separator Market Outlook, by Product, 2020-2033

- Rest of SAO Magnetic Separator Market Outlook, by Intensity, 2020-2033

- Rest of SAO Magnetic Separator Market Outlook, by Industry, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Asia Pacific Magnetic Separator Market Outlook, by Product, Value (US$ Mn), 2020-2033

- Latin America Magnetic Separator Market Outlook, 2020 - 2033

- Latin America Magnetic Separator Market Outlook, by Product, Value (US$ Mn), 2020-2033

- Magnetic Drum Separator

- Magnetic Roller Separator

- Over band/Cross Belt Separator

- Magnetic Pulley Separator

- Eddy Current Separator

- Others (Coolant Separator)

- Latin America Magnetic Separator Market Outlook, by Intensity, Value (US$ Mn), 2020-2033

- High-Intensity Magnetic Separator

- Wet HIMS

- Dry HIMS

- Medium-Intensity Magnetic Separator

- Low-Intensity Magnetic Separator

- High-Intensity Magnetic Separator

- Latin America Magnetic Separator Market Outlook, by Industry, Value (US$ Mn), 2020-2033

- Mining

- Recycling

- Latin America Magnetic Separator Market Outlook, by Country, Value (US$ Mn), 2020-2033

- Brazil Magnetic Separator Market Outlook, by Product, 2020-2033

- Brazil Magnetic Separator Market Outlook, by Intensity, 2020-2033

- Brazil Magnetic Separator Market Outlook, by Industry, 2020-2033

- Mexico Magnetic Separator Market Outlook, by Product, 2020-2033

- Mexico Magnetic Separator Market Outlook, by Intensity, 2020-2033

- Mexico Magnetic Separator Market Outlook, by Industry, 2020-2033

- Argentina Magnetic Separator Market Outlook, by Product, 2020-2033

- Argentina Magnetic Separator Market Outlook, by Intensity, 2020-2033

- Argentina Magnetic Separator Market Outlook, by Industry, 2020-2033

- Rest of LATAM Magnetic Separator Market Outlook, by Product, 2020-2033

- Rest of LATAM Magnetic Separator Market Outlook, by Intensity, 2020-2033

- Rest of LATAM Magnetic Separator Market Outlook, by Industry, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Latin America Magnetic Separator Market Outlook, by Product, Value (US$ Mn), 2020-2033

- Middle East & Africa Magnetic Separator Market Outlook, 2020 - 2033

- Middle East & Africa Magnetic Separator Market Outlook, by Product, Value (US$ Mn), 2020-2033

- Magnetic Drum Separator

- Magnetic Roller Separator

- Over band/Cross Belt Separator

- Magnetic Pulley Separator

- Eddy Current Separator

- Others (Coolant Separator)

- Middle East & Africa Magnetic Separator Market Outlook, by Intensity, Value (US$ Mn), 2020-2033

- High-Intensity Magnetic Separator

- Wet HIMS

- Dry HIMS

- Medium-Intensity Magnetic Separator

- Low-Intensity Magnetic Separator

- High-Intensity Magnetic Separator

- Middle East & Africa Magnetic Separator Market Outlook, by Industry, Value (US$ Mn), 2020-2033

- Mining

- Recycling

- Middle East & Africa Magnetic Separator Market Outlook, by Country, Value (US$ Mn), 2020-2033

- GCC Magnetic Separator Market Outlook, by Product, 2020-2033

- GCC Magnetic Separator Market Outlook, by Intensity, 2020-2033

- GCC Magnetic Separator Market Outlook, by Industry, 2020-2033

- South Africa Magnetic Separator Market Outlook, by Product, 2020-2033

- South Africa Magnetic Separator Market Outlook, by Intensity, 2020-2033

- South Africa Magnetic Separator Market Outlook, by Industry, 2020-2033

- Egypt Magnetic Separator Market Outlook, by Product, 2020-2033

- Egypt Magnetic Separator Market Outlook, by Intensity, 2020-2033

- Egypt Magnetic Separator Market Outlook, by Industry, 2020-2033

- Nigeria Magnetic Separator Market Outlook, by Product, 2020-2033

- Nigeria Magnetic Separator Market Outlook, by Intensity, 2020-2033

- Nigeria Magnetic Separator Market Outlook, by Industry, 2020-2033

- Rest of Middle East Magnetic Separator Market Outlook, by Product, 2020-2033

- Rest of Middle East Magnetic Separator Market Outlook, by Intensity, 2020-2033

- Rest of Middle East Magnetic Separator Market Outlook, by Industry, 2020-2033

- BPS Analysis/Market Attractiveness Analysis

- Middle East & Africa Magnetic Separator Market Outlook, by Product, Value (US$ Mn), 2020-2033

- Competitive Landscape

- Company Vs Segment Heatmap

- Company Market Share Analysis, 2025

- Competitive Dashboard

- Company Profiles

- Eriez Manufacturing Co.

- Company Overview

- Product Portfolio

- Financial Overview

- Business Strategies and Developments

- Metso Corporation

- LONGi Magnet Co., Ltd.

- Nippon Magnetics Inc.

- STEINERT GmbH

- Bunting Magnetics Co.

- Goudsmit Magnetics Group

- Kanetec Co., Ltd.

- Multotec Pty Ltd.

- Shandong Huate Magnet Technology Co., Ltd.

- Eriez Manufacturing Co.

- Appendix

- Research Methodology

- Report Assumptions

- Acronyms and Abbreviations

|

BASE YEAR |

HISTORICAL DATA |

FORECAST PERIOD |

UNITS |

|||

|

2025 |

|

2020 - 2025 |

2026 - 2033 |

Value: US$ Million |

||

|

REPORT FEATURES |

DETAILS |

By Product |

|

By Intensity |

|

By Industry |

|

|

Geographical Coverage |

|

|

Leading Companies |

|

|

Report Highlights |

Key Market Indicators, Macro-micro economic impact analysis, Technological Roadmap, Key Trends, Driver, Restraints, and Future Opportunities & Revenue Pockets, Porter’s 5 Forces Analysis, Historical Trend (2019-2024), Market Estimates and Forecast, Market Dynamics, Industry Trends, Competition Landscape, Category, Region, Country-wise Trends & Analysis, COVID-19 Impact Analysis (Demand and Supply Chain) |